By Roger J Kerr

The development of a two-tier interest rate market in New Zealand (highlighted in last week’s column), where official wholesale interest rates like the OCR and BKBM are much lower than the real price of money (i.e. interest rates) actually transacted between borrowers and lenders, took a further step forward last week.

The response by the banks to a 0.25% cut in the OCR to 2.00% was to increase their retail deposit rates paid to investors to ensure they have sufficient funding on their books to meet the ever increasing lending demand by home mortgage borrowers.

Major banks have lifted their 18 month deposit interest rates to 3.60% and 3.65%, a large 1.60% premium over the 2.00% wholesale swap interest rates.

No wonder commercial/industrial property investment is booming and associated funding syndicates proliferating as they offer yield returns well above the very low yields now offered on bank deposits.

Dividend stocks are also in hot demand judging by the still rampant NZ sharemarket. One hopes that these rent seeking investors are aware of the severe liquidity constraints of smaller property syndicates and the general market risk (usually from offshore) of investing in equities.

Greed and fear always drive markets.

That is why we have some cash/fixed interest investors prepared to take higher liquidity and market risks to get a yield return they want or need.

On the other hand all the printed money sloshing around the world is being invested by another group of investors in safe Government bonds at nil or near to zero return yields as they are fearful of sharemarket shocks, China, geo-political risks and the collapse of the western economies as we know them! Such divergence of opinion about the future is what all markets tick and may provide opportunities for astute cash and fixed interest investors who classify themselves in between the two aforementioned extremes.

A two-tier interest rate market does impact on the effectiveness of monetary policy, as does inconsistent messaging from the central bank. Back in June the RBNZ provided a scenario whereby if the NZ TWI currency index stayed high above 72, interest rates would eventually have the fall to 1.00% to generate inflation between 1% and 3%. Last week that scenario was seemingly completely forgotten about as the TWI soared above 76 and now the RBNZ are not expecting interest rates to go much below 2.00%! Not a lot has changed in the economy between June and September to cause such a major shift in outlook

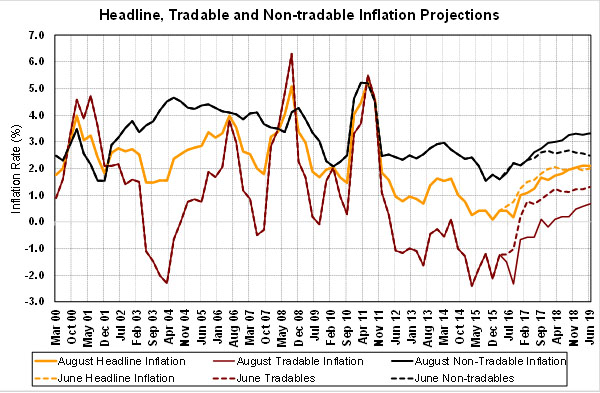

What has changed is the RBNZ’s revision upwards in non-tradable inflation in 2017 and 2018. That seems a fairly heroic assumption when non-tradable inflation is fairly static with no wages pressures.

The higher than expected exchange rate justifies the RBNZ lowering their tradable inflation (imported goods) forecasts from June to August.

However, it is hard to see the lower interest rates somehow generating the much higher non-tradable (domestic prices) inflation they are now forecasting (refer chart below).

Daily swap rates

Select chart tabs

Roger J Kerr contracts to PwC in the treasury advisory area. He specialises in fixed interest securities and is a commentator on economics and markets. More commentary and useful information on fixed interest investing can be found at rogeradvice.com

2 Comments

would be interested to see how much is heading over to peer to peer lending, is this the new finance companies for returns and high risk

Roger,

I wouldn't touch these property syndicates. I am happy to have my commercial property exposure through the quoted property trusts. As a long time equity investor with an absolute focus on dividends, I am well aware that the NZ market is trading on a multiple above its long-term average and I am comfortable with that, in a low interest rate environment. I am convinced that this is structural for a variety of reasons, but as a cautious Scot, I am keeping a fair amount in cash,irrespective of low returns. When there is a significant correction, as will no doubt happen at some point, I want to be able to take advantage of it.

I have put a toe in the P2P market and so far, I am happy with a net return of 9.90% on my portfolio of A grade loans.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.