Moving up the property ladder into a better home is probably still a realistic prospect for most existing home owners, despite the decline in property values that's occurred since the peak in 2021.

As well as tracking affordability for first home buyers in our Home Loan Affordability Reports, interest.co.nz also tracks how affordable it would be for them to move up into a more expensive home after 10 years of first home ownership.

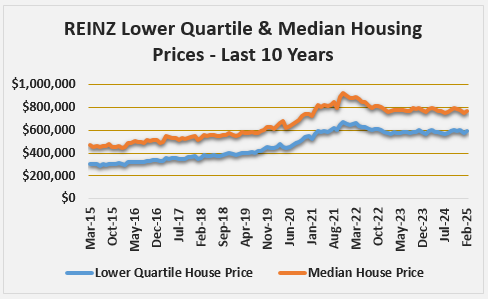

Ten years ago, in February 2015, the Real Estate Institute of New Zealand's national lower quartile price was $292,000, while the national median price was $430,000, a difference of $132,000.

Or put another way, the median-priced home was 45% more expensive than a lower quartile-priced one.

Ten years on, in February 2025, the REINZ's lower quartile price has increased to $595,000, while the median price has increased to $772,000.

In dollar terms the difference between the lower quartile and median price has increased to $177,000, but in percentage terms it has decreased to 30%. The graph below shows the trend over the last 10 years.

So how achievable would it be for a couple who purchased their first home at the lower quartile price 10 years ago, to now move up to a home at the current median price?

The figures suggest it should be very achievable.

If they sold their first home at the current lower quartile price of $595,000, interest.co.nz estimates they would be left with equity of $384,515 in cash to put towards a new home purchased at the current median price of $772,000. That gives them a deposit of 50%. (See the note at the bottom of this article which explains how that was calculated).

It also means they would need a new mortgage of $387,485 to purchase their new home for $772,000.

At the current average two year fixed rate of 5.09%, and assuming the new mortgage was for a 30 year term,* the weekly mortgage payments would be around $485 a week.

Based on the median rates of pay for couples aged 35-49, our second home buyers would take home around $2413 a week between them, after tax.

Which means the mortgage payments on their new home would eat up just 20% of their take home pay.

That's affordable in anyone's language, and helps to explain why moving up the property ladder is such an important part of this country's housing market.

So while some potential movers may be hesitant about trading their existing property for a more expensive one because of the slump in property values over the last few years, the above figures suggest the numbers still stack up for them to make the move.

It should also leave them with enough free cash to consider a few other financial options, such as reducing the term of their mortgage or making lump sum payments against the principal, setting some cash to put towards other types of investments, or blowing the lot on Champagne and travel.

Perhaps a little bit of each.

The comment stream on this article is now closed.

Note regarding equity calculation. This assumes the property was purchased with a 20% deposit at the the lower quartile price of $292,000 in February 2015 and sold at the 2025 lower quartile price of $595,000. The equity is the amount left over after deducting selling costs such as agent's fees, and repaying the outstanding amount on the mortgage. That assumes the mortgage had remained at the two year fixed rate throughout the last 10 years (30 year term) and no lump sum payments had been made.

*Mortgage term. A 30 year term has been used is the mortgage payment calculation because it gives the borrower the flexibility that comes with lower regular payments, while allowing them to make lump sum payments. However, borrowers should also consider shorter terms if/when they are able to afford them.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

21 Comments

I just bought my 2nd personal home after 13 years in my first, why buy a more expensive house though? Buyer motivations on what's value seem way off the mark compared to my own.

Because ever increasing debt makes the rocking world go round ?

if your view becomes common, the top layers of the pyramid will collapse onto the base.

"why buy a more expensive house though?"

It's human nature GP, without the urge for better things we would still be living in caves and our life expectancy would be around 30 - 40 years.

After you have the debt prison under control, move and sign up for a larger cell. Yeah yeah...yeah. What a plan. Must say there is a lot of noise in the wider market all pushing "its all ok" around larger mortgages, rates are coming down, and bring back overseas buyers etc etc. Are the billions in Bank profit not enough...

Looks like the specu owners are working out the music has slowed, with a strong forecast of Orange colored acid rain...

Agree with the article. I get grumpy watching property shows where people think they need to buy their forever home and over commit to do so or worse keep turning down perfectly adequate properties whilst in search of the pipe dream.

Ten years ago, in February 2015, the Real Estate Institute of New Zealand's national lower quartile price was $292,000. Ten years on, in February 2025, the REINZ's lower quartile price has increased to $595,000

That's a doubling of the price in 10 years, even after the slump of the last 4 years.

Indeed. But how good is that for society to be even further out of balance with incomes? But its all good as long as long as the good ol portfolio doing great. People wonder why our smart youth are exporting themselves, and why meth is out of control.

Nothing that a land tax wouldn't sort out.

Indeed. I suspect DTi even at 7x is having a big impact. Example...

- Owner buys a house for $1m. Needs 20% deposit but can borrow 800k.

- Investor buys same house $1m. Rents for $1000 per week. So rent $52k pa. x7 = $364k is max debt. So equity required is $636k, or equity elsewhere in portfolio as security.

Summary - more equity required, and is values continue to decline there is less of that every day.

Summary - more equity required, and is values continue to decline there is less of that every day.

Also side note, newer investors or those who grew too big too soon leveraging will be disadvantaged, however those who have been in that game for decades will still benefit form their high levels of equity, and now they'll have with less competition without new entrants getting in with any significant volume. The question is will they fuel another boom in future? Given historical trends in NZ I'd say so, albeit less of a boom than will be expected, despite if it is not great for the youth of the nation. I'd like to see otherwise however.

Meth is out of control because NZ doesn't hang hard drug dealers.

Yep, I also thought it was a stretch to claim that meth is out of control because of house prices. It may have some correlation, but i doubt it's the root cause.

The stress and hopelessness around access to shelter or struggle to achieve ownership of shelter has nothing to do with erosion of mental health, and then relief, however temporary, of drugs. No..nothing at all. But through the lense of narcissistic sociopathy, it is indeed all about you my old bean.

I referred to dealers not users.

Meth is out of control because NZ doesn't hang hard drug dealers.

Add in that the production capacity of Mexican cartels is always growing and NZ is a prime target for them, and Asian gangs also. The more they send, the more that gets in, and the more of a substance that is around, usually the more that gets consumed from availability.

Its coming in via the mail system in small amounts

points of meth are almost impossible to detect

despite the decline in property values

Moving is a better prospect because of the decline, otherwise the rungs would be further apart

Of course the reverse is true too. People wanting to trade down, say retirees, from an expensive house to a less expensive home lose out in a declining market. Assuming buying/selling in the same market location, if the decline is 15%, then a 2m house has declined 300k but the cheaper home of 1m has declined 150k. Ouch for the impact on extracting some retirement funds on the changeover.

Depends, if they bought the house for $20k and sell for 1.5m there's plenty to be thankful for (not that you'd always hear that angle)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.