By Daniel Hynes and Soni Kumari*

Highlights

-

Softer than expected US inflation triggered a sell-off in the USD, helping gold prices to recover. That’s unlikely to last.

-

Nevertheless, the US dollar remains vulnerable further downside amid hawkish comments by the Fed.

-

Technically, the downtrend has broken following recent sell-off in the US dollar, but failed to break the resistance of USD1800/oz. We expect gold price to resume its downtrend and fall below USD1700/oz in the short-term.

Outlook

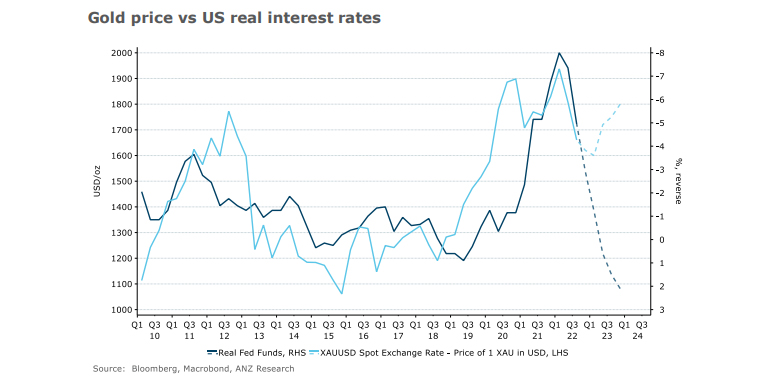

A persistently hawkish Fed is likely to keep gold prices in check. Softening US inflation raised hopes for an end to the aggressive rate hike cycle. This would raise the risks of a weaker USD and subsequently raise support for gold.

That was scuttled after the FOMC meeting, with Fed governors suggesting rates are likely to continue to rise at upcoming meetings. This is supported by strong retail sales and employment data. This is likely to remain a structural headwind for gold until the Fed’s stance turns dovish.

Data suggests that gold can still outperform against real rates. With intensifying recessionary and geopolitical risks going into 2023, this will be an ongoing issue. Central banks purchases are at record highs. Physical offtake in the emerging markets remains strong.

This should reduce the burden for investment demand to clear the supply overhang. This is important, considering ETF liquidation is likely to continue in the short-term. Nevertheless, retail investment is holding up well. Lower refined gold output could also tighten the physical market amid the energy crisis in Europe.

Q&A

Gold prices rose 9% from their early November low, do we expect this strength to continue?

The recent gold price rally was triggered by softer than expected US inflation for October. However, we believe the market reaction to the latest inflation print was exaggerated as inflation remains near 7.7%, which is well above the central bank’s target of 2%. Further, the month-on-month increase was still 0.4% for both September and October.

It is not enough for the Fed to be confident that inflation is on track to move back to 2% sustainably. Any hawkish comments from the Fed could reverse the recent bullish move in the gold price. Retreating inflation and rising rates until early 2023 would keep real rates rising, leaving the backdrop challenging for non-yielding gold.

Could we see investment demand turning positive soon?

Physically backed gold ETF liquidation has slowed in October to 59t from 95t in September, with most of the liquidation in the US (67%), followed by Europe (24%) and Asia (8%). Disinvestment of ETF holdings started in May and October has been the sixth consecutive month of net outflows, resulting in cumulative outflows of 368t in the last six months.

Stabilising gold prices near USD1620/oz amid persistent geopolitical risk has probably helped slow liquidation. Nevertheless, it would be difficult to see investors increasing their ETF holdings materially in a rising interest rate environment. We believe any short-term rally would trigger profit booking rather than fresh buying at higher levels until the Fed’s hawkish tone peaks, which is not looking likely until end of Q1 2023.

What factors are driving strong purchases by central banks this year?

Central banks purchased 399t in Q3 2022, this was a record quarterly purchase. Of this, nearly 285t of gold purchased was unreported, according to World Gold Council data. Unreported buying could be from Russia and other sanctioned countries. Turkey (95t), Egypt (44.3t), Iraq (33.9t), India (31t), Uzbekistan (28t), and Qatar (15t) are the major reported buyers this year. These countries share common factors of depreciating domestic currency and debt defaults. These factors, along with deteriorating geopolitical relations, largely drove the purchases. Central banks are trying to diversify their foreign reserves, this is reflected in the falling share of the US dollar in their foreign reserves. We are keeping our central bank purchase estimate at 700t, but this could go beyond 750t for 2022.

How is the physical demand faring in the key markets?

Despite the ongoing macro headwinds, physical demand for gold has held up well in key Asian markets so far this year. Physical demand in Q3 was 875t, the highest third quarter demand since 2015. India, the Middle East, and Europe led the demand growth in first three quarters. While gold demand in the Middle East is likely to remain strong due to increased tourism, the physical premium in China and India is weakening. Surging COVID cases in China remain a key demand drag in November but we expect offtake to improve in December ahead of Chinese New Year in January 2023. Jewellery buying in India remained strong during Diwali. We believe improving rural income should see demand in India hold up well in Q4, though there will be a y/y decline due to exceptionally strong demand in Q4 2021.

What are the factors driving the outperformance of PGMs over gold?

PGMs are relatively less sensitive to the interest rate hike cycle, given their industrial exposure. These metals could withstand an economic slowdown next year as we expect demand to remain resilient and supply continues to struggle. Our positive view for PGMs hinges on the auto sector outperforming against the industrial sector. Improving chip availability and destocking of auto inventories should see auto manufacturers increasing their production, which should benefit auto catalyst demand for PGMs.

Technical

A short-lived price rise

The gold price rebounded strongly from its key support of USD1620/oz. Prices breached the downward trend line (USD1700/oz) and both the 50dma and 100dma following the release of weaker than expected US inflation for October. However, prices failed to break above August’s high of USD1800/oz level, which remains a key resistance in the near-term. Prices settling above this resistance will be crucial to confirm a bullish trend in gold. With the Fed expected to hike in December by 50bp and inflation staying well above the target range, we believe it would be difficult for the gold price to break this resistance before the end of this year.

Recent upside momentum is waning too as the RSI (Relative Strength Index) is reversing from its oversold territory. The dollar index is also stabilising after a sharp sell-off recently. We expect gold prices to take support at USD1700/oz, while prices could still test the downside of USD1620, which is a key support level in the nearterm. A break of USD1620/oz could potentially open the door for prices to fall below USD1600/oz.

Daniel Hynes and Soni Kumari are commodity strategists at ANZ. This article is a re-post from ANZ and is here with permission.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.