Here's our summary of key economic events overnight that affect New Zealand with news of a rather surprising counterattack underway in Ukraine, with Ukrainian forces also said to be bombing targets inside Russia (a Russian claim, disputed by Ukraine - so who did it?). Russia is now left 'defending' its recent gains in the south.

Russia's poor performance in its war has left China exposed diplomatically, especially in its overnight 'summit' with the EU. What is interesting however are India's equivocal positions. New Delhi seems attracted to the authoritarian side of all this.

Elsewhere, US non-farm payrolls grew less than expected, up +431,000 in March from February on a seasonally adjusted basis. Markets had expected a +490,000 gain. But on an actual basis, +794,000 more people were employed in the month and it is the extra earnings of these 'actual' people that will drive consumption.

Their jobless rate fell, their participation rate inched up again, its sixth consecutive rise. Average weekly earnings rose +5.8% from a year ago, but average hourly earnings rose an impressive +6.7%, suggesting that workers on average are holding their position against fast-rising inflation. It will be fuel prices that will be the main pressure point and there might be some easing on that front soon.

Meanwhile, surveys of factory conditions in the US are uniformly positive. The two main ones report good expansions. The widely-watched ISM one shows overall growth marginally less in March than February, but with new orders, production and employment growing, new export orders growing, the order backlog growing, and the deterioration on supplier performance easing. The main negative issue is that all this demand is pushing up prices faster. The internationally-benchmarked Markit one was equally positive, noting production and new orders rising steeply, and cost pressures gaining renewed momentum.

These are the best American factory conditions in decades - and maybe the de-globalisation shift because of supply-chain issues are driving it.

Despite the US pull, globally factories are expanding at an unchanged rate.

March factory PMIs in the Asian region shows most expanding at moderate levels. That includes Taiwan, South Korea and Japan.

But the private sector factory PMI for China came in lower than the official version (49.5), contracting at an index vale of 48.1 when a steady-state 50 was expected. It was their biggest fall in more than two years. It will only get worse for China as they stumble over their new pandemic spread that is high risk because they have key demographics with very low vaccination rates - and they have a second-class vaccine that is barely 50% effective. A widely locked-down China will have broad trade implications.

More stories are emerging of retrenchments in China. And buyers are not emerging to re-invigorate their housing markets.

In Europe, their PMIs slid to a 14-month low in March amid rising inflation and geopolitical tensions. But they are still expanding and at a moderate-to-good clip.

But like China, not everyone is expanding, and some contractions are rather steep.

EU inflation remains high with the March level up to 7.5% pa, driven of course by energy costs. That is similar to, but less than American CPI inflation. We get New Zealand inflation data on Thursday, April 21, and that is sure to be elevated too. What is interesting about global inflation is that the effects haven't hit some countries yet. And up to now that has included Australia and many East Asian countries. What that should be, given their equal exposure to energy costs, is unclear, but the March outcomes when they are released should shed some light on these differences. It may just be a timing issue.

Globally, hiring is strong, especially in the West. But American bond markets are toying with inverted yield curves, even if it is with little conviction at this stage. Inverted yield curves suggest recession is ahead. But few but perma-bears really believe that, and the IMF doesn't. Expanding factories and strong demand for labour aren't usual signals for recession. Perhaps the supply chain realignments are helping here and that effect won't be temporary.

The UST 10yr yield opens today at 2.38% and up +6 bps from this time yesterday in volatile trading. It hit 2.45% earlier and closer to the 2.49% level it was at a week ago. The UST 2-10 rate curve starts today inverted by -5 bps. Their 1-5 curve is however a little steeper at +86 bps. Their 30 day-10yr curve is marginally steeper at +220 bps. The Australian ten year bond is up +4 bps at 2.79%. The China Govt ten year bond is unchanged at 2.83%. And the New Zealand Govt ten year is up +5 bps at just on 3.30%. A week ago it was at 3.31%, so little net change.

On Wall Street, the S&P500 is heading for a flat result in their Friday trade, and a -0.3% fall for the week after a very up-and-down five trading days. Overnight, Frankfurt ended up +0.2% for a +0.5% gain over the week. For Paris it was a weekly gain of +1.6%, and for London a weekly rise of +0.7%. Tokyo ended its week down -1.5% but Hong Kong booked a weekly gain of +2.9% and Shanghai a weekly gain of +3.1%. The ASX200 ended flat on the day and up +1.2% for the week. The NZX50 ended Friday down -0.2% but up a minor +0.3% for the week.

The price of gold starts today at US$1924/oz and down -US$20/oz from this time yesterday, and down -US$32 from this time last week.

And oil prices are down another -US$3.50 to just on US$99/bbl in the US. And the international Brent price is now just over US$104/bbl. These falls are because the US has ordered its largest-ever release of strategic reserves. And other nations are following suit.

The Kiwi dollar will open little-changed than at this time yesterday at 69.2 USc. Against the Australian dollar we are down a bit at 92.2 AUc. Against the euro we are unchanged at 62.6 euro cents. That all means our TWI-5 starts today at just on 74.4 and -50 bps lower in a week.

The bitcoin price is firmer today, up +1.5% from this time yesterday to US$46,477. From this time last week, it is up +4.9%. Volatility over the past 24 hours has been moderate at +/- 2.8%.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

79 Comments

Two Major Economies, One Key Difference In Timing

Not just China, either.

There never is decoupling. Eventually, the downside comes to everyone. Even forty-year highs for what isn’t inflation. So much worried fascination over the wrong thing, the PCE Deflator, when the vastly more relevant worry is displayed in Chinese. It’s just not Russian nor pandemic.

While that blistering increase in annual hourly earnings of 5.6% is basically the biggest jump in the current data series going back to 2007, it is still well below the 7.9% CPI rate meaning that inflation adjusted wages continue to decline.

Yes income earners are getting poorer on a weekly basis…or you could argue everyone is getting poorer including the retired.

If asset prices fall and we remain in negative real rate environment, it’s widespread financial repression…we then might get action as both asset owners and non-asset owners will be taking the hit.

"we then might get action"

What "action" are you referring to?

Central bank response

That's extremely vague IO, could you be more specific, i.e. Central Back response to….

- increase the OCR at a much faster rate?

- start a fresh round of money printing and lowering the OCR?

- another response you are thinking of?

Central blank response ! ... the financial world would be in a better place if they did nothing ... no more flooding the markets with more $ Trillions .... the party is over .... we're engorged with wildly overpriced houses , NFT's , cryptocurrencies ...

Time for the fat man in the Monty Python restuarant to explode .... we can't take any more $ Trillions ... we're stuffed .... bugger off ...

The damage has already been done and can’t be undone without consequences

So… again, what type of central bank response are you alluding to IO ?

That’s not always true. I’m an income earner, about half our costs are fixed (fixed mortgage repayment) so a 7.9% rise in CPI only increases our total expenses by about 4%.

-

But you’re still 4% worse off in buying food, fuel, rates, insurance…so still experiencing hardship relative to not having negative real rates.

Not if I get a 5.6% pay rise.

Good for you 👍

btw - don’t mistake your personal circumstances with the economy as a whole. And it’s what is happening to the whole economy that is important, not Jimbos pay rise.

And oil prices are down another -US$3.50 to just on US$99/bbl in the US. And the international Brent price is now just over US$104/bbl.

Magic. Go for a little drive to celebrate? Unfortunately the effect will be temporary, we need to drill now to defeat Russia and their OPEC friends though.

Click on the link: "And other nations are following suit" and read it

When China’s economy starts to fail significantly, I wonder how long it will be before their corrupt dictatorship lashes out militarily to deflect attention from their woeful domestic management. COVID, their second-rate vaccines and their draconian response could act as a catalyst for this.

NZ needs to distance itself from China and start renewing friendships with powerful like-minded democracies across the world. We need to get real and stop feeding the beast.

A huge increase in military spending would be a good start.

You happy to fund this via tax increases Timmy?

"A huge increase in military spending would be a good start. "

Yes

I agree with your post Timmy, except for the "huge increase in NZ military funding". No matter how "huge" this increase would be, it would be negligible vs an aggressor

That’s the point. NZ on its own, couldn’t defend itself. This was known in the early 20th century, a few port forts, the supposed “Russian Threat” thus the celebrated disappearing guns etc. So NZ bought into some safeguards. Hence state of the art of the day, purchase of battle cruiser HMS New Zealand, which carried the flag at Jutland & is reputed to have expended there, more ammunition than any other Royal Navy warship. Today’s equivalent then would be the purchase of an American nuke sub, utilising the purpose built bases Australia will have.

How could we finance and maintain a nuclear sub with the requisite onshore facilities? We struggle to build roads.

Not like you to read incompletely. Read my last sentence. And you may have missed the other point. HMS New Zealand was not based in NZ. The purpose of that investment then was, for want of a better word, solidarity with where military protection could be expected to come from.

Submarine lease costs similar to the arrangement India has with Russia are still beyond our capacity to fund, without cut backs to necessary local infrastructure.

HMS New Zealand was one of three Indefatigable-class battlecruisers built for the defence of the British Empire. Launched in 1911, the ship was funded by the government of New Zealand as a gift to Britain,[1] and she was commissioned into the Royal Navy in 1912. She had been intended for the China Station, but was released by the New Zealand government at the request of the Admiralty for service in British waters.

Military gifts to Australia would find little support in NZ.

Furthermore, nobody is going to attack China or Russia or both (nuclear superpowers) in the Pacific.

My point was not a suggestion. Simply a comparison as to what the equivalent measure would be today, if to engage the same defence strategy.

NZ cannot afford a decent sized military ... our best defence is a hedge of native shrubs and tussocks planted around the coastline ...

Foxglove, NZ has a very public non-nuclear stance. Have you forgotten about the friction caused by not letting foreign nuclear ships into NZ's waters.

As explained to adx, it was not a suggestion.

My Chinese friend says that the West certainly doesn't have to worry about the Chinese armed forces. They only exist so they can enrich themselves off corrupt practices. He reckoned they wouldn't be able to organise feeding a large force assembled to invade Taiwan, let alone actually do it. Their Tibet campaign was when they had a proper ruthless army, under Mao, who understood such things.

I have to agree here, having known some Chinese military people. Corruption all the way up the tree and nobody in government can fix it because you don't mess with the military in China except to give them more toys. One guy I knew "operated a military business" and was like the western equivalent of a major. He hid the "business" from us for years until we happened to go into his office once - was about 20 computers sitting around which had never been used looking like a troll farm except they weren't really set up to run (all except about 3 of them didn't even have cables to plug in the monitors!). Heard he had roped some people in, dressed them up, logged on some computers and took pictures of his "operation" to show to higher ups. Got paid a hell of a lot of money for buying all the equipment and doing nothing with it. Even had personal body guards, drivers and security personnel on call. I reckon he didn't actually do anything, I always saw him out drinking, at restaurants, playing games on his phone or at the golf course. Another couple of guys were clearly intelligence ops (perfect Australian and English accents) who spent almost all their time out cycling but claimed to work as teachers.

Apart from the tip of the sword, the Chinese military services appear to be a pretty motley bunch of fat, ineffective "soldiers" who don't regularly do things like practice/train or keep fit. But the tip of their sword is probably 50-100k troops that are as good as most you would find in the West, so I wouldn't underestimate them.

A hapless state of affairs that has been similarly recorded for centuries. The Good Soldier Cvejk, in other words. The Duke of Wellington had General Sir William Erskine dumped on him, who was entirely insane and squandered lives by the hundreds. There was a scandal exposed in the USA when we lived there. The Pentagon thought it a good idea to issue credit cards to the thousands of transferees, ie base to base etc, to cover expenses. It took months before they realised how that had exploded. Hookers, vehicles, 5star hotels/ restaurants, new clothes. One soldier was awol, located in Hawaii all expenses paid for two months. But my favourite is Spike Milligan in camp prior to embarking for Nth Africa, when in the mess tent for lunch he worked out they might be in a bit of trouble. Menu was, boiled potatoes, boiled cabbage, boiled peas, boiled sausages. The Medical Officer strolled between tables and asked “any complaints?” One soldier, “yes sir, please sir, me sir, I’ve got piles!” Says the MO, “that’s bloody strange, everyone else has got sausages.”

The CCP is a basket case and their economy is going backwards.

Could have been so different…

Nzs reliance on selling milk powder is the equivalent of Germany's reliance on Russian gas . It was interesting to note Russian disgust at an oil depot over the border being hit presumably by Ukrainian helicopters , as though this is a war crime or something how dare the Ukrainians go over the border . Meanwhile they bomb Ukrainian cities huh shame they can't reach Moscow.

You can't distance yourself from your biggest trading partner without inflicting some serious harm on your own economy. Distancing from China will not happen in the short term before NZ has looked elsewhere in the world to sell their products.

Globally, hiring is strong, especially in the West. But American bond markets are toying with inverted yield curves, even if it is with little conviction at this stage. Inverted yield curves suggest recession is ahead. But few but perma-bears really believe that, and the IMF doesn't. Expanding factories and strong demand for labour aren't usual signals for recession. Perhaps the supply chain realignments are helping here and that effect won't be temporary.

This FRED graph effectively illustrates that every recession since 1957 has been preceded by a yield curve inversion. (Note that the lag between the inversion and a recession varies: With the 10-year and 1-year yields, the lag is between 8 and 19 months, with an average of about 13 months.)

Is this the bond markets listening to the Fed talk about a series of hikes, and saying, "Nah, we just don't see it"?

My read is that when the disruption settles during 2022 we will be back on the 'tending to zero' interest rate trend we have been on for 10+ years - but with a one-off adjustment to the cost of living that reflects a bit of de-globalisation.

Interesting how the bond markets didn’t foretell the inflation we currently have, yet we rely upon them to foretell an expected deflationary recession in the near future.

Do you find this strange?

Are you possibly confusing supply chain disruptions with monetary inflation which bond yields reflect?

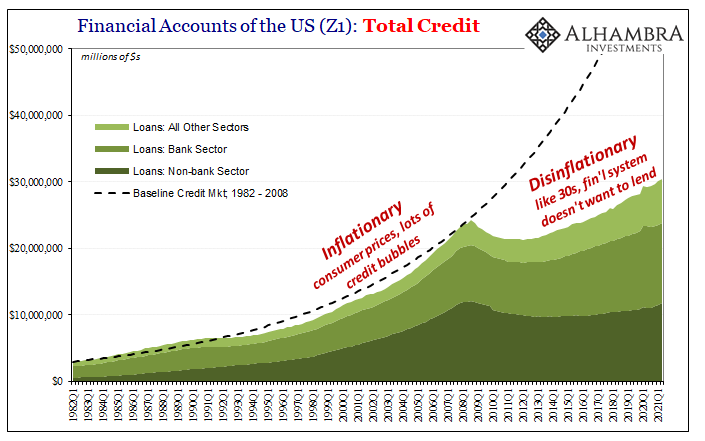

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

My theory is that everyone is confused at this point in time….and the attempt to seek clarity is difficult.

Do you mean in the above that the YC inversions indicate that monetary inflation will reduce in the near future and that markets are calling the Feds bluff? That they won’t intervene by raising rates or that if they do raise rates that they quickly change course and resume QE?

Is the horse leading the cart or perhaps are the horse and cart now detached?

There is no monetary inflation and banks are buying sovereign debt in preference to extending credit to productive enterprises.

{kind=link}

Could banks be buying sovereign debt because that is all they can to increase the return on the balances in their reserve accounts? I would rather have a yield of 2% than a yield of 1%.

Banks are more interested in the return of their money than the return on it. Furthermore:

Nobody buys securities; they borrow and claim to “own.” Repo. The hedge fund (client) says it wants to own XYZ US Treasury issue, puts up a minimal upfront investment, enough to cover some overcollateralization requirement, and borrows for the rest of the purchase price. In many instances, the broker is the lender as well as custodian.

To make this securities funding transaction as cheap as possible, the client will agree to allow the dealer to re-pledge or rehypothecate (for our purposes here, the language is interchangeable though in a legal and regulatory sense these terms can have different meanings) the very security the client is claiming to own.

What that means is the dealer acts as an intermediary rather than lending its own cash for the purposes of the client owning this particular security. Instead, the dealer will repledge that security in the repo market or to other dealers in order to borrow the cash ultimately used to “purchase” and then fund the transaction (rolling over) to its ultimate end. Not just a securities financing transaction, a whole series of them.

And this series becomes horizontal as well vertical; the already re-pledged security posted by the client’s dealer to the next dealer in line can be re-pledged again depending upon the conditions set forth between the client’s dealer and what is now the client’s dealer’s dealer. As you may already guess, the client’s dealer’s dealer may also be able to re-pledge – the same security – to its dealer; specifically, the client’s dealer’s dealer’s dealer.

In many if not most cases, there needn’t be the original client need for this chain of re-pledging, either. What I mean is, the first link in that chain doesn’t have to originate out of the client’s need to borrow directly; if permissible, the client’s dealer may re-pledge the client’s security(ies) for its own purposes, with the client being sufficiently incentivized.

Thus, a dealer who does this kind of business with many financial clients can build up a stash of usable collateral that it doesn’t exactly own; these securities belong to other firms and vehicles, but are more than useful for the dealer to fund and carry out its dealer activities as a whole because of these peculiar usage rights.

The permissibility of these kinds of doings is, and remains, much higher in the offshore domain (the non-harmonized part of these rehypothecation regimes). The more a dealer could do re-pledging for themselves, the better terms it would offer its customers; giving Lehman Brothers International Europe a serious leg up on Lehman Brothers Inc.

Net result, Lehman Brothers as a global firm had acquired a significant pool of collateral owned by its customers and custodied at Lehman Brothers International Europe which underlay a whole range of dealer activities carried out by Lehman Brothers Inc., including securities financing transactions in its own proprietary book as well as a creating a margin collateral cushion for a whole host of derivative transactions and potential counterclaims.

So, what happens when customers start to feel a little uncertain about these arrangements? Quite naturally, they may begin to wonder about what their exposure might be given how their securities are in London. In fact, this, not subprime mortgages, is what led to Lehman’s end.

Hedge funds and dealers as Lehman clients scrambled to change these prime brokerage agreements limiting Lehman Brothers Inc. from being able to transfer assets into Lehman Brothers International Europe, or demanding they be transferred back, having the effect of stripping Lehman of a huge chunk of what had been available collateral by which to supply its global operations.

The rest was typical, traditional bank run stuff; rumors of Lehman being shaky led to the initial customer collateral “run” which then made Lehman shakier leading to more customers running in and changing their brokerage language. Soon enough, bye bye Lehman.

It was a run, but it wasn’t like one Walter Bagehot or Benjamin Strong would’ve recognized. It sure hadn’t been something Ben Bernanke or any of his kind considered too important, either. The latter group, contemporary central bankers, focused instead on the level of bank reserves, even as the federal funds effective rate had plummeted and been undershooting for a year by then.

Better than cash.

My cynical view is that bond markets just tell us (a) what traders think that the Fed is actually going to have to do, and (b) what traders think other traders are going to do. Meanwhile the Fed looks to the bond markets for signals on what it should do. Bank of Japan lost patience with the charade and have simply taken over. ECB have dallied with doing the same.

Central banks follow markets.

Except when they don't.

International eurodollar banks beyond the jurisdiction of any central bank edict can overwhelm the Federal Reserve.

An operational segment as an example"

FX swaps and forwards: missing global debt?

The outstanding amounts of FX swaps/forwards and currency swaps stood at $58 trillion at end-December 2016 (Graph 1, left-hand panel). For perspective, this figure approaches that of world GDP ($75 trillion), exceeds that of global portfolio stocks ($44 trillion) or international bank claims ($32 trillion), and is almost triple the value of global trade ($21 trillion).

The outstanding amount has quadrupled since the early 2000s but has grown unevenly (Graph 1, left-hand panel). After tripling in the five years to 2007, it fell back sharply during the GFC, even more than international bank credit. This most likely reflected a reduction in hedging needs, as both trade and asset prices collapsed.

Dollar funding costs during the Covid-19 crisis through the lens of the FX swap market

Demand for dollars via FX swaps

Aggregate data on the use FX swaps and FX forwards can be obtained from the BIS derivatives statistics.2 The BIS OTC derivatives data (OTC data) show that the total amount outstanding at end-June 2019 neared $86 trillion (Graph 2, first panel), with FX swaps accounting for an estimated three quarters of this total.

Thanks, I'll have a proper read. The layer upon layer of derivatives, promises to pay, promises to buy, leveraging etc is complete madness. What's it all actually for?

Trading room profits and losses, trade finance and hedging.

There Are No Petrodollars, Plus the Focus Misses the Point

The fact that the very idea of the petrodollar keeps going to this day is instead a poignant if inadvertent acknowledgement of the limited monetary literacy provided by the dastardly discipline of statistics-obsessed Economics. We’ve all been left in the dark, and it began that way all the way back decades ago with the very people tasked with being “our” monetary stewards.

The German economic miracle no longer exists

The nightmare scenario for German conservatives is unfolding before their eyes

.... Angela Merkel astonished me ... how she shut down German nuclear power plants in reaction to the Fukushima disaster ... how she threw Germany into a huge gas deal with Russia ... implicitly trusting Putin to be a good guy , to be trustworthy .... how she opened the doors and took in 800 000 Syrian refugees ...

How did she remain so beloved by the German people , in the face of so many blunders ( asking on behalf of Jacinda Ardern ) ....

Maybe it has been the very strong economic performance?

Donald Trump sent her a small white flag , after she signed the natural gas deal with Putin ... great sense of humour , the Don ... and perceptive ...

Maybe Vlad should give her a call. Old friends in need, are old friends indeed.Get some tips. After all the Wehrmacht, Operation Barbarossa, from far greater distance logistically, dependent mostly on horse drawn transport, got through the most part of Ukraine in a matter of weeks, and then repeated the exercise in the second spring offensive.

... I do recall , as a kid , the awesome " World at War " documentaries ... all in B&W ... narrated by Lawrence Olivier ... perhaps , it ought to be compulsory viewing in schools ..

Those who forget their history .... .... repeat it !

I suppose, as a western democratic nation, we in NZ have to be very happy with the economic developments in 2022, the atrocities of the war aside of course. It seems to me that, this year, the democratic west has shown tremendous unity and strength, and it looks as if the rising power that China (and that Russia would like to be) is failing at the expense of a stronger USA.

Thoughts anyone?

Yes, and that stronger USA was set in motion by the last Administration whose focus was to alert the world to who the CCP really is, and why is the US building up an Adversary who steals every bit of Intellectual Property they can get their hands on, and then turning to Europe and forcing European nations spend more to support NATO ,rather than relying on the free lunch provided by the US over several decades. Trump had Neo liberals on the run, and the focus turned to building up America once again with unemployment amongst every minority group at its lowest level in over 50 years Domestic Security was enhanced by working out with the Mexican President a rational program to stem the floor of "que jumpers" at the Southern Border, and actually take time to vet Asylum Seekers-who once let in are on a free ride with the American taxpayers providing most of their income. Even Hispanic Voters supported this policy with Trump growing the Hispanic vote compared to four years earlier. No doubt the man was an ass (like Clinton's in private), but Trump got things done for the people who elected him. Biden is back to the Globalist neo con agenda and floating on the benefits created by the last Administration. When the effects of the $3 Trillion of free money handed out over the past 24 months wears off watch out. As an example my wife and I each received NZ$6000-or $12,000 for a retired couple. That across 200,000,000 adults creates a lot of new spending as many of those were not suffering from job losses, and the bottom 20% had cash to spend like they never had in their lives.

Yes Trump may have done all that TommyYank, but mostly he is a narcissistic, self-interested, race-baiting, climate change denying, pollution promoting, dishonest “alleged” rapist.

The thought of him being in charge during these times fills me with dread.

Trump was also a massive Putin fan boy and enjoyed Putin’s online troll factory influencing the US election in Trump’s favour.

Perhaps your not familiar with the work the Special Consul Durham has produced to puts the Russian Collusion to bed and lays it totally at the doorstep of the Clintons. Charming People.

My debt is devaluing nicely. Thanks, GR and JA.

So are incomes.

My debt is devaluing nicely. Thanks, GR and JA.

Is it? It will only be "inflating away" if your income is tracking inflation. And remember, the "real inflation" is not what they tell you in the media and a representation of the CPI.

Or perhaps you're in Japan. If you're being paid in JPY, the value of your purchasing power in NZD is down 8% over the past 12 months.

During the last bubble meltdown, banks like Lloyds were hawking yen-dominated loans to expats to speculate on housing in the English speaking nations. When the yen strengthened on repatriation flows, many of the punters took at a bath as their property rents were unable to match the value of the yen required to pay back the banks.

Caveat emptor.

Well said NKTokyo, inflation at 7% with interest rates at 2.5-3% For some reason, few people get it, or maybe they just don't like others doing well?

Someone's not getting it. The only type of inflation which erodes debt is monetary inflation, and that's not what's being tracked by the CPI.

Agreed, someone's not getting it. It is price inflation, i.e. things getting more expensive and increasing incomes which erodes debt, not monetary inflation which is an increase in the amount of money available.

BTW, monetary inflation leads to price inflation, you like to separate these as if they were not linked, but that's not the case in my view

BTW, monetary inflation leads to price inflation, you like to separate these as if they were not linked, but that's not the case in my view

Inflation is the changes in price levels of both consumer goods and services; changes in asset prices: and of course changes in the broad money supply.

Ultimately the debasement of purchasing power through monetary debasement is the most damaging.

Simple as that really.

The amount of debt you owe does not change with the price of cauliflower. It changes with the value of the currency in which your debt is denominated. That is monetary inflation.

It is separate and distinct from price inflation. Monetary inflation contributes to price inflation, but so do a million other things. You can not look at the price of cauliflower going up, and assume your debt is decreasing by the same amount.

Thanks for your reply chebbo, i believe we're doing semantics at this stage

It's worth reading Zoltan Poszar on the four 'prices' of money, and his latest epistle. He takes the concept from Perry Mehrling, and the last of the four - commodities - has an intense physical focus apart from the commodity involved: the shipping and the protection needed thereby. With longer shipping routes for key commodities due to sanctions, there is a large financing and insurance implication.......

Izabella Kaminska has a good and relatively accessible gloss on Poszar's latest.

... is it just me , or did Grant Dalton flip us the middle finger ... after removing the defence of the Americas Cup yacht race from Orc Land , to Barcelona ?

Via the government , us Kiwi taxpayers made you rich , pal ... is this how you repay us ...

We let him get away with it.

Same happened with Rugby World Cup costs - rate payers still financing stadiums, while some far off central group in the UK collared the TV rights.

... I'm not a " yachtie " myself .... but the focus the event gave to us as a nation , and Orc Land as a high tech yacht manufacturing base , was priceless ...

" Team NZ " my fat gummy arse , pull the other one Dalton , it's got barnacles on it ...

The government has no business funding big sports enterprises. It's just the smart guys pulling political strings. An cost to the hapless taxpayer.

Dalton is the worst example.

...d/p

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.