The very quick rise of floating mortgages to be top pick for homeowners in November was quickly reversed in December as six-month terms became king.

According to the latest monthly Reserve Bank figures, some $2.375 billion of the $6.237 billion taken up by owner-occupiers for new mortgage agreements in December 2024 was for six-month fixed rate terms.

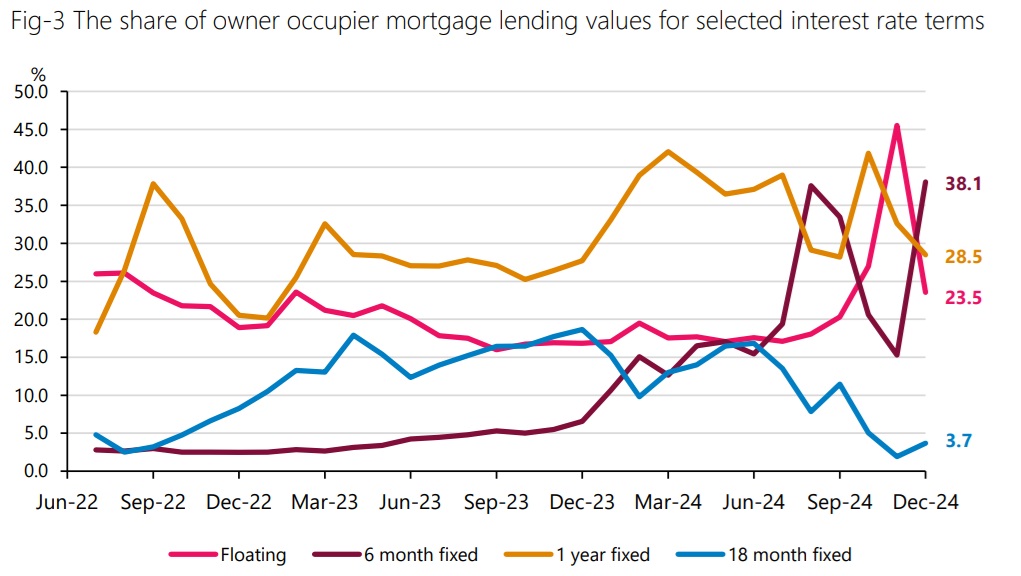

The 38.1% of the owner-occupier total this makes up (up from just 15.3% in the previous month) is a new high water mark for the popularity of six-month terms in the relatively brief time this particular data series has been published.

The RBNZ's C71 data series has data going back to 2021. It differs from other monthly series published by the RBNZ in that it shows mortgage figures for after the mortgage has been uplifted (while other series highlight mortgage figures for when the mortgage has been committed to). (The RBNZ summary of the latest data is here.)

The C71 data therefore shows the flow of the money and into what rates as and when it happens.

In November customers had flooded into the hitherto fairly unpopular floating rates - despite these rates being higher.

But it looks clearly as though the homeowners were keeping a close eye on the Reserve Bank.

In late November the RBNZ cut the Official Cash Rate from 4.75% to 4.25% and strongly indicated that a further cut to 3.75% would be made at the next review on February 19, 2025 - next week.

So, in December there was a sharp change in tack by those taking up new mortgages when compared with those doing the same just a month earlier.

In November some 45.5% of new owner-occupier mortgages by amount had gone on floating. But in December the percentage dropped sharply to 23.5%.

Still, though, the overwhelming desire demonstrated by the homeowners was to go for short terms, obviously in anticipation of further imminent rate cuts.

In the December month the share of owner occupier loans on floating and short-term fixed rates either of a year or shorter duration represented 90.1% of new lending.

And it was all pretty much the same story for the investors too, with a big move away from floating and to six month terms.

New residential investor mortgage lending was $2.5 billion. Of this, $1.106 billion was on six-month fixed. It too was a new high mark, making up 44.2% of new investor lending, from 13.9% in November 2024.

In its most recent forecast issued in November the RBNZ indicated the OCR may go as low as 3.50% late this year, however, many economists - and market pricing - suggest the OCR will hit 3.00% this year.

Those with a mortgage, or about to get one, will be looking very closely at what the RBNZ says next week for clues as to when they should perhaps start looking to fix for longer terms - or to keep on short terms and wait (hope) for further rate falls.

7 Comments

One figure's not right:

'In November some 45.5% of new owner-occupier mortgages by amount had gone on floating. But in December the percentage dropped sharply to 45.5%.'

Second one should be 23.5%?

Fixed. Thanks very much.

Typical fhb expecting rates to go into 2s and 3s again this year.

Have I got news for you.

I am keen to hear your news Toye? What's your 🔮 saying?

Typical Toye, making assumptions.

Where in the article did it say they expect rates to be in the 2's and 3's? nowhere.

only that there will be a cyclical low

Eh? Prospective FHBs don't want lower rates (but the foolish who bought, say, a few years ago might).

Most FHB understand that higher rates improve their long-term prospects as prices fall and deposits rise (balanced against unemployment prospects from idiotic fiscal policy, mind).

You know who does want lower rates though? Bag holders and wannabe bag holders. And they'll do their best to try to convince prospective FHB that "the time to buy is now!" as their sales chains hang flaccid.

Could the NZ housing investor follow the current US housing investor trend.....lol

https://youtu.be/i2AT3Msc-SE?si=KbbrygtRklKoyVgQ

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.