This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing a guest Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Rod Emmerson’s cartoons: Week of June 3 - 9 https://t.co/SXJfrzO8tY pic.twitter.com/QJuTJ4zO3p

— Rod Emmerson (@rodemmerson) June 5, 2024

1) Ripping you off in the age of recoupment.

With inflation surging as the worst of the Covid-19 pandemic passed, debate emerged over what contribution profit-led inflation, that is companies raising prices, was making. Isabella Weber, Assistant Professor of Economics at the University of Massachusetts Amherst, did some interesting work in this area, which she calls sellers' inflation, and featured in a previous Top 5.

In our Of Interest podcast I also spoke with UBS Chief Economist Paul Donovan on what profit-led inflation is, how it happens and how to combat it. And in another podcast, Reserve Bank Governor Adrian Orr told me profit-led inflation had been happening in NZ, just as it had overseas.

Now, in The American Prospect, David Dayen and Lindsay Owens have an interesting article arguing increasing prices is the new corporate mantra, replacing cost cutting.

Dayen and Owens say starting in the late 1970s institutional, or professional, investors began demanding companies cut costs to boost profits for shareholders. Mass layoffs followed with, for example, one out of every four General Electric employees laid off between 1980 and 1985. Unions were busted, jobs and manufacturing were shipped overseas and supply chains were outsourced.

Zero-based budgeting studied every sheaf of paper, every thumbtack, and slashed budgets annually. This was seen as an unavoidable strategy to become “competitive” in corporate America.

Even after the Great Recession, companies didn’t try to make up for lower overall demand by raising prices, instead viciously suppressing wages. Between 2009 and 2012, labor costs fell, and corporations maintained their margins by reducing workers’ share of the profits.

The results can be seen in ruined industrial ghost towns across the [US] Midwest, and businesses strip-mined by leveraged buyouts. But there is a tipping point to all this cost-cutting. There’s only so much fat to cut before you hit bone. The strategy eventually had diminishing returns, and without a new strategy, profits would hit a plateau. That wouldn’t cut it on Wall Street.

Enter the age of recoupment. Instead of cutting costs, the new mantra is raising prices.

Price hikes are old as dirt. But today’s companies have reinvented them. They’re using a dizzying array of sophisticated and deceitful tricks to do something pretty darn simple: rip you off.

The new tricks have fancy new names. Charging you more for less is a corporate practice known as “shrinkflation.” Revealing part of the total price up front, only to tack on all manner of ridiculous-sounding fees and service charges: Industry insiders call that one “drip pricing.” Stealing your online shopping data to predict the maximum price you would be willing to pay for your next e-commerce purchase: That’s personalized pricing. Using software to coordinate pricing with other companies to make sure they don’t undercut each other: That’s algorithmic price-fixing (or plain old-fashioned collusion). And charging you more for an item when supply is limited: That’s Jay Powell’s favorite, dynamic pricing.

Three critical factors have come together to make recoupment work. None of them are necessarily new, but they have become more finely honed, more ubiquitous, and importantly more interconnected, achieving what you might call a perfect storm for pricing.

Dayen and Owens give a range of examples from specific industries and individual companies. Technology, they say, is playing a not insignificant role.

Landlords are quietly utilizing new software to band together and raise rents. Uber has been accused of raising the price of rides when a customer’s phone battery is drained. Ticketmaster layers on additional fees as you move through the process of securing seats to your favorite artist’s upcoming show. Amazon’s secret pricing algorithm, code-named “Project Nessie,” was designed to identify products where it could raise prices, on the expectation that competitors would follow suit. Companies are forcing you into monthly subscriptions for a tube of toothpaste. Banks have crept up the price of credit, so customers who cannot afford price-gouging in their everyday transactions get a second round of price-gouging when they put purchases on credit. Expedia is using demographic and purchase history data to set hotel pricing for an audience of one: you.

I'd love to hear what readers are noticing, especially here in New Zealand. Are you being ripped off in the age of recoupment?

2) How corporations learned the maximum amount they can charge for a product.

Bloomberg's excellent Odd Lots podcast has a new episode that follows on nicely from The American Prospect article. That's because in it, hosts Joe Wisenthal and Tracy Alloway speak with Dayen and Owens.

Dayen and Owens raise numerous interesting issues including about data privacy, the burgeoning industry of algorithmic pricing companies, consumer rights and whether law changes could be needed, competition and market power, personalised pricing, using confusion and complexity as marketing tools, and a return to haggling.

Here's the description of the episode.

What's the price of a hamburger? Well, it depends. Are you making the purchase on the spot? Did you order ahead using an app? Are you a frequent customer of the burger chain? With inflation having surged at the fastest rate in roughly four decades, there's suddenly a lot more interest in how companies figure out the most that they can charge you for a given purchase at that moment in time. As it turns out, much of the economy is becoming like the airline industry, where there is no one price for a good, but rather a complex range of factors that go into what you're willing to pay. Thanks to algorithms, apps, personalized data, and a bevy of ancillary revenues, companies are increasingly learning how to not leave any pennies on the table. So how did this come about? What exactly is happening? And when did everything become gamified? On this episode we speak with Lindsay Owens, executive director of the Groundwork Collaborative, and David Dayen, the executive editor of The American Prospect. The two of them have put together a special episode of the magazine that's all about the world of pricing strategies, the tools companies use, and the industries that exist to help companies figure out what they can charge. We discuss what they learned and the impact this is having on the economy.

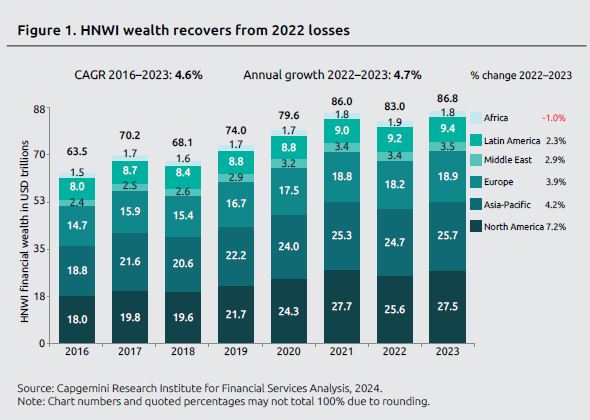

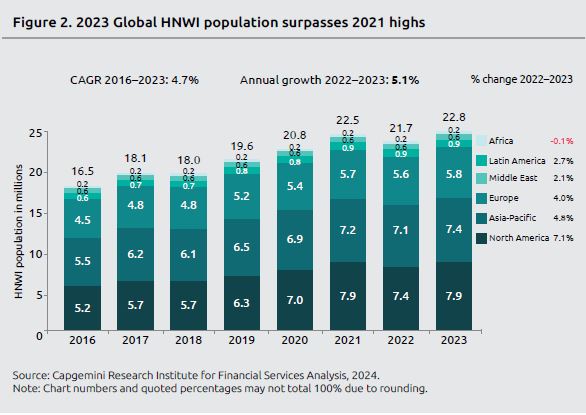

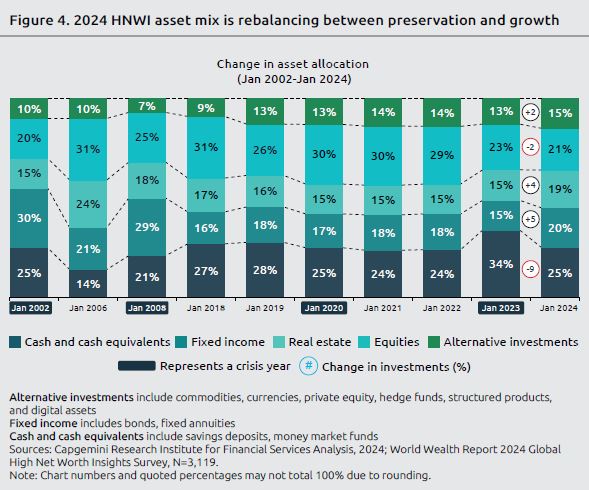

3) What high-net-worth individuals are investing in.

Capgemini issued the 28th version of its annual World Wealth Report this week. In it Capgemini's Anirban Bose says high-net-worth individuals (HNWIs) are reaching unprecedented numbers and wealth levels. And as their wealth grows, their risk aversion is subsiding, as they "slowly rebalance between safety and growth."

New Zealand doesn't get a mention in the report, which surveyed 3,119 high-net-worth people around the world. Two out of three are planning to invest more in private equity this year. Private credit is "highly sought" to meet long-term return expectations while overcoming short-term market fluctuations.

HNWIs are people with investable assets of US$1 million or more, excluding their primary residence, collectibles, consumables, and consumer durables. "Ultra HNWIs" are those with more than US$30 million in investible assets.

Capgemini says those surveyed have a growing interest in crypto-assets.

HNWIs are becoming more interested in digital assets, especially cryptocurrencies. Half of the relationship managers we polled reported a surge in client interest and investment in crypto. Wealth management firms are taking notice; too: our global survey of wealth management executives found that over 77% either maintained or increased digital asset investments. A significant rise in business activity within the digital asset space backs the trend. There was a 2.7x increase in inflows related to digital asset investment products in 2023 when compared with 2022 levels.

Writing for Foreign Affairs, Andrea Kendall-Taylor and Richard Fontaine outline increased cooperation between China, Russia, Iran and North Korea over the past few years, which they say is helping Russia's war against Ukraine, and undermining Western efforts to isolate Russia. This alignment they refer to as a new axis of upheaval.

Since Russia’s invasion in February 2022, Moscow has deployed more than 3,700 Iranian-designed drones. Russia now produces at least 330 on its own each month and is collaborating with Iran on plans to build a new drone factory inside Russia that will boost these numbers. North Korea has sent Russia ballistic missiles and more than 2.5 million rounds of ammunition, just as Ukrainian stockpiles have dwindled. China, for its part, has become Russia’s most important lifeline. Beijing has ramped up its purchase of Russian oil and gas, putting billions of dollars into Moscow’s coffers. Just as significantly, China provides vast amounts of warfighting technology, from semiconductors and electronic devices to radar- and communications-jamming equipment and jet-fighter parts. Customs records show that despite Western trade sanctions, Russia’s imports of computer chips and chip components have been steadily rising toward prewar levels. More than half of these goods come from China.

The support from China, Iran, and North Korea has strengthened Russia’s position on the battlefield, undermined Western attempts to isolate Moscow, and harmed Ukraine. This collaboration, however, is just the tip of the iceberg. Cooperation among the four countries was expanding before 2022, but the war has accelerated their deepening economic, military, political, and technological ties. The four powers increasingly identify common interests, match up their rhetoric, and coordinate their military and diplomatic activities. Their convergence is creating a new axis of upheaval—a development that is fundamentally altering the geopolitical landscape.

The group is not an exclusive bloc and certainly not an alliance. It is, instead, a collection of dissatisfied states converging on a shared purpose of overturning the principles, rules, and institutions that underlie the prevailing international system. When these four countries cooperate, their actions have far greater effect than the sum of their individual efforts. Working together, they enhance one another’s military capabilities; dilute the efficacy of U.S. foreign policy tools, including sanctions; and hinder the ability of Washington and its partners to enforce global rules. Their collective aim is to create an alternative to the current order, which they consider to be dominated by the United States.

Too many Western observers have been quick to dismiss the implications of coordination among China, Iran, North Korea, and Russia. The four countries have their differences, to be sure, and a history of distrust and contemporary fissures may limit how close their relationships will grow. Yet their shared aim of weakening the United States and its leadership role provides a strong adhesive.

Kendall-Taylor and Fontaine argue all four countries want greater status and influence than the US-dominated global order gives them.

The growing cooperation among China, Iran, North Korea, and Russia is fueled by their shared opposition to the Western-dominated global order, an antagonism rooted in their belief that that system does not accord them the status or freedom of action they deserve. Each country claims a sphere of influence: China’s “core interests,” which extend to Taiwan and the South China Sea; Iran’s “axis of resistance,” the set of proxy groups that give Tehran leverage in Iraq, Lebanon, Syria, Yemen, and elsewhere; North Korea’s claim to the entire Korean Peninsula; and Russia’s “near abroad,” which for the Kremlin includes, at a minimum, the countries that composed its historic empire. All four countries see the United States as the primary obstacle to establishing these spheres of influence, and they want Washington’s presence in their respective regions reduced.

Definitely an "axis" to keep an eye on, as is any US-led response.

On holiday in Japan last year my kids were quite taken with the huge number of vending machines they came across. The weather was hot and they were thus only really interested in the ones selling cold drinks. You can certainly find vending machines in Japan selling other stuff though. But I've not seen one in Japan selling gold. As Bloomberg's Jaehyun Eom reports, you can find such vending machines in South Korea.

Apparently this is part of a global micro-investing boom whereby young people will even invest in fractional shares, i.e. less than one share in a company. Eom writes about a vending machine at a convenience store in Seoul's Gangnam suburb that sells gold.

The machine at GS Retail Co.’s convenience store sells gold bars from as big as 37.5 grams (1.32 ounces) to as small as less than 1 gram. Prices change daily, reflecting wider market movements, but start at about 88,000 won (US$64) for a 0.5-gram bar.

The machines operate in 30 stores in the company’s retail franchise across the country, six times more than the service started with in 2022.

“Currently we are seeing about 30 million won of sales per month,” said a GS spokesperson via text message. “The gold vending machine draws customers’ attention due to increasing demand for safe haven assets and the spreading trend of micro-investing.”

91 Comments

That Prospect edition, the Blanchard article, and the plainly obvious data right in front of us, should surely close the debate on whether the last couple of years inflation has been driven by excess demand.

NZ data out on Friday showed that profit margins across the NZ economy actually went *up* as RBNZ hiked interest rates. Crushing consumer demand by hiking rates is supposed to make companies compete harder and reduce margins, but that's not how the economy works I'm afraid. As a few of us have been saying for a long time, companies adjust to lower demand by reducing capacity.

Some will say that monetary policy still works though - because if the population has less money, prices simply can't go up because there is not enough money around to pay for stuff. This misses two obvious points though:

Firstly, while higher rates hit around 1 in 6 households hard, and another 1 in 6 moderately, interest flowing from banks to other households goes a long way to compensating households in aggregate. So, plenty of people can still splash the cash.

Secondly, companies that have market power over necessary goods and services like rents, water, energy, food etc, can put prices up knowing that they can force discretionary spending on other things down (and push Govts into increasing welfare subsidies).

As an aside, it amazes me that most of the $115bn of company profit ends up as income for shareholders, but those companies only pay out $125bn in wages. It's no wonder that the gap between the rich and the poor has never been more obvious.

We obviously have a different memory of the years where inflation was crazy. Or maybe it was different where I live. I certainly remember demand being off the charts, restaurants, bars, shops and services were heaving. At the same time labour was very tight, places were sometimes closed due to lack of staff, everywhere had hiring signs up. And there were also supply issues. In this scenario you would be crazy not to increase prices.

Since the RBNZ increased interest rates all that has changed, and now I’d say you would be crazy to increase prices, unless you are a monopoly or duopoly of course.

I don't think anyone would argue that monetary policy was too loose for too long creating the trainwreck you correctly describe. The issue we face now is that monetary policy has been pushed too far the other way and held there for too long.

JFoe is 100% correct.

If Jfoe was arguing that the RBNZ had gone too far then I may agree with him. But his general argument is that monetary policy doesn’t work and it actually creates inflation, I’m not convinced by that at all.

I am sure you can guess that my bias skews heavily towards expecting the root of all evil to be profiteering rentiers. As Adam Smith noted, markets should be free of rentiers (the last two words gets missed off a lot for some reason). However, the NZ data challenges my bias.

What the data shows clearly is that rampant profiteering only really took place in 2020 and the first half of 2021 - see retail margins here and the overall economy here. While demand was hot as you note above, two things combined to constrain profiteering, Firstly, we started to get media interest in price increases and the companies that had market power were making embarassing amounts of profit - they appear to have self-moderated. Secondly, the price of systemically important imports started to climb significantly (food, oil, fertiliser etc). Companies had to manage and balance these increases in costs with accusations of pandemic profiteering. The result was that operating profit margins dropped below pre-pandemic levels by mid-2022 (when demand and labour market was tight, right?) Then RBNZ started to hike interest rates. What happened to margins? They went back up - picking up in mid-2023 as import costs fell and debt costs stopped racheting up as quickly. Meanwhile we got sticky inflation because we let those price rises just wash through the economy.

JFOE

You make fair points abouts rentiers and excess profits, however in a free society if profits are legally contrained then society is not free but public reaction is a brake as Bed Bath Beyond/Target/Disney/Bud Lite have all discovered in USA. 5% net profit in a mature industry with plenty of competition may be fair the lesser number of players and the essential nature of the product changes that as does a new product and it development costs. Banks/Food/Energy all suffer too little competition whilst being essential, perhaps the cost of a social license should be in the form of taxation on excessive profits with that extra tax used for real social benefit in health etc.The other fatcor is risk and you rile against rentals but don't acknowledge the risk and the biased legislation favouring tenants, tenancy law should treat each party equally in terms of rights and responsibilities and the renistatement of interest deductability simply returned the treatment of rental income to the same way business deductions are elswhere unless the rationale is that such activities are not commercail so become a hobby and not taxable!

As an aside, it amazes me that most of the $115bn of company profit ends up as income for shareholders, but those companies only pay out $125bn in wages. It's no wonder that the gap between the rich and the poor has never been more obvious.

What percentage of company costs are wages.

Wages are $125bn and operatimg expenses are $540bn. So wages make up 19% of total costs.

This is private sector only - not including finance (banks and insurance).

The profit your talking about is net or gross? Seems kinda high if net.

It's the operating profit that Stats NZ use as part of the national accounts (to calculate surplus), so yes, it is high, but at least it is consistently measured. You can derive profit before tax from the tax data and you get an annual figure of around $70bn (and a profit after tax of around $50bn). However, these figures miss out a lot of the surplus generated and returned to owners, and the licensing fees paid to head offices in tax havens etc. Swings and rondabouts etc.

Most economic theory was formulated for economies that have functioning markets - NZ does not. So policies designed to make companies compete for customers won't work when there are no companies competing. In order for a competitive market to exist, there needs to be a minimum of six independent suppliers in it. How many markets in NZ can claim to have six suppliers? Groceries? Airlines? Building products? Insurance? If your markets are broken, should you change the economic policy to something novel or fix the markets that are causing the problem so that long standing economic theory works?

Economic theory also reckons capital consolidates, and those inefficient get driven out. Even in much larger economies, you can have way less than 6 competitors.

I don't think there's an easy, efficient answer. We could disincentivise larger companies, but surely a supermarket is always way more efficient than a dairy?

That is why there is supposedly a competition Regulator. Although they seem to have been completely captured these days. The days when the likes of AT&T gets broken up into 9 Baby Bells in an anti-trust suit are long gone. The new MegaCaps (Apple, Microsoft, Amazon, Alphabet) all need to be broken up today - but they wont be. Instead they will be allowed to hoover up and dominate all new tech (like AI) while suppressing or killing off any new threat to their revenue streams by deploying their capital to buy promising startups and shut them down.

You need enough competitors to break up a market operating as an oligopoly or de facto cartel. One of them needs to be incentivised to go its own way and not just ride the coat tails of the most aggregious price setter. And its not just about numbers as well, but size. The Big Four banks dominated the banking market in Australia until Macquarie entered the market and started taking market share, enabled by the Regulator because the Big Four were allowed to buy up all the regional banks and disappear them. It would help if NZ enabled deep pocketed players like Macquarie or Aldi to enter the market and offer some real competition. But our market is too small for them to really be bothered.

I think the point above stands - will the consumer be better off with smaller more competitive units, or larger less competitive ones? Are 30 smaller tech companies going to be better than 4 big ones, or will they just end up more expensive or with less features? Same with NZ - would we actually be better off with 6 small supermarket chains, 10 small banks, etc? Or will it just mean the cost of operating those chains is spread across less users.

K.W.: " In order for a competitive market to exist, there needs to be a minimum of six independent suppliers in it. "

Pa1nter: "Even in much larger economies, you can have way less than 6 competitors."

Really? Care to name some?

Lets start in the good ol' USA ... Or Europe ...

Amen, here endith the lesson.

"interest flowing from banks to other households goes a long way to compensating households in aggregate. So, plenty of people can still splash the cash."

I think this is severely overstated if you believe it has an effect, even an aggregate, on the economy. I'm mortgage free and with what I'd consider higher than average savings (>$100K + Super) and any interest isn't splashable. My observation is consumption is debt fuelled and people don't seem to have learnt from GFC or covid related carnage.

" $115bn of company profit ends up as income for shareholders, but those companies only pay out $125bn in wages. It's no wonder that the gap between the rich and the poor has never been more obvious."

So, the workers got 'only' got $10bn more than the shareholders??...How many shareholders Vs how many workers?. And how many workers wouldn't have jobs if shareholders hadn't put their money in in the first place?

I was passing through Dubai & Abu Dhabi on a work trip over a decade ago & had a few days to spare. In a large hotel we went to use an ATM & initially chose the wrong one: it only provided a range of small gold bars.

How do you know they were real gold bars?

Are you aware of the penalties for theft & fraud in the UAE?

I'm not at all interested..

Then why ask irrelevant questions?

It’s what he does when he isn’t protesting stuff no one cares about.

"Are you aware of the penalties for theft & fraud in the UAE?"

I have a relative who is a lawyer in the UAE. Their responses would be:

- Only if you are caught

- Only if the police can be bothered and a conviction is even possible

- Only if you can't do a deal with the 'authorities'

- Only if you are not an Arab.

- Distantly related to the royal family, forget it.

#4: Definitely an "axis" to keep an eye on, as is any US-led response.

Director of Kurchatov Institute [Russia’s leading Soviet-era R&D centre on nuclear energy] Prof. Mikhail Kovalchuk: “They [US] are not afraid of China because only we can turn America into nuclear radioactive ashes.” Link

I think 'rents' need a good kicking if the economy is going to be opened up to a wider audience. I see some stats that throw that 22% of the average wage is spent on rent but looking I see the 'after tax' on the average wage sits around 53-56k (various sources) so lets say the average leans near 1k a week income after tax (which i suspect is being generous) again we have an NZ weekly average of $560-$648 rent that would put the % of income the average single earner contributes to rent at 56%-64% so if we split that between a couple then we see the average is no where near the 22.32% thrown around by statisticians . Its closer to 28-32% for a couple ...no wonder 36% of the populace are saying life is not really affordable. Interest rates wont make life affordable for those aspiring to climb into RE....it is their ability to save . Interest rates wont save the overall economy it is the ability of all to have loose change to spend that will bring vitality. My opinion is 'rents need a good kicking down'.... All the surplus is currently going to the banks via interest rates and high rents . Retailers and providers of services are in danger of becoming extinct via the banks. So do we have stats that lean toward making the obvious 36% that report to be experiencing hard times made out to be telling porkies? Good luck with thinking lower interest rates will solve everyones problems , I think the problems are much more complicated and shifting interest rates will only widen the gaps. Fact is a rent freeze might be in order if interest rates are to be lowered. The banks are on the 8 ball and its not looking pretty. Game Over!...lol

Rents are simply tied to house prices its that simple. Problem is however just because interest rates go down doesn't mean that rents will go down, you seriously do not expect that someone who put it all on the line is going to pass on the savings to the renter do you ? Its pretty simple really if you don't want to rent you buy instead and trust me 50-80% of your income will be going on the Mortgage for 10 years straight instead, been there done that. You cannot freeze rents, its a private concern so until the government starts building state houses again instead of trying to put people in Motels, noting will change. We now have a whole load of problems out there from multigeneration blungers that are milking the system to the way the whole next generation is work adverse. Things have changed for the worse over the years, I don't see how to reverse the trend.

You cannot freeze rents, its a private concern so until the government starts building state houses again

Which ironically will need to still be paid for by the "productive" economy.

I don't see how to reverse the trend.

You need to make housing some sort of legally prioritized right for any citizen/resident, over many of our existing rights.

Basically, you need to be able to tell the NIMBYs and regulators to get f'd.

Nope, rents in a limited supply environment are tied solely to income. They rise to whatever people can afford to pay.

Allow foreign capital in the build-to-rent housing sector and regulate it on mainly two aspects: quality and returns.

Mandate Kiwisaver, ACC and NZ Super to put a decent chunk out of their fixed income portfolio in such initiatives.

See the excess hot air gradually come out of the property market.

+ Land tax.

You might want to check the news on what's happening in the build-to-rent sector where they have become a significant player - they're manipulating markets to boost rents to the moon.

I look at my own properties, if I rented them out 25% of the rent would go to pay rates and insurance, 30% would be collected as tax. So as a landlord I would only clear 45% of the rent as a return on my investment, and that assumes that I dont spend anything on repairs or maintenance. I'd get at least double that if I sold up and put the money in the bank. As soon as the penny drops that capital gains are no longer assured, the rush to sell up will become a flood.

Falling house prices may lower mortgage interest costs. But they will do nothing for the ever increasing burden of rates and insurance costs. One thing I noticed when looking at property in Australia recently was how much cheaper rates and insurance is over there. A family could save thousands of dollars a year simply by moving and saving money on their rates bill. My rates and insurance costs are now so high that I could buy a similarly priced apartment on the Gold Coast with full resort facilities, and the Body Corporate/Rates bill would still be less than what I currently pay just to live in my Christchurch home.

As soon as the penny drops that capital gains are no longer assured, the rush to sell up will become a flood.

Except of course if someone's using debt to acquire the property, and the tenant is paying much of the debt.

There's not enough left now to pay the interest on the debt, let alone pay off the debt. When your net yield after rates, insurance, maintenance is 2% but you are paying 7% interest, the numbers simply do not work in the absence of capital gains.

If those were the only possible numbers people were looking at, then you might well be right.

But they would work after some big capital losses.

There wouldn’t be much money in rental cars either if they had to pay $1 mil for a car.

Rates aren’t that much really. Ours are $3k a year, or $57 a week. We actually get a fair amount for that; rubbish, recycling, roads, footpaths, parks, playgrounds, environment, stormwater, pet control, building control, and probably lots more I can’t think of right now. I can’t see how it could be much cheaper.

Lucky you, my rates are well on their way to 7K per year, along with my insurance...luckily I was able to half the insurance costs and get the same coverage by dumping the broker and shopping around.

Maybe time to downsize then. You must have quite the pad to have that rates bill.

My rates are $8,400 and going up another 15% next year. In comparison, a house of the same value on the Gold Coast (same population as Christchurch) is $3000. Perhaps we should send someone to Australia to find out how they manage to do all of the above mentioned things, while still managing to spend a billion a year on infrastructure projects?

I had a small 1970's 2 bedroom cross leased flat, back one of three on the title, the current rates for that little flat is $2,726. The rates on my 1950's 2 bedroom house in Marlborough is $3,166.

Sure, we can all downsize into tiny unrenovated homes built 50-80 years ago, but some of us like living in a modern house. We just wish it was still affordable.

Bitcoin up 400% since this site announced it's last stand (article)

And yes the HNW people of this world see it and are getting in. Helped several buy in over 500k since NY and they only want more as they learn

they only want more as they learn

You mean, as the price goes up.

No learning that swapping a debasing asset for a hard asset is a wise move (unless you are happy with theft, which you seem to be Painter).

Depending on the demand for the hard asset. The fact alone something is of a fixed quantity doesn't ascribe it value.

Agree - it also needs also to have portability, durability, be decentralized and have privacy.

And you think this is what's supporting the current BTC value?

There's plenty of very fragile, hard to transport items worth lots of money.

Pa1nter. Bees don't waste time explaining to flies that honey is better than shit.

Even house prices in NZ are on a steep decline when priced in Bitcoin, Gold, S&P500.

Pa1nter. Bees don't waste time explaining to flies that honey is better than shit.

This is a big problem in middle Nu Zillun. People have been conditioned to believe that things behave like they've been told and future outcomes are boiled down to simple memes. The finance industry and media are complicit here because it has put food on the table for them.

Therefore you have a population all hanging off the prophecies given to them. If the fiat price of rat poison had increased at 1,000% pa since its inception instead of closer to 100% pa, they still would claim that they wouldn't touch it with a barge pole, not even 1% of a portfolio.

My preference is to be net positive 90% of the time. I.e., any dollar I have in something should be worth the same or less than what it owes me, at any time, should I need access to the value.

You know, in case I want to expand my asset base, or just do whatever I want with the proceeds.

Bitcoin cannot offer me that same level of consistency. Nor can it offer me any form of income/annuity/dividend.

My preference is to be net positive 90% of the time. I.e., any dollar I have in something should be worth the same or less than what it owes me, at any time, should I need access to the value.

Sure. But that is impossible. The purchasing power of fiat diminishes over time, unless of course the rate of return from the currency > inflation, which is ephemeral but related to expansion of the money supply; the price set be a central bank; and the price level of goods and services.

Nevertheless, people must hold fiat. Suffice to say, people living paycheck to paycheck are in some way behaving rationally.

It's possible. You find out a way to make money reliably, and keep doing it.

But then again I'm fine clearing 20-30%. You guys are obviously more keen to make 10s of thousands of percent, very sporadically and without prior notice.

Totally different financial approach.

But then again I'm fine clearing 20-30%.

Well that's good. However, I would be surprised if most people are retuning 20-20% on fiat, unless they're a payday lender. Even with P2P lending those rates of return are very risky.

I'm not sure anyone just sitting on fiat expects it to make much more than inflation.

If you're young your surplus cash is best served being put to work rather than gathered.

Yes. If you had accumulated ratty monthly from the previous all-time high price in Nov 2021, you would easily have returned a CAGR of 30+% by forgoing fiat. Total return from that month to now - accumulating monthly - would be 134%.

I guess J.C, Painter,at the end of the day people invest in what they know. I would struggle to move away from land and forest for example.

To enter the cyber world and put money into something intangible would be like buying a ticket to Mars.

I guess J.C, Painter,at the end of the day people invest in what they know. I would struggle to move away from land and forest for example.

Yes, I can understand this. But even if I 'understand' land, property, rat poison, it doesn't mean I necessarily 'invest' in it. F'more, even if I know the value of fiat currency is being destroyed, it doesn't mean I should not hold it.

Land and property are interesting though. If it is indeed a store of value, arguably everyone should simply pile their savings into property funds. But as we're seeing at the moment, these funds are not particularly valuable. Looking at the Smartshares NZ Property ETF as a proxy, if we assume a benchmark of 10% pa to beat inflation, returns are all sub-par and dreadful.

21 Trillion, that was awesome. Had to pass that one on to a bee keeping mate.

Imagine living in a country where such a thing as a vending machine for gold can exist. If that were NZ, it would have been ram raided on the first night it was installed, and every night subsequent.

I was recently on the Gold Coast and reading the local news about the police arresting kids for stealing a car and going on a joyride. If only NZ police paid such attention to actual crime in NZ we would all be better off. Instead, Australia just deports all their criminals to NZ where NZ ignores their criminal behaviours, or gives them a couple of months of sitting at home watching TV as punishment for them.

Well at least the current government have promised to change that...who is currently the prime minister by the way?

I hope it works. NZ used to be a safe place to live. Now its constant stabbings, shootings, bus stop assaults, ram raids, and armed jewellery heists. My local FB group is full of people warning about stolen or smashed up cars, people wandering onto properties for a snoop around, break ins and burglaries. A few months ago every car parked on the street next to mine got their windows smashed in. The police do absolutely nothing. Even if they did, the courts would do even less, and they'd be back out offending within hours.

Unfortunately I cannot see things getting any better, NZ simply does not have the capacity to provide the resources necessary for a meaningful drop in crime. Worsening social issues, which also require immense resources to address, will just add fuel to the fire.

It's horrific to watch and I feel gutted that my kids will not get to see the NZ I grew up in.

I think they have been way too soft on small crime and then once those criminals get away with a few they escalate. I’m happy for people to get a second chance, but no more.

One recent offender in the recoupment trend is Dominos. Once upon a time they advertised a deal like "get a traditional or value pizza and choice of side delivered for $25". Then they changed their pricing model, and now its "from $25", because once you start ordering you find there is only one pizza and one side that you can buy for $25, anything else and you have to pay extra. By the time you've selected the pizza and side you want, and added delivery fees your $25 deal is now $40.

Consumers do eventually wake up and vote with their wallets. So its no surprise that Dominos is failing with their share price back at 2015 levels and down 77% from the 2021 peak. Its only in markets where there is no competition, substitution or discretion available that this pricing mechanism works.

I have seen a recent trend where cafes will advertise an eggs benedict option but you have to pay extra for the bacon. Needless to say on the rare occasions I eat at a cafe it's the first thing I look for and if they are taking the p#ss I leave.

This type of thing has been around for a while (pay extra for a blob of tomato sauce, mayo etc) but is really getting out of hand now.

That and shrinkflation. Have you seen how tiny a Snickers bar is these days? Its not even worth buying, 2-3 bites and its gone. So much for being the bar that "really satisfies".

One big trend I noticed in Melbourne, is that all the top restaurants (like the top 10-12) no longer do a la carte. They all do a degustation menu for a set price (usually $150-$360 a head). Thats one way of enforcing a minimum customer spend.

It's almost as if the monetary system we rely on with ever growing debt and property prices is affecting the basic business practices?

Where there's winners there's always losers and we are all feeling the losses incrementally.

Consumers do eventually wake up and vote with their wallets. So its no surprise that Dominos is failing with their share price back at 2015 levels and down 77% from the 2021 peak

Don't know where you're getting your information. Dominos share price is up almost 400+% since 2015. It's a great company and its share price has performed extremely well over the long term. Like owning Amazon or Google.

Don't know where you are getting your share price info from. Dominos (DMP) is currently $39 a share, which it was $39 a share in 2015. It reached $167 in 2021.

https://www.google.com/finance/quote/DMP:ASX?sa=X&ved=2ahUKEwjk9LLppc2G…

I get my info from TradingView and what I study about companies. Dominos is a beast of a stock and a great company IMO. Stock price has 50x'd since 2009. Even to 50x in Etheruem, you would have had to buy before the 2018 bull run.

The stock sticker and poor performance of the Aussie master franchise (DMP) is irrelevant in the scale of things.

Its relevant in that it reflects the Australian and NZ business performance, which is the subject under discussion. We dont buy pizza from America. So your comment is irrelevant, not mine.

OK.

But you will agree that the Dominos business and its performance is something special, outside the environment closest to you.

Dominos is in 83 countries - truly global. No Nu Zillun company can arguably match Dominos in terms of reach, performance, growth. Fonterra might be a supplier in certain markets.

You are what you eat ...

In my experience they always fall over eventually

Just don't buy it. Dominos pizza are only worth about a buck each in ingredients. They are terrible, my kids won't touch them. Long may that be the case.

He wasn't advertising Domino's Pizza, he was simply making a point.

Good on Dominos, if they can make a pizza for a dollar and sell it for ten, well done. {pardon the pun}

The biggest rip off merchants here in New Zealand are the local councils. Their god put it in the pipeline that 17% rates increase were fine - so they all did it.

And the last and this government has just sat bye and let it happen.

They have actually been doing the opposite of ripping us off; they have been charging us less than the real cost and using debt to pay their bills. They have decided to rip off the next generation instead. But now that the price of debt has increased it’s getting hard for them to continue with that model.

That's right Jimbo, who we have to thank for the massive increases is past councilors who have been to soft and refused to increase rates incrementally just to appease.

100%. I've just been over on the Gold Coast, which has the same population as Christchurch. If I sold up here and bought a house there for the same value, I'd save $5,400 a year on rates (thats $104 a week). And I'd have a house a few blocks from the beach with a pool. And the difference will be even starker next year when Christchurch rates go up another 15% while Gold Coast rates are only going up 4%.

I've worked out that I can buy an apartment in a 5 star building right on the Gold Coast beachfront with amazing resort facilities, and it will still be cheaper to pay the rates, body corporate fees (which includes insurance), and water bills over there then it is to pay rates and insurance on a home in Christchurch. Makes me sick.

Test your heat tolerance in their summer. Kills me, 4 months of the year is my forewarning of hell and eternal damnation. Better to head to Northern hemispheres when it’s wet/cold at home.

Yes, I plan to go check out what its like in summer, although I am used to 45 degree days from living in Melbourne. It will be the humidity that will be different. But then, theres a pool ....

Adrian Orr, the guy who printed money (the raw definition of inflation!), told you that profit led inflation was happening in NZ. This after Waikato University completed a study on it earlier this year and concluded that corporate profit making contributed little to current inflation in NZ. Orr is just trying to shift blame to anyone that is not him and the RBNZ. I’m not sure Gareth, why you would not counter what Orr told you with the Waikato study, as it would beggar belief that as a editor, you wouldn’t know about it if you were going to write opinion on profit led inflation in NZ.

#3) What high-net-worth individuals are investing in.

I've changed my opinion - am now disappointed with capitalism in how it has a pyramid affect with only a select few getting wealthy.

Also, in theory we have a higher standard of living now compared to 40 years ago - but I can't work out why it was achievable to have a stay home parent back then, but now that is quite rare - must be due to increased average taxes (including gst) plus a deterioration of home to income ratios caused by flawed credit creation economics.

Everyone has become proportionally more wealthy under capitalism Epsom. So don’t be too disappointed.

LOL.

I'm reminded of the famous line from Animal Farm: "All animals are equal, but some animals are more equal than others."

Sorry, your assertion - as it stands - that "Everyone has become proportionally more wealthy under capitalism" is demonstrably wrong . Caveat it - it requires a lot of caveats - to make it right - and the truth will out.

Duh…you do realise it’s a satire of socialism…every one hates capitalism but they don’t want to live under socialism

I can't work out why it was achievable to have a stay home parent back then, but now that is quite rare

1./ More resources available back then, could still rip down native forests to build state houses, more available land closer to cities and towns.

2./ Women have vastly more opportunity in the workplace now than 40 years ago and more social stigmas, and prejudices have been addressed more so than then as well. Having one parent at home back then was not always a choice. We have effectively doubled the labour force in doing so, and this can't be done again. It is also of note that not all parents wish to stay at home for years with their kids, some may wish to work part time or even full time given the level of opportunity today.

3./ Cost of housing, where it were possible to purchase a home at 3x DTI of one SINGLE income, free university (no student loan to stifle saving ability, allowing to save for a house faster) it was affordable to have one person at home. This is not so today unless one has substantial income.

..... plus for those who stayed at home there was 'more opportunity'? to do meaningful voluntary work out in the community. With societal change and the more individualistic we have become, when it comes to voluntary/community work, there seems to have grown a different feel for it today?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.