Foreign market reaction to economic data releases is often an instant reaction to the first headline that pops up at the scheduled time on the various market newswires. There is an instantaneous decision to buy or sell by traders, dependent upon whether the headline number is above, below or bang on prior consensus forecasts that are widely published. Large, intra-day exchange rate movements are typically in response to a major surprise, the figure released being a big miss to the forecast.

However, what does ultimately drive exchange rate direction is how central banks and governments set respective monetary and fiscal policies.

Changes to monetary policy signals and settings directly impact interest rate market pricing, which in turn determines exchange rate reaction. Central bankers do not react to one single data figure in isolation, they bring together a whole swag of backwards data, forward indicators, and trends over time. Unlike the FX markets, they generally do not react and change their stance on one single data release.

Therefore, in proffering a view on the future direction of exchange rates, it pays to sift the wheat from the chaff when it comes to economic data and the difference between short- and medium-term implications.

Over recent weeks there have been numerous examples of the markets reacting to the headline only and frankly getting the “wrong end of the stick” when it comes to the medium-term consequences for interest rates and exchange rates.

Example 1: New Zealand CPI Inflation for the March Quarter:

The immediate local media reporting of the March quarter inflation data was that it was “good news” for lower interest rates as the annual headline rate of inflation had further declined from 4.70% to 4.00% (in the middle of market prior market expectations). However, the real implication for future interest rates was closer to the exact opposite, as domestic/non-tradable inflation remained alarmingly elevated at 5.70% per annum.

To get the overall inflation rate below 3.00% this year, the RBNZ will need tradable inflation to plummet over coming months to -1.00% or -2.00%. That is just not going to happen with the NZ dollar lower and oil prices higher over recent months.

The chickens are coming home to roost in respect to high, sticky/wage-push domestic inflation proving very difficult to bring down. The result is that the RBNZ will be forced, by the data, to keep interest rates higher for longer than what the local interest rate market has been pricing of late. Wage push inflation is easy to go up, however very hard to pull down. That reality will be now dawning on the RBNZ economic forecasters.

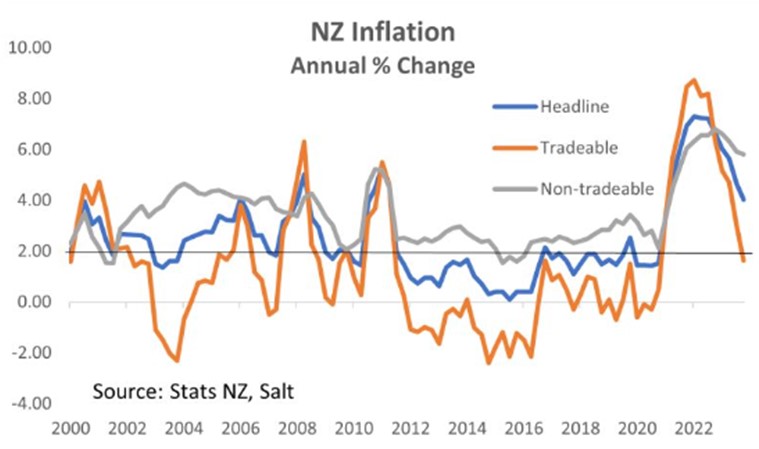

As the chart below depicts, non-tradable inflation (grey line) has been consistently running at between 2.00% and 4.00% for more than 20 years. The RBNZ seems powerless to influence the permanently high domestic inflation rates as they are caused by Government policy, regulation, and lack of competition in many sectors of the NZ economy.

On the other side, the RBNZ can only partially influence tradable inflation through statements and interest rate settings that influence the exchange rate value. Even then, the NZD/USD rate is 80% of the time determined by US dollar, the AUD and China factors. For a central bank that it has been outside its 1.00% to 3.00% inflation target for a considerable time now, it still surprises that they have failed to play the one monetary policy card they have available to push tradable inflation down further and earlier – statements and actions to force the NZ dollar to appreciate on its own, not depreciate. The RBNZ normally state that the NZD/USD exchange rate is moved by changes in interest rate differentials and that is something global, outside their control. They need to get smarter than that if they want to achieve the mandated inflation target band.

Example 2: Australian jobs data

The monthly employment measure in Australia is notoriously volatile, therefore the markets have learnt not to over-react to one month’s change in jobs, as it could be the opposite next month. In February, there were 117,600 new jobs added in the Aussie economy, almost three times the expected increase. Therefore, the March jobs numbers released last week were always going to be a crapshoot. The 6,600 decrease in jobs in March could not have been a surprise to anyone following the boomer increase in the prior month. However. the immediate media headlines and financial market reaction was that it was a weak and concerning development. Nothing could have been further from the truth.

Over the first three months of this year, the Australian economy has added 123,000 new jobs, and average monthly increase over 40,000 which is well above long-term averages. Despite strong inward migration, the labour market in Australia remains robust with continuing upwards pressures on wages. The RBA are aware of this fact and that is why they will not be cutting their interest rates in 2024.

The March jobs data was much more positive for the Aussie dollar than the initial market and media reaction.

Example 3: US shelter/rent costs impacting US inflation

For many months we have highlighted the considerable distortion the 12 to 18-month lagged shelter/rents prices are having on US inflation outcomes. The March CPI inflation numbers were no exception, with out-of-date shelter/rents data causing most of the 0.40% increase in prices over the month. The market reaction to that fraction of a miss was massive, bond yields 30 points higher and the US dollar appreciating. Fed officials (including Chair Powell) are now expressing concern that annual inflation is stalling at 3.00% over recent months and they have lost confidence that they can reach their 2.00% target. Stripping out the old and inaccurate shelter/rent data from the CPI measure results in all other prices in the US economy only increasing 1.80% over the last 12 months. If the Fed took current market rents data into their inflation equation they would be cutting their interest rates today.

Housing costs (shelter/rents) have a disproportionate high weighting of 40% in the core CPI index and the dodgy/rubbish data is artificially and somewhat unbelievably keeping overall inflation and therefore interest rates higher than where they should be. The PCE inflation numbers for March this coming Friday may return some confidence to the doubting Fed members as the annual PCE inflation rate heads below 2.50%.

US GDP growth figures for the March quarter they day before on Thursday 25th April will post a reduction from the previous 3.40% annual growth to something closer to 2.10%. Many US economic commentators express the view that 5.50% interest rates cannot be too restrictive on household spending levels as they view the economy as sustaining a robust growth path. Other economic data suggests the opposite. The chart below shows a severe collapse is spending in restaurants in the US over recent months (below 2009 GFC levels).

A fair summation of the US economy in 2024 is that its GDP growth and any inflation they do have is directly attributable to “Bidonomics” fiscal spending by the Government that is all debt funded. Their path is unsustainable and at some point, the debt music will stop. If and when that day happens, the US dollar value will plummet.

Daily exchange rates

Select chart tabs

*Roger J Kerr is Executive Chairman of Barrington Treasury Services NZ Limited. He has written commentaries on the NZ dollar since 1981.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.