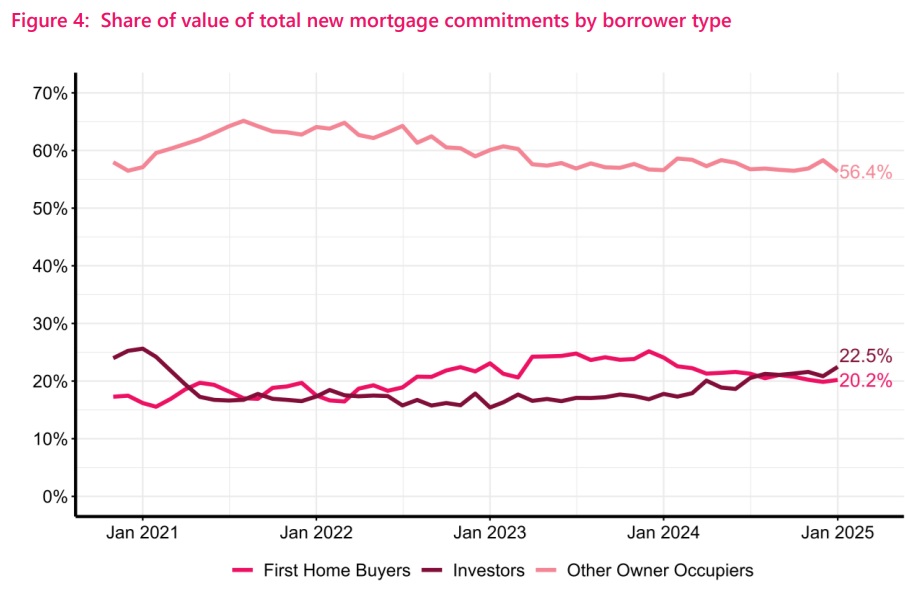

Investors have taken their biggest share of monthly mortgage money for nearly four years, latest Reserve Bank (RBNZ) figures show.

The figures show that in January the investor grouping took 22.5% of the $5.131 billion of committed mortgage money. And that's the highest percentage since February 2021, at the tail end of a big surge in investor interest after the RBNZ had temporarily removed loan to value ratio (LVR) restrictions in 2020. (Note, that when first reported, the RBNZ figures for October 2024 had a higher percentage figure - 22.7% - for the investors, but this was subsequently amended down to just 21.6%.)

The $1.153 billion borrowed by investors in January was up some 90% on the $607 million borrowed by this grouping in January 2024.

That compares with an overall increase in the total amount borrowed in January this year compared with January 2024 of 50.3%. (The amount borrowed in January 2024 was $3.413 billion.)

While a 22.5% share of monthly mortgage money for the investors is well down on the up to 35% share this grouping got in the 2014-16 period, it's a fair bit higher than it was for some time. In January 2024 it was just 17.8%.

The investors' share of the mortgage money really started surging in August 2024, with the grouping that month overtaking the amount borrowed by first home buyers (FHBs) for the first time in two and a half years.

As for the FHBs, which as a group have remained active participants throughout the recent downturn in housing activity, they saw their share of the mortgage money drop under 20% in December for the first time since July 2022.

In January 2025 the FHBs took $1.036 billion, a 20.2% share - so an increase. But that's well down on the 25.2% share in December 2023, which to date is the record share for the FHB's in this series, running since 2014.

The $5.131 billion total of committed mortgage money in January 2025 was in fact the highest overall total for a January since January 2021.

Of course not all this money is necessarily 'new' mortgage money as such.

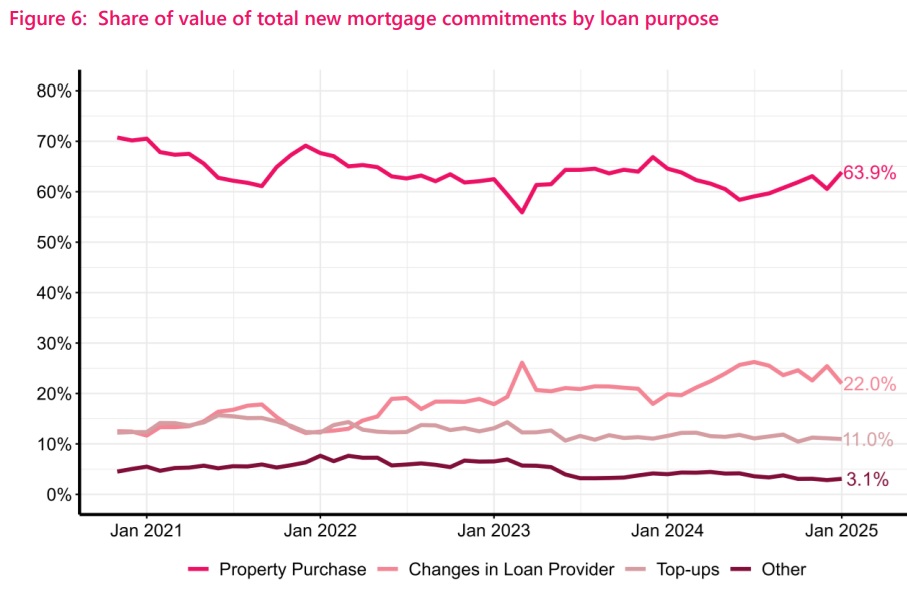

The separate figures provided by the RBNZ on lending by purpose, a more recent data series, break down money being used for house purchases, top-ups and change of loan provider.

There was a big surge in money for change of loan provider in December, but things were rather more quiet on that front in January, although holidays may well have had something to do with that.

The share of the value of new commitments for property purchases increased to 63.9% in January, up from 60.6% in December. The share for changes in loan provider decreased to 22%, down from 25.4% and the share for top-ups decreased marginally to 11.0%, down from 11.1%.

As we've been noting, mortgage customers since particularly the start of 2024 have been going shorter and shorter with their fixed term mortgages in anticipation of lower interest rates.

This has led to the situation where, going into this year, about 55% of mortgage money - over $200 billion worth - was either on floating rates or fixed and due a reset in the first half of 2025. Over 82% of mortgage money (more than $300 billion) is due a reset by the end of this year.

These are big figures. The more than $200 billion of mortgage money to be reset in the first half of 2025 works out at well north of $30 billion a month. Little wonder then that this has already having a big impact on the monthly mortgage figures.

And with customers having followed such a deliberate strategy of going short in order that they could then reset to the lowest rate possible, it's little wonder that many are prepared to switch loan providers to get what they want.

We'll be keeping an eye on these switching figures, month by month as the great reset continues.

38 Comments

Buy the dip

Investors increasing their bank borrowing for housing purchases is an interesting signal .....

We know that lower interest rates boost investor confidence/motivation. Some would argue that today's headline is a leading indicator of what's in store for 2025 and beyond.

Perhaps the market has over-shot / over-corrected downwards?? Who knows? We'll find out soon enough ....

TTP

There seems to be a very clear relationship between interest rates and house prices IMO. Interest rates going down, it’s a pretty good bet that house prices will soon be going up.

"Buy the dip"

Simple translation? "Allow the rich to become even richer."

Yeah. Only brings a revolution closer ....

Unless you're a desperate seller and are now able to move on.

Sounds predatory

Ask the seller if he was happy to sell or not when the alternative is the bank now owns your house.

If the RBNZ doesn't stamp down hard on LVR restrictions for 'property investors', we are just going to repeat all previous cycles.

Do we want that? (FYI. Offshore banks do. The landlording government does.)

Further, if the government doesn't insist on a re-instatement of ZERO interest deductibility, or at least a fair measure to balance owner-occupiers with 'investors', we're basically fucked as a nation where equity used to be a thing.

LVRs for 'investors' MUST go higher to ensure they start paying tax ealier than they have in the past and stop the milking of 'tax free' capital gains !!!!

NZ is a country that has fucked things for our children ... (Unless you have rich parents as 10% do !!!)

Chris, I wouldn’t worry about that, property is dead, stick a fork in it it’s done, in a few months the ole box of sticks will be traded for magic beans (if the vendor is that lucky)…the cycle will NOT repeat, trust me, I know this…how do I know this you may ask…well, I read it on interest.co.nz every single day so you can relax & rest easy 😏😉😂

It was a Ponzi anyway, so not sure why Chris potty-mouth is having a meltdown. Capital gains? Chance would be a fine thing!

I really enjoy CONF input, I’m sure he would’ve got the tone of my comment 😂😂

Bill English said that the market will be flat for 15 years, so it must be true.

Great satire, love it.

Chris how do LVRs help our children buy a house? As I’ve said before, it’s like trying to solve a food shortage by passing a law that only rich people can buy food.

Simple, It makes it more difficult to leverage equity vs non-investors which prevents bidding up prices due to said investors paying above what is reasonable thanks to being able to simply use equity to borrow/magic the funds into being from the banks. This in turn would somewhat cool the market and lessen any rampant increase in prices if things started ticking up again. Ergo, less buyers, harder to keep the leverage cycle going, slower increases if any, and your kids will have a greater chance of having the ability to purchase. Imagine having a child tomorrow and thinking they would ever have a chance of home ownership if prices somehow doubled again in the next 10years.

It may potentially reduce the pool of investors, though not necessarily the demand or sums available.

At the end of the day the 'money' already made (and continuing to be made) has to reside somewhere....and that tends to be in assets rather than in a hole in the ground.

we are just going to repeat all previous cycles.

Quite right Chris. This is why I have never taken the comfort many others have when house prices fell. All the same ingredients are still in the kitchen ready to be combined.

While nothing is guaranteed, it would have to be odds-on that we will have another go at 'growing' the economy via the real estate wealth effect. Consequences be damned.

You know that without deductibility rents would have to double to make a property a neutral prospect, right?

There should be a better way than a massive tenant tax.

Or conversely, people would become more mobile and go where the rent is cheaper, the LL wouldn't be able to find tenants at the price they need, and be more likely to sell as the investment suddenly becomes a dud unless they are happy to haemorrhage money into it weekly longer term. This adding supply for sale thus reducing prices, thus adding greater opportunity for those wishing to purchase to afford it, and allowing greater disposable income to allow for having children a.k.a the next generation to work, fund, and run the country one day. Why is it that so many think that landlords are untouchable and that tenants will pay whatever is asked is beyond me when currently there are plenty of rental options around to choose from.

Rent will need to double everywhere. Not just in cities. Only rentals available otherwise will be owners with no mortgage.

Is the current rise a result of the billions not being collected from Landlords? You can't just hand back billions to the landed gentry and not expect them to go cap in hand to the banks.

Further, if the government doesn't insist on a re-instatement of ZERO interest deductibility, or at least a fair measure to balance owner-occupiers with 'investors', we're basically fucked as a nation where equity used to be a thing.

A pity Chris, before this moment in reading your posts and comments I've thought you had a decent idea of how things worked. Sadly this is clearly not the case. It should be bleedingly obvious that even with full interest deductibility owner-occupiers are tax-advantaged relative to investors.

no tax on imputed rental,

no capital gains tax,

no risk of punitive governments creating policies that negatively affect you for populist reasons rather than rational ones...

That's hardly a fair reading, from a single post.

Chris has many times lamented our tax system, and with a wider stroke than just interest deductibility.

The first step to fixing our tax system would be to get rid of the business/personal divide, and put all on the same playing field. I personally advocate for FFT and LVT, and getting rid of pretty much all else.

Out of TDs and into overvalued shacks.

Excellent news indeed. Investors show why they are superior to the “do nothing” herd of nay sayers who snipe from the side lines.

Envy is a powerful tool that motivates the Left who want the government to punish innovation, in order to strip wealth from those who worked hard to earn their wealth and then give it free to the lazy and the foolish.

Socialism has proven again and again that it is only useful in evenly spreading misery.

Ain't no innovation in buying a bunch of houses!

“who want the government to punish innovation, in order to strip wealth from those who worked hard to earn their wealth” - I take it you aren’t referring to property investors as buying an existing house and then renting it out is the dead opposite of innovation - in fact you might even call it lazy and greedy…..

If capitalism is so superior, why does it need the socialism of "the left" to bail it out every couple of decades? Buy house / paint house / sell house isn't exactly world changing innovation.

More debt and the money directed to unproductive assets with the expectation that someone else will pick up the tab to service an unrepayable debt of around 90% gdp.

Investors rolling off their 2-3% 5 year fixes.

14 more months baby. I was hoping to roll onto something with a 3 in front of it but agent orange put a stop to that. Oh well.

Cool. Its not all about you, and stats show you are, by far, in the minority.

Don't dismiss it yet. Remember, the current pace of growth (or lack thereof) is gradually suppressing domestic inflation - that's the key metric driving OCR decisions.

Is the investor definition here just a non occupied purchase?

I suspect the ratio of 'buy because it's the thing to do' type investors oblivious to tax and running costs, is growing compared to the professional investors that can read the writing on the wall, selling onto the less sophisticated bag holders.

Reinstating deductibility softens the blow short term for those negative gearer's who didn't get the hint but ring-fencing loophole will remain closed

hang on a second, this is just about 'share', it could be investors are more active, or it could be about FHB less active.

which is which?

Investors back just in time for a change in Government, anti-landlord Labour!

@ Huttman

Look at the dollar numbers

yup, just read the numbers

investor mortgage numbers jumped 90% compare to Jan 2024, FHB jumped 26%, all borrowers jumped 50%.

investor is back, and FHB is not exactly shrinking but certainly not increasing as much the general trend.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.