Auction rooms around the country remain busy, but the number of properties being offered at auction continues to decline from its peak in late February.

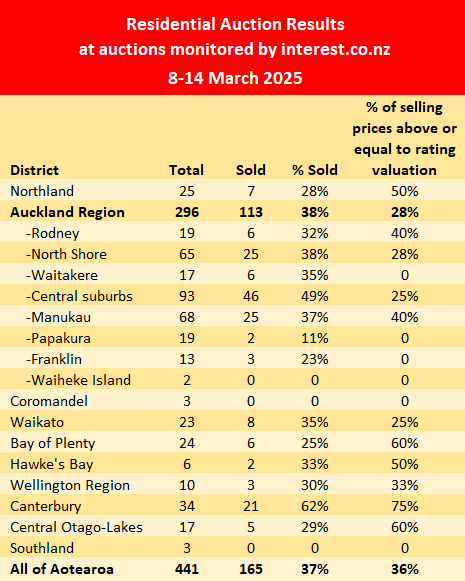

Interest.co.nz monitored the auctions of 441 residential properties around New Zealand over the week of 8-14 March, which was down from 557 in the first week of March, and 601 in the last week of February.

The last week of February was also the busiest week of the year for auction activity last year.

However, one thing that hasn't changed is the sales rate, with 165 properties selling under the hammer at the latest auctions, giving an overall sales rate of 37%.

The sales rate has been stuck on 37% for the last three weeks.

Buyers remain cautious on price, with just 36% of the properties that sold at the latest auctions achieving prices that were above or equal to their rating valuations.

Buyers were particularly price sensitive in Auckland where just 28% of the selling prices met or exceeded their rating valuations.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

11 Comments

Plenty of choice and plenty of FOOP. I guess the HPI is Tuesday?

Now we have a share market correction to go with a house price crash.

But its merely a flesh wound.

Yep. Spec town is bleeding any equity they have slowly but steadily. Youth still fleeing west. Even with a rate cut who is dumb enough to bail out the last bag holders. Rubber is hitting the road this winter and greater mortgages sales on the horizon.

by Yvil | 8th Mar 25, 8:40am

Peak auction activity generally occurs in March, it would be unusual for it to have passed already, even though numbers were down last week.

Its now the 2nd week of march and it looks like we have an unusual situation unfolding here.......... sort of confirmed by last years unusual situation

Interest.co.nz monitored the auctions of 441 residential properties around New Zealand over the week of 8-14 March, which was down from 557 in the first week of March, and 601 in the last week of February.

The last week of February was also the busiest week of the year for auction activity last year.

A very unusual situation, four cash rate cuts since July last year, 25, 50, 50, and 50. Many expected we’d be off to the races. "Survive to 2025" was the mantra.

Animal spirits require confidence, share market crash, job security Trump etc have destroyed it, massive number of listings and low sales rate means no one has to be in a hurry. They also require you to believe there will be a bigger sucker to sell to, prices have not dropped enough yet, right now, you are that sucker.

Following on the trump legacy.. additional10% tarrif (burden) on property values over winter...

Bank of America reveals the motivation behind Trump's reforms: One-third of GDP comes from fiscal spending, and 85% of new jobs rely on the government

Bank of America pointed out that the past growth of the U.S. economy has relied on unsustainable government support and protectionist policies. The Trump administration is attempting to shift U.S. economic growth from an inefficient, debt-driven government growth model to an efficient, self-funded private sector growth model. Bank of America believes this is a difficult but necessary process

To "detox," the U.S. economy is undergoing a painful but necessary transformation: shifting from an over-reliance on government spending to more productive private sector growth. Bank of America pointed out the driving forces behind the reforms in the latest research report:

The U.S. economy's dependence on government has reached unprecedented levels, with 85% of job growth coming from the government, government spending accounting for one-third of GDP, and a record budget deficit of 6-7% (excluding times of crisis and war).

Jared Woodard, head of the Bank of America Research Investment Committee, revealed the truth behind the apparent prosperity of the U.S. economy in recent years in the latest report:

"U.S. economic growth has relied on unsustainable government support and protectionist policies. As Trump attempts to shift U.S. economic growth from an inefficient, debt-driven government growth model to an efficient, self-funded private sector growth model, he is facing a high-risk gamble."

The Painful Transition from Government-Led Growth to the Private Sector

Bank of America data shows that a year ago, 85% of job market growth in the U.S. came from the government and sectors reliant on government spending, such as healthcare and education. Although this figure has now dropped to 70%, it remains at an unhealthily high level.

Even more concerning is that in 2024, government spending will account for one-third of GDP, reaching a historical high outside of wartime or crisis periods. This growth is supported by a budget deficit of 6-7%, which is exceptionally dangerous in peacetime.

Bank of America's analysis suggests that transitioning the U.S. economy from government-led to private sector will be a difficult but necessary process:

"The global handover from big government to free markets may be fraught with risks, but given the massive deficits and debt burdens, this transition seems inevitable."

Moreover, this shift is not unique to the U.S. According to the Bank of America report, the transition from the public sector to the private sector is happening globally:

In Japan, accelerated corporate reforms (buybacks and capital expenditures) are releasing ¥206 trillion (33% of GDP) to support the stock market rebound this spring.

In Germany, Chancellor Merz is preparing to lift the debt brake to fund €1 trillion in defense and infrastructure spending.

In Argentina, fiscal cuts worth 5% of GDP have balanced the budget, reducing inflation by 25 percentage points and boosting the stock market.

Painful but Necessary: Long-Term Benefits of Restarting the Market Economy

Bank of America acknowledges that accelerated private sector job growth, the relocation of government workers, widespread corporate profit growth, and global trade finding a new balance may take time, and the effects will not be seen overnight. This aligns with the views of Howard Lutnick, a member of Trump's economic team, who stated that Americans may not feel the impact of Trump's economic policies until the fourth quarter of 2025 Despite short-term pain, Bank of America’s conclusion remains optimistic. Analysts stated:

“The productivity gains that may come from the market's economic restart outweigh the risks, while the risks of maintaining a debt-financed, sluggish, and narrow economic growth status are quite severe.”

You’ve got about six odd months left of getting your jollies out property declines…then you’ll have to use “adjusted for inflation”, but it’s ok because you’ll get a couple of years out of that one 🤦🏻♂️😂

Pricing data relative to RV would be much more valuable if we knew the year of rating valuation for each district. Without that information it is of minimal use.

KeithW

Seeing a lot of listings from Oct 2024 - Jan 2025 still holding out for 2021 prices, great, since nobody is willing to pay that and the total number of listings continues to grow.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.