Demand for residential mortgage lending has increased in the past six months for the first time since 2021, the Reserve Bank says.

However, poor economic conditions and higher unemployment rates "are likely to remain headwinds against a full recovery in residential mortgage credit demand".

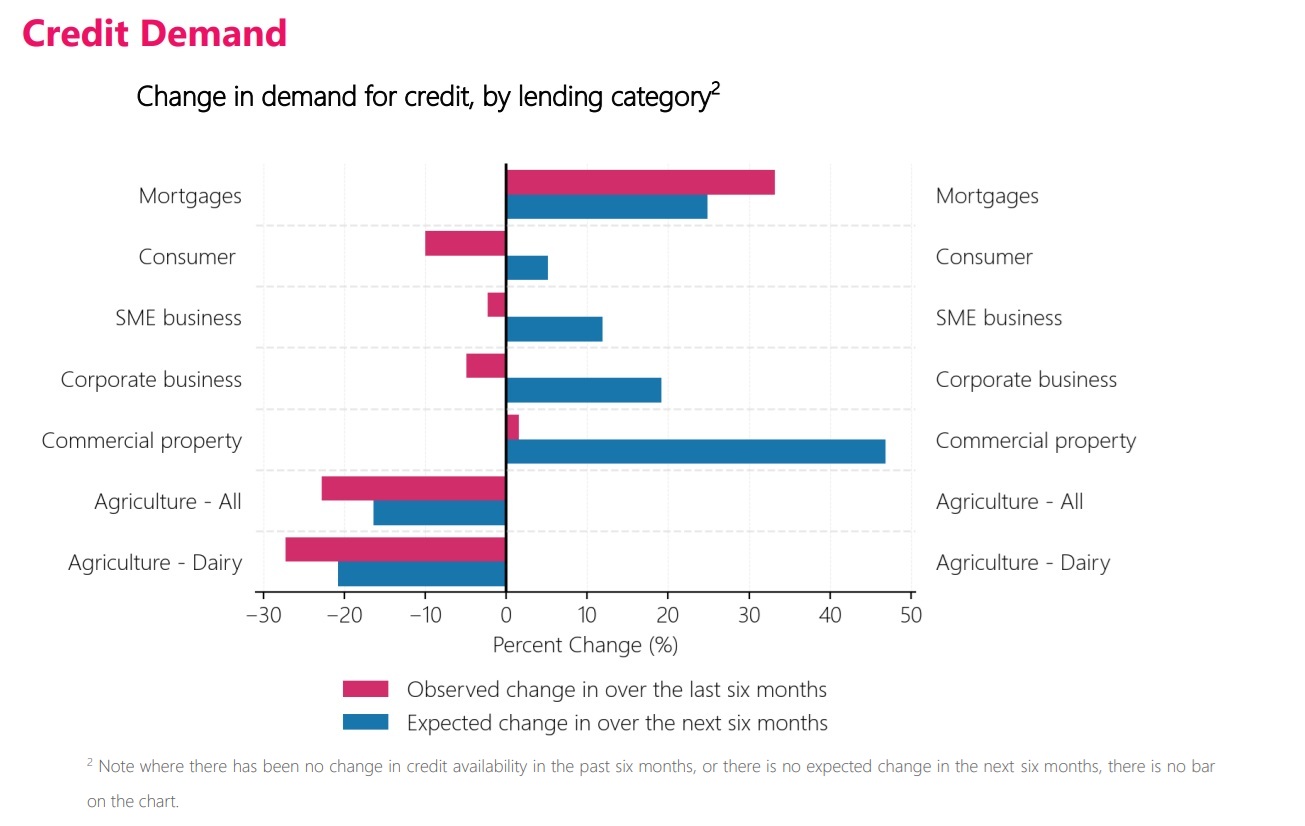

This is one of the observations the Reserve Bank (RBNZ) makes in its latest Credit Conditions Survey. The six-monthly survey seeks the views of 15 NZ-registered banks, including the big five, on both reported and expected credit availability and demand. This iteration of the Survey was completed in March 2025, covers credit conditions observed between September 1, 2024 and April 2, 2025 and asks how banks expect them to evolve over the next six months. The RBNZ notes banks formed expectations around credit demand and availability before the major US tariff announcements.

While the survey showed an improving trend in mortgage lending demand, the only other area of lending covered by the survey that had increased demand in the past six month period was commercial property - and only a small improvement at that.

The RBNZ said in its summary of the results that the banks noted that market sentiment is improving, "albeit gradually".

"They noted the impacts from the lower interest rate environment will take time to fully materialise," the RBNZ said.

"This improved sentiment has been driven by a reduction in interest rates and increased listings, which together has translated into higher demand for mortgages. Additionally, some part of the recent increase in mortgage demand has been from borrowers shifting loan providers as households seek to benefit from falling interest rates."

With expectations of further rate cuts and a continued increase in the volume of house sales, the rebound in demand for loans is expected to continue for the next six months, but as stated at the top of the article, the economic conditions and unemployment rate will remain dampeners.

Expected increase in demand for consumer credit didn't materialise

While residential mortgage demand has increased, consumer credit demand has not.

"In the September 2024 Credit Conditions Survey banks expected consumer credit demand to pick up in the next six months," the RBNZ said.

"However, this expected increase in demand did not materialise as banks have now reported demand for consumer credit declined over the survey period.

"Consumer sentiment has remained subdued, and many banks have noted that a broad recovery in the economic environment is required for consumer lending to meaningfully increase."

The RBNZ said while banks expect a small recovery in consumer credit demand in the next six months, the outlook is muted because of high consumer uncertainty amid poor domestic and global economic conditions.

"The reduction in consumer credit demand has been driven by a decrease in both secured loans and credit card spending," the RBNZ said.

"Demand for unsecured loans (loans without collateral) have seen an increase in demand in the last six months. Although banks did not comment on the causes of this, consumers may be using unsecured loans to cover short-term gaps in income or unexpected expenses."

Demand for commercial property has seen a gradual uptick in the last six months, "albeit from a very low base".

However, banks are expecting a much larger increase in demand in the next six months with expectations of further cuts in the Official Cash Rate.

"Lower borrowing costs are expected to enhance investment viability, improve returns on leveraged property investments, and attract both domestic and offshore investors back into the market. However, banks note that demand may remain uneven across the sector, with caution in office property."

Rural lending demand drops

Demand for agriculture lending decreased significantly over the survey period.

"Strong commodity prices and favourable production conditions have increased profitability for dairy farmers, reducing the need for working capital financing and liquidity credit. As a result, many dairy operations have been able to repay debt and fund capital expenditure directly from available cash flow."

The RBNZ said this has lowered farmers reliance on credit, particularly for seasonal facilities.

"Banks expect this trend of reduced credit demand in the dairy sector to continue. However, some banks noted that a sustained strength in dairy prices, alongside improving balance sheets and cash positions, could support an increase in credit demand for land purchases and business expansion."

The RBNZ said the survey found credit demand from businesses was mixed.

"Demand for capital expenditure loans declined, with many businesses delaying investment amid high economic uncertainty. However, SMEs and corporates increased borrowing for working capital and lines of liquidity due to ongoing cashflow constraints. On net, business credit demand fell over the last six months with the subdued economic environment and threat of US tariffs."

1 Comments

However, poor economic conditions and higher unemployment rates "are likely to remain headwinds against a full recovery in residential mortgage credit demand".

Isn't this what the RB have wanted for a long time? They've been spouting on about NZ's overvalued property for years. They should be celebrating the current market conditions, not labeling it "headwinds".

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.