By David Scobie*

There’s no doubt the last two years have been full of extraordinary challenges.

Following the outbreak of the pandemic, the lockdowns and restrictions imposed by governments around the globe hit economies and markets hard and fast.

What followed was unprecedented fiscal and monetary support to avert an economic meltdown not seen since the Great Depression. However, the short, sharp recession followed by the recovery has brought about another potential challenge - the re-emergence of an old foe, inflation. The question is whether the return of this “ole devil” will persist and, if so, how it will affect portfolios.

Building a robust portfolio has got tougher

There is no shortage of opinions on the future trajectory of inflation. Most central banks around the world - New Zealand included - believe the current rise is transitory and inflation will fall back down to normal levels. However, inflation is notoriously hard to predict. It is driven as much, if not more, by collective psychology as any conventional mathematical formula.

While inflation expectations remaining anchored is, in our view, most likely, it is far from certain and definitely less so than before the pandemic. Portfolio construction needs to reflect this increased risk.

Traditional portfolios, dominated by equities and bonds, have performed exceptionally well through the disinflationary environment over the last decade and longer. But in an environment of persistently higher and more volatile inflation, they would likely experience a negative impact.

Why are inflation worries resurfacing now?

Since mid-2020, inflation has risen markedly. As countries whose vaccination rollouts reached critical mass reopened their economies, the sudden release of pent-up demand boosted by stimulus and unconditional handouts ran into supply bottlenecks.

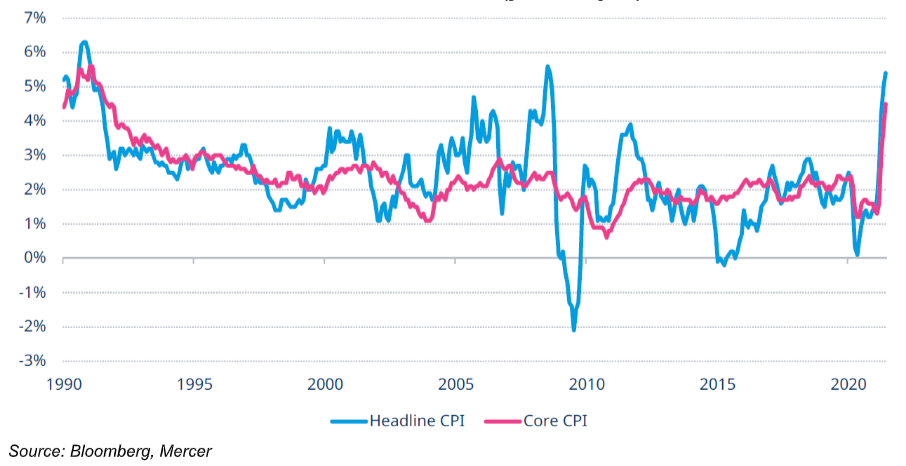

Consequently, goods shortages have arisen across the spectrum - from semiconductors and timber to household items and used cars. This has been compounded by the formula base effect - year-over-year inflation figures are still comparing to periods of lockdown or depressed economic activity. In the case of the US, as can be seen from the chart below, recorded inflation reached a three-decade high.

US Consumer Price Inflation (year-over-year)

This spike, in itself, is not necessarily a structural reason to worry about inflation risk. As noted, we believe the recent rise in inflation is likely to level out and gradually fall back toward central bank targets. Supply shortages should gradually dissipate as production picks up, continued global vaccination efforts should reduce labour shortages and the formula base effect will disappear. This is exactly why central banks describe the inflation surge as being transitory.

This relatively sanguine base case is not the only possible future state of the world, of course. What fuels our concerns over higher inflation risk and wider tail outcomes is not so much the lift in inflation seen in 2021 as it is the weakening of long-term secular, disinflationary forces in the background. The near-term rebound in inflation is merely a potential catalyst to knock loose the psychological anchor formed by central banks’ efforts of the 1980s and supported by globalisation and technology.

Central banks now appear to be putting as much or more weight on economic and employment outcomes as on inflation-fighting credibility. Fiscal authorities seem less concerned with the need for financial discipline and balancing budgets after periods of largesse, even though some countries have at least started to make an effort to reduce deficits.

More broadly, the populist renaissance over the last decade has seen globalisation, with its downward force on the prices of manufactured goods, under pressure. We expect technological progress to continue to provide a disinflationary impulse, but the push for energy transition and higher sustainability credentials in end-products will also likely prove inflationary.

Disinflationary and inflationary pressures

What implications would structurally higher inflation have for conventional portfolios?

Many portfolios have been constructed during, and for, disinflationary environments. Dominated by equities and bonds, perhaps accompanied by some diversification into asset classes like private equity, real assets and more aggressive credit-oriented fixed income strategies, such portfolios have performed strongly throughout the past two decades. The secular trend of declining yields increased discounted values of dividends and coupon payments.

Furthermore, portfolio efficiency was supported by the typically negative correlation between equities and duration, especially in major stress events, when it was needed most. With inflation low and cyclical, rising inflation was associated with economic growth that benefited equities and hurt government bonds due to central banks tightening policy pre-emptively and vice versa.

However, the market reaction to rising inflation is far less positive when inflation is already high, and, at this point, just when investors do not want it, correlations can become positive again. Adding a less predictable inflation environment now increases complexity for portfolio construction as asset allocators need to think about inflation sensitivity (“inflation beta”), not just growth sensitivity (“GDP beta”).

Scenario analysis is particularly useful at times like these, when the probability of a regime shift - specifically, a shift to a higher-inflation environment - has increased. History has shown us how frequently regimes have shifted between secular inflation and disinflation.

This informs our approach to allow for future inflation regimes to be materially different from that of the last four decades, even though a return to a benign disinflationary environment is also a possibility.

In Mercer’s portfolio modelling we consider different scenarios of how economies and markets could behave under different conditions. They span inflationary and disinflationary conditions, cost-push and demand-pull drivers of inflation, and strong and weak growth, factoring in the influence of central bank and government policy.

Strategies to manage different economic environments

Many portfolios have some diversification into asset classes that are better positioned for inflation risk - for instance, via listed or unlisted real estate - but that protection is typically for longer-term scenarios and those more reliant on growth, such as under a “financial repression” environment.

A starting point is to diversify that inflation protection. There is no single asset class solution that deals with inflation as a “one-stop shop.”

Even inflation-linked bonds, which may appear as the most intuitive solution given their contractual link to inflation, do not perform well in a range of short-term scenarios. This is because, in the near term, they are more exposed to changes in real rates than to changes in inflation expectations.

Over the longer term, the inflation linkage strengthens, but in many markets, investors are locking in negative real rates by investing in inflation-linked bonds. We see inflation-linked bonds as part of the toolkit, but more tools are worth consideration.

Investors could strengthen the growth-inflation relationship through strategies such as natural resource equities, active commodity strategies or core, monopolistic infrastructure, which thrive in a growth environment, where demand faces real resource constraints.

Where portfolios are typically most vulnerable, however, is in the more bearish scenarios, in which inflation is not transitory and central banks need to respond. In a rising interest rate environment, such as an “overheat” scenario, floating rate strategies, such as structured credit (for example, asset backed securities and leveraged loans) or some private debt issues, could fare better than duration-heavy bonds. This upside is constrained, however, to the extent that rates increase with inflation - rates are clearly below inflation today.

The scenario few portfolios would be well-positioned for is “pandemic stagflation”. Returns generated in this scenario by long-term assets like real assets or natural resource equities would be heavily dependent on the extent to which market fears of inflation translate into higher discount rates and lower valuations.

Commodity-related strategies or gold should provide more reliable protection. The former, because stagflation is often associated with cost-push inflation, of which commodity prices tend to be a key driver. The latter due to its safe-haven characteristics and higher sensitivity to inflation when accelerating from already-high levels.

Actively managed macro hedge fund strategies with a focus on commodities could also be well-positioned to pick up such momentum.

The devil is in the details

As no two starting portfolios look alike, and no single solution exists to protect against all inflation scenarios, investors and their advisors need to assess individual situations to determine appropriate action. In a generic sense, the mix of assets suited to the investor depends on specific criteria, such as:

• What inflation-sensitive assets already exist in the portfolio, such as equities and real assets

• Over what time horizon might these inflation-sensitive assets provide protection

• Under which economic scenario the portfolio is most vulnerable

• The type of inflation protection needed; that is, general CPI or specific types (education, healthcare)

• The liquidity budget and its impact on the ability to invest in private assets that have longer lock-up periods

• The governance budget and thus tolerance for complexity and monitoring of strategies

• The importance of responsible investment and non-financial considerations

To sum up, for the first time in a generation, investors need to seriously consider inflation. Although some disinflationary pressures remain, a number of factors have shifted in the past 18 months. The march of globalisation has stalled, governments are engaging in huge spending programmes and in some cases central banks have flexed their price-stability targets.

The range of potential inflation outcomes has increased. Traditional portfolios (dominated by equities and fixed income) offer limited inflation defence. Attaining exposure to a diversified blend of strategies, which seek to provide broad inflation protection in a number of different environments, offers investors the best chance of keeping the devil at bay.

*David Scobie is Head of Consulting (NZ) at Mercer Investments, a global wealth advisory and investment services business.

This article does not contain investment advice relating to your particular circumstances. No investment decision should be made based on this information without first obtaining appropriate professional advice and considering your circumstances.

41 Comments

A good article for this website.

In one word. Diversify.

The most important rule of investing. Yet often the most ignored.

A self-promoting poet?

:)

Ha yeah. In due course history will show some fund manager nailed it. He will be hailed as a genius - overlooking the fact that with so many different strategies, someone has to get lucky.

The world under rates luck.

Though a few debt free acres with you own energy systems may not feel like luck - but you were lucky being born with the ability to think, the brain to process and the opportunity to learn -and of course a country that allows..

Folks in the US would say we are lucky we can collect rainwater...

Let's see if 3 waters enables someone to regulate and then clip that ticket😕

Already happening with resource consent so why not go the whole 9 yards?

Sure will be a crazy world if we are charged for collecting rain water.

Don't you mean in one word "House" ?

If you don't know what to do?

No if you don't feel the need to do anything, just live in it. Sad but true, anyone with a portfolio of 100% houses has had returns beyond their wildest dreams over the last 12 months. Borderline criminal, its been like taking candy from a baby.

Yes some of the mature blue chip companies with PEs over 50 could be in for a selloff, together with the Kiwisaver conservative selling required before dec 1.

It's a conundrum for those approaching retirement. You want to have some cash on hand but inflation could eat it away. At the same time you don't want to take on too much risk. Shares seem a bit dangerous. You would want to hang onto any income producing property for dear life. Extracting capital from property could be more difficult once you no longer have a salary.

Investing in shares is not dangerous. Plenty of stunning companies to invest in in NZ and Au. I've been direct investing for nearly 20 years. Yes, a few duds that were more than off-set by the rock-stars. Focus on sectors. Think health, retirement, infrastructure. Plus you have the ability to free up $5k, $50k or $500k at the click of a button.

Very well said, Mountie.

If you don't have a small allocation to BTC now in your portfolio you are not properly diversified.

"If you as an investor believe that Bitcoin will perform as well as it has historically, then you should hold 6% of your portfolio in Bitcoin. If you believe that it will do half as well, you should hold 4%. In all other circumstances, if you think it will do much worse, then you should still hold 1%." Yale economist - Aleh Tsyvinski https://news.yale.edu/2018/08/06/assessing-cryptocurrency-yale-economist-aleh-tsyvinski

Wealth Management - https://www.wealthmanagement.com/alternative-investments/should-bitcoin-be-part-client-s-investment-portfolio

Its probably a less ethical investment than coal or tobacco, maybe even arms. I will die poorer and happier without it. The massive waste of energy and the obvious money laundering that the greedy will allow is staggering.

Man this is a hot take if I've ever seen one

You're incorrect on both of those points.

You might have missed the release of the Pandora papers this month, the biggest trove of leaked offshore data in history. Millions of documents revealing various offshore deals and assets of more than 100 billionaires, 30 world leaders and 300 public officials. Bitcoin was not mentioned once, not once in any of these illegal, semi legal and dubious activities. The most accurate current estimates based on chain analysis (not anecdotes) for the criminal share of all cryptocurrency activity is just 0.34%.

On the waste of energy front, those who claim that have a basic misunderstanding of how energy markets work. Bitcoin mining gravitates to the cheapest power sources so they can make profit, the reason a power source is cheap, is because there is no demand for it. Energy that is otherwise wasted, that cannot be moved to areas of demand. Things like methane flaring, and remote power stations where a significant amount is being produced for baseload but not being used. This reduces the cost of power for all other users from that source.

Most recent estimates are that the global mining industry’s sustainable electricity mix had grown to at least 56%, during Q2 2021, making it one of the most sustainable industries globally. This is actually lower than it was before China shut down mining, previously about 50% of the total hash rate was coming from Sichuan province in China. Because of their wet season there is an abundance of cheap hydropower there, much of which would otherwise go unused because it is difficult to store and transport to urban areas where there are consumers. At that stage estimates were that around 74% of all Bitcoin mining electricity was coming from renewable energy sources.

Bitcoin could be less ethical than weapons, that's a new one! There are valid criticisms but like most topics these days they are heavily polarised and propagandised on both sides for and against. The only mainstream "knowledge" of cryptocurrency through the media being BTC and its various scandels and criticisms, dog based meme coins and ridiculously priced NFT sales clearly doesn't help. Yesterdays comically non factual hit piece on stuff was a great example of just how bad the mainstream reporting is.

Oh god, you really can tell the people that have not done any further research other than main stream headlines since 2017....

Utter rubbish.

I can be properly diversified without bitcoin. What nonsense.

Bitcoin is a bet for most and a religion for some.

Absolutely No value aside from Market sentiment.

Huge fluctuations in worth.

Price only maintained by the oversupply printing of fiat currency that it it's meant to replace (oh the irony).

Hugely vulnerable to legislation change.

And yes, it's purely digital, so it is just an energy drain (not that a this is a bad thing, most of our lives are now digital)

And anything that can be created by typing out code is not Finite.

For what? No major sovereign will ever adopt bitcoin as the main currency. And if they did it would come with massive increases in regulation. Which kinda defeats the point of having an unregulated currency.

And if we are going to switch to a single limited supply digital only currency, central banks would just create thier own.

Enter “but when the world collapses the people will rise up and demand to use blockchain! For freedom!

Not saying don't invest in it if this suits your investment goals. But saying that you are not properly diverse without Is complete rubbish.

I provided you with a number of links from reputable sources that say you should have it, and the reasons why. It seems you didn't read them.

Diversification in a portfolio is about managing risk. "Owning Bitcoin does not increase portfolio risk, it reduces it. You are actually taking MORE risk by not owning bitcoin, than you are if you have an allocation."

If you are actually interested in learning something, here's a very detailed explanation from Greg Foss. He's a specialist in risk management in these markets with 30 years of experience in pricing and trading corporate credit and credit related structures. Everyone here should read this.

You only diversify if you don't know what you're doing.

This is the most incorrect statement that I have ever read.

It is interesting to see the number of likes for anti BTC statements that have little to no basis in fact. It's just regurgitating the same old mainstream arguments that have been debuked for over a decade now. This is a finance website, at some point it's ok to admit that you don't actually know much, and perhaps you should put some effort in to understand what is happening with this new asset class, that is not just going to go away. I'm happy to provide factual information for people to read and come to their own opinion.

See my below response.

I couldn't care less if Bitcoin is a good or bad investment, I don't know much about it, therefore it is RISKY for me to invest in something I don't understand.

That's absolutely a fair point. I do the same, and also not interested in property. I retract that comment.

You should read some of those links I posted. If you're primarily in stocks you'll find them interesting from a risk management perspective.

I also don't invest in things I don't understand but that does'nt mean I am against those who invest in bitcoin, if you are making money I say go for it. Plenty seem to be doing just that, good on them.

Keep fighting the misinformation Lasset!

I have given up posting useful links on Bitcoin, it is only the same people that are obviously too lazy to do any further research so it just goes around in circles. Time will tell, and im sure many people will do well without it but for hte younger generation it holds the most promise.

2010- No one uses it.

2012- Only computer nerds use it.

2013- Only drug dealers use it.

2014- Only money launderers use it.

2017- Only gamblers use it.

2019- Only a small percentage of the population use it.

2020- Only small companies use it.

2021- Only small countries use it.

How is it incorrect?

I don't invest in Bitcoin because I know little about it, likewise I haven't invested in Property. You're telling me I should put my money in different asset classes because of what some asset manager, journo, or economist says so? That is what you call RISKY. I invest heavily in stocks because I KNOW what I have bought, and have I have a sound understanding of business.

The World's top investors OWN what they KNOW. They don't diversify LOL.

Supply shortages should gradually dissipate as production picks up...

How "gradual" though? Shipping costs may dissipate as new ships enter the merchant fleet but renewable energy investment needs to climb a wall and the global workforce is falling off a cliff as more people retire than enter the workforce across many OECD countries.

Shipping can be solved in year(s), energy in decade(s) but there is no production line to replace your human labour. China will half its population in the next 30 years [link] and China is not alone in accelerating population declines.

Chinas population needs to halve, to many people. The cost of energy can only increase from here and its going to be a huge problem even with the current world population, it simply has to start dropping.

You won't be disappointed with China. Even Indias birth rate will be below replacement rate within a few years based on current trends (in fact it already is outside of rural areas.) With population decline comes immigration decline.

Less people during lockdowns etc working in the physical world doing real work with physical processes - manufacturing, logistics, extraction etc, so real goods are becoming scarce. So higher prices. Can higher interest rates really help? Tougher to fix this problem with QE & ZIRP this time.

Question: Was this all-time high inflation intentional? i.e. the stimulus & handouts planned in anticipation with pent-up demand?

If 'No', why wasn't it considered as a possible outcome and planned for?

If 'Yes', why would they do it that way?

Inflation has been *desired* by central banks for years now! They’ve been unable to generate it, despite their best efforts… until now. But they’re just starting to realise it can’t be turned off like a tap once you’ve reached the desired 2%…

Why worry about inflation as Mr Orr being governor of rbnz and who knows everything has assured that it is temperarory.

Though has not defined his meaning of 'Temepraroy' but assume should have been two quarter or three quarter of four quarter BUT knowing manipulative shrewdeness of likes of Orr, who knows as he can change the defination of 'temperarory' to a decade and should not be surprised.

Just today fed accepted inflation is not only because of supply crisis but for easy and cheap money policy......saying now, which we all knew....matter of time before Mr Orr too parrot it.

Ha! A much better article on investing.

Only wish Scobie would talk more on Greenflation.

So far oil and real estate had made the inflation a walk in the park for many.

Bitcoin

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.