It's been an extremely busy week in tax - just as we were planning to go to air, Parliament's Finance and Expenditure Select Committee (“the FEC”) released its report on the Taxation, Annual Rates for 2024-25 Emergency Response and Remedial Measures Bill initially introduced last August.

We covered the bill’s main initiatives when it was initially released, and now the FEC is reporting back on submissions it received, what's been amended and why, together with Inland Revenue’s accompanying report on submissions. There's also a supporting report from the independent adviser to the Select Committee, John Cantin, a former guest of this podcast. Overall, there are no major real changes to the legislation. There are minor amendments resulting from issues brought to the attention of the FEC which is how the submission and Select Committee process is meant to operate.

Tax relief for future emergency events

The Officials’ Report on submissions had some interesting submissions on the issue of procedures to manage tax relief for any future emergency events.

The measure was uniformly supported but several submissions proposed making ready to go after a trigger event some of the measures that were brought in and employed relatively successfully during the initial COVID response in 2020 such as carry back of losses, accelerated depreciation, or cashing out of losses. In most cases the submissions were noted or declined.

I thought it was interesting to see that the main submitters involved the Big Four accounting firms, Chartered Accountants of Australia and New Zealand, and the Corporate Taxpayers’ Group. I think these submissions were prompted by our experience during COVID in 2020, where a lot of policy had to be devised and implemented on the hoof, with frantic consultation going on between Inland Revenue and various parties.

I was involved in some of those consultations, and I think it's not unreasonable to have these measures ready to go if needed. On the other hand, I can see why Inland Revenue and the Government might be a little reluctant to have the ambit of the bill expanded.

Transferring UK pensions to New Zealand

Moving on, one of the measures I was interested in was the proposal for what they call a scheme pays measure in relation to Qualifying Recognised Overseas Pension Schemes or QROPS. These are schemes that are able to receive transfers of pensions from the United Kingdom.

There's been some debate around this, as under our rules those transfers are taxable, and it has been a long-standing issue that in many cases this triggered a tax bill which taxpayers could not pay as the funds were locked up in the transferred funds.

One suggestion that had been made was this scheme pays proposal, where transfers are made into a scheme. The scheme may make a payment on behalf of the transferring taxpayer and that will be done at a flat rate of 28%, a “transfer scheme withholding tax”. There's been a bit of tinkering with the proposal mainly about reporting requirements. Otherwise, the regime looks all set to go ahead with effect from 1st April 2026.

It's a measure I feel ambivalent about. I was part of a group which lobbied for this change so it’s good to see it finally in place. On the other hand, as I've said previously, I do think that we ought to be thinking harder about why we're taxed. (I also think taxing people years ahead of when they could access the funds is technically questionable – what if they died before reaching the required age?)

Crypto-Asset Reporting Framework

The other thing of note is that this Bill also introduced the legislation for the Crypto-Asset Reporting Framework. No amendments have been made to that regime. So that will be coming into force with effect from 1st April 2026. From that date New Zealand-based reporting crypto-asset service providers would be required to collect information on the transactions of reportable users that operate through them and report it to Inland Revenue by 30 June 2027. Inland Revenue would exchange this information with other tax authorities (to the extent it related to reportable persons resident in that other jurisdiction) by 30 September 2027.

Taxation and the not-for-profit sector

Moving on Inland Revenue has now released for consultation an Officials Issues Paper Taxation and the not-for-profit sector. This consultation is something that has been telegraphed for some time, there's what might be termed unease around the exemption for the charitable sector and the merits of some entities apparently making use of the exemption. For example, the involvement of Destiny Church in the recent events at the Te Atatu library prompted calls for its charitable status being withdrawn.

Quite surprisingly, given the scale of the topic, the Issues Paper is a reasonably short paper running to just 24 pages in all. It covers three main topics. Firstly, a review of the issues involved in the charity business income tax exemption including the rationale for providing such an exemption, and then what potential policy design issues would need to be considered if that exemption was to be removed.

The second topic is donor-controlled charities, which is probably where the most controversy is emerging. It considers the integrity issues that arise from the absence of specific rules for donor-controlled charities in New Zealand, and again looks at possible design issues, including how other countries treat such entities.

And finally, the paper considers a number of integrity and simplification issues to protect against tax avoidance.

The charity business income tax exemption

Apparently, there are over 29,000 charities registered under the Charities Act. Many raise funds through business activities ranging from small op-shops to significant commercial enterprises. There's been long-standing grumbling about how charities which run a business and have an exemption have an unfair advantage. So, it's interesting to read the background behind this exemption which has been in place since 1940.

Para 2.3 of the Paper sets out the scope of the review:

“Some tax-exempt business activities directly relate to charitable purposes, such as a charity school or charity hospital. Other tax-exempt business activities are unrelated to charitable purposes, such as a dairy farm or food and beverage manufacturer. It is the unrelated business activities that are the focus of this review.”

“…an international outlier”

According to the Paper “The current tax policy settings make New Zealand an international outlier”. According to a 2020 OECD study Taxation and Philanthropy most countries have either restricted the commercial activities that charitable entity can engage in, or they tax charity business income if the business income is unrelated to charitable purpose activities. As the Paper notes

“These countries have typically been concerned with a loss of tax revenue from businesses if a broader tax exemption was applied, unfair competition claims, a desire to separate risk from a charity’s assets, and a desire to encourage charities to direct profits to their specified charitable purpose.”

New Zealand’s exemption is based on the “destination of income approach.” This means that income earned by registered charities is exempt because it would ultimately be destined for a charitable purpose. But and this is again one of the key concerns that's emerged over time, this approach allows income to be accumulated tax free for many years within a charity’s registered business subsidiaries before the public receives any benefit.

What competitive advantage?

Paras 2.7 to 2.14 of the paper look at the question of the exemption providing a competitive advantage because they don't pay tax. This is an allegation I've seen repeatedly raised. As the Paper notes not paying tax means

“One element of a firm's normal cost structure, income tax, is not present in the case of charity run trading operation. It is argued that this “lower” cost could be used by a large-scale entity to undercut its competitors, to improve its market share, or to deter new entrants.”

The Paper does not accept this argument stating:

“Although the exemption does provide a tax advantage, it does not provide a competitive advantage. Any one type of cost can be looked at in isolation.”

The reasoning for this conclusion is:

[2.9] “Because the tax-exempt entity can generally earn tax free returns from all forms of investment, the “after tax” return it expects from a trading activity is correspondingly higher than that of its tax competitors. Therefore, an income tax exempt entity cannot rationally afford to lower its profit margins on a trading activity because alternative forms of investments would then become relatively more attractive.

[2.10] On this basis, the tax exempt entity will charge the same price as its competitors. The tax exemption merely translates to higher profits and hence higher potential distributions to the relevant charitable purpose. Consequently, funding the charitable activity from trading activities is no more distortion than sourcing it from passive investments such as interest on bank deposits or from direct fund raising.”

What about predatory pricing?

The Paper also discusses whether a charity has a greater ability to use predatory pricing to gain an advantage. Again, that's dismissed because “the value of tax losses for taxable businesses mitigates this advantage. Taxable businesses can carry forward losses to offset future profits.” That said, if the taxable company goes bust then it has no use for those losses so maybe that is an actual advantage.

“Second order imperfections”

On the other hand, the Paper acknowledges that there are “various ‘second order’ imperfections in the income tax system that may need to be taken into account.” One is that charitable trading entities do not face compliance costs associated with meeting their tax obligations. This lowers their relative costs of doing business.

Another is the non-refundability of losses for taxable businesses and can result in a disadvantage for such businesses relative to tax exempt business resulting in a higher relative rate of return for non-tax paying entities when there has been a loss in one year.

A third is the costs associated with raising external capital such as negotiating with investors or banks can be significant. These costs often make retained earnings the most cost effective form of financing. Because charities retained earnings are higher, this may give them lower costs for raising capital. On the other hand, charities can't raise equity capital because private investors cannot receive a return.

How much is ‘significant’?

Interestingly, the Paper describes the fiscal cost of not taxing charity business income unrelated to charitable purposes as “significant and is likely to increase.” But no numbers are given and I’m curious to know exactly what is the cost of this particular concession?

The Paper asks submitters to consider what are the most compelling reasons to tax or not tax charity business income before it analyses the potential implications and design issues involved. A major issue will be distinguishing between related and unrelated business activities which could prove difficult in practice without clear legislation and guidance.

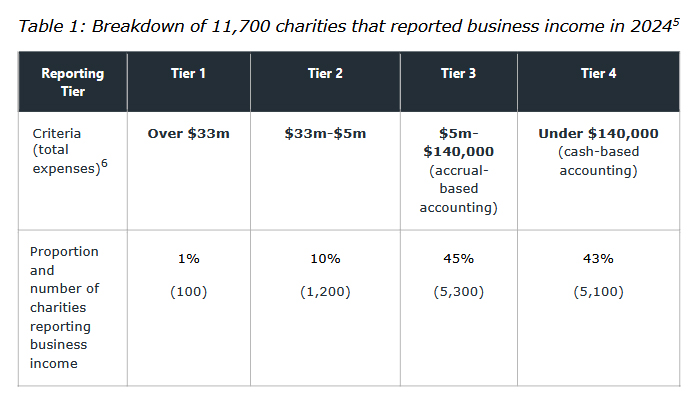

There’s more detail about the trading activities of charities. According to the Paper 11,700 of New Zealand's 29,000 registered charities reported business income in their published 2024 financial accounts.

These four defined tiers follow the reporting requirements within the Charities Act.

A de minimis exemption?

Based on this initial analysis the Paper suggests a de minimis exemption for charities within Tiers 3 and 4. This would take 10,400 charities out of scope with only 1,300 subject to any policy change. Part of any policy change would involve the treatment of accumulated surpluses and whether there should be minimum distribution requirement.

Donor-controlled charities - enabling tax avoidance?

According to the Paper a donor-controlled charity is any “charity registered under the Charities Act that is controlled by the donor, the donor’s family or their associates.” The current issue that there’s no distinction between donor-controlled charities and any other charitable organisations. The concern is growing that this can enable tax avoidance and raised compliance concerns “because of the control the donor or their associates can exercise over the use of charity funds.”

The Paper gives a few examples of potential abuse such as ‘circular arrangements’ when the donor gifts money to a charity they control, claim a donation tax credit or gift deduction, and the charity immediately invests the money back into the businesses controlled by the donor or their associates.

Also of concern with donor-controlled charities there can be a significant lag between the time of tax concessions for the donor and the charity, and the time of ultimate public benefit. This occurs because funds are accumulated and no or very minimal charitable distributions are made.

Another issue arises when donor-controlled charities purchase assets, or goods and services from the donor or their associates, at prices exceeding what would normally be paid by unrelated parties. These acquisitions are often made on terms that would not normally exist between unrelated parties.

Defining donor-controlled charities

This is the nub of the matter what criteria should be used to define a donor-controlled charity? The funds contributed and level of control a founder has. In Canada for example a charity is considered a private foundation if it is controlled by a majority (more than 50%) of directors, trustees, or like officials that do not deal with each other at arm’s length, or more than 50% of capital is contributed by a person, or a group of persons, not dealing with each other at arm’s length and who are involved with the private foundation.

The Paper suggests that transactions between donor-controlled charities and their associates could be required to be on arm’s length terms or prohibited outright noting in para 3.13:

“This approach was supported by the Tax Working Group in 2019, which found that the rules were private charitable foundations in New Zealand appeared to be unusually loose. The group recommended that the government considering removing tax concessions for private controlled foundations or trusts that do not have arm’s length, governance or distribution policies.”

Apart from citing the Canadian approach the Paper considers the approach to this issue in Australia, the United Kingdom and the United States. It suggests there should be a minimum distribution rule to deal with the question of the time lag between the charity and a donor claiming a benefit and the actual public benefit accruing from the distribution.

Taxing membership fees?

Chapter 4 considers integrity and simplification. This section has already attracted some media comment because it raises the possibility of taxing membership fees which could affect as many as 9,000 not-for-profit organisations.

At issue is the concept of mutuality and member transactions. Generally speaking, most not-for-profit organisations are treated as mutual associations. That includes many clubs, societies, trade associations, professional regulatory bodies.

Up until the early 2000s Inland Revenue’s guidance was that mutual associations were not liable for income tax from transactions with their members, including membership subscriptions and levies. Inland Revenue has withdrawn that advice and has drafted a replacement operational statement which will be released pending what feedback it receives on this Issues Paper.

The impact of Inland Revenue’s revised position would be that trading and other normally taxable transactions with members, including some subscriptions, would be deemed to be taxable income regardless of whether the common law principle of mutuality would apply. The Paper notes that most not-for-profits would not qualify for mutual treatment anyway, because their constitutions will prohibit distribution of surpluses to members including on winding up. This prevents the necessary degree of mutuality required.

Fringe Benefit Tax exemption under review

Finally, the paper touches on the FBT exemption for charities, which has been available since 1985. The paper notes “there are weak efficiency grounds for continuing this exemption” which “lacks coherence”. Inland Revenue is currently reviewing FBT generally and these comments suggest the FBT not-for-profits exemption is likely to go.

Submissions are open on the Issues Paper now, and close on the very unhelpful date it has to be said, of 31st March, when we're all rather tied up with tax year-end issues. Notwithstanding that I expect there will be plenty of submissions particularly around the potential impact of taxing membership transactions.

Meanwhile in America…

Finally, a quick update on last week’s comments in relation to my concerns about potential leaks coming out of the US Internal Revenue Service (“the IRS”), following the Department of Government Efficiency (DOGE) trawling through the IRS and every other U.S. government agency.

The update I've had is that the DOGE people are looking more at IRS internal processes and nothing to do with any data that the IRS has received from Inland Revenue, or any other agency. There are a number of international obligations that the US has still to meet, but no doubt some concerns will have been raised.

But as I said at the time, which I believe is almost certainly the case, IRS officials will be highly professional in making sure that that information shared by other tax authorities is not leaked, accidentally or otherwise, to outside parties.

An interesting choice…

On the other hand, the IRS is getting a new Commissioner. The nominee is William Hollis Long II, or Billy Long, who is a former Republican House of Representatives member from Missouri.

Billy Long, nominee Commissioner of the Internal Revenue Service

He’s a controversial pick to say the least. He’s not a tax professional, and of particular note is that he was a co-sponsor of a bill in 2015 that would have abolished the IRS and introduced a national sales tax. He is also long-time supporter of a flat income tax for the US system. It'll be interesting to see how this plays out, and as always, we will bring you developments as they emerge.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.