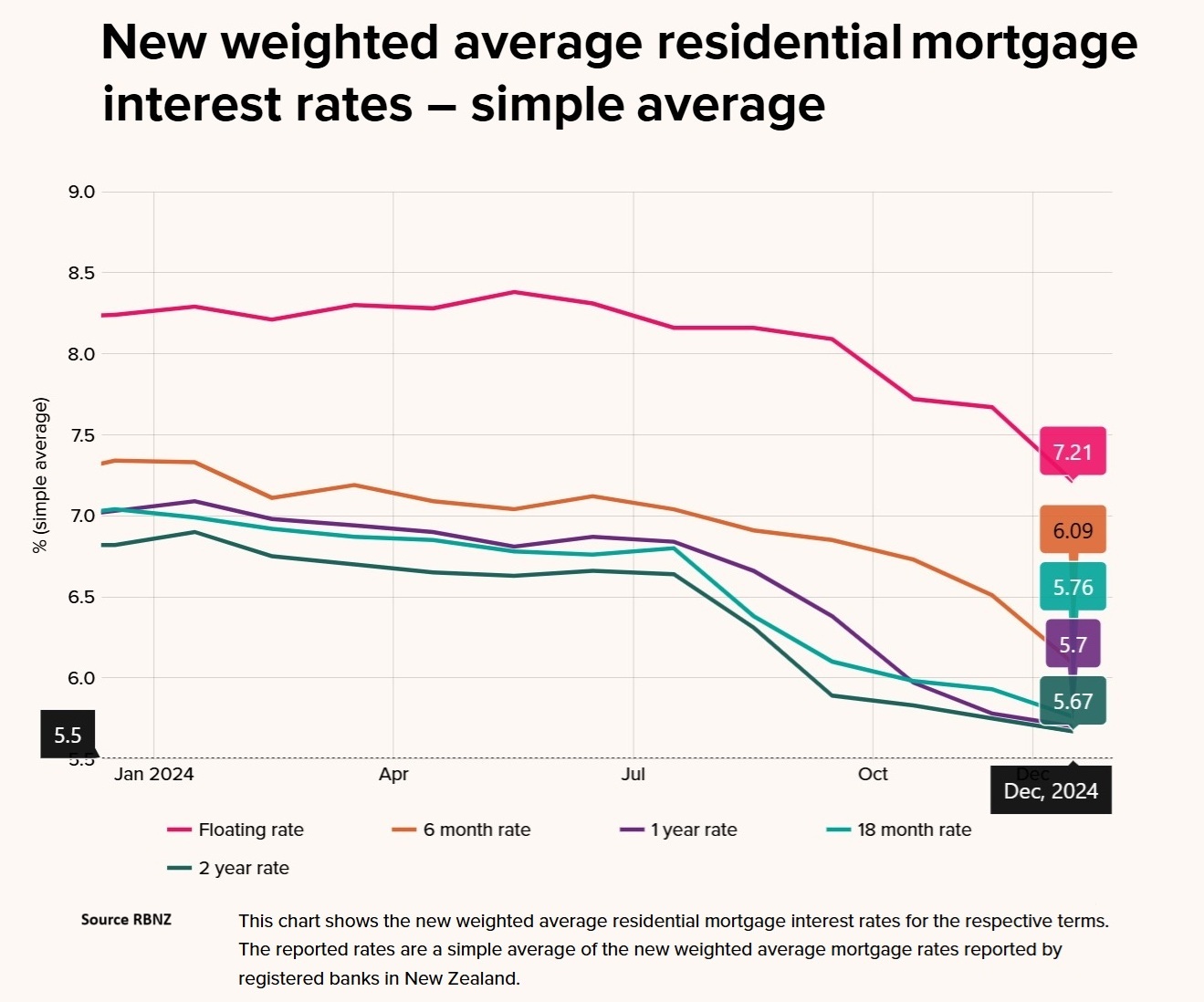

Homeowners taking up new mortgages in the second half of 2024 were paying mortgage rates around one whole percentage point lower than those prevailing in the first six months of the year.

The Reserve Bank's new residential mortgage weighted average interest rate figures, monitoring actual rates being paid on new mortgages fixed for two years or shorter, show on average the rates dropped by around 100 basis points - or more - between June and December.

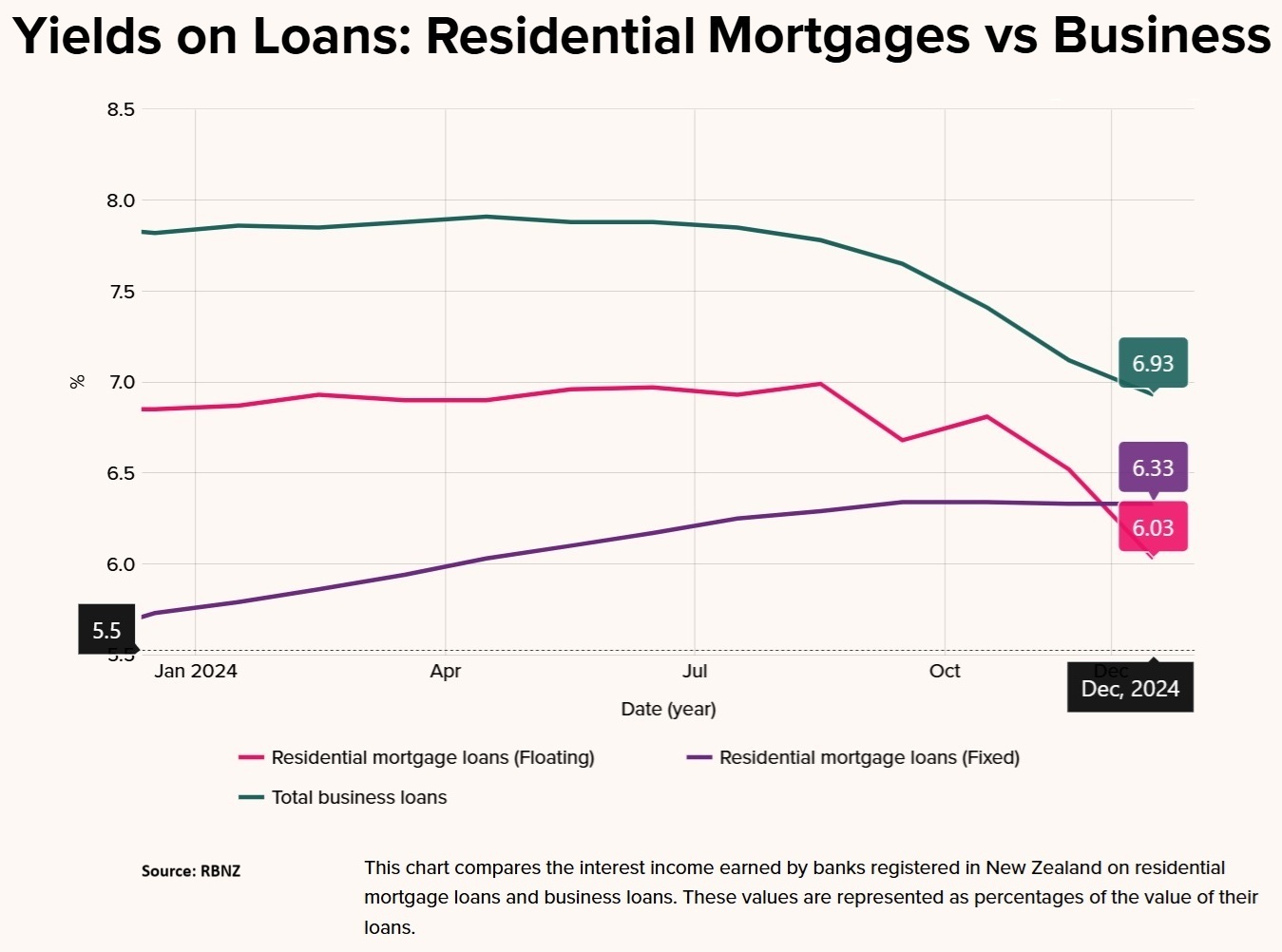

However, separate data for the bank yields on existing loans show that the rates for existing mortgage holders are as yet easing only very slowly. In fact the bank yield on fixed term mortgages didn't drop at all in December. The bank yield figures are key ones to watch - since they give the true indicator of how quickly (or not) customers are on average seeing their payments down.

And that latter point's significant because it will give us a good guide as to how quickly we might (or might not) see the economy - and indeed house prices - start to pick up.

But first up, back to the average rates being paid on new mortgages. This data series was introduced relatively recently. The Reserve Bank (RBNZ) has initially focused on the shorter term fixed rates, but says it will look to add the longer-term fixed interest rates (three-year, four years, and five years) "once we have worked through data issues impacting the accuracy of the data at this time".

As we know, mortgage customers have been going shorter and shorter with their rate fixing terms as they look to take advantage of anticipated imminent future rate falls.

Ahead of the RBNZ rate decision in late November (which saw the Official Cash Rate dropped from 4.75% to the current 4.25%) there was actually a big swing to floating mortgage rates - despite these being higher than the fixed term rates.

But in December, there was renewed surge back towards short fixed rates - particularly six months.

RBNZ figures on newly drawn-down mortgages show in December 38.1% of owner-occupier's mortgages by amount were fixed for six months.

And these patterns are clearly visible too in the separate RBNZ data series that shows the time until the next reset across the country's entire mortgage book.

In short, those figures show that just under 55% of the entire $369.546 mortgage loan pile is either floating or due a refix within the first half of this year. And over 82% of the mortgage book is due a refix this calendar year.

So, looking at those who have fixed for six months in the RBNZ monthly figures, we can see that in June the average rate being paid on new six month term mortgages was 7.12%. By December it was down to 6.09%. That's a 103 basis-point reduction.

In terms of rates paid, the biggest basis-point reduction over that period was for the currently not-as-popular-as-it-was one-year fixed term. The one-year average rates dropped 117 basis points from 6.87% to 5.70%.

The lowest average rate as at December was for the currently deserted (but again, previously very popular) two year rates. This was 5.67%, down from 6.66% in June - a 99 basis-point fall.

Those are the new mortgages.

What about those existing yields across the entire loan book?

We know that the OCR was first cut in August (from a then-5.50%) and, in fact, banks had been cutting their mortgage rates for some months prior.

But the average yields take a little while to catch up with a change in direction.

The historic lows seen before the surge in inflation culminated in a low water mark average mortgage yield of just 2.83% in September 2021.

By the end of that year the figure had blipped up to 2.94%. At the end of 2022 it was 4.35% and by December 2023 it was 5.85%.

The average yield figure continued to slowly climb through 2024 even as advertised mortgage rates were coming down, peaking at 6.39% in October. It then dropped to 6.35% in November and then 6.29% in December.

However, the falls in the overall average have to date been primarily driven by a drop in the yield to banks on floating mortgages - which are obviously the most quickly responsive figure.

If we look at the average fixed term yield, this has barely moved since peaking at 6.34% in September. It fell to 6.33% in November and remained on 6.33% in December.

The story for the early part of 2025 is how quickly those yield figures - and by extension the amount being paid by homeowners - reduces. And how many more OCR cuts will we see?

These points are the key to how quickly or not quickly the NZ economy starts to climb out again from its trough.

As we can see at the moment, getting money back into people's pockets is not like flicking a switch.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

4 Comments

And the reason floating rates are 7.21% is?

As the media tells us rates are dropping, the truth is rates on existing fixed mortgages (ie almost all mortgages) actually increased from 5.5% to 6.33% during the year. So a negative pressure on house prices still exists

Anecdotally, ASB gave me 5.49% at 1 year back in October. Now we have the exact same in app deal on offer 5 months later making headlines. A lot of sideways and even upward movement over Christmas.

"the truth is rates on existing fixed mortgages actually increased from 5.5% to 6.33% during the year… So a negative pressure on house prices still exists "

Except that it's not true at all, that was for last year.

7.2% is simply the banks gouging, trying to force you lock in for a fixed term.

No, the rates are dropping, they peaked at the end of last year and now almost refixes are someone refixing at a lower rate. The chunk coming off in June this year was fixed a 5.39 three years ago, it'll be refixed at a lower rate when it rolls over. And the chunk coming off in a week will be going from 6.85 to under 6, hopefully I can push them to 5.85 for 6 months. A whole percent off.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.