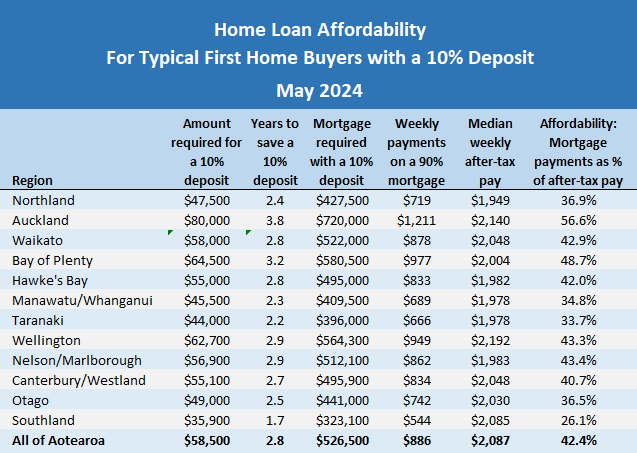

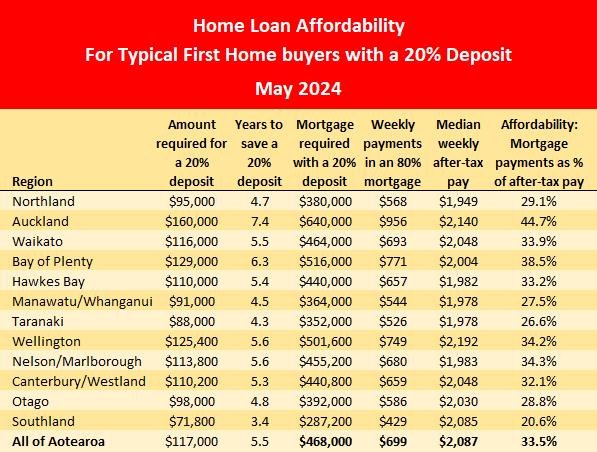

Housing affordability appears to be in a period of relative stability for first home buyers, with only slight changes in the main drivers of affordability, according to interest.co.nz's latest Home Loan Affordability Report.

There have been small monthly movements in the Real Estate Institute of New Zealand's lower quartile house price, but it has remained within the fairly narrow range of $570,000 to $600,000 since March last year.

That's still well down form the peak of $670,000 achieved in November 2021, but for the time being at least it appears prices at the bottom of the market are relatively stable.

Mortgage interest rates are also showing only small, incremental changes, with the average of the two year fixed rates charged by the main banks declining from a recent peak of 7.04% in November last year, to 6.74% in May this year, putting it back where it was in July last year.

That means mortgage payments on a home purchased at the REINZ's lower quartile price with a 10% deposit have increased by a mere $13 a week over the last year, from $873 a week in June last year to $886 in May this year.

If the same home was purchased with a 20% deposit, the difference in mortgage payments over the last 12 months would be just $11 a week, rising from $688 in June last year to $699 in May this year.

The one area which has shown some significant movement over the last year or so is after-tax income, which has risen relatively strongly.

Interest.co.nz estimates the median after-tax pay for couples aged 25-29 who were both working full time was increasing steadily by about $10 a month throughout 2022 and 2023, but slowed to an average of just a couple of dollars a month this year.

The means the average estimated take home pay for typical first home buyers increased from $2002 a week for a couple in May last year, the first time it has risen above $2000, to $2087 in May this year, which would have helped with mortgage affordability.

However most of that increase in after-tax pay occurred last year and incomes are now also flattening out.

What all of this suggests is we are in a period of relative stability in terms of affordability for first home buyers. So those who can afford to buy are unlikely to be disadvantaged by taking their time to find the property best suiting their needs.

However, those who can afford to buy their own own home will probably be highly paid, because home ownership remains unaffordable for aspiring first home buyers on average pay in most parts of the country. But at least it's not getting any worse.

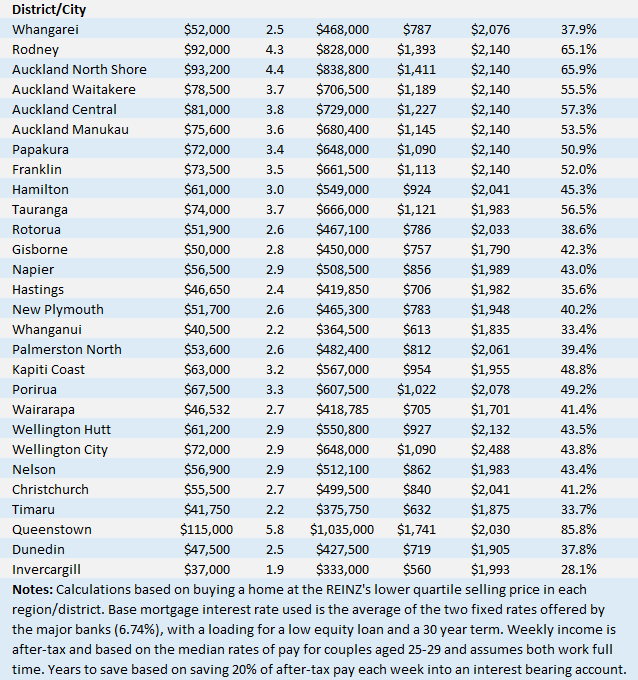

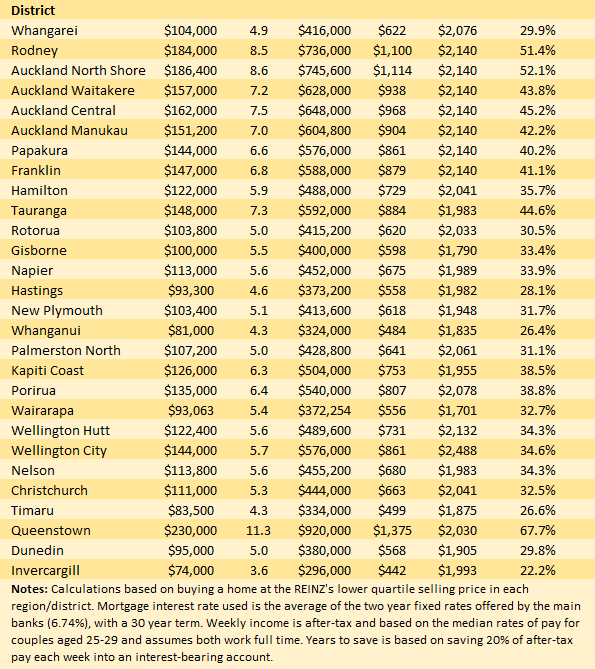

The tables below give the main affordability measures for first home buyers with either a 10% or 20% deposit, in most of the main urban areas around the country.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

69 Comments

"it's not getting any worse"

That unemployment thing is coming at ya!

So are lower interest rates

Even interest at 0% - banks will look at you more than twice if your job is at risk!

Fair enough. Though the current unemployment rate is 4.3%. The most doom forecast is for it to go up to 5.1%. As tough as it will be for those laid off, it is unlikely to be a notable blip on house prices.

When they changed the criteria as to what was classed as 'unemployed' it ceased to be a great measure.

This one might be better ... https://www.stats.govt.nz/indicators/underutilisation-rate/

Do not worry sir.

Glass half full: Keep your focus on the US. As soon as it really starts to unravel, you're going to see central bank action like you've never seen before in history. Everything is underwritten now.

Glass half empty: You cannot imagine.

GLASS has been knocked over:

On a positive side all those banks holding low interest rate treasuries will all be made good as rates collapse again....

but they will suffer bigger CRE losses for sure.

If they are made worse its game over for so many US smaller banks.

There is no end to CB F&%kery, they could take rates negative this time instead of ZIRP and QE, of course money could flee to BTC and Gold.... imagine negative interest rates, your mortgage could be paying itself off.....

If they are made worse its game over for so many US smaller banks.

Not sure I agree with you. Arguably many of these banks should be under already. It cannot happen.

they can fix liquidity by reopening the repo window at face value of treasuries, BUT they CANNOT fix capital adequacy as CRE losses are realised.... solution, make up some scheme where there is no mark to market of CRE loans..... look there is just no limit......

The system fails when and enough enough people who have cash decide to withdraw it from the system.... as its swift controlled they can probably even game this... Buy the time you start to notice there is an issue its already to late for the man on the street, by then CBs too busy trying to stop the derivatives meltdown, where ever possible they will avoid things being in default, even if its laughable to everyone but themselves.

they hate privately held physical gold as it destroys banks balance sheets. BTC is the same.

by then CBs too busy trying to stop the derivatives meltdown

This is the known unknown. Good work on pointing that out. All we can really know about this is that we don't know the how, when, and why.

imagine negative interest rates, your mortgage could be paying itself off

And you'd pay the bank (even more) for the pleasure of holding your savings. Borrow to the moon, baby! And hold that cash!

I'm getting a brain ache just thinking about it.

File it under the NO DEFAULTS section of crazy shite.... you know that the RBNZ made all the major NZ banks change there systems so they could cope with negative interest rates about 3 years ago....

Yep, which makes me think it would make all the OBR work and rehearsals a waste of time too. If you wanted to stabilise your bank you'd just lend a tourbillon* dollars to every NINJA-qualified prospective customer and hey presto, "stable" again!

I think. I need a Panadol.

*Hat tip: Bugatti.

Michael Reddell at croakingcassandra did a number of posts on negative interest rates at the time;

https://croakingcassandra.com/?s=negative+interest+rates

what will central banks do?

Like always, lie and make shite up... see negative rates above.

I think it’s just as possible that we see high inflation for decades as it is that we see sustained deflation/low/negative rates.

Yes Central bankers would rather inflate away past debt then deal with deflation.... even at 3% for twenty years ..... I just think that the next crisis is going to be bigger then the last, and that was a doozey that required international co-operation via QE and stimulus to resolve....

this next one is going to be almost every many for himself, China and Russia not going to want to help. In fact of all countries probably Russia can handle hardship better....

The deprivation they endured in the neoliberal 1990s is barely possible to imagine, from collapsing life expectancy to skyrocketing alcoholism and HIV rates. Every middle aged Russian in the Moscow power structure today came of age during that Chicago school fueled nightmare. And they are determined to never let anything like that happen to the nation again.

Why? Debt isn’t their mandate.

They’re not going to cut until they hit 2%. Otherwise their credibility in respect to that target is gone

what will central banks do?

You mean what 'did' they do. Research BTFP. You're not going to read about it in Granny Herald.

Anyway, the Fed can add liquidity without calling it money printing. Trust me.

I wonder why some quite big FX Swap lines are already in place...... between CBs

I wonder why some quite big FX Swap lines are already in place...... between CBs

In place since the GFC. Were never dropped.

https://www.federalreserve.gov/newsevents/pressreleases/swap-lines-faqs…

The Reserve Bank has re-established a temporary USD swap line with the US Federal Reserve. This will support the provision of USD liquidity to the New Zealand market, in an amount up to USD 30 billion. This is a facility that is being offered to many other central banks globally.

That was 20 March 2020, so yeah very temporary......

That was 20 March 2020, so yeah very temporary......

Swap lines were never removed from 2013.

my point is that they dont actually have any room to manouvre left.

They cant move the ocr wildly or print money without causing local or imported inflation or the economy to weaken.

I see RFK Jr is saying, that if elected, will couple the USD to a Bitcoin standard to prevent the Fed causing a domestic (and international) meltdown when the next financial crisis hits.

He can see the damage the Fed has been causing through its seemingly endless devaluation of the dollar to fund its global wars and the military industrial complex.

And enter preventable economic depressions? This is really fringe stuff.

We should all be grateful to the US dollar and its military industrial complex for the stability it has afforded us over the past few decades. You think our neighbours in the pacific would’ve just left us and our trade routes alone?

I was told (did not hear it myself) that Trump is promising no income tax - that government revenue will be replaced by massive tariffs on imported goods.

Won't happen.

Those who get themselves over-indebted are always at risk - and can soon create headaches for their creditors.

By all means buy a property that suits your needs - especially while the housing cycle is at a low point. In my view, however, you ought to factor into your purchase decision that mortgage interest rates will remain around their current level for at least another two years........ Inflation is not falling as quickly as foreseen by many. Further, RBNZ has an iron-clad mandate to deal with the issue - and won't have too much mercy for those who have landed themselves donkey-deep in debt. Economic stability is the name of the game. And rightly so. (Edit 1)

TTP

What makes you think inflation is not falling away? It's 1.1% over the last 6 months or 2.2% annualized.

I wouldn't be surprised if we saw OCR cuts in October.

What evidence are you using to suggest that homeowners are saving 20% of their after-tax pay every week?

It’s a big call given the cost of living in this country. And then you factor in many young people in their 20s have hefty student loans. I guess it’s possible if you live like a monk.

It’s also assuming the income of ‘a couple’ rather than an individual. I would suggest there’s plenty of young de facto couples who manage their finances individually. There’s also plenty of single people.

"What all of this suggests is we are in a period of relative stability in terms of affordability for first home buyers"

Prices are stable like a level and flat line. A floor if you will...

🤣😆priceless! How did you deduce that Baptist?

Because it's stated in the article! RP, you like to mock Baptist, but his comments make much more sense than yours.

more like a glass ceiling hence so many are leaving the country.

oh dear, really...housing is not for young people or first home buyers. It's important they get out of the way of the speculators so they can increase our housing supply.

Happy to sit and wait and watch this stable market…….. until it’s not.

Median Multiples | interest.co.nz

You can see How the median multiples are stabilizing, but the fall is artificially low in some areas as it has been influenced by the number of smaller apartments coming to market.

However, landbanking prices have largely not been affected precisely because they are landbanked and are not being sold.

It's this monopoly the Govt. needs to break to see any real effect down to better median multiples.

What do you mean “artificially low”? Supply responding to demand is as natural as it gets. The real artificial influence here is land use restrictions which are artificially propping up prices. Without these, prices naturally settle around 3x incomes.

I mean that a greater proportion of small houses (apartments) coming onto the market, giving the impression that houses on a like-for-like comparison over time have become more affordable.

The supply naturally responding to demand is only true in a truly free market, which this is not, thus this present system is also an artificial supply typology response to what the market would really prefer if the prices were more affordable.

The irony of course is the reason for so many more smaller apartments, is to make them more affordable due, to what you correctly say, the artificially high land prices.

This is the same distortion you get with the median multiple when the original definition of household income was one working partner. Now that can easily be two income equivalents, or more. ie it underestimates the unaffordability issue.

The median multiple is a very good measure of affordability, but you still need to know the nuances of it.

Okay, fair call on all counts.

sadly too true it is too easy to fudge the numbers to make things seem affordable but it is hard to raise a family with kids in a 1bedroom apartment on a single income (or even a smaller 2 bedroom townhouse with no land and stair only entry). Throwing in more incomes to the "household" was one way to massively fudge the numbers, now it often requires 2+ incomes since most FHB or those wanting to buy are on below average salaries (most don't get the perks of wage growth each year outside bare minimums).

Take home pay for a couple in their mid to late twenties of over $2,000pw. I wonder what percentage of people in that age group are actually in that situation?

Yea, would be interesting to know the stats for that age group.

I think the median weekly wage for 25-29 year olds (based on 2023 stats) is about $1140 p/w. Based on that it might not be too stupid to presume that a median couple (in the age group, that's actually getting some income) might be making about $2280 pw before tax and just under 2k ($1860) after tax in 2023.

Incomes have gone up in 2024, so it's possible that the median income for a couple in that age group (that's making some income) might be roughly about 2k now (median implying that about 50% make more and 50% make less). A lot of assumptions here of course - not "true" stats, lol:)

Nice. I presume those income figures are for full time workers only. One thing to consider is the percentage of 25 to 29 year olds who are in education or only in part time employment and might fall outside those numbers.

Stable, is that because the low rate fueled stupidity has stopped...?

Stable like the top of a sine wave.

Do you really mean that? If so, what goes down, must come up.

Auckland market I hear is a real battle for people and for first home buyers it is indeed pretty tough, due to the servicing criteria of around 9%.

Christchurch market is ticking along reasonably well and not seeing prices dropping, just fewer buyers around.

Opportunities always around and not the doom and gloom down here!

"Opportunities always around and not the doom and gloom down here!"

For property traders, developers, and other specialists in property industry they will always be seeking profitable opportunities - that is the nature of their profit seeking business.

Very different for owner occupier buyers who are not interested in getting into the property business. Most commenters are referring to this audience.

1.7 million disagree with him. Christchurch is small and slow for good reasons. It does punch above its weight in terms of serious crime though.

Happiest city in NZ ex Agent.

I do not see the serious crime that you suggest?

If you would stop sending down people that are sick and tired of the North, there wouldnt be the crime that I do not see!

At the end of the day, we all have choice and Opportunities away from crime is massive in ChCh!

You conveniently forget to mention all the people who left poor old Christchurch after the quakes. They escaped to places of safety throughout NZ and the remainder of the world. It must be bad down there if you have to try to convince us and yourself how good it is.

Sounds like someone has a bee in their bonnet and no idea of what is going on in Christchurch.

Of course there were heaps that left ChCh.

The quakes werent flash for Chch but the ones that stayed have turned it into the happiest city in NZ.

People like different things EX Agent, and if people like to live in less happy cities like Auckland then that is their choice.

We actually do not need anymore people coming into Chch as all it does is push up rents and our property prices, making us more money!

Interesting to make the comparison with October 2021.

Some locations have become even more unaffordable (as represented by mortgage payment percentage of after tax income)

yes housing often gains more than the median income which if sold regularly say moving investment assets around can generate more cash so there is no need to work. It does help to pick an area with good due diligence though.

When hasn't New Zealand housing been ranked as severely unaffordable? It's nice to hear though that unaffordability has, however temporarily, plateaued at base camp.

The reality is that Australian cities are far more expensive than NZ!

people that think they are going to better off in Australia are probably be in for a shock.

We know several that are living over there and they are saying basically the same things as we are.

You only need to look up the current median prices over there, and look at the property for sale sites like Domain and I would not think you would be leaving NZ for Australia for cheaper homes!

No NZ is not great at the moment due to our last 6 years if Government mismanagement, and there is a lot of financial strife out there, however things are going to improve.

The world just can not have these Leftist Governments controlling countries again, it just not work!

I think that you have used a fixed income rates across NZ in the affordability calculations.

I don't think this makes too much sense. ie In Invercargill or Whangarei for example, pay rates are not very generous compared to Auckland or Wellington. That is why house prices are lower there.

Time to heavily tax the groups that own most of the property. Put it back into hospitals, schools etc..social housing.

Government has no problem wasting a billion dollars on initiatives which harm the wellbeing and resilience of the nation. Do you think that they would have any problem wasting ten billion dollars on the same thing?

Yes it's wasteful. Terrible (sarcasm).

Ok so what if it's wasteful, it's going into the pocket of landlord leeches atm so it may as well have been lit on fire, fuckem put it into something useful for everyone rather than a new ute or yet another boat for some entitled boomer.

It's about to happen at a local government level.

A very honest and compelling article in One Roof today about breaking the social contract with the younger generation with house prices and home to income ratios increased dramatically in the last decade. The solution is no doubt complex, multifaceted and interlinked but the ones that spring to mind for me are:

Councils freeing up land for housing outside town boundries and more intensive within

Monopolies and duopolies in housing materials overcharging - needs a disruptor

Flawed economics with credit creation and poor performance with our Reserve bank - now we have to contend with Stagflation with increased prices and decreasing GDP per capita

For One Roof to be saying that it is the pot calling the kettle black.

One Roof's business model is to help properties churn, FOMO etc.

Introducing the things you mention, which are good, and are simpler than what people, through their own self-vested ignorance, have you believe, would stabilize the market over time, and severely reduce the need for the number of RE Agents, and the volume of media advertising One Roof relies on.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.