The median selling price of homes in Auckland was $800,000 in January, down 7.3% compared to December and down 2.4% compared to January last year when the median in Auckland was $820,000, according to the latest figures from the Real Estate Institute of NZ.

The REINZ said Auckland's median price in January was the lowest it had been in any month since February 2016.

Within the Auckland region, price trends were mixed, with prices down compared to a year earlier in Rodney, North Shore and Papakura, while prices were up in Central Auckland, Waitakere and Manukau.

Sales numbers were also down in Auckland, with 1152 homes sold in the region in January, down 2.8% compared to January last year.

Prices were also weaker in Canterbury, where January's median price of $431,900 was down 0.7% compared to January last year.

But prices tended to be firmer around the rest of the country, with all regions except Auckland and Canterbury posting annual increases in January compared to a year earlier and five regions - Waikato, Manawatu/Whanganui, Marlborough, Otago and Southland - posting record median prices last month.

However January's median prices were lower compared to December last year in in seven regions, Auckland, Bay of Plenty, Gisborne, Hawke's Bay, Wellington, West Coast and Canterbury, and higher compared to December in all other regions.

And the median price across all regions except Auckland was down 1.4% in January compared to December while January's national median price $550,000 was down 1.8% compared to December.

Across the entire country 4372 residential properties were sold in January, down 2.5% compared to a year earlier.

Across all regions excluding Auckland, sales volumes in January were down 2.4% compared to January last year.

"January has pointed to a two-tier market continuing around the country, with Auckland and Canterbury experiencing a slow down in price, but the rest of the country has seen strong price growth," REINZ Chief Executive Bindi Norwell said.

The interactive charts below track changes in the median selling prices and in median price growth, in all regions of the country.

Median price - REINZ

Select chart tabs

Median house price growth

Select chart tabs

131 Comments

Tell me Orr had no idea of the sales volumes. Only December/January of 2008 had lower Auckland volume. The RBNZ will cut next.

"It's the RBNZ's job to protect me from the risk in decisions I've made!" - speculators

Reserve Bank warns: 'It's not our job to protect you from the housing market' https://www.stuff.co.nz/business/99408539/reserve-bank-warns-its-not-ou…

Market forces are now flatlining the expectations of rearview mirror obsessed speculators....

The Man, The Man, please bring us your Christchurch real real estate spam!

He's unable to login right now but he did send me this text:

Once again "The Man" is right and the COL is wrong!!!

In Chch up means down so prices are actually very healthy!!!!

Property is the best way to get ahead!! Especially in provincial towns ravaged by earthquakes!!!!

He's busy filling a couple of skip bins after his Skinhead tenants stopped paying the rent and disappeared leaving the place in a tip.

Well how is hanging with the mongrel mob or black power ? Making a point

Properties in the high end of the market are beginning to pile up, while a lot of low-mid point properties were withdrawn from market prior to Christmas - possibly being placed on the rental market as prices were not achieved. A lot of rubbish stock around at the moment which looks as if investors are trying to get rid of properties. Houses that are in excellent condition are still selling, as are properties that are keenly priced. Otherwise, they're simply just sitting there for months.

Another really weird thing I am seeing is a lot of properties that sold within the last 12-18 months are back on the market. Does this suggest mortgagee sales from overstretched buyers, or naive investors that can't fund the negative yields? Whatever the reason, its very odd.

FYI, Auckland days to sell are at 51 days. The last time this statistic was at these levels was Feb 2011 when it was 50 days ..

another few months of low volumes and falling prices and yes they will.

-2.4%, panic stations

Not yet. That's still to come....

It comes after the "I wish I'd sold back in...."

and the "I'll sell when it gets back to..."

and of course well after "It's only a bit of a dip. It'll come back...."

But just before the bottom, of course!

Anyone who is not able to hold for long term should get out fast and minimize the lose but if can hold for 3 to 5 years than may hold.

Consider an owner occupier who bought in March 2017.

1) At March 2017, the median house price in Auckland was $905,000.

2) The current median house price in Auckland is $800,000, so that is a 12% decline.

Then consider that they had a deposit of 20% ($181,000) and borrowed the remaining $724,000 to purchase the house in March 2017.

Assuming an interest only loan, that equity is now valued at $76,000 (house value $800,000 less mortgage balance of $724,000). That is a decline of 58% from their initial deposit.

Now how long did that owner occupier household take to save that $181,000 initial deposit?

The owner- occupier is fine if they can continue to meet the debt payments. If there is a recession and an income earner from the household becomes unemployed, the household may be unable to continue the debt payments and be forced to downsize.

If the house price falls a further 10%, then the house value is below the mortgage and if the household experiences a job loss under these house market conditions, and forced to sell, they will effectively lose all of their initial deposit. They could conceivably go into negative equity if house prices fall further than 10% and still be left with debt outstanding to the bank after the house sale.

North shore city -5.3% YoY on the HPI.

Rodney district -3.8% in 3 months, (-2.2 YoY) ie, its a big fall, but recently.

The HPI graphs show a definite fall, not the wandering back and forth in the noise band like they have been for the last two years..

All the auckland districts have fallen at least 2.2% in the last 3 months on the HPI, with North shore -4.9% and Rodney -3.8%, the others in the -2.2% to - 2.6% range.

Just pull the blanket a bit further over your head, you'll be right.

Best get in there while the getting is good then

Nope.I haven't got the armoured gloves to be reaching out and trying to grab a falling knife.

I wonder when the OMG they were right light bulb will come on?

Pragmatist, how low do prices have to get for you to be convinced that the knife has hit the floor?

For me, I will re-enter the market when yields make it worthwhile. No knives to catch, all my rentals are cash-flow positive.

Drops normally go through the floor then recover. Rule of thunb is that drops happen 3 times faster than gains. Source: every bubble ever.

Going Up - taking the staircase

Coming Down- taking the lift

Stock brokers fancied the windows in the 30s.

I'll let you know when I hear it hit the floor.

Listening for something that doesn't make a sound - perfect excuse to never enter the market.

Well, since the knife is imaginary too.. can it ever hit the floor? Is the floor real? Does Tinkerbell fart glitter and rose petals?

You’re telling the story, I’m just asking questions. Story is a work of fiction so far - listening out for imaginary knives hitting imaginary floors.

Yeah, silly me for crediting you with the intelligence to understand the meaning I was conveying. Let me spell it out in small words: I will let you know when it looks like the falling prices have stopped falling.

At which point prices will be rising again, it'll no longer be a "buyers market", and you'll be back to saying that only a fool would get into the market now as this isn't sustainable. Mark my words. And if you're waiting for a 10% drop you're going to have to wait for a GFC.

Personally I think you're both stupid, and hope you see the light and move in next door to me in Brisbane. Home and away, closer each day!

The three of you in Ramsay Street, Noice!

Pragmatist and Saving4AUHouse will have to rent a flat together.

I might buy something at the end of the year. Something modest, but with a small mortgage (~10 years). I'm leaning towards Brisbane right now - better flights than Perth and Adelaide, cheaper than Melbourne.

Good idea in my opinion, as long as you stay in the market for 5 years at least. A certain someone will be able to tell you what happens when you sell under pressure and don’t get back in.

Nah, the last thing I want hear is you and saving4au having hate-sex through the walls.

You may not hear it hit the floor because of the sound of screaming as toes get sliced off. Long way to go yet and Mr Orr knows it. Rate cut by April.

Are you callin Adrian Orr a lier? He’s said 1.75% all year. You really can turn on a dime - you were earlier saying there would be rate hikes later this year.

why woulld they cut rates when its only Auckland an ChCh going backwards, the rest of NZ is still on the up.

I think a cut is a fair way down the track

Nic,

I am very willing to put $100 on that if you are,winner's money to go to charity. There will Not be a rate cut by April,though it's entirely possible that there will be at least one sometime next year.Interested?

Nic, what do you mean rate cut in April, not long ago you said rate rise in Q3 2019...

I think you'll discover, as will the RBNZ, eventually, that we are burning toes in the fire, having jumped out of the frying pan! They'll sacrifice the NZ dollar to try and rescue the housing market. it won't work though.

If you have your heart set on entering the Auckland market on a 30 year mortgage, I wouldn't try and game this.Time in market > timing the market.

"OMG they were right"

When will you say that MTP?, after all you are probably a speculator in DGM clothing

No don't answer the question tonight go and have valentines romance with the ....

So if someone had stumped up 1 million for a standard-ish house they'd have lost $24,000 dollars so far. I'm sure 24k is considered chump change for a NZ wage earner...

if it was bought 15 years ago, they would be ahead.. $600k?

Wait, what? 7.3% down compared to when?

“The median selling price of homes in Auckland was $800,000 in January, down 7.3% compared to December and down 2.4% compared to January last year...”

-7.3% since December 2018. So down 7% in a month. Not sure if that's apples to apples or just skewed due to lower quality stock being sold.

The house price index is supposed to adjust for the quality/type of the dwelling and that's down "-2.1% year-on-year" on a same house same street basis. So there is no way the spruikers can spin this positively.

Source: https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2019/Reside…

The January Auckland median is lower than the January median of 2018 , lower than January 2017. The last time Auckland medians reached this level was February 2016. Auckland median is now 100000 K below peak .So the housing shortage according to Bindi is not in Auckland but almost everywhere else, where prices are actually increasing.

Down 7.3% in one month, that means down 87.6% pa!

I glad that the foreign buyer ban is having no effect in auckland after all JK told us it was only 3% of sales

(sarc)

Foreign buys are going to have a massive effect on the market, but only at the top end because how many Kiwi's are in the $2.5M bracket ? Expect the sub $1M market to keep going strong, buyers have to live somewhere. Big falls at the top end is going to skew the median figures big time.

Hmmmm how many people can afford sub $1 million in the 800k - $1 million range

Answer - not that many.

There will be falls at all price points.

don't want to burst your bubble here sharetrader, but we are looking at median?

there is a massive emphasis on affordable homes now. this will be having a significant impact on median price. as an example I know of one builder that was building high-end houses 12 months ago. They are now exclusively building kb, and have 100+ units on the go.

It is astounding the similarities between the NZ market and Australia, with several months lag. Sydney hit a period of stagnant prices, followed by small falls, at which point everyone claimed strong fundamental (high immigration, low rates, high employment) would result ensure that any falls would be minimal.

Fast forward to today and the rate of declines in Sydney continue to accelerate with predictions now reaching 20-25% peak to trough falls. It started with Sydney but is now spreading across the rest of the regions in Australia.

Prices gains in both countries weren't based purely on "fundamentals". They were amplified heavily by the desire for tax free capital gains. Remove those capital gains and the demand picture will look very different.

I really hope that FHB take note of what has occurred in Australia and sit out over the next couple of years, or they risk seeing any equity they put in evaporating.

Yes, I agree. Seems to be about a year lag with Sydney this time but closer to Melbourne. It’s down about -10% in Sydney (some places in west Sydney over -20%). Even though the RBNZ gov is saying publicly that it’s likely Auckland and NZ overall will be different, does he reallllly think that? Mind you, the RBA is STILL also saying publicly that everything’s fine in Australia...

The ideal situation the RBNZ would like to steer the market towards is several years of stagnant prices to return prices to more affordable levels.

Its very hard to manage this after such a short period of sharp price appreciation. Lots of investors are on thin returns that only make financial sense with capital appreciation - falling prices make the investment feel far less appealing. Lots of FHB rushed in as they were scared of being "locked out" of the market. Lots of boomers holding on to oversized family homes as they kept appreciating in value.

Stagnant/falling prices will impact the demand from all these groups. If the RBNZ can navigate a slow inflation adjusted deflation of prices it will be quite an achievement.

It certainly would be an achievement. Has a soft landing ever been achieved from the heights of 9 times price to income? That’s higher than Ireland was before their bust, and interest rates are already very, very low. If the market starts dropping quickly, I guess it’ll be a further drop in rates and a massive round of quantitative easing.

youre kidding right?

mild drop in rates only, no QE. They need to keep something up the sleeve for when GFC2.0 hits

Stagnant prices will not return housing to affordable levels, unless incomes rise dramatically to close the gap. And in our low wage, low productivity economy (thanks to the relentless importation of third world labour) that will never happen. We need a 30-40% reduction in prices to even bring NZ housing close to the realm of affordable - probably more considering NZ is the second most unaffordable housing market in the world.

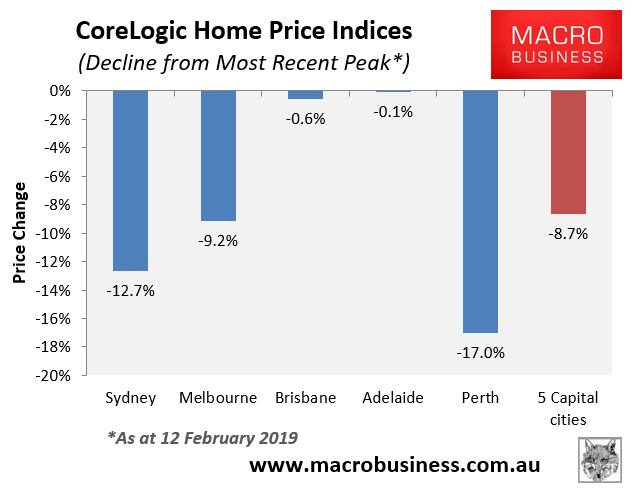

Down 12.7% in Sydney now, with forecasts of 25-30% drops. Melbourne not far behind with 9.2% falls. Brisbane starting to roll over now as well.

https://www.macrobusiness.com.au/wp-content/uploads/2019/02/Capture-202…

{kind=link}

Given that forecasts were previously 5-10% drops, like a number of economists have been picking for NZ - does that mean the new 25-30% drop forecasts are code for 50-60% actual falls?

Interesting potential implications for NZ in more ways than one. A house price crash there is likely to lead to growing unemployment. Which could see a significant number of kiwis return.

Not just Kiwis - Australians (especially recent migrants) might head across the ditch to look for work. After all, we have a Govt funded house building programme, whereas the Australian development market is drying up. I lay odds on that "builder shortage" won't last very long.

And conversely, if housing crashes over there but not here, how many Kiwis with in demand skills will jump the ditch for more affordable and better quality housing?

Yeah.....But will there be the jobs in the wake of a crash?

depends what you do.. some fields are going to stay in demand, others will be devastated by a crash. Certainly wouldn't want to be in construction in Oz right now.

I personally think it won’t be more than 30% in Sydney as I can see policy makers pulling out all the stops to ensure it doesn’t turn into a complete meltdown.

For NZ I’d say we will see less severe drops, but still within the 15-25% range in the most over valued markets.

Auckland will be no difference. Just wait for few months.

Process has already started

Some FHBs are waiting in the wings (like me), but the data has shown a increase in lending to FHBs in the last 6 months which is worrying. Overall I blame the entire situation on growing up with little to none formal finance training in schools. As a society I think we are not that financially literate...

There is no way financial literacy is going to win over the relentless reinforcing by the media of the nothing but positives in house price increases and the if your not in your locked out.

Why would the owners of the country want the population to figure out they're being milked day in day out on a mortgage farm. Stick to the important subjects like mandatory Maori language lessons and social studies.

The politicians love poor people so much they want to create more of them.

And their votes, once more of 'em are created, are so easily purchased.....

If only there were a nationalist party for working people. Maybe it could be called The Nationalist Party or The Labourers' Party.

It seems Banks are still willing to lend at high LVR, and there are still people being tempted to enter the market. If price falls start accelerating FHB won't be able to enter the market (unless they have large deposits) as Banks will stop lending at high LVRs very quickly.

I know a number of couples in their early 30's who have been sharing their success stories on FB for just getting onto the 'property ladder' in Auckland....I just can't help but think it could be a massive mistake timing wise....

Schooling prepares you for a job, self education prepares you for life.

Lots of essential life skills are not formally taught at schools. If you choose to go and learn them yourself - you'll be much better off to make informed and higher quality life decisions.

Others passively choose to remain uninformed - as a result seen many people make poor quality life decisions due to being uninformed. If they had been informed, it is possible that they would have avoided getting themselves into a bad position where the only choices at that point were miserable or less miserable.

Here's a pretty simple book which covers a lot of areas to avoid -

https://www.amazon.com/How-Ruin-Your-Life-Anthology-ebook/dp/B005MIDDQ8…

Can't put off kids forever, sadly. A lot of us are already much older than our parents were when they started families. Just have to bite the bullet and go all in.

Nah, don't bother having kids we're importing enough people from overseas who can do all that hard work for us.

the man will be along shortly to tell us all the figures for Canterbury are wrong and its all positive down that way

Nah he'll be too busy out trying to "buy the dip", adding more to his millions of dollars of indebtedness

To be fair, the Christchurch city data is pretty stable. I may be biased now as I'm in the process of buying a house there. Nicer house than we are renting at the moment, mortgage payments will be less than current rent. Not expecting the value to increase in the next couple of years.

Looked to me like prices are very similar to 2016 RVs still, we are buying ours at a slight discount to RV. Plenty of activity at open homes and quite a few quick offers made on places we were interested in.

Indeed, Christchurch is a working example of what throwing restrictive land-use policy under the proverbial bus can do for Supply. And the insurance helicopter munny meant that the rebuild was not all bank-financed. But not, unfortunately, a circumstance that can be transplanted to - say - Orcland.

yes, and I've noticed Christchurch house prices, for houses that are approx 4 to 6 years new, are selling at prices that equate to today's replacement price, ie cost equals value, which leaves very little margin for builders unless they strip more value from the house. Indeed many of these older new homes have have features that are absent from the same m2 homes built today.

Been looking for a family member currently in Christchurch, to find quality construction (to avoid EQ historical issues) plus good location in Christchurch is so hard ...limited quality stock to consider..compromise and still pay a premium is the current situation. So stats don't tell the whole story...

And no not everyone considers a new subdivision with water table issues issue further out a decent location...

Yeah, i tend to agree. A look at the chch HPI graph and it looks like it took a bit of a fall late 2016 and has been going sideways since then.

When you look at the data it all points in the same direction - the Auckland market is falling. Prices are down, volumes sold are down, inventory is up, days to sell is up. It’s just a question now how far and how fast the market falls. I’m inclined to agree with the small decline/plateau crowd but there is a case for a bigger decline. It is just lucky (or unlucky) that interest rates are so low. If mortgage rates were 2% higher we would be talking about a 20%+ fall.

thumbs up - a sober assessment based on data currently available ( rather unlike many other posts here .. )

If mortgage rates had been higher, people wouldnt have borrowed so much, and house prices wouldnt be as high as they are. Its all relative.

You were warned by me over year ago that the market in Auckland would be flat or falling and so it has come to pass.

Prices rising in small towns or in other areas is of little significance. Auckland relentlessly drives the whole market and it is foolish to think otherwise. Those other areas will also slowly flatten out and then fall under the gravitational pull of Auckland and the Australian/NZ banking system.

Get out of residential while you can and be happy with a smaller profit, or risk losing it all.

Many on this site have been warning and it's blindingly obvious this is only the start. NZ'ers need to understand that MSM commentary comes from vested interests..their opinions are nothing more than short burst of advertising - and so many have bet the house on this published rubbish. The real news is on this site and sites like DFA.

A rush for the exits will begin very soon....and the 30% drop won't seem very far fetched (oh except for Palmy and Chch i'm sure)

Agreed. The MSM have a lot to answer for. It is possible that they are genuinely brainwashed themselves, but that doesn't quite explain their stubborn avoidance when challenged. Pity nobody will get around to suing them....

The MSM are funded by their advertisers, which includes banks, real estate developers, retirement home operators, and others leveraged to the property cycle like retailers. You don't bite the hand that feeds you.

There is an issue across Senior Mgt in both Govt and Public. They earn well and are very happy with their lot. Further down the food chain joe middle class sees all sorts of issues (including inefficiently and dopey policy). But try and get something done and there seems to be zero motivation from above.....no one in these senior roles seems to give a hoot - "don't rock the boat baby I'm riding out time in my cushy position and want to keep it that way until retirement". Their lack of concern for the greater good is a disgrace.

Well done you did, your first warning was more than two years ago. But not matter how Big you are Big Daddy, you can't move the MSM.

Median price down 7.3% on the month.... Put your seat belts on kids. Lowest price in 3 years. I wonder how Tony A will spin this

Auckland City and Waitakere City still looking good. Never considered buying in the North Shore or South. Winning.

ZS, from your viewpoint (a speculators perspective), wouldn't this be a good time to buy on the North Shore whilst prices are falling? Do you now also think this is just the beginning of something much bigger whereas no area (except Auckland City - Waitakere) escapes the knife?

The Blacktown area in outer western Sydney is down over 20% already, so I certainly would not jump in asssuming parts of west Auckland won’t follow that.

.. yeah, I can't imagine North Shore City with medians lower than that of Waitakere lol!

Just confirms what many of us knew / suspected.

I think we'll see a further 5% drop this year, more if there is an 'external shock'

Auckland lowest sales since 2011! North Shore down about 3-4% over last 2 years, everywhere else in Auckland fairly static (up or down ~1% in last 2 years).

All the extra population since 2011 and now we have the lowest sales since then?

Interesting times.

House prices are falling and there is no recession. Growth is slowing in all economies and no ammunition for economic downturn. Imagine if we had a recession and people started loosing their jobs how will they service their absurdly high mortgage. Even if RBNZ reduce rates it won't bolster the housing market as joblessness will rise during a downturn.

Expect further falls in house prices this year...

"China has introduced jail terms for operators of "underground banks" illegally helping tens of thousands of its citizens transfer money out of the country to buy property overseas, in a move developers warn is a big blow to Australia's real estate market.

China's Supreme Court quietly introduced stiff penalties for illegal currency exchanges at the start of the month, in a further effort to stop capital from leaving the country. China's leaders want to prop up the slowing economy, stimulate the local property market and prevent a further sell-off in the domestic stockmarket.

The move, which imposes jail terms of five years or more for offenders, would target the operators of so-called "underground banks" which facilitate illegal foreign exchange and cross-border trading. Tens of thousands of middle class Chinese use the services to funnel billions of dollars out of the country to buy property in Australia, New Zealand, Canada, the United Kingdom and other countries."

https://www.afr.com/news/world/asia/further-hit-to-australian-property-…

Unless of course the gov't has a hand in it.....I doubt very much any factory can have any autonomy in a communist country.

Phil Goff created a massive step change in land availability and there has been a subsequent drop in land pricing - as was entirely predictable. Land over supply (sprawl in Auckland) is having it known downward effect on pricing. Lots of sprawl, lower prices.

I think the FBB and AML law changes, plus the insulation requirements and neg-gearing ring-fencing are far more likely to be the important factors.

And the fact that severe unaffordability ultimately reduces effective demand at some point

But those apply to the entire country and NZ prices are still going up. If those things are predominant the effect would be felt nationwide.

In Auckland has there been a massive increase in land supply and in Auckland there has been a price decline.

The rest of the county lagged Auckland on the way up, it'll lag on the way back down too. As the pressure to move from Auckland to find affordable housing dies the rest of the market will slow, then stall. Not sure if it will fall, or just stagnate.

I think pricing in the regions will be very sticky on the way down. If Auckland corrects big time and reverts to some sense of normality, those “refugees” who bought in the regions may see Auckland being viable again and look to sell up and move but will end up asking too much/being stranded with a house they struggle to sell.

Rest of NZ lagged Auckland on the way up, because early doors Auckland restricted land supply more than anywhere and increased rate of capital gain. And then late-2016 Auckland opened up a massive over supply of land and price started to decline, a decline even whilst high price growth is the norm across NZ. The lags did not occur due to mysterious forces.

Where is To The Point?

TTP goin' down in history

As the baddest spruiker there ever could be

RIP TTP, I miss your drivel! oh hold on, no I dont!

Probably trying to dump his properties

It's only a supermarket trolley, he can dump it in a river any time.

He’s walking around aimlessly (Ozzy Osborne shuffling) at the Palmerston North Metlifecare after they took his computer privileges away because his blood pressure was getting too high.

Couldn’t reply until now as I have been at 2 different auction in-house venues.

Did bid on 4 different properties and didn’t get any!!!

Doesn’t worry The Man one iota, as if I can not buy well under value then I don’t bother!

Actually have got one of our properties under offer this week, as not the best area, but did buy very well and have made a very good profit.

First house sold for a long time.

Don’t give a rats about Canterbury prices as our rentals are in CHRISTCHURCH!

The auctions today were very interesting with quite a few passed in but the ones that sold were achieving very good prices.

An old weatherboard home approx. 100m2 in an average area of Christchurch achieved over 600k so it does show that prices are holding up very well.

Property Bears can say and hope what they like, preach doom and gloom to property investors but at the end of the day, returns are very good and we are providing a necessary service to NZ!

Even for Canterbury being down $3000 over the last year is hardly devastating when they have gone up by plenty and if you are positively geared Rental wise, then what is the problem?

Nothing!

Dóh. "Christchurch also saw an annual decline in house prices. The Garden City’s median price was down by 0.7% to $435,000 in January, as compared to $431,900 in January 2018." Weird reporting, the numbers don't add up.

Saw that 600k old weatherboard and that was a bit over the top in my view. Not really a good purchase but previous owners bought it for a similar price only a few years ago. Only 50% sold at auction today though, market is pretty flat in chch.

Below mentions that is 35 months low

https://www.landlords.co.nz/article/976514341/auckland-prices-at-35-mon…

So the process has started and it is a wait for that that push to accelerate the fall...when it will happen to wait and watch... ..

They’re just merchants of doom and gloom.

Come on Nzdan the crash is coming.....wait for it......waiting......still waiting.......gee that retirement home is looking great.

Like any revolving door, it'll smack you in the back side when you are least expecting it!

Face the truth. Doom and gloom process has just started so fasten your seat belts.

Well, if we are to believe TradeMe there’s been another 100 Auckland listings added in less than 24 hours.

It may be that for the first time in a long while the key driver may not be interest rates, employment numbers, immigration, and economic strength etc etc – but instead, simply “supply”.

Dusting off Economics 101 – supply>demand =

I’m really interested in where the listings go from here. Can we crack 15,000 on Realestate NZ.

Is the bet back on...?

REINZ statistics are among the best we have but they are still pretty terrible really. Unfortunately they are telling a story on the surface that will create a self-perpetuating downturn. The headline says 'falling house prices', people lose confidence, then it becomes the loss of confidence itself that depresses prices.

Seems obvious but median price doesn't fall only because last year's median house is now worth less than it was, but in this case it's more likely due to a lot of new, cheaper properties being introduced to the market. In my experience, established dwellings are holding up very well, but when a suburb is flooded with new units and townhouses that is naturally going to reduce the median price.

If last year's median house was nicer than this year's median house, then a fall in the median price is not really symptomatic of 'weaker' market conditions but rather of the fact that the makeup of dwellings has changed. IMO this is what's actually happening right now.

Auckland's market is nothing like Sydney. People who bang on about how it is, and that similarity must extend to a housing 'crash', are either being ignorant or have an agenda. Beware.

Auckland may be about to undergo a transformation towards apartment and townhouse living that Sydney experienced in the 1960s and 1970s. Market statistics there are now broken down between homes and units for the simple reason that they are different markets and a single median price, like the one REINZ produces, can be very deceptive.

Our 'downturn' here, at least to date, seems to me to be more about introduction of cheaper properties than existing properties losing value. Yes, I see the evidence of it every day.

I live in the old Rodney district. Prices for existing properties are not dropping anything like what is implied by Auckland wide figures. What is happening, however, is a flood of cheap sections going in at Milldale, Upper Orewa, Red Beach and elsewhere - hundreds and thousands of sections going for $375k-$500k. Do you think that might have a little something to do with a fall in the median price where existing dwellings usually start at around $800k?

That isn't to say it won't become a fully fledged downturn for existing homes, but if it does my bet is that it will be due to a large extent to people misunderstanding what is actually going on right now and then acting based on that misinterpretation.

Well said am_fek, we are up in Puhoi and its business as usual. Nothing has changed really, you still need a good job and the ability to repay the mortgage. There has never been a bad time to buy in NZ if your in it for the long haul, 15 years later your always ahead in the game.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.