Summary of key points: -

- Latest US jobs data proves the skittishness of many Fed members

- Aussie dollar breaks higher

- What does political change mean for currency values?

Latest US jobs data proves the skittishness of many Fed members

The news article headline in one major global media website this week reporting the US Non-Farm Payrolls jobs data for the month of June was “US jobs growth in June beats expectations” – which was accurate, on the surface, as the increase in employment came in at 206,000, above the +190,000 prior consensus forecast.

However, as every prudent investor and savvy financial risk manager knows, “it pays to look beyond the headlines”. A closer examination of the jobs data from the US Bureau of Labour Statistics reveals a starkly different picture in terms of overall trends in the US labour market in 2024. The May Non-Farm Payrolls result was revised significantly downwards by 54,000 jobs from the +272,000 number originally released a month ago to a much lower +218,000. The April result was also revised down by 57,000 jobs to +108,000 from the original figure of +165,000, released in early May. It is highly likely that the June increase of 206,000 will also be revised heavily downwards when we get the July numbers in early August.

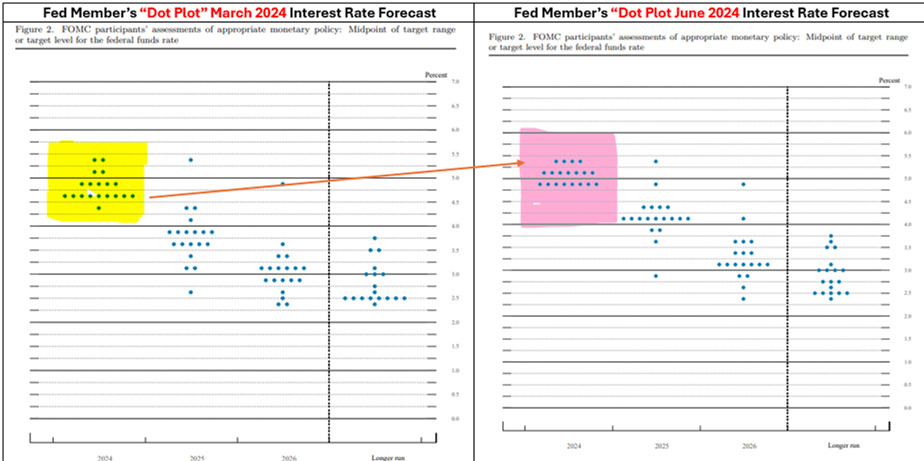

The historical adjustments to the original announcements are so large it makes a complete mockery of the efficacy and accuracy of the payrolls data as a reliable measure of employment trends in the US economy. However, both the financial markets and the 19 members of the US Federal Reserve place a lot of store on the monthly releases of the Non-Farm Payrolls data as a guide to whether inflation risks are increasing or decreasing. A stronger labour markets points to wages increasing and that in turn adds upward pressure to inflation. The original stronger +272,000 jobs number we saw for May sent US market interest rates upwards in early June and consequently the US dollar value (Dixy Index) appreciated from 104.00 at the start of June to a peak of 105.75 on 28 June. When the members of the Fed submitted their individual “dot pot” interest rate forecasts as part of the Fed’s Summary of Economic Projections report on 12 June they signalled a far greater concern of inflation staying higher for longer with many lifting their interest rate forecast for 2024 from their previous March forecast. As the two dot-plot charts below confirm, seven members increased their interest rate forecasts to above 5.00% in June from below 5.00% in March. The only factor that could have caused such a change was the higher 272,000 increase in jobs for May released on 7 June. In other words, seven Fed members completely knee-jerked to a single month’s jobs result, which was subsequently proven to be completely overstated!

A former New Zealand Prime Minister, the late Rt Hon David Lange, in the late 1980’s, appropriately labelled the foreign exchange markets as “reef fish” as they skittishly turn in different directions, all following one another in unison. It would seem to be an apt description for a good number of the august members of the US Federal Reserve!

The “bump” higher in US monthly inflation increases through January to March earlier this year has been well documented as not unusual and should have been expected by the markets and the Fed alike. As we have previously evidenced, US companies all put their prices up once per year in January and February, leading to the average monthly increase in inflation in January, February and March over the last 20 years being +0.50%. The average monthly inflation increase over the last nine months of the year has been +0.15%. Already in 2024, the April and May CPI inflation results have been lower at +0.30% and 0.00% respectively. The latest Fed worries about the risk of US inflation heading upwards again, based on a “robust” labour market, can only be described as “codswallop” of the highest order.

Supporting the case for lower US interest rates and a lower US dollar value was much weaker than expected ISM Manufacturing PMI and ISM Services PMI economic data last week. The services index falling away to 48.8, the weakest level in four years. Other measures of employment in the US, the ADP Employment Change and the Household Labour Force Survey also point to a marked softening in the labour market.

The money markets in the US are now pricing in two x 0.25% Fed cuts to interest rates at the September and December meetings. Over the course of the next month, further low CPI and PCE inflation results will see that pricing increase to three x 0.25% cuts. We have already witnessed the USD Index reverse sharply from the high of 105.75 on 28 June to 104.54 on 5 July. The NZD and AUD have made material gains in recent days and are poised to move even higher as the US dollar falters under decreasing US interest rates over the next six to twelve months.

Aussie dollar breaks higher

The Australian dollar has been out of favour with global currency traders and investors over the last three years, as the Reserve Bank of Australia (“RBA”) inadvisably only increased their interest rates to 4.35% to combat high inflation. The US, UK, Canada and New Zealand all lifted interest rates to 5.50% to get the inflation under control. Australian interest rates being over 1.00% below those of the US made the Aussie dollar an easy target for “carry-trade” participants, effectively borrowing the AUD at 4.35% and selling it to buy USD’s to invest at 5.50%. The Australian dollar was under constant downward pressure as a result.

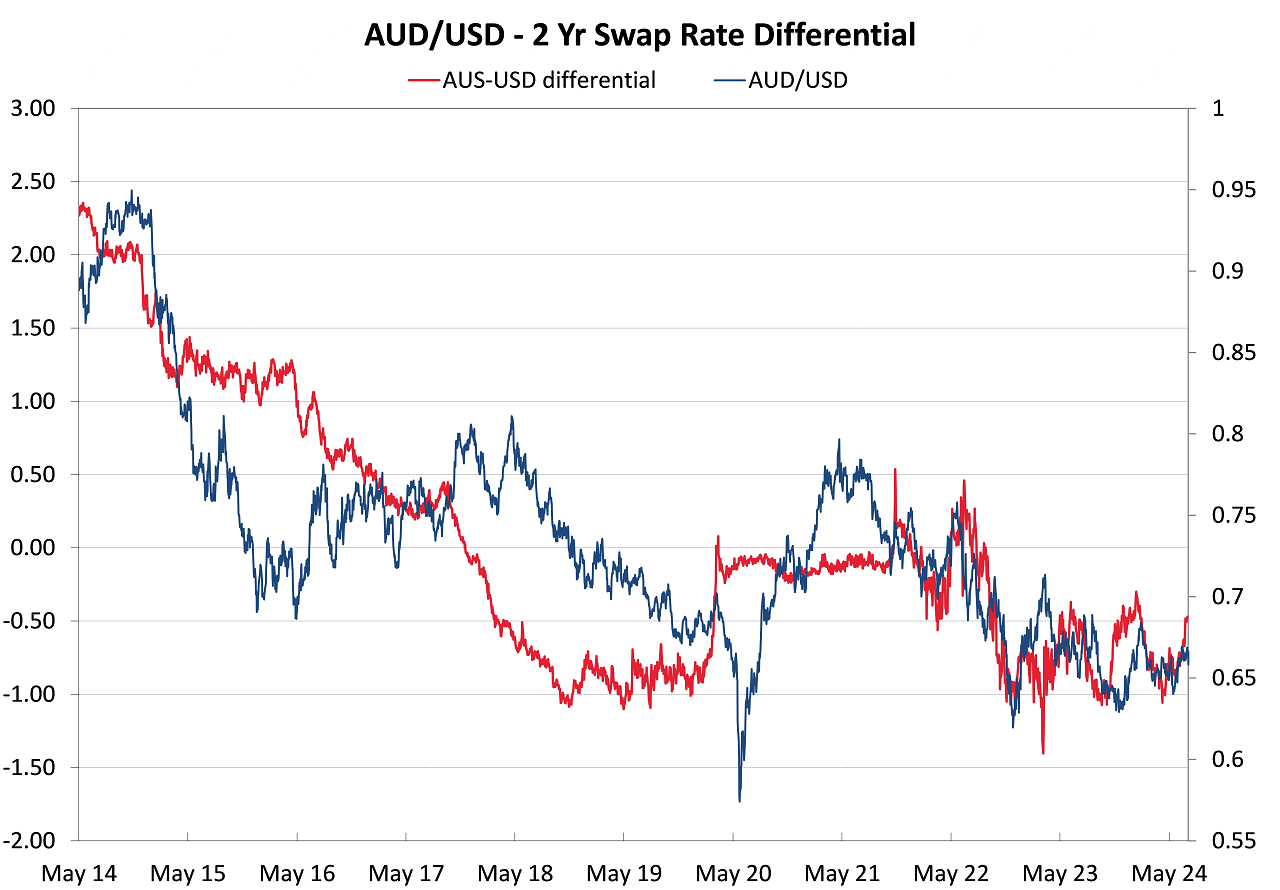

However, the interest rate gap between Australia and the US is now closing up rapidly. Two months ago, Australian two-year swap rates at 4.10% were 1.00% below the 5.10% US two-year swap rates. Today, the Australian two-year interest rates have increased to 4.35% and US two-year rates have decreased to 4.85%. The interest rate gap has now closed up to 0.50% (refer chart below). Looking ahead, US two-year swap interest rates are highly likely to reduce to the low 4.00% area over coming months as the Fed cut their Fed Funds interest rates. If the Australian June quarter inflation numbers (released 31 July) show inflation increasing, the RBA could well be increasing their interest rates at their next meeting on 6 August. The interest rate differential (red line on the chart) is poised to decrease further to 0.00%, suggesting that the closely-tracking AUD/USD exchange rate is headed significantly higher from the current 0.6750 level to well above 0.7000.

The second AUD/USD chart below confirms that at 0.6750 the Aussie dollar is breaking above the downtrend line it has remained below since 2021. The Aussie dollar is now considerably more appealing to currency traders and the Kiwi dollar does follow its trans-Tasman counterpart.

What does political change mean for currency values?

Abrupt political change around the world can certainly cause significant re-alignment of exchange rates, particularly if a change in Government leads to significant change in economic policies and shifting confidence from international investors.

The calling of a snap election in France a month ago sent the Euro value down from $1.0900 to $1.0700 as global investors expressed concern at the direction France was headed. The Euro has since recovered to $1.0840 as the US dollar has weakened in recent days. However, currency traders and investors have also been unwinding their earlier “short-sold” Euro positions as the risk of the far-right political party in France gaining a majority has reduced. We await the results of the second round of voting, but it seems an unstable coalition Government is inevitable.

Contrary to historical norms, the UK Pound has not weakened on the UK Labour Party and Sir Keir Starmer storming into power in Downing Street. The Pound has appreciated from $1.2600 to above $1.2800 against the USD as the markets expect tighter fiscal discipline and a more stable Government going forward than the previous dysfunctional Conservative lot.

The ongoing soap opera they call the US Presidential election has a number of acts still to play out over coming months. A victory for the Republican Donald Trump may temporarily be positive for the US dollar value as trade wars loom. However, tax cuts by Trump will lead to even larger fiscal deficits and even more Government debt, which must eventually end in tears for the US economy and the US dollar. A replacement Democrat candidate for the faltering Joe Bidon would have a better than even chance of defeating Trump and that would not be seen as USD positive.

Closer to home, Australian PM Anthony Albanese will come under mounting political pressure if the RBA do lift interest rates again and the mortgage belts in Melbourne and Sydney vote from their hip pockets against “Albo” at the next general election (sometime before May next year). A change of Government in Australia back to the Liberals would be viewed internationally as positive for the Aussie dollar as economic policies would be more business friendly.

Thankfully, here in New Zealand we are now well distanced from the previous Labour Government who scared off foreign investors. We need to attract those offshore investors back and if we are successful in that, it will be positive for the Kiwi dollar.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

3 Comments

Foreign investors, such as oil and gas companies, are wary of NZ after the previous government shut down new exploration. They understand that Kiwi voters could put in a Labour/Green government in two years which would re-create the anti-business sentiment of the previous six years.

I'm just laughing, how long have I been saying all the data coming out of the USA is just rubbish. Nice how all the jobs figures end up rounding to exactly 1000 as well by the way, clearly accurate.

Agreed.

Similarly, one of the best rules of thumbs I've come across for gauging predictions is basically ignore any that end in 0 or 5. e.g. We will run out of oil by 2040, interest rates have to fall by 2025, China will be global power by 2030, the USA will collapse by 2035, climate change will be irreversible by 2050, etc.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.