It was a busy week in tax with Inland Revenue releasing guidance in relation to a couple of commonly encountered scenarios. The first is QB 24/04 When is a subdivision project a taxable activity for GST purposes?

This covers the frequently discussed and very important issue of what is the GST treatment when you are subdividing land into two or more plots? The standard position about GST is that you must register if you're carrying on a taxable activity and the value of those supplies exceeds the registration threshold of $60,000.

What’s a taxable activity?

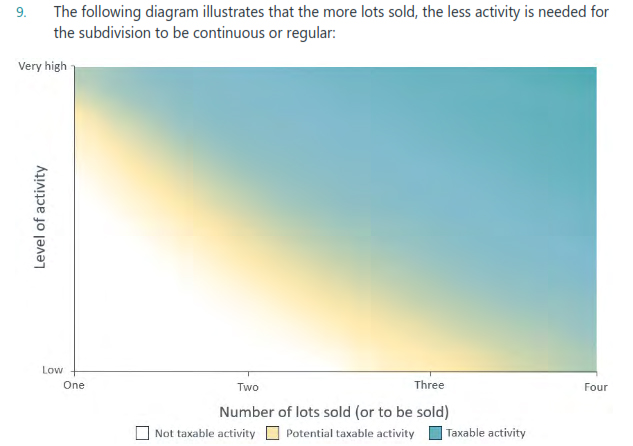

Clearly many subdivisions will exceed that $60,000 threshold when they are sold so what represents a taxable activity? In order for a taxable activity to exist it must be carried on continuously or regularly. Therefore, it follows that for a subdivision to be continuous or regular, it usually needs to involve the sale of more than one lot. A subdivision which only involved one sale would usually be regarded as a one-off activity because it does not meet this threshold of continuous or regular.

Notwithstanding that the Inland Revenue guidance points out that some subdivisions which only led to one sale may in fact be continuous and regular. But that would only be if the level of activity involved was very high. Now, like so much of tax, it's this comes down to the question of the facts of a particular case. Very high in this context might be something like construction and sale of a large office block, or more likely, because more often than not we're talking about subdivisions of residential land, an apartment block.

The guidance continues the more subdivision plots are divided, the more likely it is to be deemed as being continuous or regular. Following the Newman decision way back in 1995, if a subdivision leads to the sale of four or more lots, that's typically taken as the benchmark for determining that the continuously or regularly is happening and there is a taxable activity.

On the other hand, what happens when there are two or three lots? Then you have to consider the level of the activity relative to the number of lots being sold in order to determine whether or not this activity is continuous or regular. Therefore, you'd look at the level of development work, the time and effort involved, the level of financial investment and the level of repetition. This last point is probably most critical. If you're repeating the process multiple times, this is more likely to fall into the continuously or regularly category. But as the guidance notes, everything is fact dependent.

On the other hand, the factors that are not so relevant are whether or not the subdivision is commercial. It doesn’t matter whether the subdivision has a “commercial” flavour or you are subdividing your own land to downsize. Anything done without an intention to sell the resulting land is not relevant. For example, if you build a house on a subdivided lot with the intention of living in it, but later change your mind and decide to sell, work done before you change your mind is not relevant.

Overall, this is useful guidance which comes with a helpful accompanying fact sheet. Keep in mind that the GST treatment is not tied to the income tax treatment. Your project might not be a GST taxable activity, but it could well be subject to the bright-line test or any of the other land taxation rules.

Another common issue – loans to shareholders

Moving on, the other topic, on which Inland Revenue has released useful guidance is a draft interpretation statement on the income tax position in relation to overdrawn shareholder loan account balances (sometimes called shareholder current accounts). Now, as anyone who works with small businesses will tell you this is actually a pretty common scenario. Despite this, the income tax position is not always as well understood as it should be.

In my experience, overdrawn shareholder current account balances typically arise in two scenarios. Firstly, where the owner or shareholder is taking out more in drawings than they're being paid as a shareholder or employee or any other form of payment. This is a fairly common scenario.

The other instance is where the company has realised the substantial capital gain and shareholders extract the cash without waiting to consider the tax implications of doing so. Often in those situations, advisers don't find out until maybe months afterwards. At that point it can become quite difficult to unwind the tax consequences because the numbers involved are quite substantial.

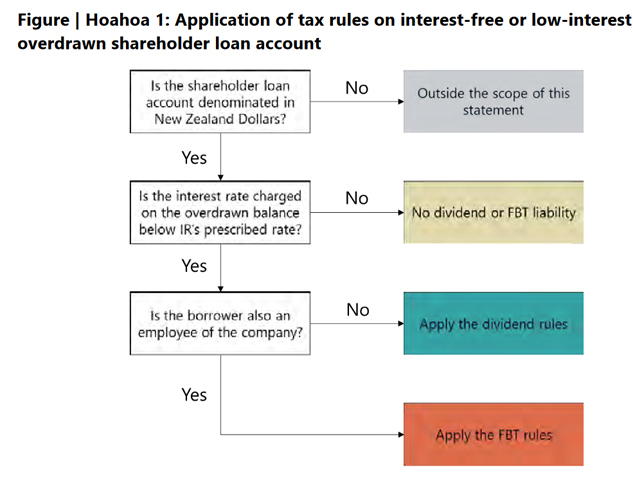

It's therefore good to have Inland Revenue guidance and this comprehensive interpretation statement runs to 41 pages begins with the summary of the basic rules. A dividend is deemed to arise for a shareholder if they are paying little or low interest on an overdrawn shareholder loan account.

The amount of a dividend on an interest free or low interest loan typically represents the difference between a benchmark interest rate that should be charged and the amount of actual interest rate occurring on the loan. Benchmark for this purpose is Inland Revenue’s prescribed rate of interest, which since 1 October 2023 has been 8.41%.

A dividend can also arise where the loan has been advanced to an associated person of the shareholder. This can lead to some quite involved tracing of shareholdings and related calculations about percentage of shareholdings. This is necessary to determine if there is an association and whether that associated company is part of the same 100% owned group and therefore potentially eligible for the exemption on intra-group dividends. This is another area where I’ve encountered situations where this associated person issue hasn't been picked up.

Incidentally, it's worth noting, by the way, that although for New Zealand tax purposes, the amount of the dividend is the amount of interest that should have been charged in Australia and the UK, the amount of the dividend is deemed to be the full amount of the advance made. This might be something we might see Inland Revenue take a look at as it’s something that has occasionally come up in discussions with officials.

Loans to shareholder-employees

Were the shareholder is also an employee of the company, then the low or interest free loan is not treated as a dividend but is instead subject to fringe benefit tax. The amount of the benefit is the difference between the interest paid and the prescribed rate of interest. Something to note here is that the shareholder-employee doesn't solely mean someone within the provisional tax regime, but it also includes shareholders who are employees and whose salary are subject to PAYE There's a couple of useful flow charts to help people determine who might be captured by these rules.

The draft interpretation statement also notes that typically interest paid by a shareholder on an overdrawn current account is generally not deductible. This is because usually the drawings are often applied for private or domestic purposes, and so there's no link to an income earning process. However, in some cases the money might have been withdrawn to invest in a residential property or some other income producing asset, in which case the interest would become deductible, if all the other deductibility criteria can be met.

One other key point to note is what happens if a shareholder is no longer required to repay the overdrawn balance, because the company forgives or remits the debt in some way. In this case the full amount of the loan will be deemed to arise either as a dividend or under the financial arrangements regime. In either case the shareholder will usually be taxed on the amount that's been remitted.

The interpretation statement also covers scenarios when resident withholding tax might need to be deducted and interest therefore be reported as investment income. This would be somewhat unusual, but the interpretation statement explains when it might happen.

Overall, this is an important and useful document setting out the rules pretty clearly on a topic which as I noted is frequently encountered amongst small businesses but isn't always as policed or managed as effectively as it should be. It’s also accompanied by a more digestible 8 page fact sheet. Consultation is open until 2nd August.

A blueprint for taxing billionaires?

One of the interesting things going on around the world in the tax policy area now is something of a trend amongst international organisations such as the International Monetary Fund (IMF), the Organisation for Economic Cooperation and Development (OECD) for releasing papers for discussion on the taxation of capital and wealth.

The latest such paper A blueprint for a coordinated minimum effective taxation standard for ultra-high-net-worth individuals was commissioned by the Brazilian G20 presidency earlier this year. The report was written by the French economist, Gabriel Zucman, a protégé of Thomas Piketty. It proposes a framework the approximately 3,000 or so billionaires in the world to pay at least 2% of their wealth in individual income tax or wealth taxes each year.

Zucman’s report notes there been a vast improvement in international tax cooperation since the mid-2010s, particularly with the Common Reporting Standard on the Automatic Exchange of Information which commenced in 2017. He also pointed to the recent agreement hammered out by the OECD for a minimum tax of 15% on large multinationals. (It's worth noting though that agreement has yet to be fully implemented as progress has slowed recently).

Zucman correctly points to this growing international cooperation and exchange of information as laying the baseline for further international cooperation in the form of what he terms a common minimum standard, ensuring an effective taxation of ultra-high net worth individuals. According to Zucman this “would support domestic policies to bolster tax progressivity by reducing incentives for the wealthiest individuals to engage in tax avoidance and by curtailing the forces of tax competition.” This would target the tax havens where much of this wealth is sheltered.

The paper estimates that a 2% tax on those 3,000 billionaires could realise between US$200 and US$250 billion U.S. dollars in revenue annually. If it was extended to those worth more than $100 million, that could generate another US$100 to US$140 billion per annum. These tax revenues would be collected from “economic actors who are both very wealthy and undertaxed today”. Those affected might not agree with this assessment that they're presently under taxed.

The paper is realistic enough to note that there are real challenges with the proposals, such as how to value the wealth, ensure effective taxation if some jurisdictions don't agree to implement it, and of course compliance by taxpayers. It's a bold proposal which has attracted a lot of attention although I'm sceptical about the potential level of revenue which could be raised. We really don't have a very detailed understanding of the composition of the wealth and where it is held of the very wealthy. That's an issue which would need to be addressed. And as I mentioned, there are serious issues around valuations and informed enforcement, which Zucman acknowledges.

Starting a conversation?

But for me, the most interesting thing to me about this whole proposal, it's the latest. As I said, it's the latest in the line of papers coming out of the likes of the G20, the OECD, the IMF, the World Bank, all of whom are basically saying that we are not taxing wealth sufficiently and we need to do something about that to address inequality. As Zucman himself puts it in the Foreword of the report

“The goal of this blueprint is to offer a basis for political discussions – to start a conversation not to end it. It is for citizens to decide through democratic deliberation and the vote how taxation should be carried out.”

In other words, he is repeating my old precept that tax is politics.

My personal view is we need to have a broader discussion around the taxation of capital. One of the points to emerge from the current debate going on over replacing the Cook Strait ferries is that the new ferries represented just 21% of the total cost of Project iReX. The other 79% represented the cost of upgrading the supporting infrastructure not just for the larger ferries but also to make it climate change and earthquake resilient for the next 100 years.

Even if we dialled back the futureproofing to, say, 50 years, we're still talking about significant sums of investment. We’re also still left with the key point of how will we pay for the vast amount of infrastructure that we will need to upgrade to deal with the continuing impact of climate change. In my view our politicians have not yet seriously engaged with us on this issue.

Meanwhile in the UK…

And finally, this week a quick note on the UK election which is next Thursday. The likelihood is that the opposition Labour Party is heading for a massive win. One of their key tax proposals is the abolition of the remittance basis or non-dom tax regime.

But not every voter has understood exactly what that means. As Labour candidate Karl Turner recounted to the Guardian

“We met a guy who said he was going to vote Labour but wouldn’t now because he had just heard that we were taxing condoms,”

“I said, ‘condoms?’ ‘Yeah,’ he said: ‘I just heard on that [pointing to the TV] that you are taxing condoms, and I’m not having it. You’re not getting my vote.’ It was Terence [Turner’s parliamentary assistant] here who worked it out.

“‘We’re taxing non-doms, not condoms,’ I said. ‘Oh,’ he said. ‘Like the prime minister’s wife? Ah.’ He calls out: ‘Margaret: they’re taxing non-doms, not condoms.’”

And on that note, that's all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

5 Comments

The current UK Conservative Govt has already scrapped non doms

What does non-dom mean and how are the rules changing? - BBC News

There's a cute spelling error in there;

the current debate going on over replacing the Cook Strait fairies

:-).

Might be the AI, fixed now.

Would be good to chase up on the release of that phase 2 doco release on the ferries. The weeks have turned into months.

Re the cost of the infrastructure for the ferries, I wonder how that projected cost would compare with a nice new terminal at Clifford Bay - and think of the emissions saved from the shorter travel time!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.