Here are the key things you need to know before you leave work today (or if you already work from home, before you shutdown your laptop).

MORTGAGE/LOAN RATE CHANGES

There are no changes to report todays. All rates are here.

TERM DEPOSIT/SAVINGS RATE CHANGES

Nothing to report today here either. All rates less than 1 year are here, for 1-5 years, they are here.

WEAKER

June is typically a low point in the year for the retail sector, and according to Worldline (Paymark), their data shows June 2024 was unusually weak nationwide. Although they say the Matariki holiday at the end of the month provided a modest boost in some parts.

JOLT LOWER

Dairy prices fell at today's auction. The [unreliable] futures market suggested this was coming, but the fall for some products (like butter and Cheddar cheese) were very pronounced. To be fair, prices have risen steadily since February, so a reset probably should have been expected. But for the rural sector, a bump like this for dairy won't be welcomed. Analysts are no doubt checking their 2024/25 payout forecasts, but there have been no moves so far. A good way to get a perspective on today's changes are from these charts.

COVENANT WAIVER

Synlait has committed to an equity raise to sort out its parlous financial situation. Now it says its bankers have agreed to waive com loan covenant provisions until that equity raising has been completed.

GLUT & PRICES TUMBLE

Realestate.co.nz is reporting it has a huge glut of houses listed on the market (now 26 weeks worth at the current sales rate) and asking prices are tumbling. Average asking price are down $90,000 since February, Auckland is down by more than $100,000.

CAR SALES UPDATE

On Monday we noted the big year-on-year falloff in car sales. We have now updated our related charts that give a good perspective on what happened in June. The NEV drops are substantial too, and now NEV sales are little more than year ago levels now that the CCD is long gone.

BRIGHTER COMMODITY PRICES

The ANZ commodity price index lifted +1.5% in June from May as prices for dairy, meat and forestry strengthened. It is now up +7.4% for the year. In New Zealand dollar terms, the index lifted just +0.3% m/m as the NZD Trade Weighted Index rose in the month. (Of course, this is before today's dairy auction.)

CENSURE

The FMA has censured Auckland-based financial services firm deVere for failing to comply with obligations under its Financial Advice Provider (FAP) licence. DeVere provides advice on insurance, investments, and retirement planning, including KiwiSaver and UK pension transfers. The censure relates to issues concerning deVere's conduct while advising clients on UK pension transfers.

THEY BUILT IT, BUT NOBODY CAME

After spending AU$1.5 bln for the Morrison government drive to get them ready for easy switching by consumers, Aussie banks report almost no-one is using their CDR system. Worse, smaller banks say they diverted large resources to the mandated project leaving them exhausted and resource-poor to compete with the majors effectively. And now few can say why consumers should be interested in the system. The net result is that the large banks, who spent most of the money to be ready, avoided competitive challenges in the marketplace. Here the Luxon government signaled recently that they want similar 'progress' on similar systems.

REAL RETREAT

Australian retail sales in May rose far less than inflation, a situation they have had for a long time now - since the beginning of 2023. What improvements there are are coming from 'chasing bargains'.

TINY GAIN

There was a small rise in May for dwelling building permits in Australia, and a helicopter view of these trends suggests they may have passed their tough.

AUSSIE PMIs MIXED

There were two PMIs out for Australia today. The internationally-benchmarked Markit version shows their service sector growth was sustained in June. New business and activity both continued to rise, albeit at slower rates. But the AiG version for their factory sector isn't flash at all, even if it 'improved' from May.

A TOUGH BUSINESS

If you want to see the scale of construction company insolvencies in Australia, download the MSExcel files from this link. Depending on the perspective, more than 3000 Australia construction companies had to throw in the towel and be liquidated in the year to June. The squeeze between the CFMEU and the market realities makes it a very hard business to be in. If you pay off the CFMEU for 'labour peace', your customers will walk away because your prices are not commercial. And if you do, the CFMEU will be back for another bite.

MOMENTUM VANISHES I

Although its June factory PMI was stronger than the official NBS version, the Caixin services PMI was weaker, and by quite a bit. But at least it is still expanding, although the rate is its slowest since October 2023.

MOMENTUM VANISHES II

And it wasn't too different in Japan. Their service sector stalled in June, according to the latest PMI data. The volume of new business was broadly unchanged from May.

SWAP RATES NOT DOING MUCH

Wholesale swap rates are likely to be little-changed today. Our chart below will record the final positions. The 90 day bank bill rate is little-changed at 5.63%, a level it has hovered around for 120 days now. The Australian 10 year bond yield is down -1 bp from this time yesterday at 4.47%. The China 10 year bond rate is up +1 bp at 2.25%. The NZ Government 10 year bond rate is down -1 bp at 4.74% and the earlier RBNZ fix was at 4.68% and down -3 bps from yesterday. The UST 10yr yield is up +11 bps from yesterday at 4.45%. Their 2yr is now at 4.76%, so the curve is much less inverted at -31 bps.

EQUITIES MOSTLY POSITIVE

The NZX50 is little-changed in late trade. But the ASX200 is up a minor +0.2% in afternoon trade. Tokyo is up +0.9% at its open. Hong Kong is up +0.3%, but Shanghai is down -0.5% to open their week. Singapore is the star today, up +1.3%. The S&P500 was up +0.6% in their Tuesday trade on Wall Street.

OIL LITTLE-CHANGED

The oil price is down -50 USc at US$82.50/bbl in the US, and still at US$86.50/bbl for the international Brent price.

GOLD SOFTISH

In early Asian trade, gold is softish since this time yesterday, down another +US$5 at US$2327/oz.

NZD FIRMISH

The Kiwi dollar is a little firmer from this time yesterday, now at 60.8 USc. Against the Aussie we are unchanged at 91.1 AUc. Against the euro we up +20 bps at 56.6 euro cents. This all means the TWI-5 is up +20 bps at 70.3.

BITCOIN RETREATS

The bitcoin price has fallen -2.4% from this time yesterday, now at US$61,468. Volatility of the past 24 hours has been modest at just over +/- 1.5%.

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

This soil moisture chart is animated here.

Keep abreast of upcoming events by following our Economic Calendar here ».

90 Comments

Ford ranger number 1 last month. Two different utes made the top three vehicle sales

All those accountants buying up large ah..?

Don't worry Simeon is making some secret changes to allow more smokey old bangers into the country...gotta keep this donars happy

Tesla grumpy only ‘handpicked allies of the current Government’ consulted on secretive attempt to water down emissions standard.

The Government is quietly reviewing the emissions standards for the vehicles car companies import into New Zealand, although it is not keen to publicise the changes or consult on them very widely.

I cant afford a Ford, unford-tunately

Fixed Or Repaired Daily

No! First On Race Day

Found On Road Dead

Then there was the Ever Rest model.

F**ked on Rainy Days

I scored one cheap and totally by accident. Was my favourite and longest owned car out of the many I've experienced. A '77 Falcon, daily driver and slow project over 11 years, until she did become a little unaffordable for me to continue with.

I think that is the data that the RBNZ sets the OCR on. While Ranger is number 1, OCR must increase.

"New vehicles sales declined for the fourth consecutive month in June: 9423 registrations represents the lowest sales for the month in over a decade.Year-to-date, 2024 is 26% down on 2023 and 24% lower than 2022.The top selling vehicles overall were Ford Ranger (889), Toyota Hilux (591) and Toyota RAV4 (556).Following the RAV4 as the top passenger vehicles were Mitsubishi Outlander (255) and Mitsubishi ASX (252). The RAV4 was naturally also the top hybrid (all models sold in NZ are petrol-electric), followed by Toyota Highlander (153) and the Suzuki Swift mild hybrid (135)."

Higher (suspensions) For Longer

All that fuel will be hurting our trade deficits for years to come.

Homeowners may be forced to sell if rates rise confirmed - council staff

The leaders said while inflation at the supermarket checkout was up 19 percent since 2020, since the council prepared its last LTP capital costs were up 25 percent and civil construction costs up 27 percent.

At local council service centre last month. Elderly lady before me in queue distressed at cost of present rates and prospect of near to 10% rise. Flat answer from staffer. You need a reverse mortgage. Firstly that is advice from an inappropriate individual but it occurred to me is it then something of a freudian slip whereby the council has realised that with the rate payer’s houses recent rapid rise in value, that extra equity is ripe for the picking. Just idle conspiracy theory, of course.

Wonder how council late fees stack up against a reverse mortgage rate? Probably not a move a little old lady might consider though.

Not like a little old lady, Texas style then. Stopped for a dud brake light, the officer issued a 10 day notice for repair and from her licence noted she was able to carry a concealed weapon and did she have any with her. “Why yes officer, I have a snub nose Colt 38 in the glovebox, a Walther P35 automatic in the console, a Smith & Wesson 5 chamber 32 in my purse and in the trunk a side by side 12 Guage pump action shotgun.” Said the officer , “my god my good lady what on earth are you frightened of?” Said she, “not a thing officer, not a f…king thing!”

Haha. So many movies have an ending where the good guy is disarmed. Only to pull out a second weapon and blow the baddies head off...

I think some councils allow elderly owners to delay their rates bills, and take the money owing from their estate/eventual property sale? Presumably including some interest and/or fees.

I wonder what happens if the elderly are forced to take out reverse mortgages and then, as a result of ill health, are forced into assisted living. My neighbour had to sell her home quickly to get a room in a care facility, but thankfully owned her home outright. Serious question.

And remember that reverse mortgage interest rates are really high so the equity falls very quickly.

Yes, 10.5% at the moment.

In Australia, the Government provides reverse mortgage financing. Just wait until Councils' cotton on to that as a new business opportunity.

Councils in NZ already allow rates suspension until sale (or death).

It's entirely understandable that heavily burdened owner/occupiers and portfolio holders will be examining their options in light of galloping insurance and rates burden. It's simply another reason to expect more property to add to the existing market glut. This downturn certainly has legs and will take considerable time to play out.

100% this. I'm re-examining my options because I could save thousands a year by moving to Australia where rates are about a 1/4 of what they are here.

Replaced by capital gains and stamp duty...

I have made this point several times. Council rates go up much more than CPI because they don't sell deflationary imported stuff. Building anything is so much dearer now.

Which in Auckland means that Len Brown and John Key should hang their heads in shame regarding the train tunnel.

Correct, JK should have funded it 100% like the RONs and left it off the council books.

You mean put it on the back of the tax paying working poor around the country, rather than the wealthy Auckland asset holders who would actually benefit from it?

You mean like Transmission Gully, Waikato Expressway, Kaikoura SH1 rebuild etc? Yes. All 100% funded from tax, not the local councils.

Those are all parts of national highway 1 and come under NZTA's ownership, therefore have to be funded by taxpayers!

CRL is an Auckland Transport project.

Auckland has been ignored for years...just look at the crappy bridge we have over the harbour...if only we had listened to dear old Robbie

The good folk of Kaitaia may disagree with you.

No, it's delivered by CRL Limited, of which Crown has the quorum on the Board.

They also have a monopoly.

I wonder how this all resolves itself. In an abstract sense I guess it acts a little bit like a capital gains tax, so if the net result is that homeowner equity growth gets partially diverted from Ford Rangers to local infrastructure it might help the long term prospects of the country. But it's the politics that I can figure out. Will property owners pay up or vote for lower rates and less investment? Will the additional rates go towards capex or be consumed by opex bloat?

Rate payers are doing it tough. (But they just keep on giving.)

https://www.stuff.co.nz/nz-news/350291538/active-hub-gets-green-light-a…

The New Plymouth District Council has given the green light to the Tūparikino Active Community Hub and lifted its budget to $50 million.

After years of design changes, a planning pause and large scale public debate, the hub was finally given the go-ahead on the first day of the council’s Long Term Plan deliberations on Monday.

Councillors spoken to after the hub was approved said they had expected to be voting on spending $35m towards a four to six court indoor stadium, money that had already been budgeted for in the last Long Term Plan.

Anyone who is bullish at present or risk taking be warned…US Shiller CAPE (cyclically adjusted price:earnings ratio) show that American companies are now as overvalued as they were in 1929. 2000 is the only other worse time in the past 100 years to buy stocks.

https://x.com/paulclaireaux/status/1748259710644425126?s=46&t=MUwQeKa7M…

https://x.com/norbertkeimling/status/1612412006484557824?s=46&t=MUwQeKa…

I’d be very cautious about buying shares the next 12 months or having an aggressive KiwiSaver if you’re near retirement and can’t afford to lose $$ (not specific financial advice…). The CAPE has been a good indicator of poor future sharemarket performance.

IREN (data centers powered by 100% renewable energy) is up 279% since Feb. Easier to say in hindsight, but I wish I'd put more chips on the table.

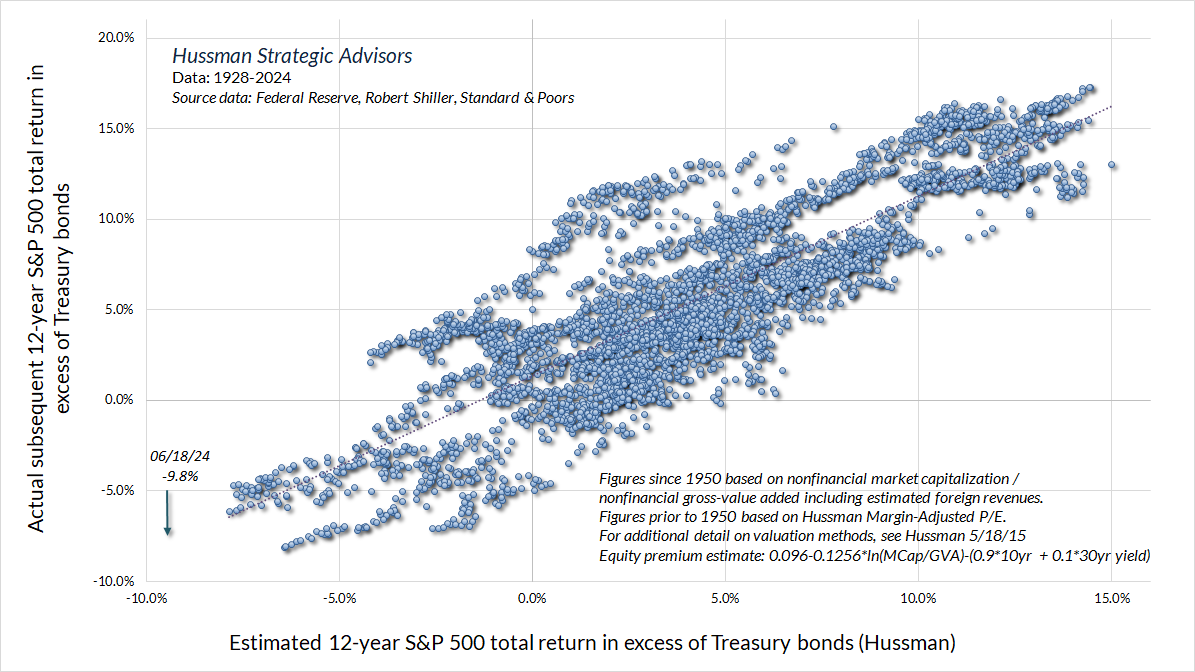

To put the current valuation extreme in perspective, the chart below shows our estimate of 12-year S&P 500 total returns over and above Treasury yields. This is the most reliable estimate of the “equity risk premium” that we have examined or developed, and is better correlated with actual subsequent outcomes than the “Fed Model” (S&P 500 operating earnings yield – 10 year Treasury yield), the “Excess CAPE Yield” of Shiller, Black, and Jirav, and annual estimates produced by Aswath Damodaran, all whose work I admire even when I might disagree. Link

{kind=link}

Yes Hussman has some interesting work on Twitter/X

There were probably no controls on companies or lending in the 1920s. I think the SEC was created following the collapse. Everyone was borrowing and buying the latest vehicles (eg 1928 Model A) and many products. It was a fantastic time technologically and socially.

Interestingly we still have the same problem today. I know of many companies investing in AI not because they have a use case, but just because they feel like they have to.

In 1929 buying stocks was entirely Discretionary . Reason markets keep inflating is now 100 years later Tens of Billions of Average Joes payroll is automatically collected in Kiwi Savers and IRA's etc around the world and hurled at the Market. All that money coming out of Payrolls each month needs to find stocks to buy indirectly through Index Funds. It's the reason Bitcoin keeps trucking along now. Each month more Index Fund money thrown at it.

Funnily enough I had just revisited the 29' crash prior to seeing your post. That dreaded inverted yield curve that is never wrong vs the long delay period does not paint a pretty picture. The dream of lower interest rates showing soon is likely sliding further away . That soft landing might get a little get bumpy fingers crossed the wheels stay on.....lol

Luke Gromen says that if there is a USD crisis, the price gold should rise 19x to match the price level it was at in 1980 relative to foreign treasuries outstanding. So a prices of approx USD $42k. He also points out that the gold price should increase 3x-6x to get back to long-term average.

19x?

yeah it feels like its going to go

Gold is sooo old school. It'll end up in crypto. (Although some will end up in gold.)

It's about time we got a top Scottish economist to manage our economy:

Such a shame what is happening to Hong Kong now.

Most people – ‘all but the well-to-do’ – paid no income tax at all. Even higher earners only paid 15 per cent. There were no tariffs or duties, no sales taxes or VAT, no taxes on capital gains, on interest or on overseas earnings. But there was a land value tax.

Sounds like my kind of guy!

Thoughts on this market view?

‘Japan's yield curve is going parabolic. As soon as they start dumping U.S. treasuries to prevent their currency from collapsing, the U.S. yield curve goes parabolic as well’

https://x.com/financelancelot/status/1808194524012790272?s=46&t=MUwQeKa…

Solid thesis. Thanks for pointing out. Only swap line shenanigans seem to be the answer.

Thanks farmers.

The latest Ministry for Primary Industries update (Situation and Outlook June 2024) reported that the primary sector is responsible for 80.9% of merchandise exports and brought $54.6 billion dollars into the New Zealand economy (forecast for the year to June 30th 2024). Of that, $35.6 billion was from dairy and drystock – 65.2% of the export economy.

https://www.ruralnewsgroup.co.nz/rural-news/rural-opinion/pastoral-farm…

Profile could you give us the figures after import costs have been deducted?

Who's imports?

Most of the inputs are water, wind, soil, and sunlight. Those are mostly still free.

What about the outputs? Poos, farts, wees, all screwing over the environment. Mostly still free too

You can farm responsibly.

Unless we're going to decide we're not allowed to externalise any of our costs anymore.

Fact is we're not that good at doing much else for export at scale, never have been. It's all odds and sods, and the few big winners end up outgrowing NZs population and capital market.

We definitely don't use enough good science to get the best out of our natural advantages anyway. I'd give us maybe 6/10.

"You can farm responsibly" - so I guess we can charge a decent rate for those outputs then

We sort of get premiums for some of what we produce on that basis.

Nek minnut

"Hey wha's ma milk done got expensive".

There's farming responsibly, and then there's farming "economically"....

Oh right...no Tractors, Utes, Diesel, fertiliser, palm kernels, or cheap imported labour.... gotcha

Many farms are profitable and that net profit is domestically generated.

It'd sorta be like invalidating your bank balance on the basis you buy Chinese clothes because they're cheaper.

Youl lost me there..too much nitrates in your local water?

I'm trying to work your angle.

Do you think our primary producers consume more imported goods than they generate?

A decent farm should be a profit generating exercise. That means, they're selling something for more than the cost to produce it. So there's clearly a net gain (presumably, otherwise the farm goes under).

I farm (not animals mind). I'd probably put the cost of imported goods (fuel, machinery, fertiliser) at maybe 15%. Dairy I couldn't say, probably higher if they're importing feed.

As a dairy farmer. Our cost of imported goods are only about 8% of income.

I don’t think you realise what New Zealand looks like if we were heavily dependent on agriculture and net zero. Don’t let perfection get in the way of the good.

I have an imported machine running on fossil fuel that does in an hour what used to take 10 people a couple of days.

Did I improve productivity?

I hope it’s not a sex doll

A diesel powered sex doll!

Avoid the exhaust

You wouldn't want to put your old fella into it.

Especially, daresay, if your big end had already been blown.

Where would you be without your gumboots

Regarding farm machinery, it pretty much impossible to do a fraction of the work a tractor does.

Saw an electric tractor at fieldays, much cheaper to run than diesel, next time you need a new asset, look it up :)

Imported fertilizer is what powers the Ag economy.

How hard would it be to change your business to another bank? I have no idea why this process needs to be made "easier".

Depends on the hook ups in place to secure the collateral if there is financing in place. For instance, guarantees by directors and/or third parties, mortgages on subject property or an alternative. All that legalised for one bank has to be unwound and reset for another bank and that involves costly lawyers.

‘Weight of the top 10 stocks in the S&P 500 has spiked to ~34%, the most in the entire history.

At the same time the weight of the LARGEST stock of the S&P 500 relative to the 75th percentile stock is 770x!

This is even higher than in the 1920s’

https://x.com/globalmktobserv/status/1808131007096205375?s=46&t=MUwQeKa…

Feeling a tad bearish today, IO? (I share your view.)

Take a look at what happens if markets start falling and boomers all decide to cash out of their pension funds. 1929 will look like a picnic.

Economic analysis prepared for Auckland Transport shows massive benefit-cost ratio of 9.0 for permanently lowering speed limits around schools.

@SimeonBrownMP's proposed approach has BCR of 0.2 and 500 more kids in hospitals and coffins over next 10 years.

Back on Track.

When the evidence conflicts with your ideology and tiny brain just go with feels and reckons, aye Simeon.

AT should increase the speed limit outside his house to 150 kmh, I’m sure he’d love the time savings.

Just get the kids on School Patrol around school to expand their reach to more nearby road crossings, and save 500 kids.

Cheap labour--problem solved.

And if anyone is interested in how out of whack this coalition's transport policy is with Aucklander's transport aspirations this post sums things up nicely.

https://www.greaterauckland.org.nz/2024/07/03/gps-vs-rltp-government-ou…

“Of the $22b, $13.8b is forecast to come from fuel excise duty, road-user charges and other fees“ - but hang on, I thought fuel excise was subsidising a handful of cycle lanes. I guess now National have cut those we’ll see a $10 billion reduction in transport costs?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.