Content supplied by Rabobank.

The global dairy market is poised for modest growth in 2025, driven by steady supply expansion and export demand, according to a new report by food and agribusiness banking specialist Rabobank.

But with this slow growth rate not expected to translate into surging stocks or general oversupply, global dairy prices look set to remain at elevated levels. And, as a result, Rabobank has revised its milk price forecast upwards by 30cents to $10.00 kg/MS for the 2024/25 New Zealand dairy season.

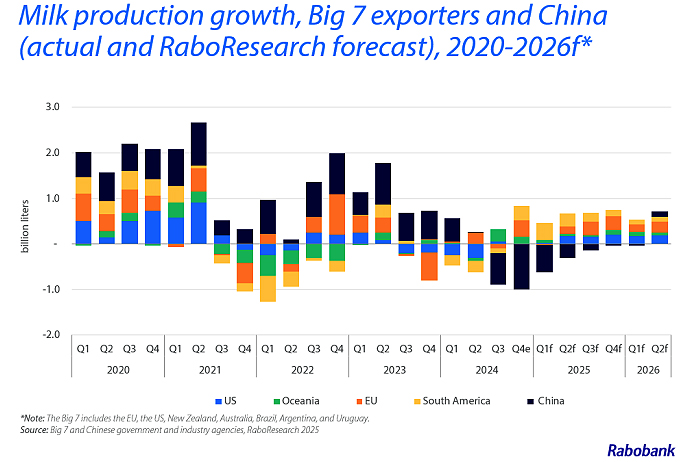

In its Q1 Global Dairy Quarterly report, titled Modest growth amid trade shifts, Rabobank says it expects milk production in the Big 7 export regions (Australia, New Zealand, Argentina, Uruguay, Brazil, the EU, and the US) to expand by 0.8% year on year (YOY), with a similar gain in the first half of 2026.

The report says this forecast is driven largely by a return to production growth in both the EU, where production has oscillated between growth and contraction in recent quarters, and the US, where the typical annual gains of 1%+ have stagnated in recent years.

“US supply expansion is expected in 2025, but it’s likely to be modest at sub-1%,” report coauthor, Rabobank senior agricultural analyst Emma Higgins said.

“Production gains are also expected from Oceania and South America, largely driven by prior year declines that are easy to surmount.

“Overall, we anticipate milk production from the Big 7 will reach 325.8 million metric tonnes (mt) in 2025, up from 323.2 million mt last year.”

Ms Higgins said global supply growth in the second half of 2025 was likely to be stronger than the first.

“2025 will begin with slower production gains, estimated at 0.5% in Q1, which will help maintain the current firm commodity prices. We’re forecasting a steeper 0.9% YOY gain in the second half of the year, which is projected to push 2025 production past the previous peak in global annual milk production, which was 323.7 million mt in 2021.”

Outside of the Big 7, Ms Higgins said, China was on a different milk production path to most regions across the world, with Chinese supply expected to fall further in the year ahead.

“Chinese milk production dropped in 2024 following several consecutive years of significant expansion, representing a stark break from the recent trend,” she said.

“Fewer cows and the steeper-than-expected decline in Q4 2024 led RaboResearch to reduce its 2025 Chinese milk production forecast, which is now down 2.6% YOY, marking the second successive year of lower production.

“Early February Chinese farmgate milk prices were down 15% YOY in US dollar terms, discouraging any near-term incentive for farmers to increase production.”

Demand outlook

The report says Chinese dairy demand is expected to improve this year, but at a slower pace, reflecting domestic economic challenges.

“Imports should also improve compared to a paltry 2024 sum,” Ms Higgins said.

“For years, the world looked to China as a barometer for demand, but as the country rapidly increased dairy self-sufficiency in the first few years of this decade, 2021’s record import year is a distant memory.”

Despite China’s retreat from the global demand stage, the report says, purchasing in other key regions is encouraging.

“US cheese exports surged to a record high in 2024, with positive signs for this year. New Zealand is also finding buyers for its additional milk, supporting a record-high milk price,” Ms Higgins said.

“However, potential challenges could disrupt this outlook, primarily related to the rapidly evolving trade barrier landscape as the US shifts away from decades of global alignment.”

With Republican leadership in Washington, DC taking a new approach to trade, Ms Higgins says, tariff implementation, and possible subsequent retaliatory tariff action from trading partners, could negatively impact US dairy exports.

“In 2024, cheese exports to Mexico, the top destination for US dairy, increased by 30% YOY, while China purchased 42% of US whey exports in 2024.” she said.

“Dairy has not yet been negatively impacted by any disruption, but the threat remains serious. Reduced exports would be bearish for US prices.”

To keep trade balanced and dairy prices supported this year, the report also notes that importers worldwide will need to keep an eye on consumer demand in the wake of recent inflation.

New Zealand update

The report says export volumes for the three months to January 2025 increased 2% compared to the prior year, with a weaker currency and stronger commodity prices resulting in an extra $1.5 billion in exports over the same period.

“Total 2024 dairy exports marked a three-year high, with sales to China following a similar trend. New record totals were also shipped to Malaysia, Taiwan, and Saudi Arabia,”

Ms Higgins said. Ms Higgins said export volumes are likely to remain strong over the first half of 2025, as higher milk flows earlier in the season and broad-based demand settings will ensure additional milk production finds a market.

“With milk price forecasts up by NZD 2.00/kgMS compared to this time last year, dairy farmer confidence is strong, and this positivity has been further buoyed by alleviating interest rate pressure following recent drops in the Official Cash Rate.”

While early summer rain made for happy farmers over Christmas, the report says, seasonal dry conditions have hit many North Island regions and the east of the South Island, hampering milk flows in recent weeks.

“If significant rain is not received over the coming weeks, there is a risk that the milk production season finishes abruptly in the western, middle, and north of the North Island,” Ms Higgins aid.

“Despite high milk price forecasts, some farmers may choose to conserve feed and preserve cow conditions prior to winter, potentially ending the season early if conditions remain unfavourable.

“For now, we’re maintaining our expectations for milk collections across the 2024/25 season and anticipate milk production growth of between 2.5% and 3% for the full season.”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.