New research by interest.co.nz suggests why residential property has been falling out of favour with investors, with negative cash flows the most likely culprit.

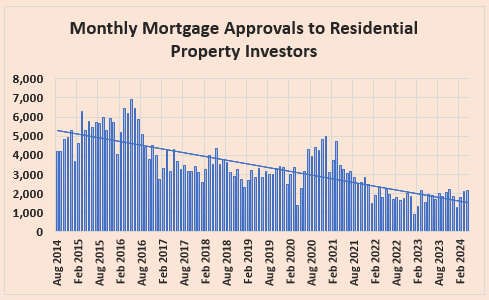

Reserve Bank figures show the number of mortgages approved to residential property investors has declined from almost 7000 a month in mid-2016 to just over 2000 a month in March/April this year. (See graph below).

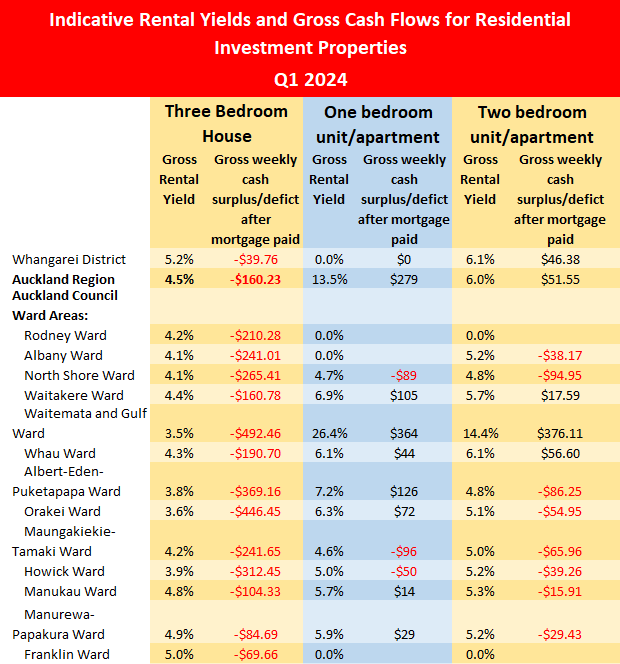

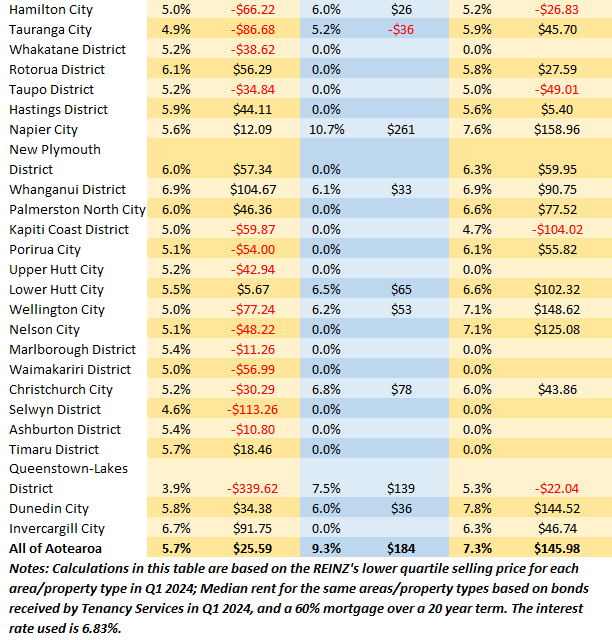

That represents a serious decline in investor activity. A new feature of interest.co.nz's Indicative Yield Table shows indicative rental yields have become so low that many rental properties would have seriously negative cash flows if they were purchased at the current lower quartile prices.

The yield table shows the gross rental yields that would be achieved for three bedroom houses, and one and two bedroom apartments or units, in all of the major urban districts around the country, if they were purchased at the Real Estate Institute of New Zealand's lower quartile price for the first quarter (Q1) this year, and rented at the median rent for that same type of property in each area.

A new cash flow figure has now been added to our Indicative Yield Table. This shows how much cash would be left for the investor after they had made the mortgage payments on the same property, assuming the property was purchased with a 40% deposit and the mortgage was for 60% of the lower quartile purchase price.

For example in Hamilton City, a three bedroom house purchased at the REINZ's Q1 lower quartile price of $629,500 and rented at the median rent for three bedroom homes of $600 a week, would have a gross rental yield of of 5%.

If that property was purchased with a 40% deposit, the payments on the 60% mortgage would be $666 a week, which is $66 a week more each week than would be received in rent. (The mortgage calculations were for a 20 year loan term with interest at 6.83%, which was the average of the two year fixed rates offered by the main banks in Q1 2024).

The investor would be out of pocket by $66 a week after making the mortgage payments, and that's before allowing for vacancy, insurance, rates, repairs and maintenance and any of the other expenses landlords can face.

So there's a serious cash flow issue there.

The same calculations for two bedroom units/apartments in Hamilton provide negative cash flow of $27 a week. One bedroom units provide a cash surplus of $26 a week after the mortgage is paid, but that is also likely to be a loss after outgoings such as rates and insurance are paid.

The numbers also show how difficult it is to achieve positive cash flow from a traditional three bedroom house in most parts of the country at current prices/rents/interest rates.

And although returns are better for one and two bedroom units/apartments, they are often still marginal at best. (The table below leaves the fields blank for one and two bedroom apartments/units where the number sold or rented during the quarter was too low to provide a reliable figure).

Traditionally residential property was seen as a way of providing a reliable income stream. But these figures suggest those days are gone and the main motivation in recent times has been the prospect of capital gains, turning investors into speculators.

With capital gains now also becoming a distant memory, it appears that residential property investment in the current market is increasingly likely to provide the worst of both worlds - potential capital losses and negative cash flows.

For residential property to regain its position of providing a reliable and worthwhile income stream there would need to be:

- A substantial drop in prices, or

- A significant increase in rents, or

- A major decline in mortgage interest rates, or

- A mix of all three.

The comment stream on this story is now closed.

Auckland Council Wards Map

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

148 Comments

It's true New Zealand, there are more productive things to invest in, other than property.

Such as?

It was a short list until last couple of years OCR, mge & TD increases

Pretty much every other investment is more productive, just historically not necessarily as lucrative.

It's easier and cheaper than ever to invest in productive businesses anywhere in the world these days.

kiwikidsnz : Such as?

Hmm. Why am I not surprised by such a statement - especially from a person whose understanding of tax seems to be limited to income tax alone.

There may be more productive things, but few are as tax advantaged as property

Step 1: Buy a house using loads of money from the bank at government mandated stupidly low interest rates.

Step 2: claim your interest payments as an expense even though most of it is offset via inflation.

Step 3: Sell the house and claim that your capital profit was an accident (you never intended to make a gain) and hence pay no tax

Step 4: keep the status quo in place by asserting any changes will increase rents.

Step 5: Increase rents to the max tenants are able to pay regardless of the reason

Step 6: Complain that FHB's need to cut back on avocado toast and work hard to save

(sarc)

Step 7: Claim you are a good Mom/Pop just trying to get ahead in life and you are doing a good deed by allowing people to live in houses built 70 years ago.

Step 8: Continue to bury your head in the sand and ignore all statistical analysis that confirms a) houses don't double in value every 10 years and b) the vast majority of properties return less than 5% per annum when measured on a gross nominal basis (which excludes insurance, rates, maintenance, inflation, etc.)

Step 9: Vote National as they are promised to look after you and protect your investment properties.

You can borrow against your house to buy shares. Currently you can get 7-10% dividend yields on a number of shares, making it not only cashflow positive, but interest will be fully tax deductible. And no capital gains either.

For the interest to be tax deductible, it needs to be in a company etc right? Would a bank lend to a company in that scenario?

As long as it pays a taxable dividend you can deduct the interest.

"And no capital gains either. "

Actually, no. Sometimes yes. Sometimes no. Be careful. Understand the rules.

And JJ - just to be clear - so long as you clearly identify your activity, as being a taxable activity, you may claim interest as an expense. Many people (including myself) have separate financial entities to ensure these taxable activities are separate and unpolluted by other activities. If you chose not too - that's allowed - but be very, very careful to keep the share trading separate in every regard to all other activities.

Driven by job insecurity, there's some evidence FHB's are pulling back too. There's certainly no need to rush. Yesterday, many who bought into the hype now find they have stretched finances and now find themselves selling into a weak market. Best advice right now is build a decent deposit so to reduce interest costs going forward plus it will put yourself into a stronger position to negotiate a premium rate with the bank.

For those who rejected the hype and waited plus want a house to live in and raise a family, things are certainly looking up.

Yep, a lot of potential FHBs looking now are those who were too sceptical and circumspect to buy into the FOMO storm. And seeing friends who did buy in get financially ruined has only reinforced their belief in a cautious approach. The final factor holding back buyers is the awareness that there are desperate vendors out there right now. Why offer anything more than a lowball when you know that, sooner or later, you'll find a vendor who'll accept one?

"And seeing friends who did buy in get financially ruined"

1) Can you expand more on those friends who were financially ruined? What are the lessons that potential owner occupier buyers can learn?

2) how are they coping mentally? Remember to check in on them and their mental health - they may need support.

Good questions - that seldom get asked on this forum.

Oh well, most rentals sold will now be bought by owner occupiers. Thats OK.

Except the low stock of rentals will make moving city very difficult if you want to move temporarily and prefer not to share with others.

We lived in a number of flats in Wn which were on a level below the owners. These felt uncomfortable. Too close to the beady eyes of the owners.

They are often in suburbs that OO don't really want, so prices may need to drop even further to tempt them....

or where current renters cannot afford, think Manurewa.... Maybe TPM can top up the deposits with pressie cards

think Manurewa

Property developer buys land at the peak looks like they will make a loss of over $900,000 before sales commissions and financing costs of over 2 years.

"Rawson said he had already taken a massive hit on the project. The total cost was $2.35m, which includes the cost of buying the property, subdividing, renovating both houses, putting in new driveways, connecting services, and upgrading the stormwater and sewer. He estimated he would be lucky to get $1.44m back."

https://www.oneroof.co.nz/news/real-estate-bosss-1-reserve-gamble-as-de…

I have so many questions about this. If this is illustrative for how savvy head of RE agency is then gawd dang

FYI, I think he is the owner of the local real estate agency franchise.

The cost of his build projects was huge!

Fewer rental houses means higher rents which, in turn, will encourage investors back - especially when interest rates start to fall.

Important to note, however, that interest rates could well remain relatively high for a good while yet, as RBNZ tackles its brief to combat inflation. All good, in my view. 👍

TTP

There seems to be an over-supply of rentals currently, abnormally high listings which do not paint the full picture of how many empty houses are sitting idle waiting to be sold/rented. Developments I've seen are listing less than half of their available completions. I see rents dropping in Wellington already.

I think the market is well and truly forked.

But that's all anecdotal, nobody with any regrets whatsoever, on our merry way. /sarc

"But that's all anecdotal, nobody with any regrets whatsoever, on our merry way."

Do you think that there is any regret by the friends of HGWR who bought and were financially ruined? /sarc

These buyers who were led to their current situation by the property promoters who repeatedly said that house prices won't crash?

If they didn’t post their personal regret in the comments section on interest.co.nz to their attention then it didn’t happen? / sarc

It was sarcasm, I too know people and know of people who have massive regret in their purchase.

During episodes of financial distress, it would feel like the bank is no better than Joe average greedy Landlord.

End of the days one simply acts as a risk buffer for the other.

Anecdotal also, but browsing rental listings of 4bdr homes close to Wellington city and I'm seeing nominal prices back at what look like 2021 levels - for what are often better quality homes. I'm starting to wonder if some of these are people who are migrating but don't want to sell because they plan to return at some point (so not your typical rental but a former family home).

I wouldn't be surprised if we see official figures showing a decline in rents for Wellington sometime in the next year.

Reports of a lot of accidental landlords. House not selling, put on the rental market.

Definitely looks like that. I'd say they're undercutting the professional landlords at this stage.

Compare this (https://www.trademe.co.nz/a/property/residential/rent/wellington/wellington/hataitai/listing/4750205308) with this (https://www.trademe.co.nz/a/property/residential/rent/wellington/wellington/newtown/listing/4749804910).

Both are 5 beds close to the city. The first looks like a former family home at $895/w, the second is the typical crap landlords offer to students at $995/w. Which would you rather rent?

p.s. That second property comes up a lot. I believe it might belong to one infamous landlord here in Wellington. Obviously can't keep a tenant.

Stark. I think the whole of Mudges street is either for sale or rent. Could be in a bit of trouble.

The infamous landlord owns 1, 2, 3, 6A, 6B, 8 and 10 on Mudges Tce across 3 titles.

Still has mortgages on them from since 1991

The infamous landlord owns 1, 2, 3, 6A, 6B, 8 and 10 on Mudges Tce across 3 titles.

Is that infamous landlord you?

I'm confidant that it's not. It'll be the same landlord that closed down Laundry Bar and left the building empty.

No

Wellington is a two tier market and heavily influences by university in central city. Rents on the larger central properties are down as enrollments are down from peak of 23k in 2031 to 20.5k last year and probable less this year.

There is a large amount of rental properties on trademe and they are sitting.

https://www.wgtn.ac.nz/about/our-story/key-statistics/pami-graphs2

Good comment and thanks for the link, I've now found other tertiary headcount figures, useful info.

There are a lot of those leaving who are renting out their house. Its not so much that they plan to return, but more that they want something to come back to in case they have to come back - ie. they dont get a job in Australia, or they lose a job in Australia and can't get unemployment benefits. Many are afraid that once they exit the property market they won't be able to afford to get back in later on. A few also only bought recently and selling would mean taking a loss, so they are hanging on "until prices recover".

However, considering that house prices in Australia are rocketing, they would be absolutely stupid to still be hanging on to their NZ property which is losing value and waiting to buy in a market that is going up, all the while paying ever increasing rents over there due to the huge rental shortage. Sell, put the money on term deposit at 6.5% and transfer it over when you've found a place to buy in Australia before you are priced out of that market as well.

"waiting to buy in a market that is going up"

"when you've found a place to buy in Australia before you are priced out of that market as well."

Rising prices certainly create a fear of missing out by buyers. That was certainly happening in Auckland and Wellington in 2020 - 2021.

If the market can't afford to pay the expected rent (which is already too high), holding costs mount.

And advertised rents will fall. Eventually, existing tenants will see cheaper lodgings elsewhere and they'll terminate ... And the cycle continues.

(I'm an optimist.)

Not to mention the on/off/on/...?

tax changes on deductible mge interest

Uncertainty in the private 500,000+ = 85% of NZ rentals can't be good for anyone

A CGT of 15% (owner occupier exempted) and both major parties agreeing to not muck round with interest deductibility and/or introduce a wealth tax would add a lot of security to the market. Buying property now is a role of the dice....who knows what will happen after the election in 2026. Maybe we will all have to start paying tribute to your local Iwi

Agreed.

Uncertainty isn't good for anybody. We run this risk of every 3-6 years flip-flopping between property investors having the red carpet rolled out, and property investors being persecuted (ok a bit extreme both ways, but you know what I mean). This constant back and forth battle makes it impossible to come to a sensible compromise.

It doesn't help that the property investment "community" likes to portray their business as a business when it's advantageous to do so, but then as some kind of social enterprise/mum and dad retirement saving scheme otherwise.

We now live in a society where, according to the likes of Stuff, selling videos of yourself online doing the kind of things that only Prince would sing about (hoping a few readers get the reference) is a legitimate business and to claim otherwise is casting unfair moral aspersions.

Even though I don't on rental property, and have no intention to do so, I don't think selling accommodation in effect is any worse.

However, let's just make it a proper business. Tax the underlying business model (the seeking of capital gains) make sure all participants are aware that landlording is a business all of the time - not just when it's advantageous to claim so - and let us move on.

negative cash flow = real time capital loss

No capital gain combined with HFL. With the dark veil of greed removed, some are starting to ask "what is the point". The difference in price between a yield value and the stupidity of speculation is very stark stark. People are asking the question "what is my risk"...?

Hot chilli on the popcorn oil...

That's including principle so you're paying off the house over 20 years.

Start with interest only to see actual profit/loss ignoring capital payments that increase your equity.

Looks like a few places, wanganui, palmy, welly apartments can still pay off the mortgage for you even at these high rates. You'll own the house outright after 20 years and it'll be worth a lot more and renting for a lot more by then too.

Property is hard to beat as a sure way to accumulate wealth.

"Property is hard to beat as a sure way to accumulate wealth"

Prior to Nov 2021, most people in NZ believed that an investment in residential real estate was a sure thing, and a couldn’t lose investment.

Many of the highly leveraged buyers of 2020 - 2022 period in Wellington and Auckland are going to learn the lesson the hard way.

Most mortgages are 30 years.

It's a long time.

A 1 off 20% drop in value will likely follow by multiple years over the 30 year term where prices rise 10%, 15%, 20% over a year.

In 30 years once paid off the property will be multiple times the value of the purchase price.

Time in the market, not timing the market.

More to the point, can specuvestor's stop being pulled underwater and drowning by the loss making enterprise while they wait for the 30 years to transpire.

"Time in the market, not timing the market. "

Many of the highly leveraged buyers of 2020 - 2022 in Wellington and Auckland are unable to hold on. That is the reason many are selling at below their purchase price.

This property developer is selling with losses of over $900,000 before sales commissions and finance costs.

Rawson said he had already taken a massive hit on the project. The total cost was $2.35m, which includes the cost of buying the property, subdividing, renovating both houses, putting in new driveways, connecting services, and upgrading the stormwater and sewer. He estimated he would be lucky to get $1.44m back.

Most Kiwi take mortgages at 1 or 2 year bites. The recent resets adding 100 to 200% to the holding costs, is a guillotine for the leveraged owners!

- Paying anything over 4.5% mortgage rates, is like a systemic Toxin for capital gains going forward.

With deglobalization and ongoing wars taking further hold, Rates are Not Coming Down!

The only future currently is major capital losses.....until 10% yields naturally appear.

In real terms I very much doubt we'll see peak prices again in this lifetime. Calculated recently a property bought would be 20 years in negative equity before turning positive, how many more years to recoup those costs? We're looking at generating income further and further into the future. Given <15% of under 35s own their own home, who remains to have the patience to wait 30 - 40 years to see a passive income trickle in? And in real terms, would it be any higher than rent today?

Capital losses on top of negative cashflow is driving you backwards every week, and then at the end of it all you need a greater fool to take on a worse bet.

Would rather invest elsewhere, anywhere. The future is tax in resi.

The average age of a property investor is 40-49 years. They dont have the time to be in the market for 30 years waiting for a payoff.

A 1 off 20% drop in value will likely follow by multiple years over the 30 year term where prices rise 10%, 15%, 20% over a year.

Those sorts of increases are going to look more and more like the aberrations they were as time goes on. I certainly wouldn't say it's likely you'll see multiple years with rises like that in the next decade or two.

"A 1 off 20% drop in value will likely follow by multiple years over the 30 year term where prices rise 10%, 15%, 20% over a year. "

Sorry. I have to call b.s. on that one.

I've been running an analysis of current sales prices minus last sale price and calculating the gross per annum nominal return when a dwelling is sold in much the same state as it was last sold.

Guess what? Even dwellings last sold 40 years ago are getting roughly the same p.a. return as those sold 30, 20, 10, or even 5 years ago.

The average gross p.a. nominal return is between 3% and 5% at this time. Very, very, very few get above 7.2% which justifies the 'houses double in value every 10 years' b.s. you hear.

I suspect we'd need to get to 20%+ mortgage rates, single income households, and a resettling of house prices to these new affordability parameters, before we can head back on a path of near 7.2% CAGR.

Either that, or incomes will rise substantially going forward to allow nominal prices to rise 7.2% p.a.

Property is a great way to take advantage of stupidly low interest rates via leverage. But if interest rates were to stay the same or worse go up over the long term (it’s possible!) then it could be a terrible investment that ruins your life, that leverage can make you really poor as well as really rich.

As an asset class, residential rental property has to sit amongst other asset classes that offer a return based on risk and reward.

Whoever in Govt. etc. has set the regulations for residential rental investment as an asset class has never looked at the balance of how that is achieved.

And in some ways this article continues that trend, in that you also have to look at ROI, not just whether the yield is negative or positive.

As with speculative capital gains, why would you fund a negative return if you can't make in up, and then some on the capital growth side.

In affordable home ownership and rental jurisdictions, return is mainly on yield, there is very little if any capital gain as the gain just tends to equal inflation, but since house prices are much more affordable, then rents can be higher on a yield basis, and yet still be much cheaper in real terms than what we pay in NZ.

I just compared the pricing and yield in a rental property I used to rent in Texas, and the rent is 1/3 less than a comparable property in NZ, yet the gross yield is 10%.

Property is doing that thing Wile Coyote does with his foot , just before he drops into the canyon below....

beep beep

But house price doubles every 7-10 years, it's low risk, and everyone needs a roof over their heads..

TTP fanclub.

TTP has taken a leaf out of the Combs book and is being very careful what he says now, he knows the great reckoning is coming....

TA posts his article on a Sunday, TTP regurgitates it Monday.

Don't forget the /sarc tag. (I almost thought you were serious.)

There's still cash flow positive investments in property for those willing to look. Try properties with minor dwellings in Auckland for example. Or try a different region such as Westport. Or buying a two bedroom home and renovating to a three bedroom with minor alterations. Yield is not everything. The advantage of property is not capital gains but that you can leverage your equity for more profitable returns in the productive sector.

Baptist, from an investors perspective and absent precious capital gains, yield IS everything. As properties continue depreciating, eventually the sums will stack even after galloping rates and insurances are paid. Due to lack of interest (or too much interest for that matter) there's still a ways to go.

No it isn't. As an investor my property portfolio currently earns me 0% capital gains and 7% net yield. But the real advantage to property is I can leverage my equity to invest in a productive business earning me 18%. Home loan rates are considerably better than business loan rates.

The idea that it is property investment vs productive investment is a false dichotomy.

That's unbelievable.

Your belief or unbelief in my portfolio is of no concern to me.

Yeah I can tell! 🤣😆

"That's unbelievable."

What is?

That Baptist only getting a 7% net yield?

Or using a rental property as collateral for a business loan?

Or that the capital gain is 0%?

I get better than a 7% net yield from my rentals (but I've probably owned mine for a lot longer, and maybe timed my buys well, while developing them into little gems). And I use them as collateral for business loans. Or immediate money for large sums. Likewise my CG for the last year is probably 0% too.

I can borrow at 6-7% by leveraging my property. If I were to apply for a business loan the base interest rate would be 13.77%. Frankly, I wouldn't be investing in the productive sector if it wasn't for my property portfolio. A number of people here dont understand this and think that property investing is creating a vacuum from productive sector investment. The opposite is true. Nearly every single small business owner uses property to leverage.

"Nearly every single small business owner uses property to leverage"

Given the deteriorating business conditions, this is a real worry given the state of the economy. Your revelation points to the potential for even more price downside for property prices. Saying you could get 18% net return investing in a productive business whilst leveraging your home is different to having actually done it and actually pulling it off - and during a recession too. But hey, on this anonymous forum, I get the impression as an individual, you feel compelled to spin it to convince others you can win it no matter what's happening in the real world.

Context. It worked for you xx years ago. Would it make sense now to invest in ppty?

No.

"But the real advantage to property is I can leverage my equity to invest in a productive business earning me 18%. Home loan rates are considerably better than business loan rates."

This seems to be a key motivation for business owners to use their properties as security for obtaining funds used to finance the business. The key risk is that if the business fails, then the business owner potentially loses their home.

I have seen it happen. Not pretty.

Saw it happen to close relatives previously.

They had to live in social housing for the rest of their lives as their entire life's savings were lost. They were in their mid fifties when it happened and the father had a mental breakdown. They never financially recovered. When they died, they didn't have sufficient funds for their funeral arrangements and the cost had to be covered by their adult children.

The adult children didn't have access to the bank of mum and dad for a deposit to buy their own home and 2 of them still rent.

I see it daily. House equity wiped out and so is the marriage. Each exit marriage, broke in middle age.

"I see it daily"

What line of work allows you to see it DAILY?

Insolvency? Receivership? Liquidator? Court system? Divorce lawyer?

Totally agree CN (and OldSkool). When you are putting your own home on the line, you only want to put it in a low risk investment. Like a business that you run in a stable sector. I certainly wouldn't advocate leveraging your home and investing in bitcoin. <Edit> Nor would I advise leveraging to the extent that they would lose their home if it went tits up.

For many peoples circumstances, however, it is better to invest big in low risk opportunities, than it is to dabble a little in high risk opportunities. Leveraging property can help make that happen.

"For many peoples circumstances, however, it is better to invest big in low risk opportunities"

Many people were willing to leverage 500 - 2000% of their entire net worth on a "low risk", can't lose opportunity leading up to November 2021. That was residential real estate in Auckland and Wellington purchased on 80% -95% LVR mortgage purchased in the period 2020 - 2022.

Now some of those highly leveraged buyers are going to be financially ruined - some of HGWR's friends.

Government bonds are the safest risk free / low risk investment opportunity, yet some buyers have been financially ruined buying these risk free / low risk assets - e.g. SVB Bank in the US.

You make a fair point. Low risk is not no risk. I am only leveraged on about 10% of my properties equity, so even if my business investment went its up ill cope.

How many will be unable to hold on?

CoreLogic data shows that 81 percent of homes bought by first-home buyers between October 2021 and March 2022 have dropped in value from the time of purchase.

About 18 percent, or 2000 first-home buyers, now have properties that are worth more than 20 percent less than they were bought for, indicating that any equity they had in the deal would probably have been wiped out.

Of those that are still more than 20 percent below their purchase price, two-thirds are in Auckland and 18.8 percent in Wellington.

https://www.rnz.co.nz/news/business/519396/thousands-of-first-home-buye…

There's still cash flow positive investments in property for those willing to look.

Rephrased: There's still cash flow positive investments in property for those who already have a portfolio with sufficient equity for them to afford to borrow against a.k.a established housing investors. New investors will not be as common as before, but those with already paid-off IP's or low mortgages on their IP's will still be able to go on the merry go round.

Yes. Existing wealth is always an advantage in any economy or sector. Just try playing monopoly when all the properties are already held by other players.

Love when anti-property commentators make yield assumptions and conclude that property is no longer viable.

May these articles spread far and wide.

My lowest yield on purchase ever at 7%, and that's in Mt Cook. 9-11% more common. Not getting those yields off the shelf, I buy run down, half-rotten old places, usually in a slump when you'd be mad to buy a property, and rebuild them. I don't do anything myself. So outsource to buyers agents, builders, project managers, architects, property managers etc. If you make the investment in knowledge and team, the investment of money tends to work out.

Yes but the NZ property market relies on the general punter chucking a bunch of cash at something and expecting it to give back. If that is no longer happening for Joe Average, then demand will wain regardless of whether there are anecdotal opportunities for those with the experience and equity to turn it around.

I'd expect greater yield opportunities in the future as the majority of people who buy property in NZ have absolutely no idea what they are doing, as is evident in the mad rush to purchase property during the peak, and all the pain that has followed.

More and more anecdotal evidence of "rent won't cover the mortgage, selling will cause a loss, what do?". Bleeding money.

nktokyo, the article is about negative cashflow turning off investor enthusiasm and you say you buy slums in a slump. This is really funny because there is no shortage of Spruikers on here who say you should NEVER time the market. If you outsource to buyers agents, builders, project managers, architects and property managers, they'll want their cut too - LOL!

Gross rental yield less than gross return in the bank. With greater downside risks in today's market, keep your $$ in the banks and wait.

Of course, cashflow is not good at all, but I still want to point out that your 20 year mortgage calculation includes the mortgage repayments. So you need to either: 1) take into consideration that, whilst the investor needs to top up the mortgage, he/she ends up with a mortgage free home after 20 years, or 2) remove the repayment amount from the mortgage, to get a true, accurate cashflow measure.

So kind of like an interest free savings account with no guarantee of income or gain?

I just did the numbers based on Greg's mortgage example for the Hamilton house. The gain is $378,000 worth of mortgage repayment, over the term of the loan (20 years) or if averaged out, $18,900 pa, which equates to $363 per week.

So kind of like an interest free savings account with no guarantee of income or gain?

No, like an interest free savings account with a guaranteed mortgage free house after 20 years, or, more specifically in Greg's example, a gain of $378,000, which is not a bad return on the $251,800 outlay to buy the house (40% of purchase price of $629,500)

Ok, but if I instead chuck that deposit into a savings account, and the $66pw negative gross cashflow, and the holding costs of the property, the interest rate on that account needs to be 1.4% to get to that same figure in 20 years.

So obviously, at the moment it's a bet on capital gains and rental inflation. I would not be taking that bet so willingly over the next couple of years.

If I instead find a 5% return (same return as the property) literally anywhere else, with the same deposit and negative cashflow figures I'd be sitting on $1.1m after 20 years. Would hit the target in just over 12 years.

Just to go further - even if the holding costs (insurance, maintenance, PM, rates) were $7k per year, that puts the gain on the property down to $240k. More importantly, to get the same return from a savings account, it's 0.4% pa.

So kind of like an interest free savings account with no guarantee of income or gain.

Drinking beer over 20 years doen't provide any return. That's the beauty of a P&I mortgage, it forces you to repy = save money, which, in the real world gets spent on consumables.

Oh ok - so IP only works currently if you're otherwise really shit with money. Which ironically you would need to be to even consider buying an investment property right now. Got it.

😆🤣✅

Sadly you haven't "got it" at all. Best of luck to you though Malamah.

No, I understand.

"so IP only works currently if you're otherwise really shit with money. "

There are many financially illiterate people in NZ who use investment calculations that lead to financial choices that can have outcomes that are undesirable.

Many don't even know what they don't know.

It worked then, but not now.

The business model was capital gain. And a negative cashflow was fine until the reward came at the end.

Anybody on negative cashflow was in the capital gain business, (despite denials) so must pay capital gain tax. It's the law already.

What about the $378,000 gained I mentioned?

DP

No, cashflow calculations are just that - cash flows. Not removing various amounts of them to calculate an "underlying" cashflow or accounting based profit. Cashflow is very simple - actual money in vs actual money out. What is left over? If you want to do it your way you could calculate it on a 5 year interest only mortgage, but then the tail repayments for the next 15 years would go up astronomically.

"If you want to do it your way you could calculate it on a 5 year interest only mortgage, but then the tail repayments for the next 15 years would go up astronomically."

Some borrowers are able to get interest only financing.

The non owner occupier buyer on interest only financing only needs to hold for 2 years and sell and no longer be subject to tax under bright line rules.

These non owner occupier borrowers potentially have financing advantages over most owner occupier borrowers and hence able to outbid owner occupier buyers.

Also the incessant govt interference

Instead the govt should be taxing the unproductive trading of shares between each other on the Stockmarket

32000 + homes on the market. Highest inventory since 2015. How many of those are vacant?

What happens next?

just did my numbers, basically the rent on my rental doesn't cover even interest, rates and insurance this year. and I bought the house 6 years ago and have paid big chuck of mortgage back.

I can see many investors will be in a painful position until some time 2026.

Now imagine how dire things would be if ~30% of the rent had to be handed over to the Labour Govt in tax first, before paying the mortgage costs and other expenses.

Yeah, you really wouldn’t want to pay today’s house prices as an investment would you? House prices could halve and people could afford to buy their own again, how dreadful.

Except that every home owner who needed to sell a home (due to death, divorce, job loss, changing location) would be forced into bankruptcy. Then you cant even rent a place. Had an American friend who got divorced after the GFC - if they sold the house both of them would be forced into bankruptcy due to the negative equity. My friend had to pay the ex $45,000 to KEEP the house and to take over the mortgage. People in NZ who wish for dramatically lower house prices have no idea, its like they werent paying attention to the disaster that happened in 2007-2010.

"Those who fail to learn from history will be doomed to repeat it".

oh well, the insurance and council rates alone is about $150/week for me.

Landlords is not cause of a problem, just an easy target.

Speculators are a large part of them problem, and if the rental income is so bad then most property investors must be speculators.

"Now imagine how dire things would be if ~30% of the rent had to be handed over to the Labour Govt in tax first, before paying the mortgage costs and other expenses. "

The restriction was on interest deductibility as other expenses remain tax deductible for non owner occupier owners. That would still put non owner occupier owners in the long term rental market at a cashflow advantage compared to owner occupier buyers who have ZERO deductibility for tax.

Should non owner occupier buyers have advantages over owner occupier buyers? Who should be given priority over owning a residential dwelling -

1) an owner occupier ?

2) non owner occupier owner in the long term rental market?

3) non owner occupier owner in the short term rental market?

The disadvantage of owner occupier buyers has led to the lowest rates of home ownership in NZ in many decades.

Would owner occupier buyers need to sublet rooms to earn Airbnb income to be able to afford the mortgage?

If these are purchased by non owner occupier buyers for rental in the short term rental market, then owner occupier buyers may be being outbid.

Would a capital gains tax on non owner occupier buyers prevent them from outbidding owner occupier buyers?

https://www.stuff.co.nz/business/350305789/queenstown-affordable-homes-…

Emergency coalition meeting is coming soon. Landlords urgently need another taxcut or some other form of government assistance.

Can't have poor chaps losing their dignity by not making obscene untaxed gains. There are still so many life saving drugs we can stop buying to fund that.

The assistance will come in the form of reversing the foreign buyer ban but foreign buyers will be subject to a tax on the purchase.

It was one of Nationals election promises.

A, Rent increasing need increase wages which leading inflation ➡️ B, interest go up and higher interest rate keep longer

RBNZ don’t want that happen and current government will not doing that, therefore only way to cure this problem is C, property price drop hugely till invest property turn to positive income.

also, that will largely lower living cost till our young people come back and invest in production is more profitable, the country back to right track.

Agree. It's a natural reset.

There was an extended boom time because the the ocr was dropped too far and excessive amounts of money was printed.

Nobody has a way to restart the boom without breaking something.. so we have to wait for things to run their course.

On a scary note.. I read this morning that the issue will be if AI starts to destroy jobs whilst the coming recession is ongoing... because the huge job losses will prolong and deepen the recession and there won't be an easy way to Kickstart a boom (if as businesses start to grow they don't hire much)

AI starts to destroy jobs

How many net jobs have been destroyed some computers came along? AI isn't magic, the amount of jobs I see being created in the industry will boom.

Exactly. Rather than replacing jobs as predicted back in the 80s/90s the consequence to workers following the productivity gains of computers and digitisation has simply been a requirement to be more productive for the same pay.

Don't see why AI will be any different.

Fear of blood loss found to be a key reason people avoid being stabbed

Anyone pondering what the no consent required for a secondary 60sqm dwelling will do for housing supply?

Supposedly a change in the RMA coming up. If this gets passed another nail in the coffin.

Which is why I suspect it wont.

I suspect this will put a lid on prices rather than depreciation. It will provide fast easing to rental congestion. Much like the unitary plan change did to Auckland.

You'll always need consent to hook up 3 waters. Otherwise it would be carnage.

And meet the setback requirements from the boundaries too?

The proposal is no consent, just engineers report.

The Labour governments war on landlords.

Change of government has helped.

But they will be back and pick up where they left off guaranteed.

You would be very unwise to be owing money when they do.

Maybe residential property 'investors' have been listening to me when I've said recent changes to zoning rules both nationally and regionally will ensure more dwellings - of many different types and entry points - can now be built to meet demand and the days of absurd untaxed capital gains are now long gone?

Maybe they've also figured out a Capital Gains Tax is now inevitable and the only thing to argue about is what form it takes? Some - including me although I'll have to pay it - will relish the prospect that it gets backdated to 1900.

Just out of interest, what would non owner occupiers do if a CGT was imposed?

1) Sell before start date of capital gains tax?

2) hold and never sell (especially those owned by trusts and other non natural owners) - [would this reduce the number of existing residential dwellings listed for sale?]

3) other

It might depend on whether the property is low yielding or high yielding and the motivation of the buyer. (i.e income oriented buyers vs capital gain oriented buyers)

Sorry CN.

I really can't even guess unless I know roughly what form a CGT would take.

Just about every country has a CGT. But all are different. Some vastly so. And many, the tax rate is so low (artificially, as they too bow before rich people) that it really doesn't have any significant effect. Further, the list of inclusions / exclusions with each CGT - usually at the whims of vested interests - are significant and complicated.

These two I can sort-of answer ...

1) Sell before start date of capital gains tax? ... Why I suggested backdating to 1900 ... [evil grin] ... It becomes inescapable and revenue is generated almost immediately so PAYE rates can go DOWN almost immediately too while giving workers more choices about how they spend, save and invest. The downside is mass confusion (kiwis are terrible at maths) as people try to figure out what things are currently 'worth'.

2) hold and never sell (especially those owned by trusts and other non natural owners) - [would this reduce the number of existing residential dwellings listed for sale?] ... Liquidity is always going to be a problem if the CGT rate is set too high. Or if a new CGT is widely hated and it becomes inevitable that a future government will repeal / adjust it.

The first CGT in NZ must follow IRD general principle of low rate and wide coverage.

Thank you for sharing your perspective.

I wonder how many on this forum understand that, in Greg's example of the Hamilton house, the buyer more than doubles his money in 20 years, without accounting for any capital gain?

"the buyer more than doubles his money in 20 years"

How so?

In Greg's example the buyer pays $251,800 for the Hamilton house (40% of purchase price of $629,500) and he/she ends up with a mortgage free house after 20 years, a gain of $378,200 (because Greg included principal repayment in his weekly mortgage expense of $666).

As proved above, when not accounting for inflation or capital gains, it's a 0.4% return.

You need to consider future gains and inflation to really be making any kind of assumption like this. Both capital and rent seem to be about to track downwards, at least here in Wellington, so yea, 5% in the bank wins.

I'm making no assumptions, it's simple maths: $629,500 - $251,800 = $387,200, no assumption there.

You're making the assumptions when you guesstimate "Both capital and rent seem to be about to track downwards"

Yes, I never said I wasn't making an assumption.

Your assumption is that just because they hold the house mortgage free, that entire $387,200 is a gain. Which, by the numbers I have provided you with, it is not. The investment makes a 0.4%pa gain. The rest is invested by the investor. So basically an interest free savings account.

All else is reliant on capital gains and rental inflation > income, which is speculation.

FYI,

Using the same methodology, for a buyer at the peak for Hamilton (by applying the 25% price fall in the REINZ HPI since the peak for Hamilton), the annual return was -0.13% p.a for 20 years, so all the returns were rental growth offsetting expense growth, and tax free capital gains.

Most highly leveraged buyers at the peak did not see that.

One property accountant was using capital gains of 6% p.a.in their calculations based on extrapolation of historical house price gains.

Well, no surprise here. Most people I know who bought a house recently are paying over market rent in terms of their mortgage repayments. But they're all young couples who value having a home of their own over a home as an investment. They've also said investors are gone from the open home circuit, likely due to this negative cashflow situation. There was an article on stuff recently about first home buyers having their deposits wiped out - I was super curious as to how many investors have had their deposits wiped out, as they tend to be even more highly leveraged. Once again, media conspicuously quiet on this issue.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.