By Patrick McGuire & Goetz von Peter*

Tracking the size of carry trades and the entities involved is notoriously difficult. While Bank for International Settlements (BIS) statistics record total amounts of yen borrowed from banks or via foreign exchange (FX) derivatives, they do not reveal specific uses – the carry trade being just one of many.

This article explains how these statistics can provide some rough indicators of carry trade activity. The figures should be interpreted with care given data gaps and the assumptions used.

A carry trade is a leveraged cross-currency position designed to take advantage of interest rate differentials and low volatility. The strategy involves borrowing funds at a low interest rate in one currency (the funding currency) and buying a higher-yielding asset in another (the target currency). In recent years, low interest rates for the Japanese yen relative to other currencies have made the yen a funding currency of choice. The use of leverage makes these positions sensitive to changes in exchange rates, interest rates and volatility.

There are several ways to implement a carry trade, each with different implications for what can be seen in international statistics. The textbook case involves borrowing the funding currency, selling it spot and investing the proceeds in an asset denominated in the target currency. This is recorded as debt (eg bank loans) owed in the funding currency.

The more common approach used by hedge funds and other speculators relies on derivatives – eg FX forwards, swaps and options – to establish an open forward payment obligation in the funding currency. An outright forward position to deliver yen at maturity is a bet on yen depreciation. Borrowing yen in an FX swap to sell yen spot is an attractive alternative, given the depth of FX swap markets. Since the use of derivatives requires no on-balance sheet borrowing of the funding currency, it is difficult to trace the trade in the statistics.

Despite these limitations, the BIS international banking statistics (IBS) and over-the-counter (OTC) derivatives statistics shed some indirect light on carry trade activity. This is because they provide a currency breakdown of banks' on-balance sheet positions and of outstanding amounts in FX derivatives markets, respectively. Consider on- and off-balance sheet yen borrowing in turn.

The IBS show a sustained rise in on-balance sheet yen borrowing over the past few years, an increase that may – but need not – be linked to carry trades. Banks' yen-denominated claims – which include loans, holdings of debt securities and derivatives with a positive market value – on non-banks resident outside of Japan reached $880 billion, or ¥133 trillion, in the first quarter (Q1) 2024 (up from ¥110 trillion in Q4 2021).

The bulk of these claims are on borrowers in the Cayman Islands, mainly non-bank financial institutions (NBFIs). Special purpose vehicles located there issue debt securities purchased mainly by banks located in Japan. Such financing structures, however, have been in place for decades and have shown modest growth of late, so that they may not be related to speculative carry trade positions.

Banks' yen-denominated loans to non-banks outside of Japan have grown noticeably, in particular since mid-2021. Outstanding amounts rose from $228 billion (¥25 trillion) in Q2 2021 to $271 billion (¥41 trillion) in the most recent data for Q1 2024. (The depreciation of the yen between then and Q2 2024 would put that value at roughly $250 billion.) These loans were mainly to borrowers located in the United Kingdom, the Cayman Islands and the United States. Without more detailed data, however, it remains unclear whether this relates to carry trades.

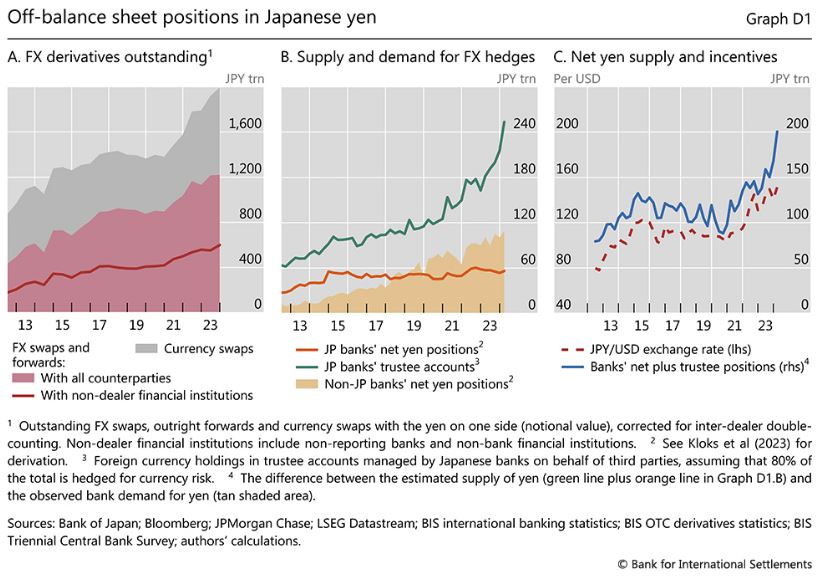

What about information gleaned from the BIS derivatives statistics, the instrument more likely to be involved in carry trades? These statistics show that the notional value of outstanding FX swaps, forwards and currency swaps with the yen on one side has grown to $14.2 trillion (¥1,994 trillion) by end-2023, up 27% in yen terms since end-2021.

FX swaps and outright forwards drove this growth (red shaded area). The bulk of these are used for hedging and liquidity management, but they can also be used for speculative purposes. While nearly half of the outstanding FX swaps and outright forwards are with "non-dealer financial institutions" (red line), which includes non-reporting banks and NBFIs, the share specifically related to speculative activity is likely to be much lower. For example, using counterparty turnover data, estimate hedge fund FX forward positions to have been about $160 billion.

An alternative approach to assessing carry trades via FX derivatives is based on the IBS, which provide an indirect and incomplete view of positioning in the markets for FX derivatives. These statistics track banks' net on-balance sheet positions in major currencies, which in turn reveal their net positions in FX derivatives under the assumption that they do not run large open currency positions.

This is a reasonable assumption because of supervisory guidance. If so, any open on-balance sheet position must be offset by a corresponding off-balance sheet position. For example, a bank with a yen funding base can exchange yen for dollars via an FX swap to purchase a dollar asset; the offsetting on- and off-balance sheet positions shield the bank from exchange rate movements for the duration of the FX swap since the exchange rate at which it is unwound is set in advance. Currency mismatches in banks' on-balance sheet positions are thus indicative of their (unobserved) net positions in FX derivatives.

To a large extent, banks from different currency areas offset each other's FX derivatives positions. For example, Japanese banks are natural suppliers of yen via FX derivatives: they have a domestic yen deposit base but hold portfolios of foreign currency assets and use FX swaps to hedge the currency risk. Non-Japanese banks in turn absorb much of this supply by providing dollars and other currencies in exchange for yen via FX derivatives.

They do so to hedge their own yen-denominated asset portfolios and, since the Great Financial Crisis, to take advantage of the cross-currency basis trade. Their net yen assets, and hence their estimated net yen borrowing via FX derivatives, has grown threefold since 2017, surpassing the net supply of yen from Japanese banks (shaded area minus orange line).

Non-banks also use FX derivatives, but here the picture provided by the IBS is far less complete. These statistics capture only the assets in "trustee accounts" managed by Japanese banks on behalf of third-party investors (ie not on Japanese banks' balance sheets); they do not capture those of other non-banks around the world.

Even so, assets in these trustee accounts, which totalled $2.7 trillion at end-Q1 2024, imply a supply of yen in FX derivatives when they are hedged for currency risk. More than three quarters of the total amount is denominated in currencies other than the yen, and the bulk is likely to be in debt instruments.

Assuming 80% of these holdings are hedged for currency risk, an estimate of the supply of yen via FX derivatives reached $1.7 trillion (¥254 trillion) at end-Q1 2024. If only 60% were hedged, the amount would fall to near $1.3 trillion (¥190 trillion). Other institutional investors in Japan that hold foreign currency asset portfolios on a (partially) hedged basis would add to the supply of yen in FX derivatives, as would corporates outside of Japan that issue yen-denominated bonds on a hedged basis. Unfortunately, these positions are not observable in BIS statistics.

Combining the observable elements – the trustee positions and banks' own use of FX derivatives – yields a time-varying, albeit incomplete, measure of the net supply of yen available for other players in the FX derivatives market. The blue line in Graph D1 above is the difference between the estimated supply of yen (green line plus orange line in Graph D1 and the observed bank demand for yen (tan shaded area).

Market clearing requires that other, unobserved non-bank market participants absorb this supply. These could include institutional investors outside Japan that hold yen-denominated assets on a hedged basis as well as speculative investors seeking to engage in carry trades by borrowing yen. If the latter transaction involves a subsequent spot sale of yen, to bet on yen depreciation, it can put downward pressure on the currency.

The co-movement between the measure of net yen supply and the USD-JPY exchange rate suggests that speculative investors may indeed have been involved. The measure rose by ¥66 trillion between end-2021 and Q1 2024, or $435 billion at Q1 2024 exchange rates, coinciding with a significant depreciation of the yen (red-dashed line) and rising incentives for engaging in carry trades.

The IBS alone reveal little more than an indirect picture of the global dealer banks that sit between the various types of non-banks with positions in FX derivatives. Better data on the users of FX derivatives and their positioning in these markets are needed for a more complete picture. To this end, the BIS is working with the Committee on the Global Financial System to enhance the OTC derivatives statistics. Such data would complement other market indicators and flow data in the monitoring of carry trades.

*Patrick McGuire is Head of International Banking and Financial Statistics and Deputy Head of Statistics and Research Support at the Bank for International Settlements (BIS). Goetz von Peter is Deputy Head of International Banking and Financial Statistics at the (BIS). This article comes from the BIS Quarterly Review for September 2024 and is used with permission.

The views expressed are those of the authors and do not necessarily reflect the views of the BIS.

5 Comments

Its bigger that all believe. When the Japanese sell up, who will buy and at what, much lower prices will these assets go to?

Don't want to be a PC police officer but that's not necessarily an appropriate term for Japanese people. One of our revered All Blacks used the term in a podcast. Unfortunate as he was living there.

Your questions are all valid. I recommend looking at JPY/NZD and JPY/AUD during the GFC period to get an idea of the extent of how disruptive the carry trade can be.

Soz.....just being lazy and short.

CARRY TRADE

What this article doesn't mention is the fact that the massive carry trade industry is a product of the global fiat casino system that is a debt death spiral. It's just another symptom of a system that was always going to have a very finite life span.

More than 90% of the Western world, including analysts and commentators, whether or not they are genuine or just simply shills for the global private banking cartel, don't mention any of this.

They/we suffer from ingrained recency bias - the fact that most of us have grown up with a fiat system when in the entire scheme of things, in 5000 years of banking, fiat has only been around for a mere 100th of this timespan - where money has not had some form of hard-backing.

This is a big enough problem at national currency level, but when the global reserve currencies are all fiat as well, it is a guaranteed recipe for disaster. It was a kleptocratic planned move away from productive industrial capitalism, into the trappings of parasitic and non-productive financial capitalism - a system that cultivated blatant neo-feudalism and neo-colonialism

Japan is a classic example of this - their incredible growth was based on banking run as a public utility, and investment in industrial capitalism rather than asset bubbles. This remarkable little resource-poor country once threatened to overtake the U$ in total GDP - until they chose to squander their economic miracle with disastrously inappropriate QE and endless money printing.

THE END OF FIAT CURRENCIES

Globally, somewhere in the region of 4800 fiat currencies have completely failed (IOW, gone to a big fat ZERO). Their average lifespan is a mere 35 years - at 53 years (since 1971) the US dollar has already outlived this figure - it has already lost around 98% of its value.

The British pound is a classic example. Once upon a time, you could buy a gold sovereign for £1 - now that same coin will cost you £450 - IOWs, the £ is only left with 1/450th of its original purchasing power - roughly 0.2%!!!

THE BIS - FIAT'S NEMESIS

It was painfully obvious to me that the BIS and most of the global central banking

industry has already decided that fiat currencies have had their day when Basel III changed the rules to allow physical gold to be classed as a Tier-1, from the previous Tier-3 balance sheet asset. It now enjoys the same balance sheet status as cash and govt treasuries - but with 2 massive additional advantages...

(i) Zero risk in asset value erosion - they hold an asset on their balance sheet that has retained its purchasing power for goods and services for 5000 years.

(ii) Zero counter-party risk compared to holding cash or bonds, which are essentially paper credit obligations with no inherent ultimate value and which become increasingly risky by the day - especially with two major wars on the point of escalating into full-on global warfare.

Even the central banking industry realises that the fiat system is so utterly broken that they need to hold a degree of physical assets on their balance sheets, rather than exposing themselves to unnecessary man-made paper assets.

J P Morgan was right about one thing ... "gold is money - everything else is credit' - of course in this day and age that's all that the 2.5 million different crypto-currencies are too - credit tokens, with only implied value - they rely on their credibility, having ZERO intrinsic value - less inherent value even than tulips!

GLOBAL DE-DOLLARISATION

The global CBs could see the writing on the wall - the growing trend for bilateral direct trade and the declining need to hold these increasingly risky assets as reserves. The BRICS could announce their new UNIT, a global first - a trade-only currency instrument which is not a national currency at all - rather it is 40% backed by physical gold, with the other 60% backing derived from a mixture of their member-nation currencies, which are soon poised to be hard-backed too.

In doing so, the BIS in reality became the formal nemesis for all fiat currencies and the catalyst for the return to hard-backed national currencies. What we are seeing now is a major splinter in the global central bank's historical orchestration of continually masking the physical gold price to try to hide the massive erosion of the purchasing power of the fiats.

Clearly, the Fed has diverged and continued to bet against gold. Along with their massive leasing and rehypothecation of their claimed reserves (8133 tons) it is looking increasingly likely that they own a significant negative tonnage of physical bullion. The Fed and the US Treasury have been disastrously wrong-footed.

This central bank move appears to me to be payback for the US deliberately wrecking the German economy, and as such the entire EU economy as well. It is also a desperate attempt to save their own national currencies - personally, I think it is far too late for that now - they are already being sucked into the debt death trap vortex, arguably worse even than the US.

GOLD REVALUATION

At any stage BRICS could announce a physical buy price for gold at the Moscow and Shanghai exchanges, which would immediately revalue gold globally - paper manipulation would become nothing more than a quaint historical notion on that very day.

The physical gold price would break out and head for the hills to a new organic price discovery paradigm - $3,000/oz, $5000, $50,000 - who knows?

Of course, this is not the value of gold changing - it would simply be the unmasking of the dismal plummetting purchasing power of fiat currencies, including the one that is nothing more than portraits of dead presidents printed on fancy paper.

Regards to all

Colin Maxwell

I have done NZD/JPY carry trades for years. Buy NZD sell JPY 1 year forward. Pick up the interest differential. Then forget it. The currency gains just add to the overall gains.

Most years, it goes well. Every now and then there is a steep drop lower. I just wait. It always corrects higher again. Most times I do more when it falls hard. But you need deep pockets to cope with the sharp down moves.

It has been extremely profitable.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.