Bank of New Zealand (BNZ) has made a net profit of $1.506 billion for the 12 months to 30 September 2024, down $3 million on the prior financial year's record profit.

BNZ said the profit was driven by lending and deposit growth partially offset by lower net interest margins, higher operating expenses and includes the impact of the sale of BNZ’s wealth business.

BNZ chief executive Dan Huggins says this is "a solid result in challenging conditions", which reflects BNZ’s continued growth as more New Zealanders choose to bank with BNZ. According to information provided by BNZ's parent bank National Australia Bank (NAB), BNZ had "strong customer growth with ~100k customers onboarded in the last 12 months".

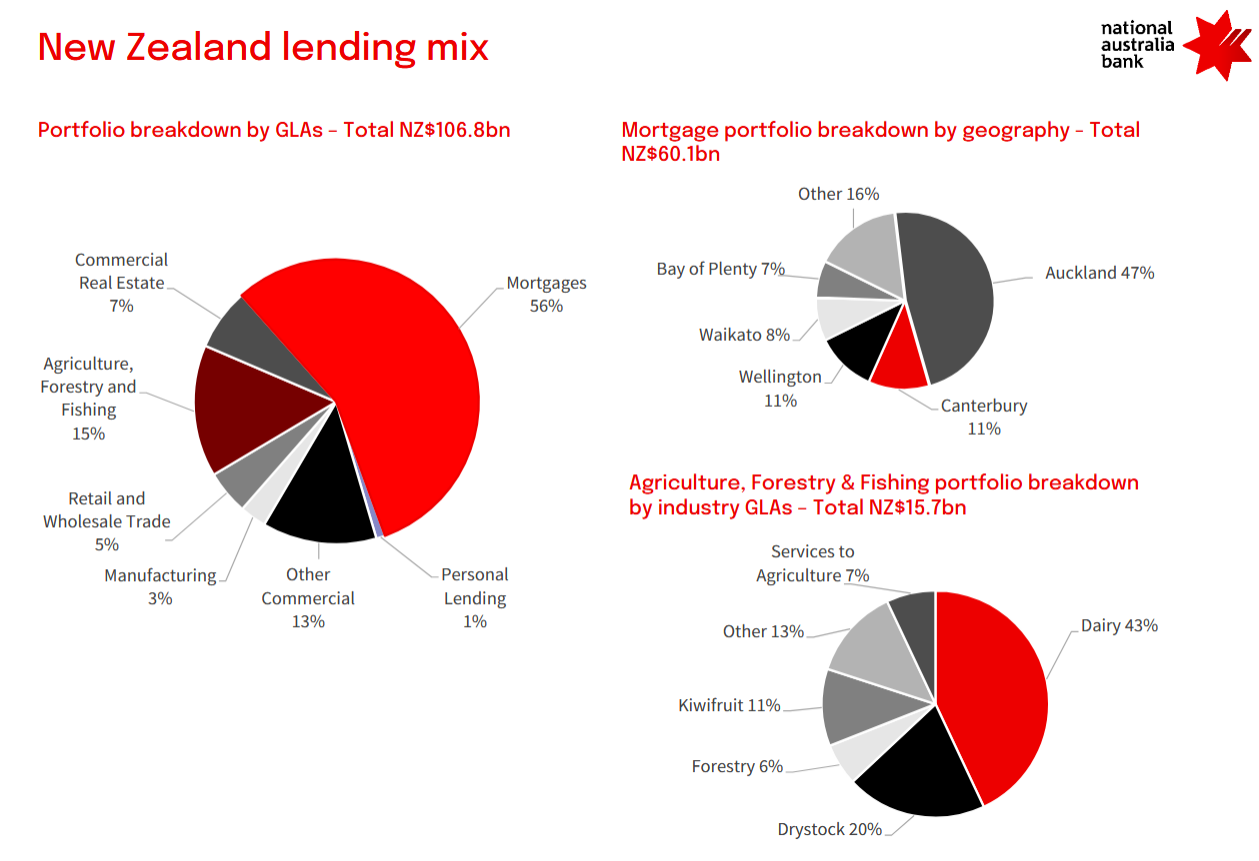

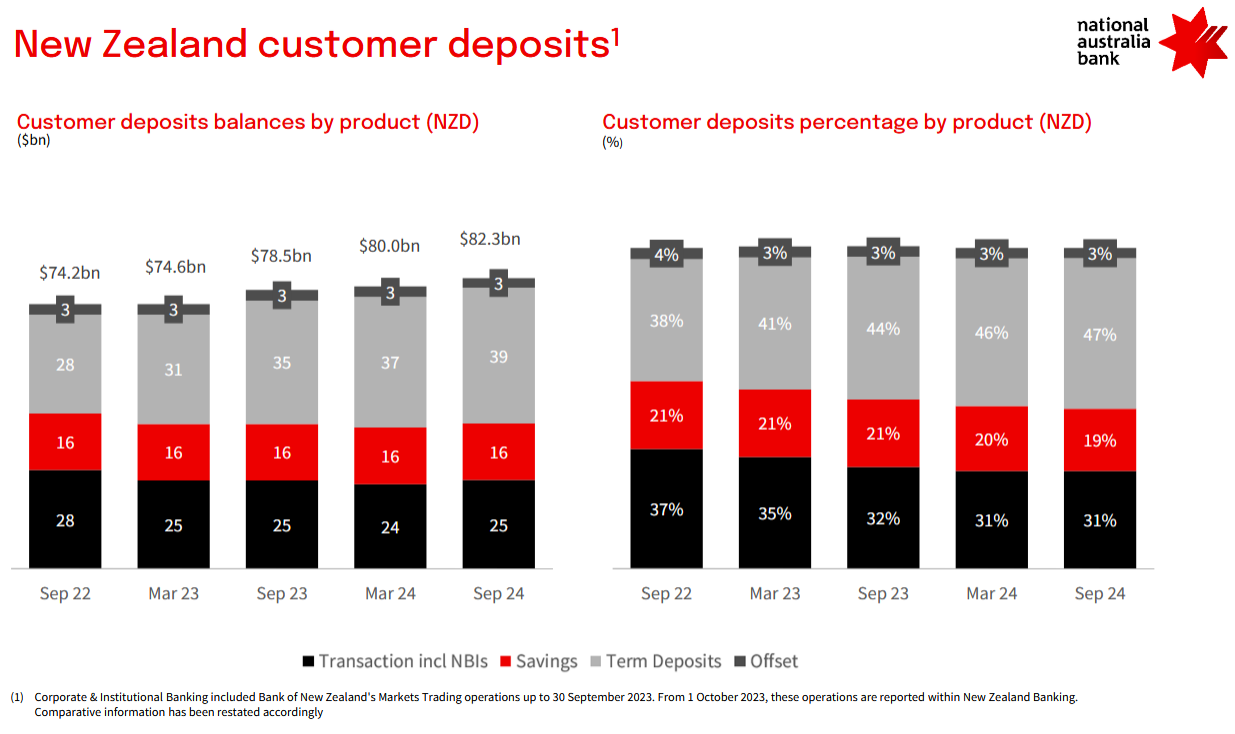

BNZ’s total lending increased $4.3 billion or 4.2%, with business lending up $2.0 billion or 4.6% and home lending up $2.4 billion or 4.1%. Total customer deposits increased by $3.8 billion or 4.8%.

Huggins says BNZ continues to support its customers through one of the most difficult economic cycles in recent history.

“With inflation back within the Reserve Bank’s target band and as interest rates begin to fall, this will be welcome news for many households and businesses.

“However, there is always a lag between changes in monetary policy and its impact on the economy, and it will take some time for the benefits to flow through. For customers feeling under pressure our message is get in touch,” says Huggins.

The bank's net interest margin fell to 2.37% from 2.40% last year, while the cost to income ratio rose to 38.5% from 34.9%.

BNZ paid its parent National Australia Bank (NAB) $1.305 billion in dividends this year, up from $869 million in 2023 and $560 million in 2022.

Also on Thursday, NAB reported a cash profit of A$7.102 billion for the year to September, down 8.1% on the prior year's performance. Its full dividend for the year was A$1.69 up from $1.67. NAB's common equity tier one capital ratio at September 30 was 12.35%, up from 12.22% a year ago. Its net interest margin was 1.71% down from 1.74% a year ago.

Figures released by NAB put BNZ's housing lending market share at 16.7% at September 30, up from 16.6% a year earlier. Its agricultural lending market share was 21.6% versus 21.5%, its business lending was up to 22.9% from 22.4%, and its share of deposits up to 18.3% from 18.1%.

Businesses will be crucial

Huggins says businesses will be crucial to driving the economic growth that will help power the economic recovery.

In the year BNZ says it was the largest lender to New Zealand’s productive sector, with almost half of New Zealand’s total business and agri lending growth coming from BNZ.

"As New Zealand’s largest business bank, we’re proud that we have backed our business customers through the economic cycle with an understanding that while times are tough now, there will be opportunities for growth ahead."

Huggins said in addition to supporting businesses, BNZ has continued to back customers’ ambitions to buy their first or next home.

"Over the past 12 months, more than 6,500 New Zealanders have chosen BNZ to help them into property ownership, with first home buyers representing around half of that figure.

"For our existing home loan customers, we have been focused on helping them manage in the current higher interest rate environment.

"Customers are paying close attention to interest rates, and we’ve seen a significant shift towards shorter fixed term loans. Over 70% of our home loan customers are due to roll off their fixed term loans within the next 12 months."

According to NAB, BNZ's home loan loss rate was running at 0.00% at the end of its September financial year, unchanged year-on-year. Its 90+ day past due home loan rate was 0.20% versus 0.24% at March 31, and 0.17% at September 30 last year. BNZ's impaired home loan rate was 0.12% versus 0.09% at March 31 and 0.02% on September 30 last year.

Housing lending as a percentage of BNZ's total lending stood at 56% at September 30, unchanged from a year earlier.

Unlocking home ownership

BNZ says it has also focused on unlocking home ownership on Māori land. This year BNZ launched and then expanded its funding model that enables iwi, as well as individuals and whānau in Māori land trusts and incorporations, to secure home loans for housing on Māori land at standard home loan interest rates.

"We’re proud that we’ve managed to develop a solution that can not only enable home ownership on whenua Māori, but also acknowledges and protects the deep connection Māori have with their whenua," says Mr Huggins.

With more than 250,000 customers already benefitting from BNZ’s application programming interface (API) technology, BNZ has reinforced its market leading position in open banking, Huggins said.

This year, BNZ was the first New Zealand bank to deliver on all industry API milestones required to enable open banking in New Zealand.

Huggins said BNZ recently announced it is backing Payap, an easy-to-use digital wallet and point of sale/e- commerce app powered by open banking and developed by Centrapay.

BNZ also announced it has bought fintech BlinkPay. BlinkPay offers payment services which save customers time and money. BNZ’s investment will help accelerate BlinkPay’s development of new products and services powered by open banking to improve outcomes for consumers across Aotearoa New Zealand, the bank says.

“These initiatives support industry competition and demonstrate BNZ’s significant investment and commitment to accelerating open banking as we continually strive to make banking simpler and easier for all of our customers,” Huggins said.

BNZ's full media release is here.

4 Comments

Data from Stats NZ shows interest payments increased 117 percent in the three years to September. Over the same period, inflation as measured by the consumer price index (CPI) increased 15.7 percent.

Source: Debt servicing to stay hard unless house prices come down - economist

What is the BNZ doing wrong, ay? (I'm yet to drill into the numbers)

Hmm ... "net interest margin fell to 2.37% from 2.40% last year"? Overseas banks in competitive environments would kill to have such margin!

edit: ah hah! "BNZ paid its parent National Australia Bank (NAB) $1.305 billion in dividends this year, up from $869 million in 2023 and $560 million in 2022." Accounting hijinks? ... And into the books I go ...

"BNZ paid its parent National Australia Bank (NAB) $1.305 billion in dividends this year" Puts the proof to the lie Antonia Watson sold to the banking inquiry.

I hope they harness this proof of the waffle that's been said and actually use it act on the banks.

Antonia Watson is ANZ.

Was she speaking for the whole of the NZ banking industry (or pretending to), or was she speaking just for ANZ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.