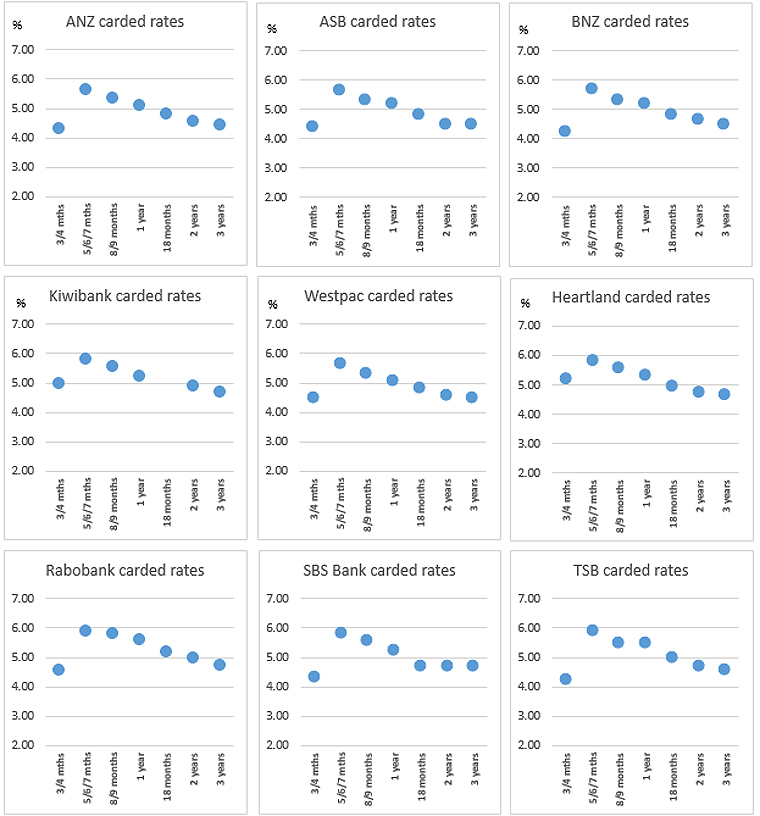

One of the resilient ends of the term deposit curve recently has been the shorter end. Rates have changed little for terms of six months or less.

But on Friday BNZ took some small steps to reduce these rates as well.

And while that does not make them the lowest in this zone, it probably indicates that rates for all banks will likely fall soon for short-end term deposits (TDs).

This is the part of the curve where all banks have had relatively high rates.

In the six month range, term deposit rates are at their highest for all banks. In the three month rate, they are the same as for long term commitments (three years plus).

Inverted rate curves are not 'normal' although we have been living with them for years now. 'Normal' is when savers are rewarded with higher rates for longer term commitments. That is fundamental to a time value for money.

Things are no longer 'normal'. However the natural pressure is to return to a positive-sloping rate curve. And as we come out of recession (at some point), 'normal' should return.

Although every bank has an inverted rate curve offer set, not every bank offers the same.

Part of the reason banks currently offer a premium for about-six month savings rates is that this is where savers feel more comfortable. So retail funding demand has to follow savers' preferences. However, if loan demand stays weak, then banks run little risk offering less. And when loan demand picks up, expect banks to try and juice up longer term offers.

Also coming into play is the impending Depositor Compensation Scheme (DCS). It's in the background now for savers because it won't be effective until mid-2025. But financial institutions are well aware this is on the horizon. They are aware the DCS will be funded by levies, set out in regulations, collected from licensed deposit takers, which they will be paying starting in about nine months from now.

Savers who use three and six month term deposits are known to almost always roll them over. So banks will probably feel the need to trim offer rates to accommodate the DCS fees soon, so as to not make that such a big impact when the DCS goes live.

The Depositor Compensation Scheme essentially makes all deposits less than $100,000 risk-free for savers. So expect TD offer rates to trend down to the equivalent risk-free return (like the Kiwi Bond offer rates).

On the other hand, deposits with all licensed deposit takers including building societies, credit unions and deposit taking finance companies, will have the DCS guarantee. All non-banks offer more than banks currently. They are undoubtedly looking forward to promoting their 'guaranteed' offers against banks. But non-bank financial institutions (NBFIs) typically push to keep their funds flowing with longer term (more than one year) offers. This pressure will be another than could raise bank TD offers in 2025 for longer terms. For longer terms, the 'floor pressure' from Kiwi Bonds is minimal with 3.75% being the current Kiwi Bond four year offer. (No doubt that will have changed by mid-2025).

Big bank funding options are constrained by Reserve Bank regulatory requirements, wholesale market funding costs, and competitive pressures. Challenger bank options don't have the wholesale funding access in the same way. NBFIs wholesale funding access is usually only via a main bank, although some of them fund via securitising their loan portfolios.

In the grand scheme of things, the big banks have more options, better access to broader range of funding, better credit ratings, and stronger prudential reputations. But are the targets of smaller institutions continually trying to feed off their embedded base. The coming DCS will downgrade some of the big-bank advantages.

When you invest, always check how interest is compounded. Depending on how much you are committing, compounding more often is materially better. But some banks advertise their "interest at maturity" rates different to their compounding rates, which for some can be set a little lower. Both Kiwibank and Rabobank do this, although most other main banks don't.

Use the calculator at the foot of this article to see the differences.

But for taxpayers on 30% and living in a 3.3% inflation world, that gets breached when offer rates fall below 4.70%. We still have headroom but it is retreating quickly. You now have to think we are looking at a future where tax-paid term deposit rates are likely to fall below inflation again. Many savers have been there, done that, and know it is not nice.

Both the wholesale and retail rate curves are falling and flattening, a trend we expect to see for a while yet.

We should also point out that after-tax returns can be enhanced for some savers with higher tax rates, by the choice of PIE structures. Not all banks offer these, but most of the main banks do. For a nine month bank offer, they can be boosted by about 30 basis points going this way. In some cases that will make up any difference, or more.

Always ask a bank for a better rate. Many bank staff have discretion to offer more than the advertised rate. (And check your bank's app offers as they too are often enhanced to retain you). But in this environment don't get your hopes up for a positive response. Carded rates are likely to now be the 'best rate', except in quite special circumstances.

Use the term deposit calculator here, or the one below the table, to calculator your expected net returns.

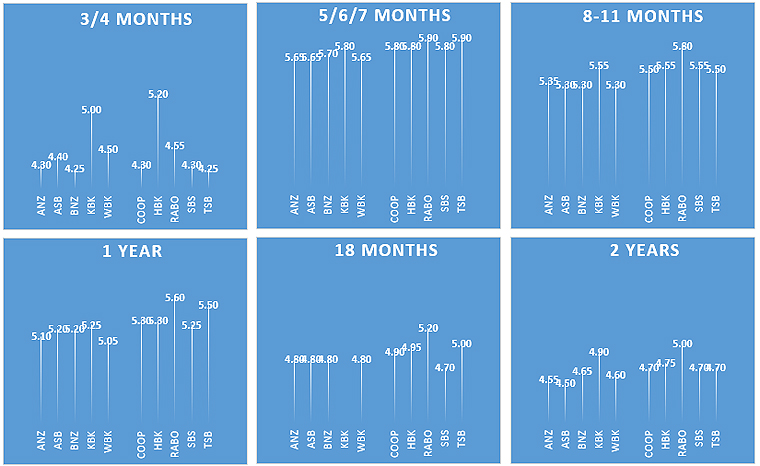

The latest headline term deposit rate offers are in this table after the recent changes to start the week.

| for a $25,000 deposit September 13, 2024 |

Rating | 3/4 mths |

5 / 6 / 7 mths |

8 - 11 mths |

1 yr | 18mth | 2 yrs | 3 yrs |

| Main banks | ||||||||

| ANZ | AA- | 4.30 | 5.65 | 5.35 | 5.10 | 4.80 | 4.55 | 4.45 |

| AA- | 4.40 | 5.65 | 5.30 | 5.20 | 4.80 | 4.50 | 4.50 | |

| AA- | 4.25 -0.05 |

5.70 -0.10 |

5.30 | 5.20 | 4.80 | 4.65 | 4.50 | |

| A | 5.00 | 5.80 | 5.55 | 5.25 | 4.90 | 4.70 | ||

| AA- | 4.50 | 5.65 | 5.30 | 5.05 | 4.80 | 4.60 | 4.50 | |

| Kiwi Bonds. 'risk-free' | AA+ | 5.00 | 4.50 | 4.00 | ||||

| Other banks | ||||||||

| Bank of China | A | 5.30 | 5.90 | 5.60 | 5.50 | 5.10 | 4.90 | 4.90 |

| China Constr. Bank | A | 5.30 | 5.50 | 5.40 | 5.35 | 5.20 | 5.05 | 5.00 |

| Co-operative Bank | BBB | 4.30 | 5.80 | 5.50 | 5.30 | 4.90 | 4.70 | 4.60 |

| Heartland Bank | BBB | 5.20 | 5.80 | 5.55 | 5.30 | 4.95 | 4.75 | 4.65 |

| ICBC | A | 5.30 | 5.80 | 5.45 | 5.40 | 5.05 | 4.85 | 4.75 |

| A | 4.55 | 5.90 | 5.80 | 5.60 | 5.20 | 5.00 | 4.75 | |

| BBB | 4.30 | 5.80 | 5.55 | 5.25 | 4.70 | 4.70 | 4.70 | |

| BBB+ | 4.25 | 5.90 | 5.50 | 5.50 | 5.00 | 4.70 | 4.60 |

Term deposit rates

Select chart tabs

Daily swap rates

Select chart tabs

Term deposit calculator

3 Comments

So should we go long or short with our TDs that are currently due for reinvestment??

The problem with DCS is that non bank lenders (obviously more risky) come on par with deposits up to 100K. Finance companies have created may problems in the past with bankruptcies and out right fraud. This will mean the DCS will be bailing out the companies that are speculating (basically betting) on the economic conditions for a short period of time. (say 1-3 years). Not sure what all the regulations are for non bank lenders to be covered, but I am sure some fraudsters cannot wait.

Does this mean that banks can now look at more risky investment positions with customer deposits knowing the government/insurance will back stop them?

Doesn't that incentivise bad behaviour or is just what has to happen to be able offer returns above inflation going forward?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.