First home buyers continue to play a remarkably steady role in the housing market.

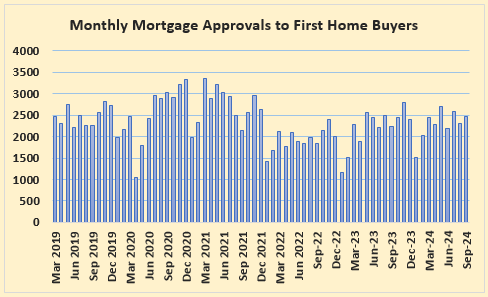

The latest Reserve Bank figures show there were 2469 mortgage approvals to first home buyers in September this year.

That's pretty much in line with where it's been since about March last year. Over the 12 months to September this year the average number of mortgages approved to first home buyers each month was 2344.

Numbers may pick up slightly as we head towards Christmas.

Over the 12 months to September the highest number of approvals to first home buyers was 2804 in November last year. The low point, leaving aside January which is a bit of a nothing month, was 2019 in February this year. See the first graph below for the trend.

Of course there are variations either up or down in the figures from month to month, but so far they appear to be remaining relatively stable at about 2500 a month.

Assuming most of the mortgage approvals were to couples, that's an average of about 5000 people a month moving into their own homes for the first time.

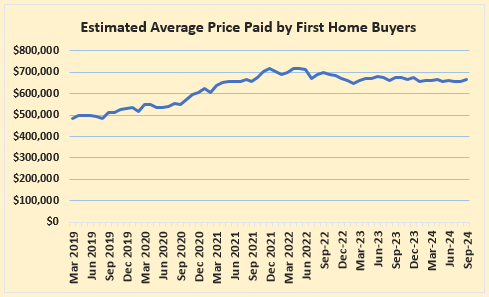

The amount of money they are paying for their homes is relatively stable.

Interest.co.nz estimates over the 12 months to September this year, the average price paid by first home buyers has ranged from $655,000 to $677,000, and was at the mid-point of that range in September this year

So although there are monthly variations, they are tending to be relatively minor. See the second graph below for the price trends.

That's not to say that first home buyers aren't affected by major disruptions to the market.

Like many others, they piled into the market when interest rates were slashed to next-to-nothing in 2020/21, which pushed their estimated average purchase price up to its record high of $718,000 in April 2022, but things settled back to more realistic levels pretty quickly after that.

For now the prices they are paying for homes appear relatively stable.

However, one figure that has increased substantially for first home buyers this year is the number of them taking out low equity mortgages to buy their home with less than a 20% deposit.

That went from 29.7% of mortgage approvals to first home buyers in February this year, to 38.4% in August before dipping back slightly to 37.7% in September.

That's almost back to the record high of 40.3% set in May 2020 when the Reserve Bank briefly wiped low equity lending restrictions altogether, as part of its economic stimulus package to shore up the economy against the ravages of Covid.

It's likely that we'll see an increase in both borrowing and buying activity by first home buyers over the next few months, helped along by lower interest rates and the usual summer upturn in activity.

However, indications so far are that the upturn could be fairly modest.

The comment stream on this article is now closed.

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

88 Comments

Congratulations to them, well done, lucky they didn't take the negative advice that comes up here regularly.

I doubt anyone has any objection to First Home Buyers who want to establish a family of some sort. That's how it's supposed to be in a civilised society.

What many of us have an objection to is property speculators who are aided-and-abetted by the institutional, short-sighted policy settings that will eventually ruin the country. A lot of people, whose only failure has been to be encouraged by the belief that property will make them rich by taking on Debt, will find out that the opposite can also happen. What we will only know after the event is when that happened.

"What many of us have an objection to is property speculators who are aided-and-abetted by the institutional, short-sighted policy settings that will eventually ruin the country"

Yes - in the existing residential dwelling market this is comparable where owner occupier buyers compete with non owner occupier buyers looking to rent out, this could be akin to concert / event goers trying to buy tickets but the ticket scalpers have bought them instead to resell to concert / event goers at a higher price. Obviously, the scalpers protest at any changes that adversely impact their economic activity or changes that restrict their ability to buy tickets to resell to genuine end users.

Lots of vested self interests involved (both financial and political) that prevent addressing the issue and effective solutions to the issue of affordability housing for residents.

For those that are interested.

Here is an example of out of town non owner occupier buyers, having been priced out of their own geographical market and moved to other geographical markets, have outbid local owner occupier buyers / residents in the existing residential dwelling market.

https://www.stuff.co.nz/business/property/117317608/how-a-town-changes-…

This went nationwide in most geographical locations so that house prices for many owner occupier buyers (especially first home buyers) were priced out of the ownership market.

If the interest deductibility policy had been entirely phased in at this time (i.e zero interest deductibility for non owner occupiers owners in the long term rental market), would an out of town non owner occupier buyer using equity release / deposit recycling techniques have made that purchase in the existing residential dwelling market? Less likely as the property may have become negative cashflow, potentially resulting in reduced buyer competition for owner occupier buyers in the existing residential dwelling market in that town.

Helped us in a way. Bought 2017 for $200k in Masterton just prior to things really getting stupid. Sold in 2021 for just shy of $600k.

When F U ,I GOT MINE, Is a national strategy, ( of which your example is a part), then the outcome effects all im the nation, right?

That's the shame if it.

Definitely. We had no intention on making that sort of capital gain, it was a house for us to live in and start a family. The market did some stupid stuff at a time we were ready to upgrade.

Could we have sold for less? Sure. Could the FHB offered less on our Deadline sale? Our BEO was $500k so yes they could've.

@ jimmyH - How about you lead by example then and either rent for life, so that another family may take your place and shot at home ownership, or you sell your home for next to nothing to help out the next family who wishes to own?

No? Unless your prepared to give up yours and your families financial position for someone else's family, it's rather hypocritical of you to stand there shouting the idea that putting one's families own interests before someone else's is somehow selfish. If you do in fact believe this mantra, then I look forward to staying in touch as my family would like to purchase your home for next to nothing - it would be a big help to us so thanks for doing your part in selfishly giving up your self interests for a family you don't even know. My children will thank you one day for it, though yours won't for squandering your families wealth.

Oh if only everyone who had more than me just gave up and stopped and gave someone of their stuff to me and to others like me, the world would be a better place. More equality right? This is Labourland hippy stuff.

Market observation

The non owner occupier buyers in the existing dwelling market have renewed confidence.

https://youtu.be/vB21bGuh8HA?t=24

Would the non owner occupier buyer be looking to buy if the tax deductibility of interest policy was entirely phased in (i.e zero interest deductibility for tax) for owner occupier buyers in the existing dwelling market?

The non ability to claim s legitimate expense for any business is just ludicrous.

If it remained and wasnt overturned, the consequences would be huge.

I got no problem not being able to claim interest costs but do not expect me to be paying tax on profits from rents!

"If it remained and wasnt overturned, the consequences would be huge."

What do you think the consequences would be if the previous policy on interest deductibility remained? (i.e interest deductibility in the existing dwelling market was zero, and 100% interest deductibility on new builds, and social housing providers)

@ CN - We already know what the consequences were & are if the previous policy on interest deductibility remained - you get faster rising rents.

The objective of this policy was to punish the purchasing of existing, and wrapping it up to sell it as an incentive instead for building new. This obviously didn't happen. You don't get a donkey through the corn fields by whipping it. Exactly why Labour failed. They failed to build their 100,000 ghost homes they were solely elected to build, & instead attempted to get investors to build them. Investors quickly realized that the numbers for return on investment just didn't stack up building, as building is far too expensive. If Labour wanted investors to build the homes they failed to build, they should've actually incentivized building such as removing gst off the build cost for anyone who builds. Not try to to punish those who buy existing with another form of tax. This was another failed dumb idea of Labour to add to their absorbent list of unintended consequences.

Instead, the non ability to claim interest added around an extra $4,000 - $8,000 per property to a landlords operating costs. Guess who ended up paying that? I'll give you a hint, it wasn't the landlord. Providing homes to those who cant provide for themselves is a business, not a charity. Its what you & Labour failed to consider. The additional costs to operate are past on, just like any other business, ultimately to the consumer, in this case the tenant. This really is just basic business & economics- they should teach this stuff in schools rather than the woke gender dysphoria stuff.

We can see the effects of such ill thoight out policies here: NZ median weekly rent according to Stats.co.nz

Oct 2017 $400

June 2023 $620

55% increase under 6yrs of Labour

Nov 2008 $310

Oct 2017 $400

35.5% increase under 9yrs of National

Rents increasing 20% faster under Labour in less time than under National

CN if you support lower home ownership rates, rapidly rising rents, more homeless out onto the governments emergancy social housing wait lists as you seem to, then by all means "attack the greedy landlord with every cost under the book". However, as the evidence supports, if you actually want to see more tenants into homes, you don't increase the costs or the risks for the landlord. It's just simply business & economics CN. Getbya head out of the Labour clouds, and back into reality. The envy train of "I dont like property investors as they have more than me & it's just not fair" is irrelevant. Facts over feelings CN. Sounds as though you could learn a thing or two off these property investors your so wound up about.

It's a bit of a stretch to call them "lucky" when they require a low equity mortgage to get into their first home.

Someone will probably come along shortly with their own false equivalence, claim that it's always been a struggle to get into one's first home, and how they had to take out a 2nd or 3rd mortgage to buy their home when prices were 2 - 3x the average annual wage and term deposit rates were north of 10%.

Ask the ones who purchased in 2021 what they think.

I suspect most will be really happy and house proud. It's not ever day a house comes up that you full in love with. If they are smart, they may have a few flat mates helping to pay the rent, while inflation eats away at their mortgage. It's mostly irrelevant what your house is worth until you want to (or have to) sell it (or leverage it). In a few years it could be worth a lot more. No one really knows for certain what the housing market will do short term however it's always been a great bet long term.

It's always been a great bet long term due to increasing population and falling interest rates. So really you are betting that those two things continue in the long term. I guess it depends on what duration you consider long term.

Interest rates have historically been cyclic. Population growth has been consistent over the past 70 years and projected to hit 6mil by 2050 according to Stats NZ. As to a definition of long term I don't really know however if I was to guess in about 5-7 years we might be near the next housing peak.

In 2021 were first home buyers (especially in Auckland) able to buy houses they fell in love with though? Or did they buy what they could afford in an area they may not have wanted to live in due to a competitive market fuelled by FOMO and low interest rates? After the excitement of buying a house wore off how many of them look at the property now and wonder if it was worth it, especially now they're looking down the barrel of a 25-30 year mortgage at higher repayments than what they had when they bought.

@ 26@Main - Ask any tenant if buying a home vs renting for life is worth it. Giving $600+ a week for life to someone else to house them vs the little extra per week for 30 years to house themselves. Yeah...it's absolutely worth it. Tenants can't sell their landlords home after 30 years of renting to help fund their retirement. What a silly question to even ask. Your not by any chance a disgruntled tenant who has in fact missed out?

The mistake people make is comparing ownership vs renting costs in the short term. When rents rise by 3 - 5% p.a. eventually (usually around the 15 year mark if you run some very basic numbers) the 2 intersect.

They also forget that a house purchase today locks in a capital value significantly higher than the renter's "investment" by way of initial deposit. A 20% deposit invested will need to return almost 30% p.a. to match a 4% annual house price inflation.

@ NZDan - Your not seriously trying to pitch that renting for life is somehow better for ones pocket than actually owning their own property?

One pays a mortgage for 30 years. With a bit of extra savings, & a clever set up mortgage structure, this could be less.than that.

One pays rent until one keels over. Have you factored into your cost analysis the difference between when paying a mortgage stops vs a continuous rent till one passes on?

Someone buys at 30, takes the maximum time to pay it off, has no mortgage by 60, then lives mortgage free till roughly the average life expectancy in NZ of 80, so for a good 20 yearz they have no mortgage. A renter at 60yo will still have to pay rent, even at 80. There's no discounts for pensioners. Even if we went by today's rental amount for say a basic 2 buddy roughly $450 a week give or take. Over 20 years that's an additional $468,000 that a renter will end up paying over and above someone who has brought & paid off their mortgage.

Worse than that, my mortgage was gone in 15 years now redo the math. In 15 years time your rent will have doubled, in 30 years time your rent will have tripled or more.

Did you read my comment? I was saying people look at the short term numbers and mistakenly decide that renting is better financially than owning.

Basically in agreeance with you....

Your reply is irrelevant Go Woke, buying vs renting for life was not discussed.

Congratulations to the 5000 new home owners, I hope you will be happy and settle into a great life.

Lots of things beyond home ownership that contribute or detract from happiness

"Lots of things beyond home ownership that contribute or detract from happiness"

Yes. Here are some that most people forget and take for granted:

1) personal health, and health of loved ones

2) personal safety and security and that of loved ones

3) loss of loved one - know several people in this situation currently

Some that recent owner occupier buyers could face:

1) loss of employment, and mental stress

2) cashflow stress from taking on too much debt to purchase a owner occupier residential dwelling

3) rapidly rising insurance and council rates costs

4) unexpected repairs and maintenance that are costly

5) residential dwelling is located in an area impacted by climate change

6) house price falls and the owner occupier goes into negative equity

CAVEAT EMPTOR

Well said CN. Home ownership after thought and preparedness to mitigate the many downsides that we have recently witnessed is more likely a pathway to lead to healthier living. The thought of speculators profiting from FHB's makes my skin crawl. Homes are for living in not speculating on. That said, in this market, still viewed as stretched affordability wise, I wish all FHB's well.

There need be no hurry to rush in to buy. Question the motive of anyone who spreads the fear of missing out.

DGM -

"We want prices to drop so FHB can afford a place to live.

Interest.co.nz -

"FHB making a move in latest figures"

Yvil -

"well done FHB for pursuing and achieving"

CN and RP -

Bad move FHB, we don't want you to have houses anymore.

Case in point folks. As I said above, "question the motive of anyone who spreads fear, the fear of missing out". It strongly suggests they're looking for a bigger fool on which to profit from.

Again, I wish all FHB's well.

@ Retired Poppy - Where do you expect tenants to live if rentals are not supplied for them?

Tenants still require to be houses by someone else until they themselves can save a deposit. Your surely not suggesting that everyone stays at home until they can purchase? Or that the government can house nearly half the country that rent?

If all investors left the market, that's not a guarantee that house prices would drop, Norris it a garantee that even if they did drop that tenants could still save the deposit required.

You havent thought any of this throigh have you? Just more envy waffle from the tall poppy crowd. There's no free ride in this world. Tenants must pay their way until they can afford to buy. That's not their landlords job to sacrafice their finances for the better of their tenant. That's entitlement & socialism.

Question the motive of anyone who spreads entitlement, tall poppy syndrome & actively disencourages personal growth & instead encourages handouts at the expense of others financial wellbeing.

"Bad move FHB, we don't want you to have houses anymore."

An incorrect interpretation.

Another property besotted poster being conveniently obtuse - LOL!

It’s not a pathway to living a healthier life at all. It’s almost completely irrelevant.

So essentially no different from renting then ? The one or two things that don't apply get swapped with a landlord putting up your rent every year and then deciding to boot you out because he is supposedly selling the place. If you are a practical person that can do a hell of a lot more than change a lightbulb then I recommend that you buy. 5000 a month agree with me, that's a lot of ticks.

Most start out renting or living at home and with the same discipline can save and enjoy financial freedoms in preparation of buying their first home. There are freedoms enjoyed when renting too. That's how we started out.

Oh - and Zwifter, when in self flattery mode, best you use words like "up votes" not "ticks". Clear thinking people are likely to have visions of you incessantly scratching yourself in search of pleasure.

All things equal, yes it’s nice to own. But it’s not the path to unbridled happiness. I know a FHB who bought at the silly peak, his household’s life has become a misery with interest rates soaring and his wife losing her job.

If they had continued renting their life would have been much easier. For a start, their weekly outgoing would be $400-$500 less

also, 5000 sounds a lot but how about all those who can’t buy? A much, much bigger number. And how many of those 5000 got help from mummy and daddy, a privilege many don’t have?

Sometimes it's short term pain for long term gain HM....

"All things equal, yes it’s nice to own. But it’s not the path to unbridled happiness. I know a FHB who bought at the silly peak, his household’s life has become a misery with interest rates soaring and his wife losing her job.

If they had continued renting their life would have been much easier. For a start, their weekly outgoing would be $400-$500 less

Unfortunately a buyer at the peak. For those who don't know and unable to see the financial consequences of that single decision to buy at the Peak.

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT") - Sept 2024

In 2021, the buyer who waited, deposited the same $260,000 equity into a bank deposit earning interest. Also BT would rent an equivalent house and have still saved money due to the rental being below the monthly P&I mortgage payments of Peaker - in 3 years the savings would have been about $20,000 annually. So a Buyer Today would have an amount of $340,233 to use as a deposit.

The current median house price for Auckland is around $950,000

Equity deposit of $340,233

The mortgage at this purchase price would be $609,767 (an LVR of 64%)

The Peaker has a mortgage which is higher by $430,233 (mortgage of $1,040,000 for Peaker vs $609,767 for BT). BT's mortgage is 41% lower than Peaker's mortgage.

Assuming BT, pays the same exact dollar amount each year that Peaker pays for their mortgage, as a result of that additional borrowing, Peaker is paying $1,232,229 more over the 30 years than BT (This is due to higher borrowing amount of $430,233, and total interest on this of $801,996 over 30 years). BT is mortgage free by the year 2037, whilst Peaker continues to pay their mortgage until 2051 (14 years later) - so after the year 2037, BT can save all that money that Peaker continues to pay on the P&I mortgage.

Assuming same incomes, and same living costs (food, travel, etc except mortgage) , BT can save the total $1,232,229 in payments that Peaker is paying. If BT invests the annual P&I payments that Peaker continues to pay after the year 2037 at 4.0% p.a, then in 2051 this amount will grow to $1,401,500.

Remember that at the end of 30 years, the house price will be EXACTLY THE SAME for Peaker and BT.

BT will have more money available for retirement than Peaker. Conversely, Peaker will have less money than BT at retirement.

That single decision to buy in November 2021 would have cost $1,232,229 extra to buy the exact same house for Peaker compared to a Buyer Today.

Those who fail to learn the lessons of history are doomed to repeat them.

Great analysis! But its all based on hindsight. I know of many who paid much more over the last 20 years by waiting.

"But its all based on hindsight. "

Yes, the lessons for the future are all learned in hindsight. People will continue to repeat the same mistakes in future.

A few people who knew where to look and what to look for could see the indicators of elevated house price risks. Some were giving warnings on interest.co.nz.

Reminder of the warnings given by the RBNZ governor on the elevated house price risks:

1) Feb 2021: https://www.stuff.co.nz/national/politics/300238808/reserve-bank-govern…

2) March 2021: https://www.stuff.co.nz/business/124430525/adrian-orr-frets-over-soarin…

3) Nov 2021: https://www.rbnz.govt.nz/hub/publications/speech/2021/speech2021-11-02

4) Nov 2021: https://www.1news.co.nz/2021/11/24/first-home-buyers-encouraged-to-wait…

In light of subsequent house price changes, these warnings now may have a different interpretation by readers.

These warnings were similar to warnings by Civil Defense of a high risk natural disaster (e.g tsunami, earthquake, volcanic eruption, flooding, high winds, landslip, etc). People who chose to ignore those warnings potentially face the consequences of their choice.

People are free to choose, however people are not free to choose the consequences of their choice.

People have been claiming elevated house price risks for decades. How can you know what to believe.

"People have been claiming elevated house price risks for decades. How can you know what to believe. "

When the RBNZ governor is giving warnings publicly, people should definitely pay attention. If the RBNZ governor is speaking publicly, then it is in extreme territory.

Trouble is,he was drowned out by the real estate industry shouting out buy now it will never be cheaper.....same as what they are saying today

"Trouble is,he was drowned out by the real estate industry shouting out buy now it will never be cheaper"

Yes. Those with their vested financial self interests with their profit motivated economic activities and large marketing and promotion budgets to create a fear of missing out in potential buyers by frequently repeating in the media the conventional mantras:

1) house prices double every 10 years

2) house prices will not crash, due to population growth and they're not making any more land

3) buy when you can afford it

Owner occupiers: CAVEAT EMPTOR

I know a FHB who bought at the silly peak, his household’s life has become a misery with interest rates soaring and his wife losing her job.

If they had continued renting their life would have been much easier. For a start, their weekly outgoing would be $400-$500 less.

Housemouse,

1) Do they regret buying?

2) With the benefit of hindsight, would they have chosen to remain renting back in Nov 2021 instead?

Yes to both questions

what makes it worse is that pretty much everyone said buying was a no brainer, that prices would only go up

HouseMouse,

Unfortunately the common belief by the general public was that house prices don’t fall by much, frequently repeated in the media by those with vested self interests.

At the time of their purchase, they would have been overjoyed at owning their own home rather than paying rent, they would have been congratulated by others as they got their foot on the property ladder as they could afford to buy. Given the situation that they are in now, they regret their choice to buy.

How much has the market value of the house changed (either upwards or downwards) since their purchase price in percentage terms?

Probably around -25%

"Probably around -25%"

Thank you HouseMouse for sharing that story.

Hopefully they can continue to make debt service payments and hold on.

So if they were an 80% LVR borrower at time of purchase, they would be in negative equity now on a like for like basis - their equity deposit and likely lifetime of savings has in less than 3 years evaporated and they would owe more on their mortgage than the current market value of the house. (Note: they may be in positive equity now only due to loan principal repayments which is not a like for like comparison).

Does anyone else have stories to share of owner occupiers being caught at or near the peak or others in cashflow stress? These stories are less likely to be reported, or fewer are reported in the media due to the vested financial interests involved.

@ CN - "Unfortunately the common belief by the general public was that house prices don’t fall by much"

It's not just common belief CN, it's fact. We have just had the largest property price decline in over 40 years, 20% drops accross the country, in just 3 years. In comparison under Arderns 6 years property prices rose over 94%. So despite there being the largest decrease in 40 years, property prices still remain 74% higher than they were 7 years ago, when Labour were shouting out it was a "national housing crisis". You conveniantly ignore this fact: That property prices in NZ fall much faster than they rise, however they rise for much longer than they fall. Property prices have not fallen further than they have risen in NZ for over 100 years. What you are crossing your fingers hoping, is that we have another 1920s property crash. Your already 100 years too late. The common belief that house prices don't fall by much is very much true. You only hope it's not because you yourself have a vested interest. Facts over feelings CN.

"those with vested self interests".

Whether one rents, owns, or owns multiple, everyone with a roof over their heads has a "vested interest" in property & it's prices. Your vested interest is that property prices decline "all the way to the bottom", what ever that is. Yet, hypocritically I doubt you would be willing to sell your house for significantly less than you paid for to "help the next generation out", when you finally retire. Don't pretend that only property investors have "a vested interest" in property prices. It's more likely that single home owners that are banking on their one & only home that have the most "vested interest" to ensure the home remains enough value to cover a potential of 20+ years of retirement, & of course who that don't own, tenants, that have the largest "vested interest" in property prices in the hopes that the prices come down so far that they're practically giving away properties out of charity.

Are you really sure that prices almost doubled from 2017-2023?

"In comparison under Arderns 6 years property prices rose over 94%."

FYI, REINZ median house price for NZ:

i) Nov 2017: $540,000 (previous government elected in)

ii) Nov 2023: $784,000 (current government elected in)

% price change: +45.1%

https://www.interest.co.nz/charts/real-estate/median-price-reinz

"property prices still remain 74% higher than they were 7 years ago"

FYI, REINZ median house price for NZ:

i) Sept 2017: $525,000 - 7 years ago - https://www.interest.co.nz/charts/real-estate/median-price-reinz

ii) Sept 2024: $781,000 (latest reported) - https://www.reinz.co.nz/Web/Web/News/News-Articles/Market-updates/REINZ…

% price change: +48.7%

@ HouseMouse - Absoutely sure.

QV & REINZ Property Prices show:

NZ median house price value

Nov 2008 $355,000

Oct 2017 $530,000

49.3% increase in 9iears under National

June 2023 $888,930

67.9% increase in 6years under Labour

Peak prices hit in November 2021 to median house price value $1,029,820

94.3% increase since Oct 2017

You don't seriously believe that the changes Labour made during their 6 years reign actually made property prices cheaper do you? If property prices by in 2017 were "A National housing crisis", and they have risen since that significantly, it must be A Labour catastrophy. You seriously didn't think they "fixed" the housing crisis like they were elected solely on the promise to do did you? Not another one that's drunk the coolaide.

"The one or two things that don't apply get swapped with a landlord putting up your rent every year and then deciding to boot you out because he is supposedly selling the place. If you are a practical person that can do a hell of a lot more than change a lightbulb then I recommend that you buy"

Each person needs to assess their own situation. People are in unique circumstances.

For owner occupier buyers, the purchase of a residential dwelling is the largest financial decision of their entire lives. This single purchase could represent 500 - 2000% (80-95% LVR) of their entire net worth and require the use of their entire lifetime of savings.

Most owner occupier buyers are unknowingly making this financial decision:

1) pay 5-10% higher rent?

2) lose 50 - 200% (due to high amounts of leverage) of their entire equity deposit due to potential house price falls? Remember that equity deposit is likely to be their lifetime savings.

Which would you choose?

Each person need to assess their own financial situation and housing market conditions for their purchase.

People are free to choose, however they are not free to choose the consequences of their choice.

Remember, the owner occupier buyers of Nov 2021 are now facing the financial consequences of their choice to buy at that time. Many are now in negative equity. Many will have large mortgages to continue repaying on a property that is 15-20% below their purchase price. There will be some that are unable to continue to meet debt service payments and have to realise the loss in equity - their entire future financial trajectory has changed and their entire future financial security could be at risk.

Those who fail to learn the lessons of history are doomed to repeat them.

Owner occupier buyers: CAVEAT EMPTOR

FHB's are also paying higher interest on deposits less than 20%. In this new normal of a flatlining market, that's even more dead money just because they apparently followed Zwifters advice not to wait.

What, 7-8% instead of the 20plus % we used to?

@ Mypointis - 20plus % interest rates on a 120k mortgage with a 5k deposit is not even remotely comparable to 7-8plus % interest rates on a 600k mortgage with 150k deposit.

Ask any tenant, or first home buyer, they would swap their 600k debt on 8% for 120k debt on 20% any day of the week.

Wouldn't they have to swap a 100K salary for a 10K salary as well?

Are you suggesting people were taking out $120k mortgages @ 20% interest rates on a $10k salary? The numbers GWGB are adjusted for inflation.

@ NZDan - The numbers are adjusted for inflation. When you could purchase a $120k mortgage @ 20% interest rates the income to total house price ratio was around 3-4x the annual salary. Compare that with today where house prices can be 8-10x an annual salary.

Again, I stand by my original statement, to say "we had it worse because our interest rates were triple what yours is now", is not even remotely comparable to today's interest rates given that wages have not kept up with inflation at all.

I think most people with half a brain would trade a larger mortgage with a low interest rate with a smaller mortgage and higher interest rate (assuming the cashflow remains the same). It's only Boomers with the incessant need to "one up" everyone everybody else's struggles that bring up the 20% interest rates on a loan of 1 - 2 year's wages.

@ NZ Dan - Totally agree. On the same page with this one.

@ Retired Poppy -

That scenario there are two options available:

1 - except the higher interest on a deposit less than 20%, and eventually one will accumulate 20% in which the higher interest rate can be dropped.

2 - except the higher rents on renting from the landlord. After all providing a house to those who can provide for themselves is a business, not a charity. Businesses exist to make money. When business expences rise, so must the cost of the service. Simple basic economics.

If it comes down to the ability to achieve ownership but at a temporary higher cost vs renting for life with known rent rises on their way, it's a no brainer which one should choose.

Are you sure your advocating for more home owners? Because for many the 20% deposit is out of reach, even with today's massive 20% drop in property prices. For many just starting out they will have to take what they can get, which may mean a 30 year mortgage instead of a 20 year mortgage, and may also mean a deposit size of less than 20% with a temporary higher interest rate. My god if my wife took your advice she would still be renting, blaming her landlord for why she can't buy a property.

"Lots of things beyond home ownership that contribute or detract from happiness" 1) 2) 3) 4) 5) 6)...

That's a bit of a sad reply CN, I was simply wishing the new home owners happiness in their new abode. I hope you have a good, happy weekend yourself.

There is no point arguing with some of these people.

CN

Basically don't buy a new home because its stressful...

then prices can drop and us investor can take them.

"then prices can drop and us investor can take them."

Thereby creating competition for other owner occupier buyers (who can only afford to pay and finance a lower house price) in the existing residential dwelling market.

Basically don't buy a new home because its stressful...

No. Each person has to do their own assessment based on their own circumstances. They need to consider and evaluate all the essential issues and avoid being potentially blind sided. I am merely highlighting some of the essential issues that need to be considered by owner occupier buyers.

then prices can drop and us investor can take them.

If that's not a frank admission that current pricing doesn't stack up for the "savvy" investor then I don't know what is!

The FHB are the most desirable buyers, they have cash.

Ask anyone selling how keen they are to sign up a sale to a conditional on sale of own home?

No one wants to sell conditional.

A lot of FHB's are ignorant to the power they hold as buyers, sucked in by real estate agents doing their job (they work for the seller children, not you) and media hype.

A lot of FHB's are ignorant to the power they hold as buyers, sucked in by real estate agents doing their job (they work for the seller children, not you) and media hype.

I don't believe they hold as much power as you suggest. This is war. They will be pressured to sacrifice themselves for the greater good. The last thing those who rely on the Ponzi want is for the marginal buyer to believe they wear the pants.

This raises 2 questions for me:

1. An estimated 60,000 people becoming owner occupiers. What is that as a percentage of the incoming generation + immigrants? I suspect very low, pointing at low future ownership rates.

2. How much room is there left for low equity mortgages? As I said the other day, OneRoof reported people were being turned down because the banks hit their low equity cap. I'd be keen to know the veracity of this, as our experience early 2023 was similar (our bank advised they simply weren't lending below 20% at that time). Is this still in the legislation? If so, I imagine it gets harder for the banks to lend at that level as existing equity reduces (assuming price drops > principle repayments in aggregate)?

However, one figure that has increased substantially for first home buyers this year is the number of them taking out low equity mortgages to buy their home with less than a 20% deposit.

The pressures they would have felt would have been societal--family, friends, and the narrative bandied around the water coolers and BBQs--so it is understandable that they throw caution to the wind. But now they've signed on the bottom line and the bottles of Spumante have been popped and drunk, they will feel accepted by society and affirmation that they've 'done the right thing.'

A family member recently bought a 2 beddy townhouse in central Auckland for around 700, then turned up to move in and got pats on the back as an identical one next door sold for 750 a couple of days later. Not sure what to make of that situation - the family member only just came inside their yield target range, so did they make $50k overnight on paper, or did the other buyer overpay?

@ Make Change - What difference does it make, when they now own the home, and have left renting behind?

Tenants who wish to own their own home aren't concerned about capital growth, or how much they paid or over paid. We know this as most first home buyers offer their max pre approval amount, instead of doing a little research on the property type, it's condition, surrounding area ect to find out whay they should be paying for the property. Most first home buyers aren't concerned about over paying, you'll never hear one say "yes we just brought a house, but unfortunately we well over paid for it and I'm not sure it was worth it". Every first home buyer, even if they acknowledge that hey maybe they paid a little more than they were expecting, it was well worth it, and had they have the chance to do it again, they absolutely would. First home buyers aren't motivated by bargaining the price down, or we would have much lower prices than we currently do.

They just want to own their own asset, a security without worrying about rising rents or the thought of one day being asked by the landlord to move on if they sell or move back in ect.

Purchasers who buy with either capital growth or cash flow in mind are investors.

Why not both?

It's priceless when some posters are hell bent on twisting sound advice that's intended to mitigate financial and emotional risk, to mean something totally detrimental. With less haste and more thought, home ownership is more likely to be a life changing step for all the right reasons.

Who really are the peddlers of doom and entertainment here?

Financial literacy is low. Most people believe commonly repeated mantras which can be incorrect. Here are a couple:

1) buy a house when you can afford it - (remember the buyers of Nov 2021 could afford it at the time? how were they blindsided)

2) there can be no house price crash because there is population growth and they aren't making any more land - what were the flaws in their argument? How were they blindsided?

3) house prices double every 10 years

Yeah there’s no way house prices can double within 10 years (or even come close to that), unless wages change by a similar magnitude. It’s pretty much an economic and political impossibility.

@ CN - Financial literacy is certainly low.

Why ever would you think the advice "buy when you can afford it" is bad advice? Your only quarrel with this advice is who it comes from- those who already own, and know just how hard it is to get there. Your suggestion of "don't listen to them, they know nothing & only scaring you", is about as sound as taking sobriety advice from someone who's never been under the influence before.

Of course you should absolutely buy when you can afford it. The banks heavy financial scrutiny well insures that a would he first home buyer can of course afford to buy. The banks check their bank statements, review their financial habits, request a decent deposit size, request evidence of regular savings history, & finally test the applicants approval based on a much higher interest rate than they would be offered. Up until recently that test rate was close to 9%, we have interest rates now in the 5% range. That means a bank has already tested a first home buyers ability to buy based an an additional $300 a week added to their mortgage. If a bank can test all of that, & still say your ready to buy, then your ready to buy.

What's the alternative? Rent for life? Wait for the opportune moment to buy? How many of those chicken little sky is falling property skeptics do we know? The ones that know it all about property, they're waiting for another 1920s property crash, and theyve been waiting since the 1980s for it. They think they're smart by waiting, but how much money have they thrown away every year to their landlord in rent, just to say they're smart? Think about it, wait for 5 years to buy instead. Pay average $600 a week in rent. Over 5 years that's $156,000 in someone else's pocket, while they wait for property prices to decline. Thats not very smart at all. The largest property price decline in over 40years has just happened. Property prices have dropped by a similar amount. If one can't recognize this is now the opportunity to buy, one likely will never buy.

The right advice, in most cases, no matter who it comes from, is if one can afford to buy a home. buy a home.

Doesn't matter how clear you make it, some on here do not get it. Perhaps they should just stay quiet because if the 5000 first home buyers this month turned up on here they would be silenced.

"because if the 5000 first home buyers this month turned up on here they would be silenced."

Let's hear from the highly leveraged first home buyers in Auckland and Wellington who purchased between February 2021 to August 2022 to share their experience and perspectives.

1) Do any of them regret their purchase?

2) With the benefit of hindsight, would they have preferred to rent instead?

Perhaps others know of some of these first home buyers like HouseMouse's story of their friends.

How many first hand accounts are we getting on here ? Yep pretty much none. Are mortgagee sales flying to the moon ? Errr no.

It would be interesting to see the FHB percentage in Auckland. Does that average mean they're buying flats ?

Averages don't tell a useful story without enough detail accompanying them.

"In September 2024 $140,800,000 was the amount withdrawn from KiwiSaver attributable to first home purchase" (IRD)

And the average age of those FHBers? 37.

Just 28 years left of their probable 45-year working life to replenish their retirement savings. Worse. The remainder of a 30 mortgage will still be hanging around the necks of some at the current retirement age. Yes, we have a universal retirement entitlement - at the moment. But if Australia is any guide, that's going to diminish to poverty levels at some time in the future.

Something's gone horribly wrong with our social values.

Inflation should take care of some of that debt burden, but still math is math. Borrowing 2 x your annual income at 20% p.a. is much better long term than 6 x at 6% p.a. Increase your repayments by 10%:

- The 2 x mortgage goes from 30 year to 12 years.

- The 6 x mortgage? Well it drops to 23 years.

This is where old people are so out of touch.

"Borrowing 2 x your annual income at 20% p.a. is much better long term than 6 x at 6% p.a

- The 2 x mortgage goes from 30 year to 12 years.

- The 6 x mortgage? Well it drops to 23 years."

Exactly. Most people are unaware of the maths that you have highlighted above.

Lower house prices (on a house price to income basis) results in owner occupiers being mortgage free in a shorter period, compared to owner occupier buyers in a market where house prices are high (on a house price to income basis).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.