The number of residential properties listed for sale on Trade Me Property is the highest it has been in more than a decade, meaning buyers still have plenty to choose from at the end of the summer selling season.

Total listings on the website in February were up 12% on February last year.

"We continue to see supply outpacing demand, however the gap is narrowing with demand hitting a three year high and up 8% on February 2024," Trade Me Property Customer Director Gavin Lloyd said.

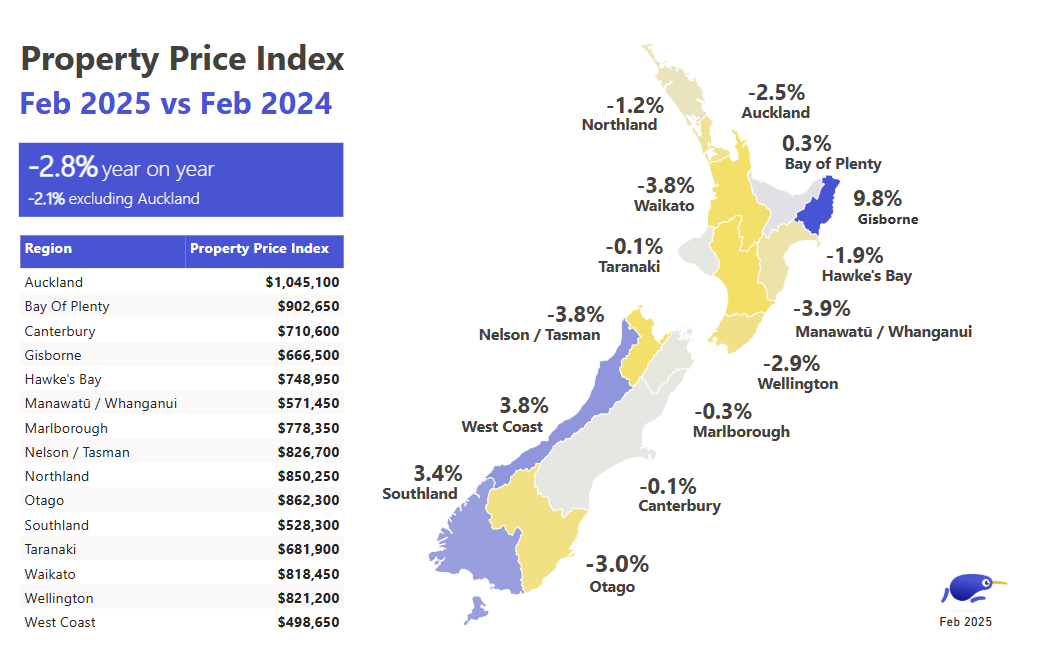

Growth of stock for sale was particularly strong in Otago where it was up 25% in February compared to February last year. Wellington, Southland and Canterbury all had annual stock growth of 19%.

The national average asking price in February was $851,500, down 2.8% compared to February last year.

Around the main centres, average asking prices in Wellington had the biggest annual decline of -4.9% compared to February last year, while Auckland followed closely behind at -4.3%.

See the charts below for the full regional asking prices and the price breakdowns by property type in the main centres.

The comment stream on this story is now closed.

58 Comments

The bad news for the housing market continues through the week..

Winter is not looking good for the tired and deflated housing market

I thought it was wonderful news, as per my earlier comment below.

Why do you think this is bad news ?

Glad you discovered supply and demand. So ???

Really, I have to spell it out for you? I gave you a link to learn. More supply puts downward pressure on house prices.

High stock levels on Trade Me Property giving buyers plenty of choice as the summer season winds down

I'm curious, after reading the article, what makes you think this is a good thing for property investors?

"More supply puts downward pressure on house prices"

Good on you for learning that, well done.

"what makes you think this is a good thing for property investors?"

I never said it was a good thing for property investors, re-read my post. Although it could certainly be a good thing for the property investors who are sitting on the sidelines and waiting to buy at cheaper prices. Why do you speak about property investors?

Then we agree prices are going down. I’ll try to remember this is your position in the future. Not sure if you’re the type to say prices are headed down but then call next month the bottom, or if the bottom is 27/28. So when’s the bottom, so I can buy at the same time as you?

The latest QV House Price Index Report shows the average value of New Zealand homes was $912,904 at the end of February. That's up 0.5% compared to three months earlier

After some pretty significant volatility throughout the past half decade, the housing market now appears to have well and truly stabilised

https://www.interest.co.nz/property/132351/despite-backdrop-falling-int…

😂🤣👍

A classic Nifty "been found wanting" post.

In this week's TV I discuss results from my latest Spending Plans Survey which show consumers are pulling back from their recent optimism about this year. I also look at reasons why it is unreasonable to expect average house price rises of 7.2% nationwide as prevailed from 1992 to now. In the interest rates section I discuss the uncertainties created by US tariff policy.

tonys view just out, got to be a hard sell once the professional Spruikers abandon your cause

I’ll start with the item which I feel overwhelms the others. Increased house supply.

On average since 1973 the annual number of consents issued for new dwellings to be built has equalled 0.62% of the NZ population. Following periods of high interest rates and recessions the proportion would spend time below that 0.62%.

For instance, in the 1991 recession the ratio fell to 0.5%, after the 1997/98 recession the ratio fell to 0.54%, and after the GFC it fell to just 0.31% in 2011. That low level explains why house prices surged so much after that event. Now, following our most recent recession the ratio has fallen to only the long-term average just over 0.6%. Supply growth is remaining good and that reflects changes in rules for land availability and intensification as well as incentives for borrowers to build rather than buy an existing property.

Good supply won’t cause prices to fall given the high cost of construction. But good supply growth as the cycle turns upward again for this ratio next year will constraint the pace of price increase.Second, while there is now a cyclical recovery in bank finance availability underway (easily seen in my surveys), there are more rules than before. These include LVRs (Loan to Value Ratios) and DTIs (Debt to Income rules). The impact of these rules is twofold. They force some people to delay their property purchase and encourage construction for those bumping up against bank lending limits.

Third, the rise in prices for the next three years will be constrained by the absence of the very low interest rates we saw for much of the post-GFC period. Now, following our most recent recession the ratio has fallen to only the long-term average just over 0.6%. Supply growth is remaining good and that reflects changes in rules for land availability and intensification as well as incentives for borrowers to build rather than buy an existing property.

Good supply won’t cause prices to fall given the high cost of construction. But good supply growth as the cycle turns upward again for this ratio next year will constraint the pace of price increase.

Second, while there is now a cyclical recovery in bank finance availability underway (easily seen in my surveys), there are more rules than before. These include LVRs (Loan to Value Ratios) and DTIs (Debt to Income rules). The impact of these rules is twofold. They force some people to delay their property purchase and encourage construction for those bumping up against bank lending limits.

Fourth, the extra rules imposed on landlords, ring-fencing of cash losses, ban on foreign buying, and natural aging of the population bringing selling by Baby Boomers and Generation X (born 1965-80) will mean less net demand over the cycles from investors.

My best guess for the next 32 years is that average house prices will rise by 5.5% - 6.0% rather than the previous 7.2%. Give me a call in 2057 to see if I was right. Actually, by then we'll probably have a communication device hardwired in our body and we'll call an incoming call a buzz. So, buzz me.

ITG, Are you quoting Tony Alexander, the one you and others used to call "The comb" and used to make fun of… when he was writing things you didn't like? A bit cynical for you to now quote "Tony", because you like what he says. A bit of integrity would be nice.

I was thinking the exact same thing…do I read Tony’s view and think “gah, what does that idiot know” like I have been told by so many on this website over the last couple of years…or is Tony no longer an idiot 🤷🏻♂️🤦🏻♂️😂

He is a legend in the Spruiker world.

https://www.youtube.com/watch?v=Ka9mfZbTFbk

he has shown us a sign.....

Classic Nifty posting current stats... sorry to disturb your DGM echo chamber.

Haha, then we got Nifty saying this is it. This is the bottom. Go buy yourself a townhouse in Christchurch then, they’ll probably pay your mortgage for the first six months.

"So when’s the bottom, so I can buy at the same time as you?"

Why should I help a condescending person, who assumes plenty about others, and then doesn't apologise for being wrong ?

You're wasting your time Yvil... the comments section is washed up with a few hardcore DGM left.

Whoop-Whoop! It looks like prices are likely heading south over the winter months. It's totally understandable if some are wondering where the finish line is. Like Yvil, I think an ongoing inventory glut with ongoing falling prices is wonderful news! Let it rip!

I don’t think you could get better news. We have a market that has choice. We have more buyers around meaning affordability is coming back on line thanks to the mix of cheaper funding, lower house prices and higher incomes over the last few years. Isn’t this exactly what we want?

A modest family home that a 26 year old can buy on a single income to start a family is what we should want.

Well, Houses Overpriced thinks it's bad news, as per her comment above.

Yawn. You know exactly what he/she means.

Yes, she means it's bad when prices rise and it's bad when prices drop. It's just her mentality, things have to be bad.

Why some people upvote themselves while paying $10 per month for the privilege of digging themselves into a hole is beyond me.

haha you tried that attack on me last night..... is it on page 2 of some Pollyanna handbook?

It wasn't an attack, just an observation. You've become very sensitive.

Maybe I'm wasting my time but I'll try.

At any given time, there are always good and bad events happening, sometimes more good, sometimes more bad. Each of us can choose if we want to focus on the bad, or the good or if we want to have a balanced outlook on life. There are unfortunately far too many people who revel in the bad, expect the worse and then wonder why they end up living a miserable life.

Lower prices for:

Food & Groceries = Good

Transportation = Good

Entertainment = Good

Healthcare = Good

Insurance = Good

Education = Good

Housing = Bad, Bad, Bad!

Yep, I've wasted my time.

This article of today is not about the same topic, but it's about a similar concept about each of us having a choice about what we think about. Maybe it will help some understand?

Lynda Moore says we can spend far too much time and energy worrying about things we can’t change

https://www.interest.co.nz/personal-finance/132374/lynda-moore-says-we-…

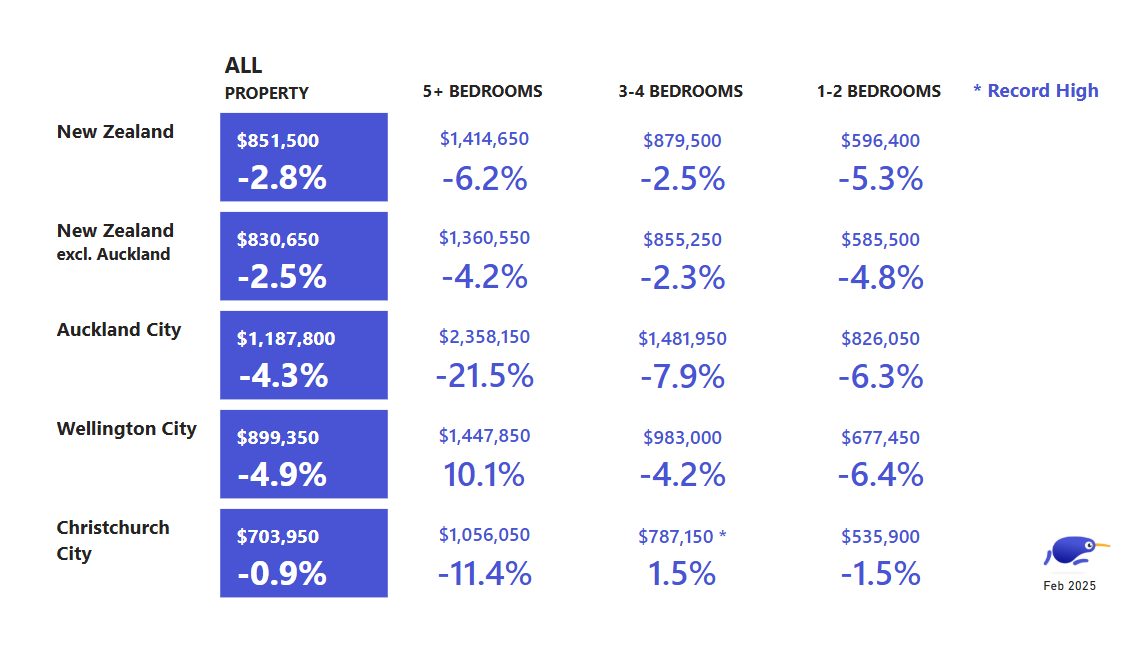

The rungs on the property ladder are compressing , ie the 5+ bd rms are falling higher % then the starter homes

Even in CHCH -11.4%, these will not be shit box houses.

AKL -21% and stil at 2.35mil

Spruikers are a little bit quiet this morning?

"Spruik that!" as Toye would say.

Indeed. Are they...

a) going cold turkey and not posting to avoid paying 27c per day,

b) been banned

c) struggling to divest their rentals

Regardless, the lack of endless spruik and people objecting to that has cleaned the comment up significantly.

You forgot:

d) Yvil not being able to afford his 17 other accounts ;-)

Nice to see a sense of humour. Well played.

PS I never though you had multiple acc's. Some clearly did and outed themselves in a senior moment by cross posting the same signature under different accounts.

Thanks.

Alright I'll have a crack(en)...listings will peak over coming weeks (classic March is the "time to sell"), activity will begin to ramp up (already happening) but prices will most likely continue downwards slightly (although didn't it rise last month nationally?), in the meantime the RBNZ will shit the bed (come on, they have a history!) with the OCR at 2.75% by the end of '25, sentiment will improve (is improving...credit card sales was slightly up too eh?) and with that job security will feel a bit safer...chuck that all in a pot and by this time next year(ish) with hindsight now(ish) would've been a great time to buy...or I am wrong, but you did ask 🤷🏻♂️😂

I really don't think we will see the ole double every ten years, I do think it is a cycle...lets see!

OCR at 2.75%? You w(ish).

It could be but don't wish for it, it would imply share markets have globally crashed with all the ramifications.

ie the average house in NZ would be about 25-30% off peak and your kiwi saver similar.

Global recession settings.

Bank of Canada cut to 2.75% today, but they’ve got tariffs coming at them left, right, and center. Going to be interesting to see what happens with their housing market. It’s going to be a toss-up between the UK, NZ, and Canada for whose market crashes first. Australia will follow 4th across the finish line.

Well played with w(ish) 😂…shit yes, I’d take a punt on it hitting 2.75!

We are still well in their contractionary range…the longer they sit above neutral (think they’ve called the NIR 3.0?) the higher the likelihood of needing to stimulate…makes 2.75 hardly a super wild thought…hell, 2.5 isn’t way of the mark…especially once the fed ✂️

I’d be far more worried about someone relaxing/removing DTIs/LRVs than I am about a 2.75 cash rate…maybe someone in a blue suit desperately trying to keep their job next year 😬

Gotta say the speculative money that drove Gisborne crazy is looking more and more like it came from Wellington. Also its not the up up and away in CHCH that some members suggest.

Is a return to mean underway, if yes there is still a fair bit of movement to unfold.

Wonderful news !

You forgot the champagne emoji 🥂

Why ?

Permabull property investors use the champagne emoji because there isn’t a cognitive dissonance emoji.

Well, then you should be able to work out that I'm not a "permabull property investor" then.

I believe you, you're in a similar camp to Zwifter. You can see the downside, but at the first sign of green shoots, you're thinking the market's off to the races. Maybe I’m still misrepresenting you, it’s hard to remember everyone’s view.

We're on the market, already bought the next place as I mentioned a few weeks ago. Not having much luck attracting the price we want. Looked at costs of renting it out. Same as we are already paying so now I have 3 rentals.

Woops

Nice troll. If not, then you made a bad mistake.

No troll, don’t think we are being unreasonable. I can take a lower today or put in some cash and it pays for itself.

Happy with what we’ve bought as it’s a personal goal to move into the new location. New one is same price as old one so we aren’t going up a rung on price.

Good on you then, GP.

In general what % below your view are bids being spoken of?

10% or so. It would take about 5-10 years to accumulate that amount renting it out. Have owned it over a decade.

Would prefer not to have another rental, but this is original house and we own the others which were added via subdivision. All standalone properties.

Trade Me is up 288 listings since yesterday, now showing 49,380 results. I’m getting that champagne emoji ready for 50k next week.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.