The interest.co.nz team enjoyed our end of year function recently. We had much to celebrate.

And readers may also be interested in some of the 2024 activity and results that we shared at that function.

We have had a successful 2024 from a readership perspective. It has been a tough year for media generally, and we also suffer from being revenue-challenged. But we are engaging with a much larger audience this year, and that brings some benefits.

On our website we have a link that includes these charts.

This gives a good perspective on how 2024 compares with other recent years.

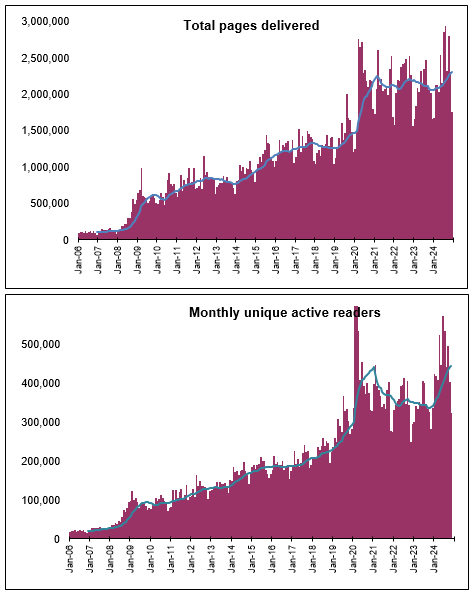

The top chart tracks the number of individual pages readers accessed. The bottom chart tracks the number of unique readers each calendar month. Both have grown encouragingly in 2024. The blue lines are the moving averages. In both cases we ended the year with the blue line at a record high.

In 2023, the reader-focus of the major stories were on the Savings aspects. In 2024 this shifted to a focus on Borrowing aspects.

In 2024, we delivered 27.5 mln pages of content (stories, and resource pages). That was up from 25.6 mln in 2023 – and was like having an extra month’s worth of content consumed.

We think we engage at least 2.5 million different people at least once in the year. That is because we recorded 4.1 mln “active users” in 2024. But many of them would have read us on different devices, multiple devices, so getting “active users” back to “unique people” is always going to be something of a guess. (Others pretend there is science to this, but those processes remain just 'estimates'.)

But we can record average session time. And that shows a high average, and a growing one. In 2023 the average session time was 3:56 mm:ss which we were proud of. In 2024 that rose to 4:37 mm:ss, which is a very heartening shift. And that is just the overall average.

Our mobile:desktop ratio rose to 60% : 40% from 55% : 45% in 2023.

Our gender balance stayed similar at 45% : 55% F:M.

Demographic records show little change there too, with 44% of readers 45yr and younger.

The news story read the most was one read 207,000 times.

But this was just the tip of a swelling catalog of well-read stories.

In 2023 we had 97 stories read between 10,000 and 15,000 times. In 2024 that rose to 107 stories.

In 2023 we had 23 stories read between 16,000 and 19,000 times. In 2024 that rose to 39 stories.

In 2023 we had 11 stories read between 20,000 and 29,000 times. In 2024 that rose to 41 stories.

In 2023 we had 3 stories read more than 30,000 times. In 2024 that rose to 22 stories.

And of course our data resource pages were read very heavily too. Most of the key ones were read more than 1 million times each in 2024.

2024 Projects

We completed some improvements in 2024 that will be important for years to come. We re-established some excellent insurance and climate change content, and added a Technology section. In the background we made some major upgrades to our Drupal CMS, and we developed a way to track the commission earned by the mortgage broking industry. There were a number of smaller improvements too. All contributed to the growing readership and engagement.

2025 Projects

At our end-of-year function we outlined a larger set of projects for 2025. But we will announce them when each is ready to launch.

One thing that won't change is our open and free access to almost all our content. We have no intention to add a paywall.

But all this is only made possible by the combination of judicious advertising, data sales, and readers support. And the most important one is readers support. We know readers like our content. We have GoogleAnalytics running live on our office wall, so we can stay abreast of engagement trends. But only a small fraction of our readers support us. They are crucial, and we would love it if you can join them. You can do so here.

There are direct benefits for doing so. You can choose an ad-free experience. And from March 1, you can continue to receive our daily and weekly newsletters right into your inbox. And you will still be able to comment after March 1 if you are a qualified Supporter.

Happy holidays to all our readers, Supporters or otherwise.

We will continue to update our content and articles over the summer break, and will return in full mid-January.

16 Comments

I have learnt so much by coming on this site both from the articles and comments. Thank you very much.

But all this is only made possible by the combination of judicious advertising, data sales, and readers support.

What sort of data are you selling?

Mostly granular interest rate data, but also other commodity and rural data too. (We never sell readership data.)

Good to know it's not readership data, thanks. Congrats on 24' & all the best for 25'.

I really hope the pay to comment does not destroy what defines.int.co.

It will be interesting

Methinks the "stack it high, sell it cheap" premise applies. But I expect i.co.nz have done their price discovery and know better.

Yes, it will be interesting.

Well everyone can still read the articles at will for free and that goes for the comments too. Some regulars here that are unwilling to pay for the privilege of commenting might though find themselves somewhat foiled by not being able to enter the argument and/or offer a rebuttal. Suspect some may find the temptation to enter the jousting, too difficult to resist. Who knows? We shall see.

Property articles seem to attract the bulk of the comments, a lot of them sour and snarky, and the vast majority of those commenters are free riding.

I'm kind of looking forward to some peace and quiet from the reflexive commenters, bots and old guys shouting at the kids on the front lawn.

Hopefully the too often extreme political partisanship will reduce and as well those using double identities, monikers to comment will disappear entirely. Every election year that unwelcome feature would appear, a little coven of head nodders and up tickers registering and then applauding one another. Very obvious, very annoying.

The_Golem,

I am curious about your non-de-plume. Like you, there are quite a few commentators I will not miss, but i think that in the end, many will pay up for what is a great site.

A man created of clay, animated and motivated by a sacred word in his head.

Seemed appropriate. :-)

Many thanks to the i.co.nz team for providing us with such a fertile and active financial think-tank.

In preparation for the wild ride that 2025 promises to be, both financially and geopolitically, we do however need to be acutely aware of what the global financial plutocrats have planned for Mainstreet, if we wish to minimise the fallout.

The most reliable and experienced global geopolitics analyst on the planet, Pepe Escobar, describes the 2025 journey as 'The Highway to Hell' - I happen to agree - it will be precisely that - especially if we are unaware of the grand heist that the global plutocrats have planned for us - we all must make provisions accordingly, but even if we have a basic awareness of what they have crafted over the last 50 years or so this will be a huge advantage.

THE GREAT TAKING - interview #2 by Paul Buitink of 'Reinvent Money'

https://www.youtube.com/watch?v=Jt0d70fqHok

Every NZer needs to be aware of the incredibly serious implications of what is planned to be the greatest heist of wealth from society in financial history.

... quoted...

"For some 400 years securities were your personal property, meaning that the public was protected in the event of a failure in the financial system because it was simply your property, and if it was not returned it was a criminal offence.

That is no longer the case - this has been subverted in a very deliberate process over about half a century - first in the U$ through changing the uniform commercial code at the state level, and then led by the State Department at the highest level, then forced globally including in Europe.

What has been done is to shift the certainty of control of the property from the investor to the secured creditors elsewhere in the financial system, so that in a systemic failure it is the secured creditors that will take the property

The claims of the public, including individual investors, pension plans, and all investment funds, only run to the first-level intermediary broker or the first-level custodian, but the property is not held there - it is held at a higher level on a pool basis, when it is used without restriction, and free of payment as collateral underpinning the global derivative complex."

................................................

And from...

https://trunorthpublicpolicy.com/when-the-locusts-come-they-eat-everyth…?

...quoted...

"So, what is the status quo under UCC Article 8 in all 50 states? A state-approved “bait & switch”. According to Cornell Law School a “bait and switch takes place when a seller creates an appealing but ingenuine offer to sell a product or service, which the seller does not actually intend to sell.” In other words – fraud. But that is exactly what your state law allows when it comes to your IRA, 401(k), or personal investments.

Under UCC Article 8, every time an investor directs their broker or investment advisor to purchase a stock, bond, mutual fund, ETF, etc. and your broker deducts the funds from your account to purchase the investment you do not actually receive the stock or bond you thought you bought. What you actually receive under UCC Article 8 is a ‘security entitlement’.

A security entitlement was defined by the folks drafting this law as ‘a bundle of personal rights you hold against your broker’. In plain English, you have a contract with your broker – you do not own the investment the same way you own a physical stock certificate.

Your broker, investment advisor, any custodians your broker uses for buying, selling, and holding these security entitlements are called ‘securities intermediaries’ under UCC Article 8. This is important because the law gives certain creditors of the securities intermediary priority over your investments in the event the intermediary (broker or custodian) fails and files for bankruptcy."

The Great Taking crosses partisan lines when lawmakers understand who stands to win and who stands to lose when the next financial crisis strikes. (as I write this the financial markets are in free fall – but the question is not if a major financial crisis will occur – but when) UCC Article 8 has clear winners and losers, and that is intentional."

......................................................

By the way, I am rather gobsmacked as to the childish behaviour of Chris...., a particularly prolific commenter - a few days ago I was greeted with this in the link shown...

https://www.interest.co.nz/economy/131348/massive-revisions-gross-domes…

"If I can respond in kind, Colin Maxwell, I find your ravings such a load of nonsensical drivel that I am surprised you can still feed yourself, or wipe your own bottom. Come to think of it, maybe you employ people to do that for you? I expect so."

As sad as pathetic attacks like this are, especially from people who choose to cower behind a nom de plume - it's like water off a duck's back for an old campaigner like myself. Nevertheless, it can be very revealing as to the true character of the commenter. We live and we learn.

Seasons greetings to all

Colin Maxwell

I've just been in the supermarket and thought I'd buy a magazine for the holiday reading, gosh a major shock at how much they now cost. As a subscriber myself I recognise the excellent value it represents 365 days a year. Come on folks - why not gift a subscription to someone this Christmas.

Tempted to gift one to JFOE to keep his comments coming :)

Quality and transparency in a particular market niche seems to work for both you and for your readers.

Other media outlets take note?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.