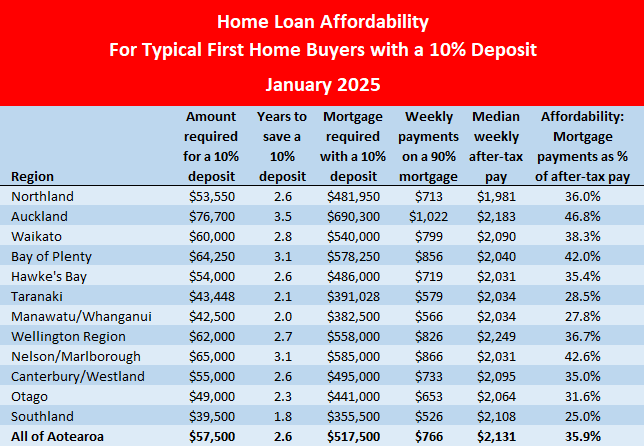

Affordability continued improving for first home buyers at the start of this year, thanks to ongoing declines in house prices at the cheaper end of the market, lower mortgage interest rates and marginally higher wages.

According to the Real Estate Institute of New Zealand, the national lower quartile selling price was $575,000 in January 2025. That was down $25,000 from December 2024, and down $95,000 from its peak of $670,000 in November 2021, since when lower quartile prices have been in a more or less slow but steady decline.

The lower quartile price is the price point at which 25% of sales are below and 75% are above, representing the most affordable end of the housing market.

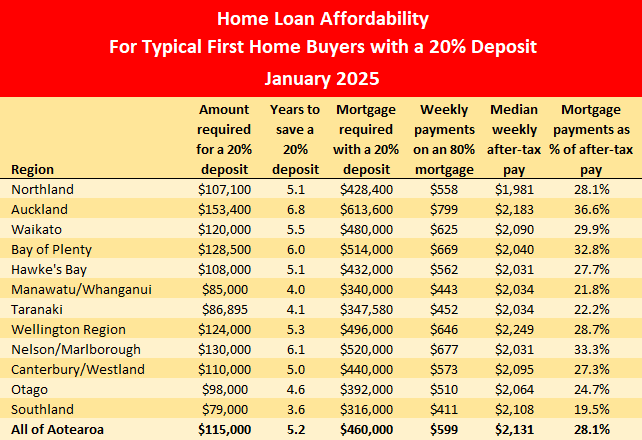

The decline in prices has seen the amount required for a 10% deposit on a lower quartile-priced home drop from $67,000 in November 2021 to $57,500 in January 2025, while the amount needed for a 20% deposit has declined from $134,000 to $115,000 over the same period.

Mortgage interest rates have also been falling steadily, with the average of the two year fixed rates offered by the main banks dropping from its recent peak of 7.04% in November 2023, to 5.45% in January 2025.

That combination of lower prices and lower mortgage interest rates has pushed down the mortgage payments on the purchase of a home at the national lower quartile price with a 10% deposit from its record high of $935 a week in November 2023, to $766 a week in January 2025, providing a saving of $170 a week.

Over the same period, the mortgage payments on a home purchased at the lower quartile price with a 20% deposit would have dropped from about $740 a week to $599, a reduction of $141 a week.

At the same time, incomes have been slowly rising.

Interest.co.nz estimates the combined, after-tax wages, of a couple working full time at the median rates of pay for people aged 25-29, would have increased from $2053 a week in November 2023, when mortgage interest rates peaked, to $2131 a week in January 2025, giving them an extra $78 a week in the hand.

Over the same period, the mortgage payments on a home purchased at the national lower quartile price with a 10% deposit would have declined by around $169 a week, while the mortgage payments on a home purchased with a 20% deposit would have declined by around $141 a week.

That means as a percentage of after-tax pay, mortgage payments on a home purchased at the national lower quartile price with a 10% deposit would have declined from 45.5% in November 2023 to 35.9% in January 2025.

Housing is traditionally considered unaffordable when mortgage payments exceed 40% of after-tax pay. So by that measure, home ownership has gone from being quite substantially unaffordable for typical first home buyers to well within affordable limits in the space of 14 months, even if they only have a 10% deposit

And the good news for aspiring first home buyers is that those trends are evident to a greater or lesser degree, across the entire country.

Problems persist

That's not to say that there aren't still problems.

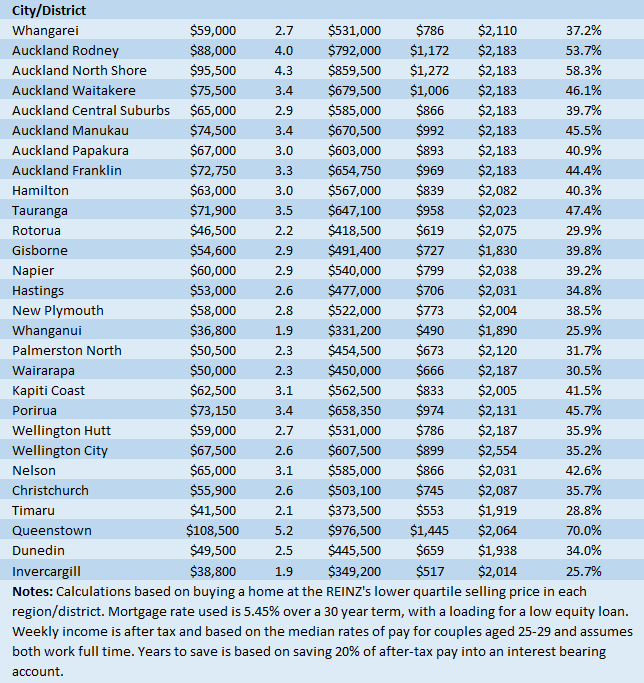

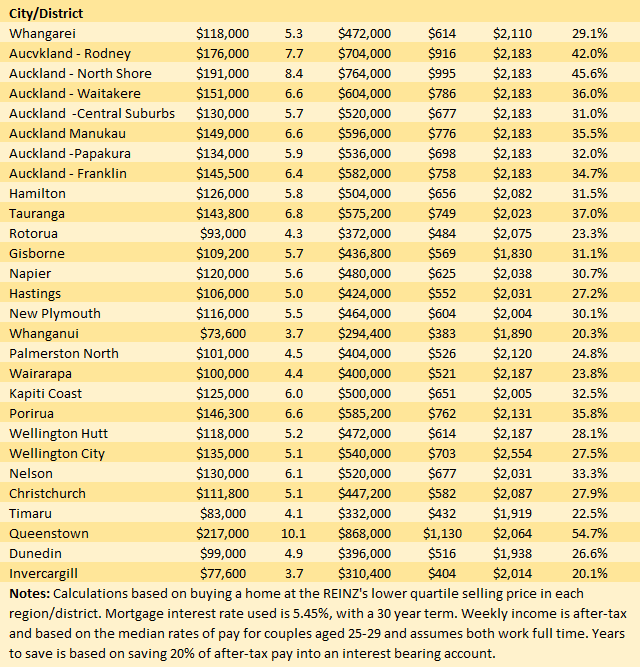

Although prices have declined everywhere, they remain high enough to keep housing in unaffordable territory for typical first home buyers across the entire Auckland region and in Tauranga, Kapiti Coast, Porirua and Nelson, while Hamilton is marginal.

And prices in Queenstown are so ridiculously high that home ownership there is simply not a realistic option for people on average incomes.

However the trend is clear, the prospect of home ownership is improving for first home buyers across the entire country, and the turnaround in affordability has happened in a relatively short space of time.

The tables below show the main affordability measures for typical first home buyers with either a 10% or 20% deposit, in all of the country's main urban areas.

The comment stream on this article is now closed.

85 Comments

According to the Real Estate Institute of New Zealand, the national lower quartile selling price was $575,000 in January 2025. That was down $25,000 from December 2024, and down $95,000 from its peak of $670,000 in November 2021, since when lower quartile prices have been in a more or less slow but steady decline.

SAVINGS 30 year 5% mortgage saving on 95k is $510 a month or $6,120 per annum

Interest + fees paid: $88,600

Principal repaid: $95,000

Total amount paid: $183,600

so buying now vs the peak will save you $183K in the long run. discount?

yes over life of loan.

its been 39 months since the peak, by not buying you have saved $4,707 EVERY MONTH

FOR 39 MONTHS

which illustrates how stupid the Spruiker bleating has been over that period......

I see what you're saying but most, if not all of the price drops were in around 14 months, so it's more like you would have saved $13K per month for 14 months if you bought in Jan 2023.

Jan 2023 is the current low point for Auckland, the rest of NZ has dropped around 2% since Jan 2023.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

Which also illustrates a point that in Auckland the current bottom of the market was in Jan 2023.

most, if not all of the price drops were in around 14 months

Do yo have any evidence to support this statement?

Yes, look at the chart i attached in the comment.

Learn from the teachings of The Prophet. That 2023 low will be exceeded shortly.

Currently that is not the case. neither of us will be here to hold each other accountable so it doesn't really matter what happens tomorrow, only what is the case right now.

When you cease to be a rookie you will understand that the low is already a hair's breadth from being exceeded and the trend is downwards.

If that curve was smoothed to a three month rolling average it would already be exceeded.

Your comment is filled to the brim with convincing arguments....

Smooth that curve to anything long term and you will see the trend is upwards.

A three month rolling average for property is sensible, it removes noise.

Smoothing out to four years is not sensible, it's the kind of thing a retard would say.

Ahhh yes, smart, financial performance of assets should be determined by the last 3 months, not the long term performance.

4 years? try 10, or 30 even, all of these are upward trends.

That's how the SNP500 became so popular, because Warren Buffet advocated it for it's 3 monthly rolling average....

you know someone has no real argument when they start insulting you.

I have never seen a Kiwisaver performance analysis commitee use a 4 year average....

Rookie, you are marked daily now days with weekly sessions of ball squeezing

you need to learn how the game is being played. I got out earlier in the week.

I told you about it, did you not listen?

5 year though?

are you suggesting i should follow you, i think not. each person makes choices on their own situation, yours is obviously different than mine.

You were claiming that Jan 2023 was the bottom for Auckland.

I was just pointing out that particular data point was noise that would be removed by a three month smoothing and that the prices are actually lower now (and still falling). The bottom has yet to be reached.

I am sorry that you find this upsetting.

it was the low point.

It was an anomaly, an outlier. The true low has yet to be reached. This will be revealed in the coming months.

But currently, it is the bottom, as far as we can see it.

The chart tells the story properly. New and sustained lows are going to be tested.

Only despair and misery await those who were lured by the fools gold of lousy Auckland property.

The chart tells the story properly.

Yep you're right there, the chart says we have seen the low.

"The chart tells the story properly. New and sustained lows are going to be tested."

Some people may be mistaking the difference between a bottom vs THE bottom.

Latest reported median is 0.6% above lowest price since peak in Nov 2021.

Time will tell.

CAVEAT EMPTOR

Brocky,

's the kind of thing a retard would say. I find that highly offensive though i was not the target. I suggest that if you wish to continue to post here, that you learn to modify your language. It's perfectly possible to express a contrary view while remaining polite.

I've been saying for a while houses are affordable for FHB, now we can see this is in fact true.

In some parts of NZ, but in Auckland the numbers above say if you have a 10% deposit the mortgage would cost you $1,022 a week or 46.8% of you typical income

I have never had to allocate that much to a mortgage ever....

Can your average FHBer afford $4,428 a month in Auckland?

what type of shitbox do you get for this in AKL

Honestly? Probably. It's all DINKs now. And at the margin it's less than you might think. The measure of affordability should be considered relative to paying rent. As a couple going from say $550 week rent to $1,022 is $472 more per week or $236 each. On a combined household income with two professionals in their early 30s/late 20s of somewhere around the $200k mark, they should be fine.

Others however may not, especially if you've got kids in the picture early and perhaps only one bachelors degree between you...

this is the exact profile that is leaving for aussie right now

in Auckland - buys a shitbox

In Brisbane - buys a standalone home

The DGM are here again - whinging and moaning as usual …..

But those who have bought a (first) home are happily and proudly getting on with their lives - ever so pleased that they ignored all the negativity.

Nonetheless, the DGM will continue on - in their relentless mission to brainwash the naive and gullible.

TTP

P.S. Interestingly, this site rarely (if ever) gets people expressing regret about getting into their first home. 🏠 👩🏼🤝👨🏻 Take heed, folks. ⚠️

Yeh - just like you never hear about a gamblers losses, only the wins. Its a big deal to admit you messed up.

I don't know what world you inhabit but there is a tonne of grief and regret for many who got into housing in the last few years. They are locked - they cant sell without loosing all of their equity and they cant even afford to transfer towns to a new job/promotion. The anxiety remains behind closed doors and for many ends in marriage failures and breakdowns.

This mess was created by complicit media, banks, politicians RE and other spruikers. Time to give it up.

Spot on...

We are led my a ship of fools, who care only about their short term gratification...

We need to bring back the gullotine, to ensure those in power do not abuse the privilege.

Rather than sending lambs to the slaughter house, it should be those that have created the current mess.

Interestingly, this site rarely (if ever) gets people expressing regret about getting into their first home

what type of person fronts up here and states I am happy that I am paying $510 a month for the next 30 years.....

you seem happy for them, what an idiot trying to cover up constant bad advice...

Have you ever been convicted of real estate fraud? it would be true to your online character....

In fact, there was a beautifully written post a couple of years ago expressing just that. (And I know the poster irl, they eventually gave up the house. Happily they were able to repurchase something cheaper).

You say: Interestingly, this site rarely (if ever) gets people expressing regret about getting into their first home. 🏠 👩🏼🤝👨🏻 Take heed, folks. ⚠️

Many FHB who bought in the last 4-5 years says : we are now in nagative equity, with much higher costs for everything (inflation) and unstable jobs.

FHB who didnt buy in the last 4-5 years: Pfew we were lucky. lets goto Oz and get a better house, better career, better public services and escape the crappy go-nowehere nz economy and crappy houses which are falling in value and these crazy ponzi drivers who have nothing better to do than talk up house prices..

DGM definition - a greedy person who tries to market young professionals overpriced houses in a crappy country with a crumbly economy..... when the economy and house prices are on a downward trend.

I can say that as a FHB I don't agree with this, although i do understand everyone's situation is different.

I have friends moving to Australia and renting their NZ home (bought at peak - now negative equity) in NZ for the sheer reason that they will be able to afford to rent, top up the mortgage in NZ, and still live relatively good lives over there given the level of income they can command in Australia. People o what they have to do to pay the mortgage, and Oz is a very easy option.

If someone is simply stating facts, can they still be 'labeled' a DGM?

Not trying to stop people from moving to Australia if they are truly struggling here.

But take a look at how many have crawled back from Australia after years wasted and nothing to show for it, except maybe a sunburn. Mindset is everything, but let’s be real, a Kiwi will always be a Kiwi in a kangaroo’s eyes. You can perfect the Aussie accent all you want, but spoiler alert, it’s not a magic passport to belonging….

So, how many have come back? I've heard plenty of anecdotes, and read the sad sob stories on MSM - but are actual numbers available somewhere?

It'd be interesting to see them.

Edit:

Over the last 10 years: 349k 444 visas nz->Oz. 233k 444 visas Oz->Nz.

So ~2/3rds have returned. Note however that is skewed by pre-covid, since 2020 the ratio is 40%.

So many factors unaccounted for here obviously (such as duration of stay, or if the returnees are aus-born children, or 461s).

From ABS:

https://www.abs.gov.au/statistics/people/population/overseas-migration/…

We all know that Auckland is well overpriced for what you get.

Immigration is what has caused it mostly.

Reality is that if you want a better lifestyle then you will need to move out of Auckland.

I'm with you on this, most here live in Auckland so that's mostly what they see.

I recommend Queensland.

For overpriced housing?

I do wonder what will happen to houses prices in that region if the Bendigo-ohpir project kicks off, 250 extra jobs in the region.

Queensland not Queenstown.

Queensland probably has a lot more kiwis anyway :)

Brocky, just back from holiday on GC.

If you think things are cheaper over there, you are delusional.

Housing, food every bit as expensive as Auckland.

Weather hotter, more storms but yeah if you think you can do better there, then book your flight?

I can assure you that, even after the house price inflation in SEQ over the past few years, you still get significantly more bang for your buck than Auckland.

Food is also of a higher standard and fresh fruit and vegetables are much cheaper. Alcohol and junk food are not.

Why do I need to book a flight when already live here in a lovely spacious home?

Sorry Brocky but you are 100% wrong.

Christchurch is better than wherever you are. I don't know where you are and neither does The Man but it is definitely worse than Christchurch.

I know this for a fact because the Williams Corp fanboy come on the forum everyday to tell people CHCH is better than anywhere else in the world.

Indeed. The secret is out!

In some parts of NZ

Actually in most parts on NZ.

They should have a 20%.

36.6%, still quite high.

I have never had to allocate that much to a mortgage ever....

Neither did people in the 1960's, do you think we should be going back there? 30% is considered affordable.

its mainly about what you get for the money - kiwis do not want the "affordable" product in Auckland... so are leaving for a better

"affordable" product in aussie

Surely as people move there it will only drive up prices in desirable areas?

Of course no denying many are still leaving for there, but that will only last so long before they're in the same situation as us, what happens then?

The rising affordability crisis is stark. Between 2002 and 2024, the house price-to-income ratio almost doubled, with the average house in Australia now costing nearly nine times the average household income. Rent has more than doubled over a similar period.

Both city dwelling values, including freestanding Brisbane houses, townhouses and and unit values are on the rise, crafting a robust housing market. Over the past three years, Brisbane’s median house value has jumped by 15.2%, with the median house price soaring from $650,000 in 2021 to $977,000 in January 2025.

Yes. Australia is on the same ruinous path that NZ followed, just a couple of years behind.

They are now discussing raiding their super to further raise property prices - ahem - give FTB a leg up. At least it's a restricted amount and their super scheme is good.

Interesting comment re:rents though, as rents largely track incomes - so that line is there as a diversion. Note average adult income has gone up ~2.5x in that same period (ABS).

Many who go to Australia do not need to buy a home. they can save significant sums from working and renting given the much higher income level there and reassess in a year or two where their financial position is at. Chances are it will be better than in NZ, and they will have been able to live less frugal lifestyles at the same time compared to their NZ peers.

Having moved to Oz over a year ago, my wife and I just reassessed buying this week.

Assuming we buy a property the same value as our rental with a 10% deposit (which only took a year to save), the interest alone is double our rent. Add on maintenance, rates, insurances.

Unless things drastically change [and they always could], we've decided to keep renting for the foreseeable future. Note we live in a better house than any we ever lived in in NZ, within walking distance of our kids school and my wife's work, and the train into town for my work.

PS. Don't get me wrong. Emotionally, we really really really want to buy. Atm, it's heads overruling hearts stuff.

Thanks for the reality, theMam, sorry, man will be shocked. One year to save a 10% deposit while renting a lovely home with no maintenance cost, rates, insurance people, and with a family. Does this not show how insane it is in NZ???

It's more affordable for FHBs, but unfortunately it's also more affordable for Investors...

MORE INVESTORS ARE THINKING OF SELLING

Investors have taken their biggest share of monthly mortgage money for nearly four years, latest Reserve Bank (RBNZ) figures show.

More investors looking to buy too apparently.

Touche'

It would be interesting to see an overlay of these "affordable" houses against job availability (as you note).

We only looked in one very specific sector - my wife's - and there was only 1 town in NZ affordable with jobs available. Taumarunui.

I don't mind living in the sticks - but - we moved from rural to Auckland as our petrol bill went past $200/week. Which was a significant addition to our rent.

Great news again - NZ is just getting better and better :)

safeashouses,

Great news again - NZ is just getting better and better :) It is just possible that you are being ironic, otherwise what you really mean is that the NZ property market is now slightly less unaffordable, but still grossly overpriced.

@linklater - thought the article said that its becoming more affordable - if you want to put a dark cloud in it no problems - I cant help you - i think even if you give it to people for free in NZ they will still complain, personally i also like people who complain they will not change their circumstances and keep renting - up to you -save yourself no one else will do it for you - I am of for a swim pool is 28 degrees xx

So Auckland is still unaffordable even if you only consider a 767k property.

Also, those median estimated after-tax incomes are probably dragged up by people living in Auckland where you need more money just to survive and it has 33% of the population.

His metric is all off.

It's actually 30% and it includes all ownership costs not just mortgage costs i.e. also includes rates, insurance, body corp fees etc..

By Greg's metric leasehold properties would be super affordable.

Thanks to the flawed credit creation theory implemented by banks and encouraged by the Reserve Bank, a FHB has to spend half their income to service a loan on a lower quartile house in AKL, forced to both keep working and delay having kids.

and if buying a low end shitbox, it will never provide capital appreciation to move to next rung of the ladder

because they will just keep on producing crappy low end shitboxes....

Not all FHB have a morgage to worry about . As i understand it immigrants are classed as FHB on their first house purchase in NZ

But on the positive side, this helps many an older speculator live beyond their own productive means with the following generations having the bill to pay! And surely that's what is most important for society!

It’s definitely a better time than a few years ago. I’ve just stumbled across a house for sale that I worked on. It was constructed in 2021. A rather steep building site, a lot of engineering involved to get it out the ground. Three bedroom, 2 bathroom 300sqm house, lower Northland on the east coast. The owner and now failed property developer built this for himself was crowing towards the end of the completion that local real estate agents think if this house was to be put on the market it would fetch in excess of 2.3 million. Fast forward a few years, it’s sat for sale for 1 year with no buyers, I now see it’s a mortgagee sale with an asking price of 1.1 million. This would be to be considerably less than cost. There’s some bargains out there!

yes I get interested in some things at 50% off.

Mangawhai?

That looks like a maintenance nightmare waiting to happen.

Well done. Thats the one. Some bad design calls on that house. Some are easy fixes, some not so much. If I was a braver man I’d consider buying it for the CG

Ooft 300m2 is the threshold for most insurance companies that kicks you into the upper bracket of premiums. Shouldda built it to 290m2 to save on ongoing costs.

I take it back 289m2 - they knew what they were doing? I didn’t know that rule. I’ll keep it in mind for my next house

Still massively overpriced no matter what..

NEWS FLASH!

The market has turned and the rush has started.

Ray White New Zealand scheduled 240 properties to go under the hammer last week, with a clearance rate of 51.6 per cent.

There was an average of two registered bidders and 1.7 active bidders per auction.

(Twenty years from now you will be calling these as the "good old days".).

I haven’t checked Ray White yet, but I find that 51.6% pretty hard to believe.

Barfoot this week:

Barfoot auctions - Tuesday:

9/21 = 42%

5/13 = 38%

2/7 = 28%

Total: 16/41 = 39%

Barfoot auctions - Wednesday:

3/25 = 12%

11/23 = 47%

0/1 = 0%

11/32 = 34%

9/23 = 39%

1/1 = 100%

2/3 = 66%

1/4 = 25%

Total: 38/112 = 33%

Barfoot auctions - Yesterday:

2/3=66%

7/16=43%

0/2=0%

0/4=0%

0/1=0%

1/1=100%

0/1=0%

Total: 10/28=35%

Barfoot auctions - Today:

0/5=0%

1/1=100%

Total: 1/6=16%

He was talking about RW New Zealand whereas barefoot only includes Auckland.

We all know Auckland is the lowest current performer.

Thanks RookieInvestor.

51.6 percent is a reasonable clearance rate but, in time, it will go much higher.

Much respect your pro-active and positive attitude, RookieInvestor. Your astuteness and intellect will bring you sizeable rewards.

This site needs more contributors like RookieInvestor, in order to sort out all the nonsense spouted here by the DGM dullards.

Best wishes to all aspiring property owners.

TTP

appreciate it, best wishes.

Backslapping spruiker lovefest.

Take care with which dawgs you lay with Rookster......convicted price fixers, masquerading as "responsible real estate agent"

https://www.landlords.co.nz/article/976513217/final-price-fixing-defend…

- You will get fleas!! - associating with the convicted.

Why do you care who I associate with? I'm a spruiker and you are a radical DGM

Lay with, whoever you please.

Their darkened, convicted brush will tar their bedfellows.......fleas can and do jump close hosts !

Housing is traditionally considered unaffordable when mortgage payments exceed 40% of after-tax pay.

I don't think that metric is correct Greg. It's actually 30% and it includes all ownership costs not just mortgage costs, including rates and insurance e.g. mortgage payments only would make leasehold properties super affordable.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.