The tax year-end of 31st of March is fast approaching and at this time of year tax agents are busy with the last year's tax returns and also giving a heads up to clients about what actions they need to take ahead of 31st March. It’s always an incredibly busy period and it's often easy to overlook some important matters amidst the rush and the mayhem. So, here’s a quick reminder of key issues that that you should be considering as the tax year ends.

GST and Airbnb

First up, a GST election is running out in respect of being able to take assets out of the GST net. We discussed this a few weeks back. To quickly recap, this could particularly affect Airbnb operators that may have bought a residential property, rented it out and then realised that Airbnb produces a better return. They've therefore signed up to Airbnb or other apps and then registered for GST either voluntarily or because they’ve exceeded the $60,000 registration threshold.

Subsequently, the taxpayer may have claimed an input tax credit on the property but now realise that they could be liable for a substantial GST bill on any subsequent sale of the property. That obviously is a big shock

To address this issue, a transitional rule was introduced under section 91 of the Goods and Services Tax Act with effect from 1st April 2023. The rule enables a person to elect to take an asset out of the GST if the following four criteria are met:

- the asset was acquired before 1st of April 2023; and

- it was not acquired for the principal purpose of making taxable supplies; and

- it was not used for the principal purpose of making taxable supplies; and

- and a GST input tax credit was previously claimed, or the asset was acquired as part of a zero-rated supply.

If all those criteria apply, then the person can elect to take the asset out of the GST net and pay back the GST that was claimed on the original input tax. In other words, they don't pay GST on the increase in value. A good example here would be a bach or family holiday home which was subsequently rented out for short stay accommodation.

The key thing is this election expires as of 1st April 2025, by which time you must have notified Inland Revenue of your election. You don't necessarily have to pay the GST; you can do so as part of your GST return to 31st March, but you must have notified Inland Revenue in a satisfactory manner. I would recommend using the MyIR message service to do so.

Other year-end matters

There are a number of elections relating to whether or not a taxpayer wants to adopt or leave a tax regime. A classic example would be companies entering or leaving the look-through company regime. Another, lesser known one would be entry or exit into the little known, and apparently little used, Consolidation regime.

Another matter that pops up regularly around year-end is checking your bad debts ledger. Bad debts are only deductible for income tax purposes if they are fully written off by 31st March so make sure this happens. Then there is the year-end fringe benefit tax returns where taxpayers should check to see whether they are making full use of any available exemptions.

A very important one for companies is to ensure their imputation credit account, either is in credit or has a nil balance. If there’s a debit (negative) balance on 31st March, that will result in a 10% penalty. It may be possible in some cases to make use of tax pooling to rectify some of these issues.

Finally, if you're registered with a tax agent, your tax return for the 2024 income year must be filed by 31st March otherwise late filing penalties may apply. Possibly more critically, the so-called "time-bar” period during which Inland Revenue may review and amend already filed tax returns is extended by another year.

Lessons from the country’s biggest known GST fraud

Moving on, an interesting story has popped up in relation to what was then the largest known GST fraud. Gisborne farmer John Bracken was jailed in May 2021 after he was found guilty of 39 charges of GST fraud. He had run a scam through his company, creating false invoices totalling more than $133 million between August 2014 and July 2018 which resulted in receiving GST refunds totalling $17.4 million to which he wasn't entitled. He was jailed and is currently out on parole.

At the time he was sentenced Inland Revenue and the police issued restraining orders and are trying to make an application for an asset forfeiture. In other words, assets subject to the forfeiture order were acquired through fraud and should be forfeited and handed to the Crown.

Now naturally Mr. Bracken and his family, including his wife and his parents and his son, are all fighting back on this because they stand potentially to lose assets that may be subject to the restraining order and subsequent forfeiture. The interesting part of this is the sheer scale of what went on and how it went undetected for four years before an employee got suspicious, notified the Serious Fraud Office, who then tipped off Inland Revenue.

At the time the frauds were committed, Inland Revenue was at the start of its Business Transformation project, upgrading all its systems. Until it got tipped off It had no idea of the extent of the fraud. Mr. Bracken appeared to have covered his tracks reasonably well, although once uncovered it was a fairly simple GST fraud. He just submitted fraudulent GST invoices, but he was careful to get them from actual companies with whom he had established some form of trading relationship.

Obviously the concern is now twofold. The Crown will be wanting to recover as many assets as possible to the value of the $17 million that it was defrauded, but also, can this happen again?

I'd like to think “No”. Certainly, Inland Revenue feels that its new systems have enhanced its capabilities greatly and that would appear anecdotally to be the case. There was a GST fraud scheme spread by TikTok influencers which caught the Australian Tax Office completely off guard and was worth tens of millions of dollars. Inland Revenue feels that that sort of fraud could not happen here. Mr Bracken's release on parole and the ongoing forfeiture case is a reminder that Inland Revenue has to be vigilant all the time.

But sometimes it comes down to a conscientious person, an employee usually, tipping off the authorities. But it shouldn't always come down to that. Inland Revenue and other authorities should be able to pick up signs of these frauds. As I said, I have confidence they do, but I would also hope that confidence is not tested too much.

Corporate tax cuts – a possibility or just flying a kite?

In recent weeks there's been some chatter or hints from the Government and Finance Minister Nicola Willis about a potential corporate tax cut. She made the not unreasonable point that our corporate tax rate is high by world standards. This prompted comments from the former Deputy Commissioner of Inland Revenue Robin Oliver that tinkering around the edges by reducing it from 28% to 25% might not achieve much. If the Government wanted to attract investment, they'd have to go big, maybe nine or ten percentage points cut. Robin was sceptical the Government could afford to do so because of the loss of revenue. And I agreed with that assessment.

I do wonder whether this idea might be something of a bit of a red herring. Some comments I've heard seemed to suggest that maybe the Government was just flying a kite to see the reaction.

Anyway, this week a poll run by Stuff which suggested that very few would support a corporate tax cut, or rather that that the population was pretty lukewarm about the idea. The poll carried out by Horizon Research, found only 9% of adults supported lowering the corporate tax rate, while 25% actually wanted it increased. There were a few other interesting results:

Who would benefit from a corporate tax cut?

Craig Renney (the chief economist for the Council of Trade Unions) and researcher Edward Miller also looked at who would benefit from a drop in the New Zealand company tax rate. They concluded the main beneficiaries of a corporate tax cut would probably be overseas shareholders. In terms of attracting greater foreign direct investment, they saw little evidence that corporate tax cuts would be likely to achieve that.

As they noted,

“…company taxation is only one aspect of a decision by a company or fund to invest in New Zealand. In addition to the company tax rate, there is the R&D tax incentive, the lack of a capital gains tax, and the lack of substantial payroll taxes. These taxes affect the actual tax paid by corporates in comparison with other countries when considering investing in New Zealand.”

Renney and Miller’s modelling suggested that a tax cut would not result in further investment but would just simply increase the funds flowing offshore. In particular they saw the Big Four Australian banks as being prime beneficiaries. The pair estimated that a cut from 28% to 20% would have increased the annual income to offshore shore shareholders by up to $1.3 billion.

There’s always a lot of debate around the benefit of corporate tax cuts, whether they do drive investment, or they simply put money into the back pockets of the shareholders. That debate has gone on for a long time and continues again. But it's interesting to marry that along with the public's general lack of enthusiasm for such a cut.

Yeah, but what about the IMF?

I think it was also noticeable that the International Monetary Fund in its recent Concluding Statement for its 2025 Article IV Mission suggested “judicious adjustments to the corporate income tax regime.” So maybe it too isn’t entirely sold on corporate tax cuts as a key driver for investment.

No doubt more will be revealed in May’s Budget. And until that time speculation will mount, but we will find out on the day and as always, we will bring you the news when it emerges.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

4 Comments

Apparently, there is some voter support for the idea of tax reform.

Would a Wealth Tax in the form of a Land Value Tax be the easiest of all to implement? It really shouldn't be difficult to sell to voters as long as one always starts the discussion with "income tax will be reduced..."

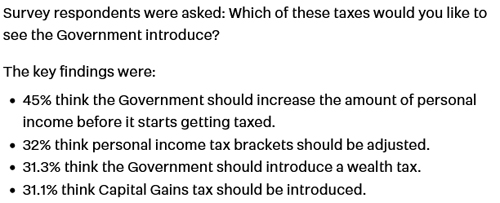

"Survey respondents were asked: Which of these taxes would you like to

see the Government introduce?

The key findings were:

. 45% think the Government should increase the amount of personal

income before it starts getting taxed.

32% think personal income tax brackets should be adjusted.

31.3% think the Government should introduce a wealth tax.

31.1% think Capital Gains tax should be introduced."

Your survey appears to confirm that a significant majority disagree with any such taxes

The devil is always in the detail.... I suspect that the majority of voters have not given it much thought.

If you ask voters "do you want a new tax added to your burden" then I suspect you would get 99.9% "no". If you ask voters in their 20s "would you like to pay less income tax, but that there is a tax on land instead" you would be more likely to get a lot of support.

Other than assume the difference between 28% company tax and 20% company tax would be offshored could NZ Inc not be thinking smarter by retaining the difference onshore? The IRD has comprehensive systems to follow the money and ensure maybe the difference can be held for say 2 yrs? for NZ benefit. Lots of squeals no doubt but there has to be better way to make it appealing to run and invest in NZ. How about "how can we" rather than look for "too hard" NZers are smart when they need, want to be.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.