ANZ New Zealand has a group of borrowers who bought homes when house prices were especially elevated in 2020 and 2021 "under heightened alert," as past due loans and the volume of borrowers in negative equity creep higher, CEO Antonia Watson says.

In last Wednesday's Financial Stability Report the Reserve Bank said 25% of outstanding mortgages were taken out between late 2020 and late 2021 when house prices were high and interest rates low. As of March this year, Reserve Bank figures show $347 billion worth of home loans. Thus a quarter of that is a bit less than $87 billion worth.

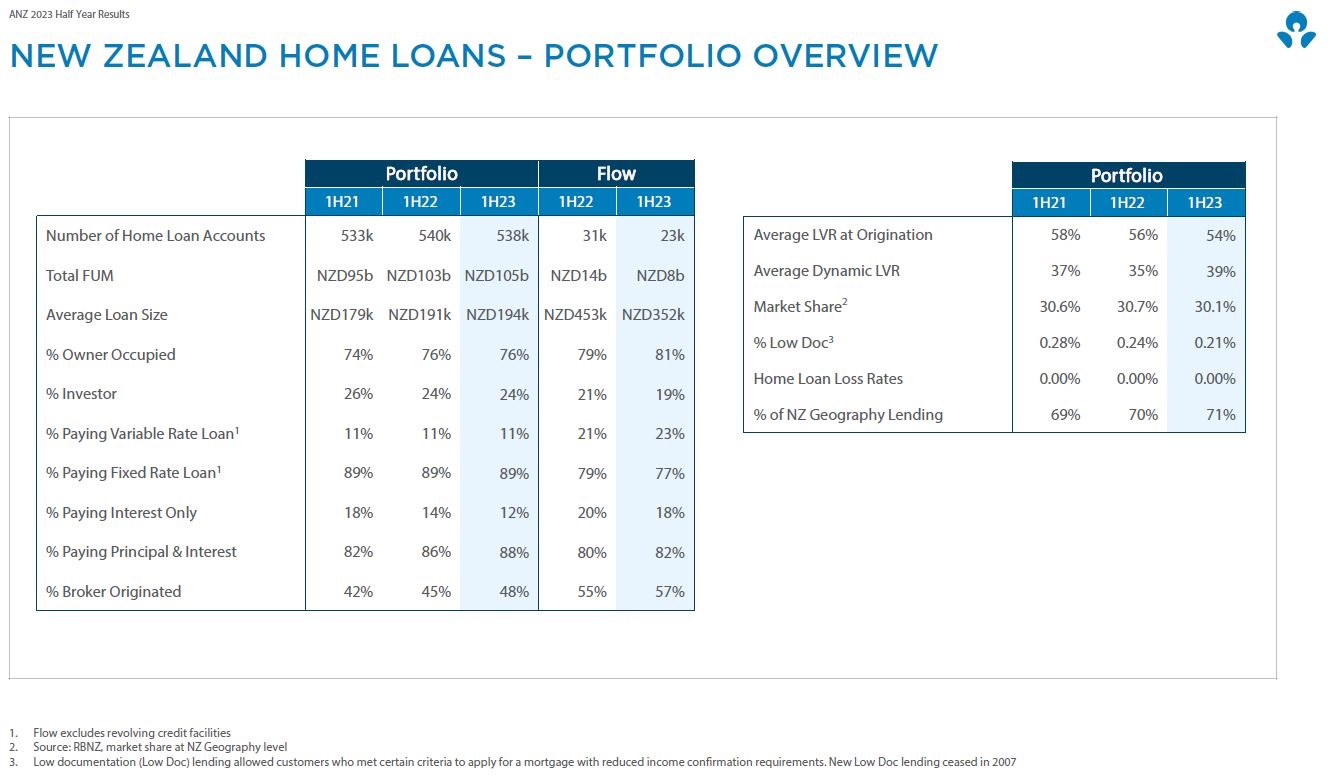

The Reserve Bank also confirmed that 25% of loans stress tested by banks in 2020-21 are now above their stress testing limits. Banks use test rates to assess would-be borrowers’ capacity to meet repayment requirements if interest rates rise. ANZ NZ is NZ's biggest home lender with a $105 billion home loan portfolio.

Speaking to interest.co.nz after ANZ NZ released its interim financial results on Friday, Watson said the 25% figure for borrowers stress tested in 2020-21 was "probably about right" for ANZ NZ's home loan portfolio.

"Not forgetting that our affordability tests tend to be on the conservative side. So yes, there are some people paying more now than they were tested at. They've probably also had a pay rise don't forget," says Watson. "People have had pay rises and people have still got jobs. So all of that really sits on the positive side."

"The cohort of people who bought at the peak of the market and who might be in negative equity, we're definitely seeing an increase in the proportion of our book in negative equity. But it's still small. It's 2% or something like that," Watson says.

"Obviously if you've still got a job and you can service the loan it becomes not so relevant. So employment is really important here."

Unemployment remains low, with the latest Statistics NZ figures putting it at 3.4%. Nonetheless Watson says ANZ NZ is keeping a close eye on borrowers who bought homes in 2020-2021 and whose mortgage rate may now be higher than the rate they were tested on.

"That particular cohort we've got them under heightened alert, making sure that we're looking for the watch points, contacting people proactively if they look like they're in trouble. And if anyone feels like they're getting in a bit of trouble the best thing to do is come and see us as early as possible," says Watson.

Negative equity is when a house price falls in value to the extent where the owner owes more on their home loan than what the house is valued at. The NZ median house price peaked at $925,000 in November 2021, according to the Real Estate Institute of New Zealand, and had dropped $150,000, or 16%, to $775,000 in the latest figures, for March this year.

And since October 2021 the Reserve Bank has increased the Official Cash Rate by 500 basis points to 5.25%, with the average carded, or advertised, two-year bank mortgage rate rising to 6.491% from 2.715%.

"We've got 45 basis points [of loans] at 90+ days past due. That's back just a squeak above where we were pre-Covid, which was still historically low. We're absolutely expecting that number to rise," says Watson.

"But customers have put themselves in pretty good positions overall...About two-thirds of customers have moved onto higher rates with about a third left, and of them 40% don't move onto a higher rate until next year or afterwards. People have been paying down their debt because when interest rates went down they didn't readjust their home loan repayment. So that put them in a better position. Our average rate across our portfolio at the moment is 4.46%."

After a credit impairment charge of $121 million in its interim results, ANZ NZ's total credit impairment provisions increased to $860 million.

Shayne Elliott, CEO of ANZ NZ's parent the ANZ Banking Group, says the provisions set aside for potential losses in NZ are now "higher than at any time in our history." Elliott notes, however, that NZ past due loans from retail customers are at levels still substantially lower than Australia.

'They're so much a last resort I wouldn't even want to talk about them at the moment'

At the start of last week there were 38 properties being advertised as residential mortgagee sales nationwide. During 2009, during the Global Financial Crisis, there were 3,024 mortgagee sales. Interest.co.nz asked Watson whether mortgagee sales could make a come back.

"Mortgagee sales, look they're so much a last resort I wouldn't even want to talk about them at the moment."

"What we want to encourage customers to do now is come and see us without any fear that they're going to lose their home because there are so many options we have before that happens," Watson says.

We asked Watson to elaborate on these options.

"Term out the loan. So if you were sitting on 15 years to go, term it out to 20 years so you reduce the repayments. Go to interest-only. We do some stress testing on our [loan] book that says [for example], 'if interest rates go up to 7.5% what percent of our book would need to go to interest only and they'd still be fine.' So that's a big buffer for people."

"Loan repayment holidays are sometimes suitable, we did them on mass at the beginning of Covid. That was suitable for a low interest rate environment. We'd never want to do them on mass now, but it's absolutely an option, especially to tide people over just for a little while well they're getting back on their feet again say, or if they've had an unexpected expense which we sometimes see," says Watson.

Another option is working with the customer on their overall financial position and options they might have. Or customers might proactively decide their current loan, in terms of the value of the house they've got, isn't feasible and decide to downsize to another home. And people with investment portfolios can reduce their debt by selling a property.

"There's all sorts of different options out there on the table which is why discussing it with someone is really helpful," says Watson.

'Short and shallow' recession seen

Meanwhile, Elliott says a "short and shallow" recession is "looking probable" in NZ.

"We're well placed to assist customers and manage stress given the strength of our franchise, our balance sheet and the provisions we've set aside for potential losses in New Zealand which are higher than at any time in our history," says Elliott.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

76 Comments

Reads a bit like the Goldilocks Principle.

"Not forgetting that our affordability tests tend to be on the conservative side (yes of course they are). So yes, there are some people paying more now than they were tested at, they've probably also had a pay rise don't forget," says Watson. "People have had pay rises and people have still got jobs. So all of that really sits on the positive side."

Watson, let’s not forget that apart from increased mortgage repayments, they're also paying more for food, rates, insurance and electricity too!

Watson, let’s not forget that apart from increased mortgage repayments, they're also paying more for food, rates, insurance and electricity too!

The Goldilocks Principle + Known Known

The test itself is conservative but counteracting that is lenders ability to massage applications and coach clients on passing.

After the GFC collapse of WaMu the FED did a wider study of fraud in financial services finding that most fraud is actually committed by lenders. External fraud is rare.

"parasitic finance capitalist worries that host is unable to sustain blood draw."

These banks deserve the blame for the housing bubble more than any other institution since they facilitated it and are the primary beneficiary of it. This is the second housing bubble in this century to occur and burst.

These institutions render the economy unproductive by driving so much money, manpower and time into these housing bubbles. The banks provide significantly lower interest rates to mortgages and housing speculation, then we wonder why our economy is so unproductive. It artificially raises the price of financial assets to render wages less competitive for exporting.

Why these institutions are never even mentioned as drivers is beyond me.

Quote of the year "parasitic finance capitalist worries that host is unable to sustain blood draw."

These institutions render the economy unproductive by driving so much money, manpower and time into these housing bubbles. The banks provide significantly lower interest rates to mortgages and housing speculation, then we wonder why our economy is so unproductive. It artificially raises the price of financial assets to render wages less competitive for exporting.

The trade off for the bubble is the credit creation foregone for productive enterprise. The argument used by the monetary elite will be that the bubble - housing - is the collateral for lending for productive purposes.

the bubble is about the price, not investing into housing. People need houses. and it's not fair to pin the price bubble onto banks, as the root of the bubble is from monetary policy.

the bubble is about the price, not investing into housing. People need houses. and it's not fair to pin the price bubble onto banks, as the root of the bubble is from monetary policy.

The 'bubble; is about 'credit creation'. The 'price' is determined by 'credit'. The 'money supply' is 'credit creation.'

the price of the monies, or 'credits', is from monetary policy.

the price of the monies, or 'credits', is from monetary policy.

Wrong. Private banks create credit, not central bank monetary policy. For that reason, Japan has lower broad money growth than the U.S. and the EU over the past 30 years, despite monetary policy.

comercial banks create credits, yes, but the price of the monies are dominated by central banks, this is why and where OCR matters. the money policy also controls the rate of money creation by capital requirements. tools like LVR is just such thing that controls how much credits can be created.

Housing is consumption, not production, thus the banks do not understand, housing is speculation. And when interest rates are near zero, speculation rules.

You can not blame a shark for killing each other in a feeding frenzy.

Blame the RBNZ that started the feeding frenzy by reducing the OCR to 0.25 and throwing cheap money at the sharks via the 'funding for lending program'.

They did put a lot of chum in the water...... The RBA we will not increase rates until 2024 is a blinder

Who supplied " said Chum" to Orr to dump in the property ocean?... his Chum Robertson. He made the chum factory using the tax "meat of the bone" gifted him by labour voters circa 2020

The banks are just following RBNZ guidance and govt policy.

RBNZ sets the risk weights for various types of lending, and govt wants everyone in a house.

Interesting to see the percentile of Interest only has dropped. Possibly from investors shedding some of their portfolio to cover the rest, and bough by owner occupier? Or from home owners doing their best to throttle down the mortgage? Interested to hear thoughts around this point.

ANZ are refusing to let IO loans roll over and extend. Other banks more flexible or nuanced.

Banks were insisting if you were a investor and on interest only that you go to P and I I had two mortgages come up for review last yr and mortgage broker said Interest only wasn't an option

More pressure coming from everywhere.

Just picked up the usual bags of coffee beans - up 20% from a month ago.

It's hard to brand yourself as friendly and approachable, while saying you will take their house and ****ing sell it if they so much as sneeze while they might be low on equity.

But little old Grandma Annie has 50k on term deposit used in those loans, she has rights to get it back... banking is a nasty business... Its all in the fine print.

Granny is getting robbed even if she doesn't want her money back immediately. By the time the financial system has finished with her savings, she'll be lucky to afford the taxi to bingo.

"Think of it as an investment in New Zealand"...

Customer: "I'd like to go interest only until rates come down below 5% and then I'll sell and downsize"

Antonia Watson: [maniacal laughter]

Sad as it may be but that is one reality of what people have done to themselves. Bank exist to make money for shareholders, so it would be foolish to expect charity.

Which bank will start shooting the speculative first...?

The correct phase is: "Bank exist to make money for shareholders and their rich clients."

The rich clients will be ready and waiting to scoop up assets at rock-bottom prices.

Bank exist to make money for shareholders, so it would be foolish to expect charity.

And to give jobs to former politicians who create and nurture favourable environments for milking the population, surely?

Banks 'create' the money out of thin air (charity), for the shareholders to extract rents from the workers. Seems the banks get the charity.

This bank charity when lent out (especially for speculation), never included the interest (ursury) to be repaid by the borrower. So herein lies the problem, the debt plus interest cannot be repaid, the Ponzi scheme collapses and in the end, it will be the banks that become insolvent.

Agree 100%

In ten years we will look back and ask why the banks lent out money with no requirement for the capital to be repaid…. well I guess we know the answer… profits!!

in all honesty why would anyone lend someone half or a million dollars for an investment if the numbers we’re so poor that the principal couldn’t be repaid

knowingly….for about forty percent of lending…madness!

Customer: "I'd like to go interest only until rates come down below 5% and then I'll sell and downsize"

Antonia Watson: [maniacal laughter]

Antonia: Come in and talk to us about it. One of my foot soldiers will work you through some of the options.

ok lets sell first... done Now I am sorry but you do not have enough deposit for that house.... seen it happen.

We asked Watson to elaborate on these options

Well done for calling them out. They spout this off all the time on msm unchallenged.

They make out they have some magical option that you will find out when you come see - when they don't!

In 2016, Antonia Watsons predecessor David Hisco gave a stark warning about NZ property prices being "overcooked" and said "Having been in banking since 1980 I have seen this movie before, the ending is pretty much the same - sometimes a little plot twist, but usually messy"

https://www.nzherald.co.nz/business/david-hisco-housing-and-nz-dollar-o…

We've certainly had the not so little plot twist (COVID), now comes the mess. Did Watson not feel the same urge to sound a warning of carnage? NO - The sugar rush of obscene interest margins must have got in the way....

And all the time the RBNZ continued with its well-worn mantra about how well capitalised the banks are.

What a shame the RBNZ cared not a jot for the borrowers that will be going to the wall.

Just goes to show - Our national institutions care much more about the fate of rich shareholders than they do about ordinary working people trying to buy a house and live their lives. How much more morally bankrupt can they become?

22nd Mar 22 - "If housing market participants think the RBNZ have their back and will act to prevent house prices from falling too much, they may be unpleasantly surprised" https://www.interest.co.nz/property/114939/inflation-has-so-much-streng…

From the same article:

The ANZ economists recently forecast that the RBNZ would hike the Official Cash Rate to 2% (from 1% now) by the end of May and see it reaching a peak of 3.5% in April next year. They now see house prices falling 10%.

It's always fun to look back at past predictions.

Just like Tone to Comb...... spouting trash about interest rates peaking every 2 months for the last year......then wipes the dripping egg from his face, only to create a new cluster fudge story (more egg on face) of why you should " buy that overpriced house now!" "DONT DELAY"

" Never been better"

FACTS AS I SEE IT:

NZ banks gave made a lot of bad loans from 2015 and passed out way too much rope already.

Reckoning days are approaching!

Oh, stop it! I'm eating my popcorn too fast.

Wow, I cant believe that article came from the CEO of ANZ NZ... surely he got pushed out of ANZ after saying that?

Well yes and maybe his dodgy work expense claims.

Economics Question: Which is it better to foreclose on?

a) a borrower with zero equity?

b) a borrower with 80% equity?

The 80% can downsize the 0% is almost broke, renter for life now.

Good question. Talked to a Developer last month who cut his teeth as a newbie working for a well know property figure in the 80s. That figure went on to be crushed by the 87 reset as many speculators were. His feedback on a similar question was that the banks targeted the 80% equity people because the 0% equity people, owing tens of millions, had no recovery possible after they were declared bankrupt. Accordingly they targeted everyone else to try and get any money back.

Could such a thing happen again, we have some very exposed developers, and homeowners and investors. Watch this space...

Many of those small scale developers are probably not financed by a bank. But for 2020 - 2021 14 billion was loaned to 22000 owner occupier borrowers with investment property collateral at DTI's from 7 to 9. 11 billion was loaned to 23000 Investors at DTI's from 7 to 9. These are the loans that are at risk.

It's a trick question,

When you foreclose, the 20% equity owner has less than 0%, and the 0%'er? Well, that hits the books.

Isn't one of the reserve Bank's functions to ensure stability in the economy ?

Maybe this is a warning to the RBNZ that the recession they desire will have consquences... meanwhile inflation... maybe 1/2 a bucket of popcorn tonight.

Inflate or bust. Next episode, USA style bailout of the banks. Keep the bucket of popcorn full.

Will be interesting to see the approach banks take with delinquent mortgages.

Do they either move quickly and foreclose on those that can't/won't make payments. The advantage of this is you take losses as the arise. You don't build a giant contingent liability which comprises of a pool of delinquent mortgages. Further you limit your losses as if these mortgages are under water as if the market falls another 10% The bank will be wearing this 10% of this fall.

Or do they try and constructively work with home owners. This may sound good in practice but isn't really what the banks are in the business of doing. Further you just build a giant contingent liability of delinquent mortgages. Further once word gets out you won't foreclose some may elect to tactically fall behind on their mortgage to maintain a quality of life they are use to while praying for the market to bonce.....

Some banks may chose the either others the or.

Perhaps they hold back as a sort of agreed truce. But once one bank starts to go for it, trying to get as much back before a mass value slump - then the truce might break and its every bank for themselves.

One option - but I don't know whether Govt or the RBNZ has the power to enforce - is to sell all the delinquent loans to a government owned(?) entity to manage, with the banks taking a massive haircut in the process. The new entity - being a non-profit - doesn't need to annually feed shareholders or have fancy offices or massive bonuses to pay, and can take their time letting inflation and appreciation do the work to save the borrowers from financial destruction. Eventually, the entity can be sold off, floated, or wound down.

I relish the thought ... Anyone know if government or the RBNZ has such powers? (I guess ultimately the government does as they can can the rules if so required.)

We have come a long way in 6 months, from the Spruikers like TTP and HW2 assuring us this will never happen to our banks creating the BIGGEST provisions for defaults in their HISTORY.

Now the banks are DGMs to the collective tune of what 700 mil already?

Must say TTP and HW2 have been conspicuously absent from this and other some recent posts about banks provisioning for property debt turning into a millstone as they squash debtors. Hope no one read their mindless spruiking here and went large on debt thinking that magic low debt jellybeans would rain from the sky forever.

Perhaps they are showing some temperance, as it would be rather poor form to be conducting Ponzi Pumping under this topic.

"Ponzi Pumping" - snicker :)

Reminds me of a Black Adder episode for some reason. Was something like "But what of love, my Lord?". "Oh!, You mean 'Rumpy Pumpy' ".

After Covid arrived and interest rates went down Banks like the ANZ threw money at customers. All the managers lusted after potential bonuses. The Banks have had a large part in causing the disaster that is evolving in NZ where people have to sell before the greedy Bank sells them. The Banks knew interest rates were on emergency settings. They still gladly assisted people into levels of debt they should never have been given. Like Casinos Banks always win and some punters lose a lot.

100% correct. Complicit by their own greed.

So, just so I understand...

(1) RBNZ has no responsibility even though it lowered rates so THAT banks would lend?

(2) Individual customers have no responsibility even though they borrowed the money and would have just gone to another bank to borrow it

(3) If all banks had said no thanks and not lent any money, there would be a ComCom investigation into collusion on lending practices

(4) The vendors selling at elevated prices also have no responsibility, even though they have walked away with the cash?

Agree on 1 and 2. Disagree on 3 and 4.

On 3. hard to understand the line of attack of the com com i.e. you can allegedly collude on lowering credit standards but not when raising them?

On 4. why would anyone rationally sell for a lower price than what someone is willing to pay? Buyer beware.

It's on the government as well. LFP could've as well been conditioned to be business only. But no, they chose mortgages because 'wealth effect'. Reaping what they've sown tbh

Don't underestimate this bubble, banks have and may be the losers. In the GFC banks were 'too big to fail', now they have become 'too big to bail'.

https://www.stuff.co.nz/business/130439924/buying-12-houses-in-a-pandem…

Banks lend to folk like this.

For what it's worth, that investor is incredibly transparent with their numbers. He's big on being cashflow positive and finds creative ways to do it. He also manages to do so with some second-tier loans. He's crafty and he's not a speculator that's going to be burned over the next 12-18 months.

his numbers show he has loans of $3.6m and has a questionable positive cashflow of $100k only…. effectively insolvent as he can’t repay his debts, only roll them over

he is skating on such thin ice and all on interest only if my memory serves me right

if he has to go p&i or roll onto higher interest rates he is toast. good luck to him trying to raise rents quicker than interest costs are rising

and there are thousands in the same precarious situation as this muppet

“I knew my cash flow was still good at that interest rate, but I knew at 6%, 7%, 8% it wouldn’t be, so I kind of tried to be proactive at that.

and

Burge opted for two-year terms because he wanted to see through the next general election...He said his cash flows remained healthy up to about 7.5%, with things getting hairy at 8%.

So looks like he could be rolling off sometime after the election. And hoping for a nice dose of welfarism for property speculators from National should they get in.

Too many people think banks are benevolent societies. They're not. I'd refer to see banks foreclose after 30 days of non payment of the usual mortgage payment amount and the govt stepping in and buying from the bank but not at the market rate for the property but at what the outstanding capital owed to the bank. After all it was Robbo combined with RBNZ who created the problem in the first place.

More likely greed and stupidity.

Seems like every option means the bank gets your money, one way or another.

The same banks that walked away with many millions of dollars profit recently..

"Obviously if you've still got a job and you can service the loan it becomes not so relevant. So employment is really important here"

Good thing the RBNZ aren't explicitly trying to drive up unemployment... Oh wait

I loved the sentiment.. Giving all sorts of options to the borrower. Hahaha..

You mean keep them the slave of the bank as long as possible and squeeze all life out of them.. When they have no juice left and banks have sucked the dry, the throw them in the gutter really.

But why would RBNZ or the government which created such a situation buyers would take any responsibility.

Let the fire works begin.

"...we're definitely seeing an increase in the proportion of our book in negative equity. But it's still small. It's 2% or something like that," Watson says.

2% of $105 billion is still $2 billion in home loans with negative equity.

"There's all sorts of different options out there on the table which is why discussing it with someone is really helpful," says Watson.

Yeah. I can imagine how that conversation would go.

1) Cancel any non-essential services.

2) Sell any motor vehicles and cancel the insurance.

3) Do a garage sale and sell any non-essential items.

4) Only buy the cheap self-branded products from the supermarket.

5) Only buy items when they are on sale.

6) Rent out your garage as a sleep-out.

7) Take on a second or third job.

Under no circumstances can you reduce the amount you pay the bank each month.

In fact, we're going to increase the repayments since you now have less than 20% equity, so we've added a Low Equity Premium of between 0.35% and 1.15% to your mortgage, and when you refinance, we'll move you to the standard rate, which is 0.6% higher, as the discounted classic rate only applies if you have 20% equity or more.

Oh. Still can't pay? Then we will have to sell your house. You have 4 weeks to leave, or be evicted and get a criminal charge brought against you for trespass, and if we sell at a loss you will have to pay us back the difference, and we'll have a court order that will get those repayments taken from your wages.

The $1 billion profit? That's for us, not for you.

You've been a banker? Spot on summary. That's pretty much covered it all.

To anyone going underwater ... Go to a budgetary advisory service. They know all the tricks ... INCLUDING THE ONES THAT BANKS DON'T WANT YOU TO KNOW!

Good advice. Plenty of free financial services out there. Start with these to find a local one.

https://sorted.org.nz/guides/planning-and-budgeting/getting-advice

https://www.moneytalks.co.nz/find-help-now/

https://www.cab.org.nz/article/KB00001442

Take lots of paperwork with you, last 3 months of finances is a start but a year would be better. Be totally honest with them. They really can't help you unless you do. And finally, do what they tell you to do! In full. Don't just nibble at the edges. The pain you will feel from giving up a few things is fleeting, and the reward for getting your finances sorted sooner than later is so much sweeter.

ANZ

The YES bank

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.