Summary of key points: -

- US Federal Reserve on track for interest rate cuts

- RBNZ shift their monetary track, once again!

- RBA wander off their monetary track

US Federal Reserve on track for interest rate cuts

Whilst investors, borrowers, financial market participants and economic commentators may be wondering which track the RBNZ will take next with their management of monetary policy, the policy path ahead is looking considerably more certain in the US of A.

A negative print for US CPI inflation in the month of June (-0.10% change of the month) has re-ignited expectations that the Fed will cut the Fed Funds interest rate three times 0.25% this year. The current restrictive 5.50% interest rate level is no longer justified with the annual inflation rate more rapidly approaching the 2.00% target than what most expected. Further confirmation of the re-acceleration to a lower inflation track will come with the Fed-preferred PCE Price Index inflation result for June on 26 July.

The markets have already voted with their feet as the sentiment shifts back to the three 0.25% cuts before the end of 2024 (the original “dot-plot” interest rate forecasts from the members of the Fed in December 2023 when they made the initial pivot on monetary policy.

- US 10-year Treasury Bond yields have decreased from 4.50% two weeks ago to 4.18% today (the lowest levels since March).

- US 2-year Treasury Bond yields have decreased from 4.80% two weeks ago to 4.45% today (the lowest levels since February).

- The US dollar Index (Dixy) has depreciated from a high of 105.75 at the end of June to 103.77 today (the lowest levels since March).

Further falls in US market interest rates over coming months are set to weaken the US dollar a whole lot more, sending the Australian dollar and NZ dollar exchange rates to the USD northwards from current levels of 0.6790 and 0.6120 respectively. A return of the USD Dixy Index to 100 would see the NZD/USD exchange rate lift to above 0.6300.

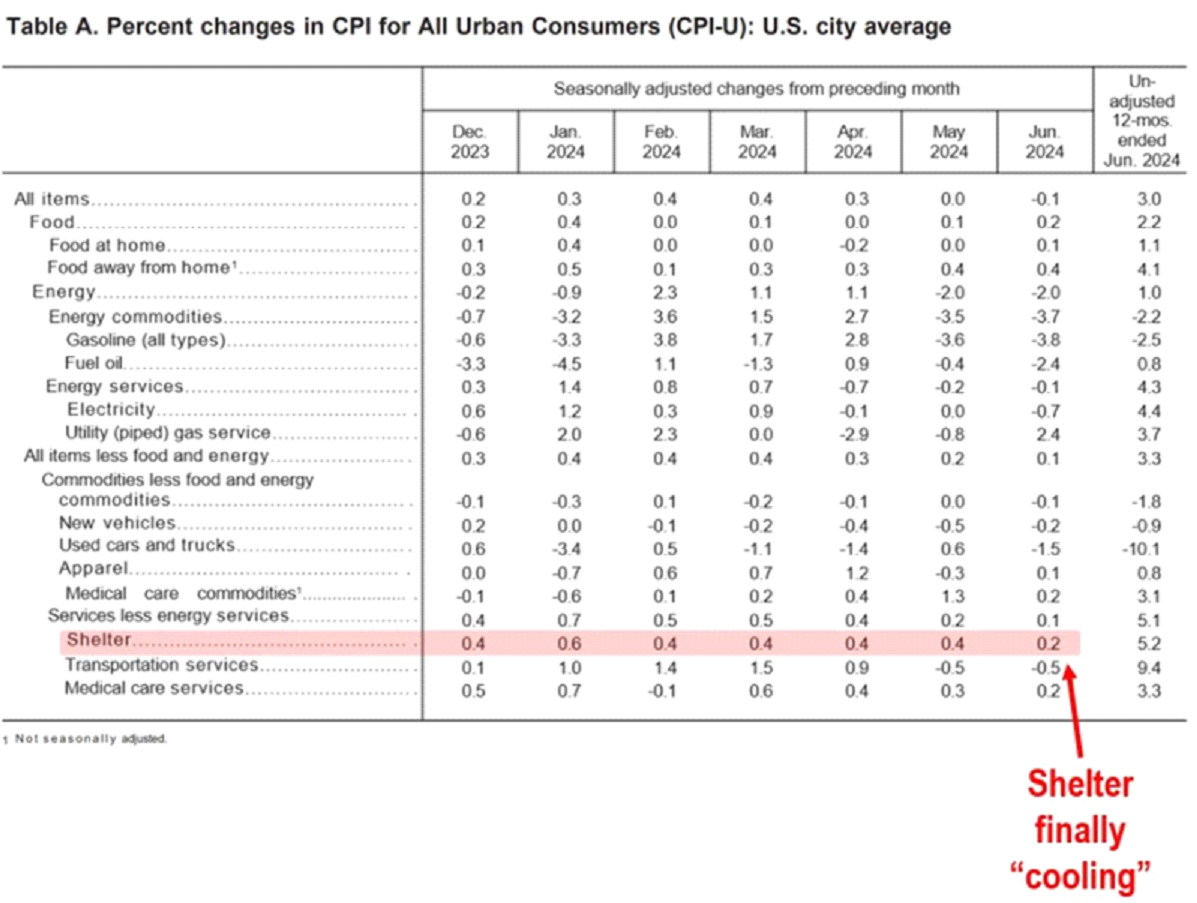

The US June inflation outcome confirms that the “bump” upwards in inflation over the period January to March is now well and truly behind the markets. The table below evidences the component parts of the CPI inflation index that recorded elevated increases in the January to March period, however they have now all reversed back to very low monthly increases. Notably, the troublesome and disruptive “Shelter” CPI component for housing costs has dropped to much lower +0.20% increase in June after consistent +0.40% and +0.60% monthly increases over previous months. The shelter price measure is notoriously lagged and inaccurate, not reflecting current market rent changes at all.

Looking ahead, the Fed’s next meeting is 31 July and whilst there is not yet a groundswell of opinion for the first interest rate cut to come at that meeting, there could be a sufficient change in the wording of the Fed’s statement to propel market interest rates lower and the USD value lower, well ahead of the likely first cut at the 18 September meeting. A continuation of weaker retail sales and house construction data (for June) next week will keep the current market momentum going for lower interest rates and a lower USD.

US price increase for clothing (apparel), transportation and medical care, in particular, have dropped away in May and June following the higher annual price adjustments made in January to March.

The US dollar has depreciated against all the major currencies over this last week. “Stop-loss” USD sell orders have been triggered at key resistance levels of $1.0850 in the EUR/USD (now $1.0910), $1.2850 in the GBP/USD (now $1.3000) and 0.6750 in the AUD/USD (now 0. 6790). There remain very large amounts of “long” USD speculative positions put in place over recent years around the globe that are just only starting to be unwound i.e. more USD selling to come.

Local New Zealand exporters in AUD’s would have heard the repeated “ping, ping, ping” of their FX orders for hedging being struck from 0.9100 down to 0.9000 in the NZD/USD cross-rate last Wednesday, following the surprise “dovish” RBNZ OCR review statement.

RBNZ shift their monetary track, once again!

According to local media reports, it is now all cut and dried that the RBNZ will cut interest rates over coming months as they have won the battle against inflation and all borrowers can exert a combined sigh of relief.

Last Wednesday’s surprisingly “dovish” OCR review statement from the RBNZ was polar opposite in its message about the economy, inflation and interest rates, compared to the clear “hawkish” message in their 22 May Monetary Policy Statement just six weeks ago, that it cannot go unchallenged without a few inconvenient questions: -

Question 1: Has the RBNZ been consistent in its outlook?

To an outside observer, the only consistent message coming from the RBNZ is their totally inconsistent messaging! A recap back on the last five statements from the RBNZ on monetary policy since November 2023 have been in chronological order - hawkish, dovish, balanced, hawkish and dovish. Such flip-flopping and lurching from one side to the other is not what you would expect from a central bank managing monetary policy 12 to 18 months ahead. Off course, whether a RBNZ statement is labelled hawkish or dovish comes down to how the markets and economic commentators interpret the message. However, the RBNZ should never be surprised as to how the markets interpret or react to their words, it is their job to know in advance how the markets will react. It is the market’s reaction that sets the monetary conditions in the economy through interest rate and exchange rate changes.

Question 2: So, what has changed in the last six weeks?

Such was the extreme change in tone for the outlook on inflation in last week’s statement, it felt like it was written by an entirely different committee to the 22 May Monetary Policy Statement. The May message was that interest rates could not be lowered until well into 2025 as non-tradeable/domestic inflation was still far too high and it would take time to pull that inflation down. Last week’s message was that demand had weakened in the economy; capacity had freed up and, in that environment the annual inflation rate would be below 3.00% by year-end. What changed over the course of six weeks is hard to fathom. What we do know is that retail, housing and manufacturing activity levels have slowed dramatically. If inflation was coming from the demand side of the economy the RBNZ would be correct to expect contracting GDP to automatically lead to lower inflation. Unfortunately, the inconvenient truth is that New Zealand’s high non-tradeable/domestic inflation problem comes from the supply side of the economy. That situation has certainly not changed over the last six weeks.

Question 3: Why do the banks want lower interest rates?

Some of the local banks were calling for the RBNZ to cut interest rates before the end of the year prior to last week’s U-turn. Now they are all confidently predicting and expecting three cuts of 0.25% each before December. The money markets are pricing-in this change into the forward interest rate curve as well. The banks have no interest in solving New Zealand’s non-tradeable/domestic inflation problem. Their interest is their own profitability, and their profits decline sharply when their new mortgage lending is less than the rate of their borrowers repaying mortgage debt. That has been the situation over the last six to 12 months. The banks desperately need lower interest rates so that the mortgage lending market picks up and the New Zealand economy returns to the “fool’s paradise” of creating “wealth” by buying and selling houses with each other! – Yeah, right!

Question 4: What would cause interest rates not to be cut over coming months?

Outside of external events or factors, the June and September quarters’ inflation increases would need to be well above current RBNZ CPI forecasts for the interest rate cuts to be pushed back to early 2025. The RBNZ are forecasting the June quarter inflation increase to be +0.60% (released on Wednesday) and the September quarter to be +1.30% (includes the astronomical local government rates increases). If the two quarterly CPI increases are in line with the RBNZ forecasts the annual rate of inflation will be 3.00% come 30 September. There is not a lot of room for error to the topside. In terms of timing, the 9 October OCR review statement will be before the September quarters’ inflation figures are available, so the earliest the RBNZ could cut interest rates would be their 27 November MPS. From an exchange rate perspective, that timing will most likely be after two US Federal Reserve interest rate cuts, therefore a late November RBNZ cut will not be negative for the Kiwi dollar.

Question 5: Does inflation automatically reduce on weaker GDP outcomes?

The economic theory is that weaker consumer demand cause weaker GDP growth and then in turn inflation falls as goods and services providers drop their prices to get sales/cash in the door. We have certainly seen food and building prices level off and not increase over recent months. However, nothing has really changed with the supply-side price-setting behaviour by the public sector (council rates, health and education) and less competitive private sector parts of the economy (banks, insurance, electricity and transport). The chart below shows that there is absolutely no connection between GDP growth and non-tradeable inflation over the last 20 years. Domestic inflation does not follow GDP downwards in New Zealand as it does in much larger economies like the US. Non-tradeable inflation only fell marginally and then went up when GDP collapsed during the GFC period in 2009. Non-tradeable inflation was “low” in the 2.00% to 3.00% band when GDP was strong in the 2014 to 2019 period. It is difficult to see non-tradeable inflation reducing to 4.00% over the next six months, let alone falling away to 3.00% or 2.00% as some seem to be suggesting.

The econometric models may spew out results that point to a collapse in inflation in New Zealand over coming months, however the reality is that significant parts of the economy in their price-setting behaviour are impervious to overall economic conditions and immune to interest rate changes.

The NZD/USD exchange rate briefly depreciated from 0.6120 prior to Wednesday’s RBNZ statement to a low of 0.6070 on the day. However, greater forces in the form of a weaker US dollar, have since allowed a return to 0.6120. The FX markets have already priced-in three x 0.25% cuts to NZ interest rates this year, so it is only upside for the Kiwi dollar if and when those cuts do not eventuate.

RBA wander off their monetary track

The FX markets are now voting with their feet in sending the Australian dollar higher to 0.6800 against the USD as they price-in the growing probability that the RBA will be forced to increase interest rates on 6 August. A stronger than expected increase in jobs in June (released Thursday 18 July) will add to the Aussie dollar’s upward momentum. An increase between 10,000 and 20,000 jobs is forecast, following the 39,700 increase in May. A 1.00% increase in their inflation over the June quarter, lifting the annual rate of inflation to 3.80%, will be the second positive for the AUD and will add to the pressure on the RBA to hike. The Kiwi dollar will follow the AUD higher.

Over coming weeks, additional forces that will lift the AUD/USD exchange rate from 0.6800 to above 0.7000 will be a generally weaker USD on global FX markets (discussed above) and a potentially stronger Japanese Yen. The Bank of Japan took the opportunity last week of a weakening USD (due to the low US inflation result) to intervene directly in the FX markets, buying the Yen and forcing it down from 162.00 to below 158.00. The level of Bank of Japan intervention was estimated at US$22 billion. However, the Japanese still need to increase their interest rates to stop the Yen depreciation.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

Excellent commentary!

I fully agree! What Mr Kerr explains with question 5 is showing the crux of the issue with non-tradable inflation. The only way to fix it is with good government policies, creating a better market environment and create decent funding for local authorities, but I don't trust the current lot in achieving this.

It is difficult to summon up much confidence in the RBNZ given the inconsistency as detailed in this article. The latest outlook makes the earlier statement as utterly lacking in credibility and you have to ask what were they then thinking and basing that thinking on. Recall some time back the tenacious Chloe Swarbrick, in committee, was able to reveal that the RBNZ was establishing a benchmark for their calculations by a method little short of firing a dart at a dart board. If so, little then has changed.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.