There's no question it was bad. But HOW bad?

That's what we are asking ahead of the release on Thursday, September 19, of GDP figures for the June quarter 2024.

I didn't have all the major bank economists' forecasts in front of me at time of writing this, but most estimates appear to be between -0.3% and -0.4% (although, ANZ is going for -0.1% ). The Reserve Bank (RBNZ) has forecast -0.5%.

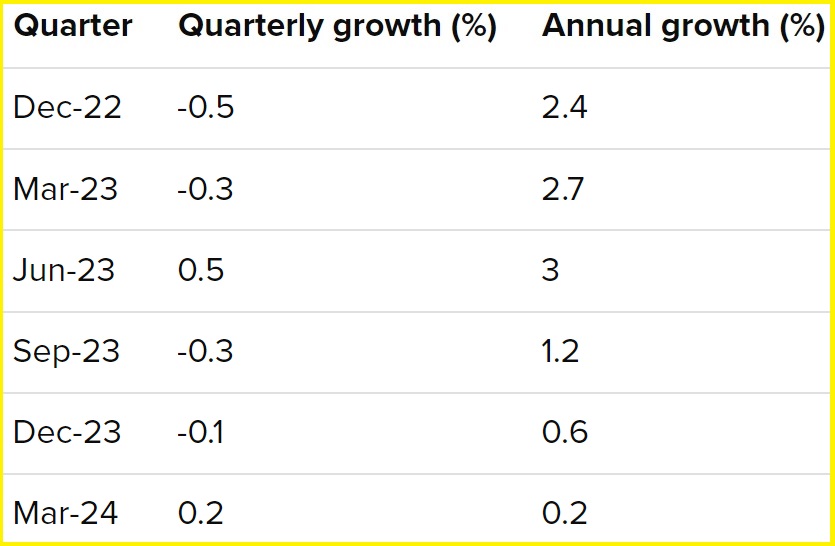

For some context, GDP figures for the past six quarters (up to March 2024) have read like this:

Well, plenty of room for improvement, isn't there?

But let's look on the bright side. At least the figure for March quarter 2024 didn't have a minus sign in front of it. And this means we are not as of now technically 'in recession'. Small consolation though. The fact is our economy's in a big hole, whether we are 'technically' in a recession or not. The past two years have really been a long rolling recession.

As can be seen from the figures above, our GDP has contracted in four of the six previous quarters. With the June quarter widely expected to have a minus in front of it, this means five out of seven quarters will have had our economy going in reverse. And just for the icing on the cake, the RBNZ is forecasting that the September quarter we are now in will also produce a negative outcome. So it might end up with us experiencing six quarters out of eight of negative GDP figures.

The current run of negative GDP outcomes can be compared to some of our more notable past economic struggles. For example:

- In the 1988-91 period we had six out of nine quarters of negative GDP, and then threw in a short, but sharp, two quarter recession in 1992 for good measure.

- During the 1997 Asian crisis we had four out of five quarters of negative GDP.

- From the start of 2008 and the Global Financial Crisis we had five consecutive quarters of negative GDP.

Even grim figures don't necessarily depict the 'true' level of grimness, however.

Arguably the most telling measure of GDP is the GDP per capita figure - namely how much each person in the country is producing.

So, how are we doing on that score at the moment? Oh, abysmally.

More hands producing less

It won't have escaped your notice that once our borders opened again after the pandemic, thousands of extra people started flooding in. What this means is that our basic GDP figures, bad as they've been, have been produced by a lot more people. Therefore they are even worse than they first look.

Already our current economic downturn is, on a per capita basis, more severe than the GFC was.

During the GFC period our per capita GDP fell 4.2%.

In the current downturn, up to and including the March 2024 quarter, our per capita GDP had fallen 4.3% (that's from the third quarter of 2022 onwards).

And regardless of how bad the 'headline' GDP figure for the June 2024 quarter proves to have been, we can say with confidence that the per capita GDP figure will have gone backwards again. So, the overall per capita GDP contraction is definitely going to end up being even worse than the 4.3% figure we currently have in front of us.

So, what can we expect in those the June quarter figures?

We can get some clues by looking at already released June quarter results from some of the key sectoral contributors to GDP - the 'partial indicators' as the economists like to call them.

The results have been pretty bad - but perhaps not quite as bad as might have been indicated other high frequency economic data.

Retail sales volumes fell by a chunky 1.2% in the June quarter, confirming what you've been able to see if you look around your local shopping centre. It's tough out there. Comparing June quarter 2024 with June quarter 2023, sales volumes were down some 3.6%.

The volume of building work put in place fell by 0.2%, although that was a smaller fall than some economists had expected. Nevertheless, it was the lowest volume of building work seen in a June quarter since the Covid-affected June 2020 quarter.

The volume of total manufacturing sales rose by a surprisingly strong 0.6% after three consecutive quarterly falls. Wholesale trade sales, however, fell on a seasonally adjusted basis by 1.1% in the June quarter.

What's it all mean then? Well, that overall picture highlighted above doesn't look great. But as stated above, these June quarter figures are now already vaguely historic. The fact that they will be some kind of bad really doesn't have much impact now.

The bottom of the cycle?

The RBNZ's decision to cut the Official Cash Rate in August from 5.5% to 5.25%, with more cuts likely to follow in short order gives good reason to think this might well be the bottom of the cycle.

The June quarter GDP figures are not likely to have an impact on the RBNZ. The only vague possibility of some impact would be if the fall in GDP was to be bigger than the 0.5% the RBNZ's forecasting. If the economic situation was looking REALLY dark then our central bank might consider doing a double-cut (50 basis points) to the OCR.

Indeed the financial markets ARE still pricing in a double cut before the end of this year, but I tend to think that's the markets getting ahead of themselves.

What we'll be mostly looking for from the June GDP figures are signs that the bottom has been reached and that maybe we can draw some positives and encouragement that the future is now looking 'less bad'.

But less bad doesn't immediately become good.

As said further up the article, the RBNZ is currently forecasting that the September quarter we are now in will also see the economy shrink.

It could be that the August OCR cut, with promise of more cuts to come, may just turn things around enough for GDP to creep positive for the current quarter.

Realistically though, regardless of whether the September quarter sees a plus or minus GDP figure, it's difficult to see the economy getting much momentum until into 2025.

Much will depend on how quickly there is a positive reaction from businesses and individuals to the encouragement of lower interest rates. Early signs have been good. We saw a big bounce in business confidence in the latest ANZ Business Outlook survey.

However, to express confidence through a survey is one thing. The real test is whether such confidence is backed up with actions.

Economic growth

Select chart tabs

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

146 Comments

The real question is will any of my favorite restaurants survive.

Please Allah don't take Prego.

🥂

... mine was the Foosan , near Canterbury Uni ... when they retired , it left a huge hole in our life ... praying that our patronage keeps Daphnes going ...

Daphne's is the Greek joint?

Yes hope they survive also 🙏🏽🥂

Chinese : at Church Corner in Christchurch .... good value for money , and Monsoon ( Harringtons ) beer ...

Harringtons are brewing again?

Was not aware that they'd stopped brewing .... the Ngahere Gold seems to still be about ... Monsoon is a range of 3 pilsners they brew & supply to Asian restaurants ...

Harringtons were sold to NZ breweries (lion) in about 2019 and as far as I know the only brew they continued was Rogue Hop...and theyve changed the mix.

They closed the Wigram brewery in 2021 and the range steadily decreased from then.

Foosan is gone? Many a memorable byo had there in my student years. Unbelievable value.

... the restaurant has new owners ... the original crew of old chefs & staff are gone ... sigh ! Very sad .... they were legends ...

Too late for me, SPQR has already fallen. A more recent favourite is Origine so hopefully that lives on.

SPQR has found new owners. "Origine" is indeed very good.

The bottom of the cycle was in mid-2023! This is clear from the most basic of available data. The risk that we should have been managing since before then is a painfully slow recovery, spiralling unemployment, or, even worse, a dip back down again.

Now compare the credit anatomy of the GFC vs the 23/24 self-inflicted disaster. What do you see? Govt turned up the deficit spending in December 2008 (broad money increase) and this plus Chch EQ investment dragged the economy, GDP, employment etc up (albeit painfully slowly). This time, Govt purse strings are pulled tight. The risk now is a turn for the worse. It's so obvious it hurts.

Yip I think we’re just about to get started. People talking about ‘recovery’ but I don’t even think we’ve had the recession yet! That is coming the next 12-24 months.

Yes, I flip between thinking it's late 2008 or 2010. Note that we had a dead cat bounce in 2009 and that was with pretty significant Govt fiscal support. We're heading into 2025 with no obvious stimulus in sight.

Haha I sometimes think it’s 1929 but then get worried about just how crazy fiscal and monetary policy responses might be if things really start crashing down hard - and then what happens to inflation if we do 2020-2021 again while not increasing the quantity of goods and services produced in the economy (ie we this huge amounts of stimulus into the economy again but only produce more of the problems we already have - overpriced assets, high debt to GDP etc). So part of me hopes we actually just let the ship sink a little this time to bring back some sanity despite how painful it will be for some in the economy. Ie let’s reduce private debt to GDP so we can raise future mortgage rates if need be.

Like I said, November 2023 was the time for the RBNZ to start easing.

Now, almost a year later, we're starting to see easing ... But only after the RBNZ has ensured we've sunk even further. And the further NZ Inc. goes down, the greater the damage, so the longer it will take to come back up.

Even if the RBNZ cuts a further 0.75% - making a full 1.0% - the OCR is still contractionary by a full 1.75%.

(i.e. Year end OCR of 4.5% less the RBNZ estimate of a neutral OCR of 2.75% equals a contractionary difference of 1.75%.)

Do we need further contraction ???!!!??? [rhetoric question]

(Saw in the news today: "Hold prices, and don't forget a 1% price increase means an 11% profit increase." OMG ! Perhaps we do.)

The Christchurch earthquake happened in 2011 not during the GFC period.

Lol, yes, and the recovery from the GFC took 10 years! It would have taken longer if we had not had the Chch investment (including offshore reinsurance money).

Many people miss this when they look back with fondness at the John Key rockstar economy.

That chart doesn't show the bottom of the cycle in June 23. It shows that the speed of decline peaked in June 23 - but growth is still negative in the following year so it clearly didn't bottom out at June 23. You should probably correct your comment above.

Anecdote:

Visted my local Saturday market for the first time in several years. Half the stalls have disappeared and normally I can't move for the crowds, but not the case this time. Generally only Boomers doing any spending. Times are grim indeed.

We run an Airbnb in Central Otago. It is dead, few bookings, even less views. Our competition is the same. It is weirdly quiet. Feels bleak.

It has the sniff of the 80s all over again...but this time without the semblance of a plan.

If you look at asset markets yield curves and wealth inequality, it’s possible we look more like the late 1920’s just before the Great Depression (not a forecast but there are similarities).

New Zealanders work hard. But we are crap as a nation at retaining the benefit.

Ultimate benefit flows to the owner - always.

As a nation we need to get back into owning our stuff. And as individuals get rid of the idea that debt works for us.

Would our nation pass the EQ marshmallow test? Don't think so.

We work hard to the benefit of others because we do not save enough, and rather than investing such small savings in the real economy, we waste economic resources in parasitic housing speculation, thinking that we can get wealthy by selling houses to each other at progressively more unrealistic prices. Economic stupidity at its worst.

I think this and KH's comments sum up perfectly why we are in the situation we currently find ourselves.

Yes. Well said.

For people to be saving, others have to be borrowing. The savings we have are in large part a direct product of our housing ponzi scheme. Perhaps the savers are the real parasites? I agree with the basic thrust though - we need to direct investment into productive public and private enterprise that improve our lives.

The ones I know with a large quantity of cash are those who are 65+ are mortgage free and have reduced their exposure to the housing market so they have savings available for retirement ($500k +).

I wouldn’t call those people parasites (they weren’t buying up homes in competition with FHBs - they’ve downsized their housing situation into something smaller and now have cash on the sidelines).

The parasites in my opinion are those who have been hoarding up existing houses in competition against FHB - ie greed to own more than what they need to line in themselves.

Those with the savings now can drive future investment - and it may not be into the housing market because as I say, those I know with savings aren’t interested in buying up houses given their age/living situation. At present many (that I’ve provided advice to) are mostly in TDs/cash and now rates appear to have peaked into bond funds - if sharemarkets come crashing down as yield curves normalise, then investment could be made into some appropriate shares as well.

There could be a generational shift away from this obsession with housing as millennials own their own homes and boomers are downsizing/dying (ie the two largest demographics who have been competing with one another the last two decades for the same/similar houses ie family sized dwellings)

Sorry, that parasite comment was a little dry. My point was that all of the bank deposits in NZ started life as loans - and the vast majority of those loans were for housing. The more people borrow (net), the more other people can save (net). I tend to think of investment as being dependent on loans, and savings as financial assets. I know that economic models assume that savings drive investment, but that is because most economists don't understand how things actually work.

Perhaps your mental model is based upon ever increasing private debt to GDP which isn’t actually sustainable over the long term and it has been that increase in private debt that has created those savings that those I mention above currently hold. As I say we may now have a reverse of the cycle the past 30 or so years where private debt has skyrocketed compared to GDP - so my question is where do those with the current savings as a result of past loans deploy their cash in the future? As far as I can see it isn’t going to be into housing.

Hoe does your mental economic model look with falling private debt vs GDP?

Perhaps your mental model is based upon ever increasing private debt to GDP which isn’t actually sustainable over the long term and it has been that increase in private debt that has created those savings that those I mention above currently hold.

Compare NZ to Japan h'hold debt to GDP from the early 90s - ours takes off when bank regns shifts the focus to building the Ponzi while Japan's remains flat. Now, we also know that Japan's public debt took off at the same time - after the bubble burst, huge public spending on white elephants and infrastructure projects to keep the economy moving.

Debt deflation is accompanied by flat or falling pvte deby.

https://tradingeconomics.com/new-zealand/households-debt-to-gdp

My mental model is based on either Govt or Banks creating money through deficit spending or new lending. The net flow of new money into the economy has be high enough to satisfy domestic and offshore savings desires. The offshore savings desires are obviously a side effect of (and in proportion to) our current account deficit.

So, if domestic savers are saving 2% of GDP and our current account deficit is running at around 3% of GDP a year (adding to offshore savings), then we need a net flow of new money of at least 5% of GDP - more like 7% once you allow for how slowly money moves around the economy these days. That was the norm from 2011 to 2019 when private sector debt hovered around 150% of GDP.

Since 2022, our current account deficit has been running a lot higher at 6% to 8% of GDP and the net flow of new private debt has dropped to 3.5% of GDP. Thankfully, Govt have taken up the slack - deficit spending at 5% to 7% of GDP. This has allowed us to manage private debt levels down to just under 140% of GDP (a Govt / private debt swap).

So, to answer the question, we could manage private debt down. We would need to both increase Govt debt and do something about our current account deficit. Electrification would make a massive difference given the cost of imported fuel. As would reducing our car obsession. But, a 10 - 20 year economically literate plan seems a long way away at the moment.

LOL. In my 'mental model' - you're both missing the point.

My mental model says:

1. We need to create new stuff faster.

2. We need a faster reduction in what we consume that is limited or bad for us.

Case in point: I_O: "At present many (that I’ve provided advice to) are mostly in TDs/cash and now rates appear to have peaked into bond funds - if sharemarkets come crashing down as yield curves normalise, then investment could be made into some appropriate shares as well."

Is anything created with this behavior? Mostly not. Buying stuff that already exists simply shifts the ownership. Classic rentier behavior - buy low, sell high.

Case in point: Jfoe: "My mental model is based on either Govt or Banks creating money through deficit spending or new lending."

So what happens bright spark comes along with idea that destroys 'money'? I did a skunk project for a government that resulted in 100s of millions being written off and 1000s having not getting a promised job. On plus side, it also resulted far less fossil fuels & roads being consumed, and saved millions of hours of people's lives that would otherwise have been little more than paper pushing. My bright idea reduced the money supply and reduced economic growth when measured in money spent. Weird huh?

I_O: "Those with the savings now can drive future investment - and it may not be into the housing market because as I say, those I know with savings aren’t interested in buying up houses given their age/living situation. At present many (that I’ve provided advice to) are mostly in TDs/cash and now rates appear to have peaked into bond funds - if sharemarkets come crashing down as yield curves normalise, then investment could be made into some appropriate shares as well."

Please do explain how you believe these risk adverse older people will drive future investment by holding their untaxed capital gains in TDs. ;-)

If history is any guide, because returns on TD's are so low, banks will have no issues throwing the money they create into yet more risky housing loans, you know, growing the ponzi.

Jfoe. With saving emphasis, actual investment including a muscular Kiwisaver, New Zealander's would be extending ownership offshore and reducing foreign ownership our onshore jewels.

Yes that means others are borrowing from us, and I am happy with that. And ownership control earns well beyond the trading profit. Bonus.

Our current account deficit has been negative for 50 years. We have zero chance of reversing that position without a very significant change in economic policy. The idea that we can become net lenders to the rest of the world seems fanciful. Furthermore, we are increasingly paying for services offshore - software licences, franchise fees, video streaming, return on bank equity, global reinsurance, etc. Unchecked, this outflow will grow and grow, leading to increasing offshore savings, and increasing offshore ownership of our domestic assets (generating further outflows of rent).

Jfoe says

"...We have zero chance of reversing that position without a very significant change in economic policy..."

Yes exactly. We need that significant change in economic policy. Let's get on with it. I have no time for those who point out the tough things in that.

The alternative is the death spiral you describe in the rest of your comment.

"We have zero chance of reversing that position without a very significant change in economic policy."

That policy change may well be forced upon us...and perhaps sooner than we think.

Nope. Much further away than you think.

Government - both central and local - would need to sell off much, much more of the family silver for that to happen 'sooner than you think' (which I took to mean in the next 30 years).

For people to be saving, others have to be borrowing.

Much as I rate your comments highly Jfoe, the above just doesn't ring true to me. For example, I saved quite a decent amount exporting IT consulting services to Australia (sometimes flying over there, sometimes working remote from NZ). I saved, no one in NZ had to borrow.

I agree that while I was doing that in the 2000's and 2010's, many more were getting rich via house trading and your statement works for them. But that isn't a reason to dismiss the notion of saving as being of limited value due to it being offset with borrowing. Exports pay some of our (NZ's) way in the world, I wish they paid all of it!

Sorry, no offence intended. I was talking in aggregate. People selling stuff abroad do build up savings, yes, but at the aggregate level those savings are outweighed by savings offshore (because we run a persistent 50 year+ current account deficit). What always amazes me is that it would not actually take too much to balance our current account. We would need to get off imported fossil fuels - and perhaps export some more renewable electricity (in high-energy products like datacentres, aluminum etc)..

Great to hear Murray. You were exporting, while the Australians were importing.

We need much more of this.

It always saddens me when the NZ Government (and some businesses) does the reverse and 'outsources' I.T. stuff offshore because it 'costs less'. A growth opportunity lost. If we need these generic skills in NZ, invest in growing new ones.

Its not like we have an alternative, have you seen the state of the NZ stock market? Anything decent has decamped to the ASX. And if you want to invest in overseas companies, you are hit with a wealth tax (aka FIF). Why are we surprised that people pile into property?

If you want to change investor appetites the first thing that should be done is to merge the NZX with the ASX, align the dividend franking/imputation credits across both countries, and remove the FIF tax (if not on all overseas stocks, at least on all ASX listed entities). Then people might start migrating money away from the property market.

A tax advantaged superannuation scheme similar to Australia would also be greatly beneficial.

NZ Smartshares ETFs?

There's an exemption on FIF for many ASX listed shares & an IRD tool to check

https://www.ird.govt.nz/income-tax/income-tax-for-businesses-and-organi…

The exemption does not cover ALL ASX shares, only some. It should encompass anything listed on the stock exchange. People shouldnt have to avoid certain investments because they will be hit with FIF taxes. Tax returns are already complex enough with foreign exchange and withholding taxes.

For clarity, I couldn't agree more. The FIF is blatant ticket clipping of unrealised gains (& completely ignoring losses).

Very hard to see consumer confidence returning when the consumer sees their friends and neighbours (and maybe themselves) losing their jobs. I think everyone knows someone who has been made redundant lately. Big business and SME's are finally biting the bullet and making cuts, and the cuts are escalating.

The Reserve Bank is forecasting a rise in unemployment to 5.4% by May 25, a quite savage increase from here, in a short time. I concur with Jfoe above,

The risk now is a turn for the worse. It's so obvious it hurts.

Can someone detail what the coalition's plan is to get us out of this nosedive...? I am at a loss..

Fast-tracking hundreds of economy-boosting projects, signed off by ministers if the panels don’t approve

whoops…….

Roads to prosperity?

... the Gnats appear to be under the spell that John Key is weaving ... traditional steady as she goes , don't rock the boat ... which means , even if we pull out of Robertson/Orr's triple dip recession , we'll putter along slowly towards the next crisis ....

True structural reform is required ... don't hold your breath waiting ( if you pass out , our healthcare system is too rooted to revive you ) ...

You don’t think National contributed to the problem? For example had they not removed the full employment mandate I think the RBNZ would have started cutting at the start of this year. And sacking half the public service was never going to help either.

No , the Reverse Bank ought to focus on one thing : Inflation ... as they amply demonstrated during Covid19 , they're not even competent enough to do that ... Orr shouldve been booted out ...

"Orr shouldve been booted out ... "

So another broken promise from National then?

Conversely if there hadn’t been an employment mandate under Labour the RBNZ may not have cut so hard and fast in 2020, setting up all the problems we now face

... good point ... that mandate may have made a bad situation worse ...

I think it was poorly implemented. It should have always been a secondary goal, the primary goal should have been inflation within band.

At the moment the RBNZ don’t need to cut the OCR unless they think we are heading under 2%. It’s rubbish that they should be encouraged to run much higher unemployment than necessary just to have inflation at 2% instead of 2.5%.

We sacrifice the few in order to benefit the many. Inflation is far more destructive over time, then a small rise in unemployment.

But an obsession with 2% is just crazy. At some point unemployment is more important than a very slightly high inflation figure.

Perhaps, but not nearly as crazy as excluding land / property price rises from the inflation measure.

In short, we've had lower interest rates than we should have for over 20 years now. I didn't hear people complaining then. Some 20+ years later and still we don't like the taste of the medicine, one more kick of the can please, just one more and I'll be alright...

Did you complain and fight the good fight over the last two decades Murray…I assume you offered to pay higher interest on your loans as matter of good morals eh 🙄🤦🏻♂️😂

LOL. Did you think for any time before writing that?

Hint: with higher rates and house prices not exceeding the rate of inflation people would have borrowed less and would be making monthly payments of far less.

Murray is not wrong in his observation.

LOL. Yep I did.

Hint: you are bang on, well, maybe...if that's what Murray meant by his comment. What grinds my gears Chris is that I would imagine a lot of the commentators on here, and maybe I am unfairly throwing Murray in this mix, would have done bloody well out of the two decades of low interest rates and high capital gains...so I am a bit tired of hearing them now spout on about the damage it has done. Are they wrong, nope, it is potential hypocritical behaviour...maybe. But hey, each to their own eh.

maybe I am unfairly throwing Murray in this mix, would have done bloody well out of the two decades of low interest rates and high capital gains

I agree many have, I would have done better to put my money in property and not worked a day. I worked, exported, saved and paid tax in NZ. All to receive zero thanks other than as you point out - lower interest rates on my savings to support the leveraged.

Did you complain and fight the good fight over the last two decades Murray

Yes, I have been outspoken on the foolishness of bidding up the price of existing housing stock for decades.

I assume you offered to pay higher interest on your loans as matter of good morals eh

I didn't have any, but I guess I did accept lower call and term deposit interest rates than would otherwise have been the case. Does that count?

"Conversely if there hadn’t been an employment mandate under Labour the RBNZ may not have cut so hard and fast in 2020, setting up all the problems we now face"

Say what?

By the end of 2020 we had the beginnings of a severe labor shortage ...

Wages were rapidly rising in many sectors ...

Consumers were 'revenge spending' ...

There was no risk to jobs at that time - The employment mandate shouldn't have factored into to the RBNZ's thinking.

Did the RBNZ decide to raise rates to slow the economy? No they did not.

The OCR didn't get into the even the mildly contractionary zone until Oct 2022.

And didn't get to 5.5% until May 2023.

And it wasn't just cuts to the OCR either. The RBNZ threw millions at the banks so they could lend like crazy (and make obscene profits to boot). Pretty damn hard to understand how the employment mandate played any part in their decision making processes once we'd come out of the first lockdown.

The large majority of such jobs in the public sector were never real in the first place, but only created by an incompetent socialist government under the ideological premise that money grows on trees. Such jobs were never sustainable.

Except for the ministry of red tape cutting..I wonder how their KPI's are tracking?

... the government could set up a working group to look into that .... .... oh , no ... that's right , Labour aren't in power now .... teeeee heeeee ....

That might be true, but it was the wrong time to make those cuts.

The expansion of the public service was a part of the COVID response.

You know - a two pronged approach - 1) keep people in jobs so they could continue to spend into a hard hit economy, and 2) set a floor under the number of unemployed so that heaps of unemployed meant businesses could pay less.

Half the public service should go but they always sack the wrong half. The good workers leave and find jobs where they are appreciated and the incompetant hang on desperately.

Well put! Mostly true

Also the fact that you leave the organisation itself to make the cuts, so they sack the people who don't agree with their ideologies, thus entrenching them. If NACTNZ wanted to make true changes, they would select the redundant themselves, not leave it up to the people who hired them in the first place. You see this in the hospital system already - instead of making cuts to management, management are making cuts to operational staff thus increasing the problem. The real hangers on will never agree to sack themselves.

Yeah I hear this all the time. It's ignorant reckons. Big organisations require bureaucracy, end of story. There is no silver bullet where we just employ doctors and nurses.

The more complex the organisation and objectives the more bureaucracy.

The front lines always get hit because those imaginary savings don't exist anywhere other than the minds of those who think public sector wasteful, private sector efficient. It's a myth peddled by libertarian know it all's. As soon as they have to actually deliver those imaginary cuts and increase efficiency they end up creating more bureaucracy eg. Seymour's ministry and Winston's bureaucracy not having to make cuts.

All part of the culture war narratives that it's all going to shit and we need radical conservatives to rescue us. The actual issue is increasingly unequal distribution of societies resources in favour of the super rich. The solution is more equitable taxation.

Disagree. These organisations used to operate in the past with far less bureaucrats and delivered far more front line services. Spark(Telecom) is a mere shadow of its former self, yet it still delivers phone and internet services. Look at the staff to student ratio in Universities - they've blown out to ridiculous proportions. 14 layers of management in the hospital system. 69,000 extra public servants were employed by Labour - what contribution to output have they made? Everyone hired in the last 6 years needs to be sacked, and then some more.

All these places need to go full Elon Musk on their staff. Sack 80% of the non-producing people and see what breaks. If nothing, you have the right staffing levels.

Agreed. By head counts, many government departs are sizable 'businesses' that most commentators here probably have no understanding of.

Key and English ripped up Labour's budget in 2008 and turned on the deficit spending taps. They still under-cooked it, but Luxon / Willis appear determined to avoid doing what is plainly required. It is crazy.

I don't know what their plan is or even if they have one. Even if they do have one it is or has been poorly signalled ( I would argue that this applies to our government and major businesses - . an example is the uproar of spot power prices - it happens , has happened in the past and will happen in the future - where was the planning Both the government and the major businesses seemed like deer caught in the lights of an on coming car).

The question / answer in the end is what is YOUR plan - how are you going to react.

I'm pretty sure dry year electricity planning was a UoA engineering school final year systems project circa 2016.

There cannot be a plan that works when Government has to look over its left shoulder at what the next MMP election results could be.

One thing is for sure. Putting the last lot back in will not improve anythng.

But removing MMP would stop all This namby pamby, woke, and compromised, decision ( or lack of it) making.

MMP = you don't get what you vote for!

MMP allowed the loonies with 5%, and Maori seat winning super minorities to much say on money wasting non important issues.

As a dual nationality POM-Kiwi much as I grumble nobody can persuade me that the last 25 years of Britain's first past the post produced better govts than NZ. Instead of moving towards a dictatorship my the biggest party why not try Switzerland's system with everything delegated to the lowest level of govt with many referendums.

Seeing how the UK general election went with FPP and Labour there getting ~30% of the vote I think ours is far superior not with standing a wart or two on the 5%. There would be no 5% if the Nats had tuned there policies better, copying one or two from NZ First and Act. I'm quite happy having both Act and NZ First putting there oar in.

Same, I like the fact that different parties can represent different people's wishes, and we all get a bit of what we voted for. I voted for the first Labour/NZ First govt and found that reasonably amenable because Winston seemed to be a sensible handbrake on Labour's truly stupid policies. The real problem came when Labour got a 50% majority in 2020 and went beserk, destroying entire industries and making half the country hate the other half (be that by race, gender, class, wealth, asset ownership or whatever other "identity victim" Labour tried to create). Imagine how bad things would be if Labour got to do that with a mere 30% of the vote?

making half the country hate the other half (be that by race, gender, class, wealth, asset ownership or whatever other "identity victim"

Labour didn't do that. Making half the country hate the other half is the culture wars playbook and it is largely funded by right wing interests. Labour were victims of that actively funded communication campaign, NACTNZ will also become victims off it. The plan is to erode societal cohesion so that it can be exploited by commercial interests.

You may be right, but it was Labour and Jacinda Ardern that introduced it to NZ. It wasnt John Key, or anyone before him. And the level of entitlement that has been encouraged is predominantly in those traditional Leftist voter "victim" groups.

The entitlement and victim mentality has always been around, slowly growing, more so since the polarising impact of social media. People were scared due to the pandemic, and they latched on to what is familiar and comfortable to sooth this psychological need for connection which they lacked due to isolation. Sadly many latched on to social media more and became more polarised, latching their sense of identity to beliefs etc which again was more severely enhanced by the likes of mandates. This coupled with the sad truth that many lost connection with friends or families over such polarising issues, that this reinforced again the connection in the sense of identity to ones beliefs, thus drowning out the ability for many to consider other points of view and see things objectively. Luckily the ability for critical though, though quelled somewhat by the above is gradually returning to the masses. The greatest example of which is the ability for society to evaluate the performance of their government and vote accordingly.

My anecdote: the bigbox retail business I work for is doing really well the first 2 weeks of September after 3 months of relatively bad sales (10% down on last year each month)

Our business has seemed to mirror gdp growth good and bad so will be interesting to see if this is just a blip or if things have actually turned a corner.

... our factory uses massive quantities of electricity ... the escalation in spot prices is smashing the profits into the dust ...

NZ desperately needs a truly reformational government ... Labour were the opposite of that , the Gnats are only mildly competent at it ...

What would you suggest...nationalize Contact Energy and Manawa? Well, the Government already has a majority shareholding in three of the four biggest power companies so they can call the tune regarding the price of power. At any time, with their majority shareholding, the Government can opt to reduce the retail price of power to customers. Then, to remain competitve Contact Energy ( fully privatised ) would have to follow suit or lose market share.

Contact Energy is looking to buy the smaller Manawa and, of course, the Commerce Commission will have a close look at that and hopefully not just use it to justify their existence and show that they are not the toothless tiger we have witnessed up until now. This would be a huge mistake because a larger enterprising Contact is probably what is needed to keep the other three government-controlled power companies from just providing an easy source of revenue for the government A well-resoured Contact will be essential in the push to develop clean energy and put an end to the importation of 'dirty' coal.

.

.. I would suggest massively increasing competition within the energy market , getting the government out of the way of the competitive market place ... splitting energy producers from energy retailers ... creating infrastructure funds to provide funding for private dwellings to set up solar panels ... a massive ramp up in wind , solar & geothermal energy production ....

That approach has never delivered lower costs, it results in private monopolies that run down public infrastructure and make people pay more for the same thing. It's exactly what got us where we are in the first place.

LOL. Did you experience any cognisant dissonance when writing that? Even just a little?

Here’s my anecdote.

Spent much of yesterday in Ponsonby with an old friend back for a week from Japan. We walked the length of Ponsonby Road and back, having a good chat on the way. Btw both of us think Ponsonby Road has become something quite special, ‘world class’ even.

What we noticed is that it was superficially busy. A few of the trendy restaurants and cafes were absolutely pumping, but many places were moderate or quiet. Many of the shops were fairly quiet or dead (we popped into quite a few along the walk), of course the occasional was busy (eg. Decjuba’s discount shop)

This is the kind if thing I have noticed at the malls over recent months - superficial busyness, but not much below the surface

Btw both of us think Ponsonby Road has become something quite special, ‘world class’ even.

Why? Compared to what?

Number of new developments, lots of new eateries, stores, boutiques etc. some quality modern architecture.

I would rate it as highly as Daikanyama in Tokyo, for example.

In terms of a character-filled, hipster-ish precinct

I wouldn’t have said this 2-3 years ago

That’s just my opinion of course

I would rate it as highly as Daikanyama in Tokyo,

OK. I wouldn't rate Ponsonby as nearly as hip and fashionable as Kita Horie in Osaka.

Even before Covid, NZ has been over-supplied with restaurants and take-aways. Even the so-called best of them are mediocre. I mean all the meals are based on Canola oil, which is not surprising I suppose because Canola oil has now become well and truly established as our main food staple. We should be producing it in New Zealand to save on overseas funds. 99% of packaged food concoctions in supermakets these days have Canola oil, or other branded oils, as an ingredient...soups, icecreams, packaged meals....virtually every shelf item.

A great stroke of marketing genius to rebrand an industrial lubricant as food.

I’m not convinced a casual observer could notice a small decline in retail spending. Can you really look into a shop and say “hey there’s only 9 people in there instead of 10”. If the decline is noticeable it would have to be massive, I doubt the next card payments data will show anything that big.

I usually judge it by how full the carpark is. When you can easily get a car park when normally it takes a while, then you know that retail spending is down.

Hipsters walk, bike and Uber, don't ya know. ;-)

Throw more and more people at a construction site and work will become less efficient and slow down. If a farmer opens up more and more fields without expanding other aspects, none of them can be plowed, seeded and tended as well as before. Taking on more and more debt at artificially low rates means much of it will not be productive.

In the aggregate and in the round, industrialised economies operate no differently from family units. Things just take longer. Over the last two decades (and longer) in the aggregate and in the round NZ has taken on much unproductive debt. The question of why productivity is slipping, is now easily answered. The action of taking on this debt was enabled by low interest rates. Like any price control, moving the price of money over time (interest) reduces willing seller-willing buyer dynamics and causes distortions. Which is what we now have; distorted low productivity. Debt is being serviced and repaid but we don’t have properly reflective increased productive capacity to show for it.

That’s it in a nutshell Macroview, money got so cheap we stopped looking after it.

"Throw more and more people at a construction site and work will become less efficient and slow down."

NZ could throw heaps more people at a construction site before there was a noticeable drop in efficiency.

No. Wait. We couldn't because our project managers are absolutely hopeless. (The good ones have left and are working overseas.)

GDP Bottom reached? Maybe. But I expect near flatness from here over the next 6-9 months, with potentially some little dips negative again in terms of GDP growth.

improvements from this time next year

I personally think you’re overly optimistic (same with your house price forecast) but I guess we will see. My view is things are going to get a lot worse as the yield curve normalises now and through the next 12-18 months

Heard Ashley " boom boom " Church on NewStalk ZB yesterday , 4-5 pm ... joyfully announcing that when the RBNZ drop the OCR rate further ( because businesses are dying & swathes of Kiwis are losing their jobs ) , the property market will burst forth , prices for houses will soar once again ...

OMG ... what a cretin !!!! ...

I respect your views and you could well be right.

I think OCR cuts will start to stabilise things

To 'stabilise things' would need an OCR at the neutral rate, i.e. neither contractionary, nor stimulatory.

The RBNZ say that is 2.75%. I.e. mortgage rates at 2% more, about 4.75%.

Or maybe the RBNZ has the neutral rate all wrong? :-)

Here’s the plan https://youtu.be/rMePrwQfT5I?si=2aYOLZSxrYOLresM

.. sadly , that sums things up ... the Gnats aren't as completely useless as Labour were , but are still not nearly good enough .... very very far from what the nation needs ....

When he says - in great seriousness - "There's a lot of options. There's a lot of options. But I think ... " - I crack up.

There's a great deal of seriousness required to answer asinine question. I am so pleased he's wasting time with such banality.

Austerity ....Austerity ....Austerity .... there I've said it . Hopefully no one has encountered a pothole lately . I dont see any progress when I see mills closing and ambulance drivers striking /unemployment lines growing...the only constant I see is austerity. .... stunned hearing some politician say we cant control electricity prices.... my thoughts are being the government you can actually set electricity prices....no enquiry needed....just do it...lol

I wonder if the + March quarter will be revised down. She'll be a long hard road getting the GDP/capita going up again.

Yes, I think it will be revised to negative or zero - I nearly made the same point.

Likewise pondering the same thing. I won't be surprised if it is.

Since the ANZ and RBNZ are both so shit at forecasting, I will split the difference: -0.3%

Humph. Anything below +1.5% is a sign of woeful mismanagement.

My concept of good and bad times is somewhat at a variance. I'm no longer in the workforce but get info from a family member who knows a person in wholesale type sales who has lost a job and also via a senior govt policy writer where a few have lost their job in that company. This dry up of govt policy work is unusual, not withstanding there was always reduced work load over change of govts spanning about a year. This time the govt policy work has definitely dried up under this current National govt. At the back of my mind is were those jobs of value to the economy? During boom times probably and now we are ostensibly at bust rather than just reduced economic activity, those jobs are gone. Is boom or bust not the case for many other countries? What is a boom or bust in economic terms? A recession but needs quantification in how deep and for how long. It maybe that a sledgehammer is required to fix inflation at the expense of of increased unemployment, rather than high unemployment, in my book > 7%, not 5.4%.

Unemployment at 5.4%. Is that so bad or are we too used to unemployment, around 4.0%+

My perception is that there were too many restaurants, cafes and bars pre-covid and during Covids the marginal ones closed and now during the downturn some more are closing.

On a recent company closure not covered much by interest, Winstone Pulp Int. Is energy cost the real reason? I suspect there were other reasons but energy costs broke the camel's back. Although generally not in favour of govt rescues and running companies such as this, would this not have been a case for temporary subsidy with oversight and conditions for a return to the profitability in a given time period?

Similarly for the Whakapapa ski field, a past section of the Ruapehu Alpine Lifts. Scant financial news on that now so back to a profitable or as a minimum no loss situation? Ruapehu Alpine lifts (the parent of Whakakpapa), seemed to have sucked up a lot of subsidy under Labour to keep it going. Too much interference by Iwi and Labour trying to accommodate by pumping excessive amounts of financial help? Suspect a lot hidden from the public by Labour. Nats any more transparent? Probably not but cutting off any subsidy will soon focus minds.

It is a difficult economic situation all round and certainly not curable by Labour. The jury is still out for the National govt but not that hopeful.

"cutting off any subsidy will soon focus minds."

Accomodation supplement. Now that would be a worth while focusing.

Accommodation supplement, WFF, any business tax subsidies, exemptions and loopholes. If a business isn't viable/profitable without tax subsidies, it's ultimately an economic drain, unless it can be proven there's a greater good benefit, which, may not be measurable in $$.

Heaps more. Free child care. ACC for sports injuries. Make Churches pay tax and rates. Auckland Cathedral sits on a 70 million block of land and pays $1000 a year in rates.

It would be interesting to see what would happen if the 2.3 billion in accommodation supplement was cut.

Combined , the 28000 listed " charities " in NZ turn over about $ 16 billion annually & pay $ 0 tax on that ... they own $ 65 billion in assets ... also completely tax free .... ahem , yesssssss !

"It would be interesting to see what would happen if the 2.3 billion in accommodation supplement was cut."

Rents would drop to realign with the market which is primarily determined by peoples ability to pay not landlords costs.

I doubt it. We would have more people sleeping in cars.

...& if WFF was eliminated, wages and salaries would increase as a similar market response. The reason National (Key) never canceled it after Labour introduced it is because its a massive taxpayer funded corporate welfare subsidy.

It's not only left wing governments that ignore the history of market interventions with unintended (?) consequences

... until they could afford to buy a place after the biggest property crash on global records.

Re Winstone - it would not have been a temporary subsidy but a long term one. The problem is structural and was not going to be fixed - NZ is simply not competitive with overseas energy prices any more, even in good times we have the most expensive energy prices, and the cost of future hedging reflected that.

As for the Ruapehu ski field - Maori have effectively hung out a giant sign saying "NZ is closed for business, thanks for coming and wasting all your money in getting here, now p*ss off". Closing a ski field for 3 days because of "the mountains hurt feelings" whilst giving a big middle finger to all those tourists who had flown into the country, paid for hotels, ski passes, and rental cars, is about as damaging to NZ's tourist industry as you can get. That place will never get back on its feet now. https://www.nzherald.co.nz/waikato-news/news/mount-ruapehu-death-local-…

Spare me KW...How about the $100 levy imposed on tourists visiting NZ ...all good with that I suppose?

Australians coming to NZ for a weekend skiing dont pay it. They'll learn their lesson, and go spend their money elsewhere.

I'm in QLD. A few parents at local school tell me they now go to Japan for Ski trips. Cheaper. More consistent conditions. Who would have thought that Japan would be a cheaper destination than An Z!!

Flying in to ski Turoa, hahahaha, ok.

Doubtful that a plant like Winstones, commissioned in the 1970s, would still be economically viable today. New Zealand needs to change our financial settings to direct savings and investment out of housing speculation and into productive industrial and commercial activity.

Of greatest worry to me is the disastrously reduced, onshore, timber processing capacity that will drive further increases in construction timber.

I'm more worried about the toilet paper!

"This dry up of govt policy work is unusual."

It hasn't dried up. The current government is letting vested interests write it.

Financial crises are always caused by a disconnect between the financial economy and the real economy. Govmt (in all western economies) should disincentivise financial asset accumulation, and incentivise actual production by all legal and democaratic means. If they don't, they will have a revolution on their hands, brought by disaffected youth. Businesses that invest their own capital in non speculative or leveraged businesses should be championed. Any normal assets that have been converted into financial assets (like housing) also need to be converted back into personal assets through financial disincentives. Show me the incentive, and I'll show you the behavior.

💯. As an example, I founded and operated a dental lab in NZ for nearly 20 years. That mistress bled me with constant investment, capital, tech upgrades, staff, compliance, increasingly impoverished patients, etc, etc. At about the same time I went into business we purchased a shit box rental. The later set and forget was a blessing, fiscally speaking! No CGT. You know the story. Looking back the incentives are all wrong.

Any normal assets that have been converted into financial assets (like housing) also need to be converted back into personal assets through financial disincentives. Show me the incentive, and I'll show you the behavior.

Well said.

The 'bottom' will be hit April-June 2025 then maybe?

It will turn when commercial landlords wake up to the fact that trying to put rent can only be a part of economic reality. To high for the times and you shut down.

Hi David, is there any chance you'll do an article on who or why we're in this mess?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.