“I alone can fix it,” Donald Trump proclaimed in 2016, when accepting the Republican nomination for president. Fix what, exactly? Among other problems, “the economy, stupid,” to borrow the famous mantra from Bill Clinton’s 1992 presidential run. Last year, Trump once again campaigned on the premise that the US economy was “in crisis” and a “disaster.” He began his second term with a solemn promise to usher in “the golden age of America.”

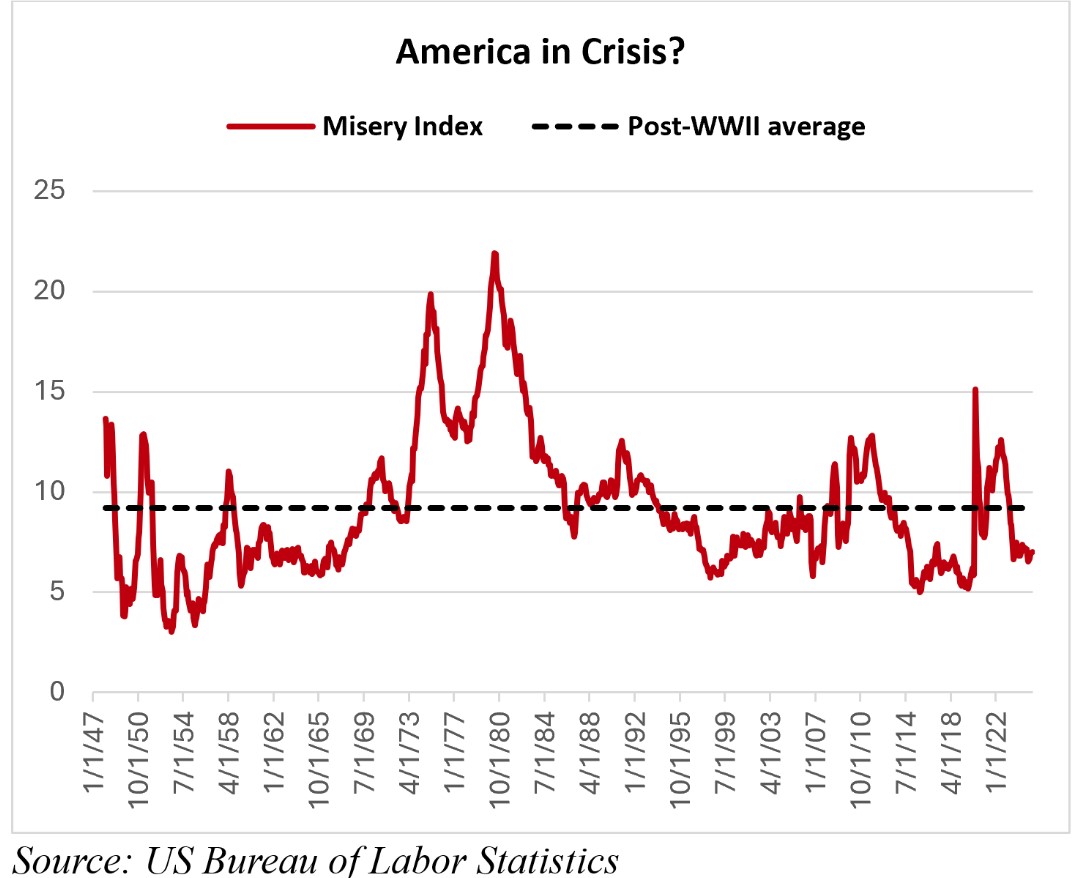

Donald Trump’s bleak diagnosis of the US economy is not grounded in reality – at least not yet. America’s “misery index” – the sum of the unemployment and inflation rates – hardly suggests an economy in dire straits: it was 7.0% in January 2025, down dramatically from its post-pandemic peak of 12.7% in mid-2022, and more than two percentage points below its postwar average of 9.2%. In fact, the latest reading is virtually identical to the 6.9% average recorded during Trump’s first administration (2017-20), which he fondly recalls as “the greatest economy in the history of the world.”

Campaign rhetoric is one thing; acting on it is quite another – especially if its core premise is false. The risk is that the initial policy frenzy of Trump 2.0 – some 73 executive orders in his first month back – could spark the very crisis he currently imagines is now at hand.

The inflationary impact of tariffs is a case in point. Here, I find Trump’s new “reciprocal” tariff plan more worrying than targeted bilateral tariff hikes (which are still a serious blunder, as I have argued ad nauseam). This new plan reflects Trump’s belief that the rest of the world must conform to the American “model,” and his willingness to use tariffs as a cudgel to make that happen. This applies not just to cross-border trade, but also to industrial policies, value-added and digital-services taxes, currency manipulation, and any other so-called structural impediment to foreign-market access.

Trump’s plan flies in the face not only of well-established supply-chain efficiencies, but also of the eight rounds of reciprocal tariff reductions after the United States enacted the Reciprocal Trade Agreements Act of 1934. Is the Trump administration, with its grandiose insistence on reciprocity, actually unaware of this?

Nor does Team Trump acknowledge the inflationary potential of these actions, pointing to the lack of inflation fallout from the tariffs of 2018-19. This is a false comparison: reciprocal tariffs are aimed at all of America’s major trading partners, not just China, as was the case back then. Moreover, they are being proposed during a period when core inflation (the Consumer Price Index excluding food and energy prices) is 3.3% – well above the Federal Reserve’s 2% target. By contrast, average core CPI inflation was close to the Fed’s target during Trump’s first administration.

Much to Trump’s displeasure, an inflation-targeting Fed will likely be wary of cutting policy rates in the face of price increases from tariff hikes. And it’s not just eggs – Americans now seem to be bracing for a sustained period of higher prices. The latest University of Michigan survey showed that consumers expect inflation to be 3.5% over the next five to ten years – the highest reading since 1995.

Another concern is that Trump’s policies will pierce the denial embedded in financial markets. The US stock market has been on a tear, largely owing to a speculative binge on artificial intelligence. According to Bloomberg, the “Magnificent Seven” – the tech giants Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla, all of which have poured billions into AI development and infrastructure – are up fully 3.2-fold (on an equal-weighted, total-return basis) from the end of 2022. Bloomberg calculates this group has a price-earnings ratio of 32.9 – nearly 40% higher than the average PE ratio of other large-capitalisation stocks.

Moreover, by December 2024, the Magnificent Seven accounted for 34% of the S&P 500’s total market capitalisation – nearly six times the internet sector’s market-capitalisation share prior to the end of the dotcom bubble in March 2000. A DeepSeek selloff in late January, caused by the stunning revelation that a Chinese startup had created a large language model on par with those of American AI firms at a fraction of the cost, underscores this concentration risk. While AI may represent a revolutionary technological breakthrough, it may be only a matter of time before this speculative bubble bursts.

I also worry about a sharp dollar correction. To be sure, I wrongly predicted a dollar crash in mid-2020. But with the broad dollar index – the real effective exchange rate as calculated by the Bank for International Settlements – surging to a record high, my concerns have multiplied. America’s gaping current-account deficit and domestic-savings shortfall are far worse today than in mid-2020; there is limited upside to interest rates after their recent normalisation; and the eventual collapse of the AI-fueled equity bubble could lead to cross-asset contagion. American exceptionalism, a pillar of the greenback’s dominance, may also be at risk; key soft-power attributes long associated with US global leadership – morality, character, adherence to the rule of law, and unflinching commitment to alliances – are fraying as the MAGA grip tightens.

A polarised American society endlessly debates whether Trump is as crazy as a loon or as sly as a fox. The MAGA hope is that the savvy dealmaker will ultimately prevail, winning major concessions by taking tough positions and bullying foreign adversaries. In these days of froth, that may not be the wisest bet to make. In the end, America may well get the economic and financial crisis that Donald Trump falsely claims to be confronting. The Misery Index will then finally live up to its name.

*Stephen S. Roach, a former chairman of Morgan Stanley Asia, is a faculty member at Yale University and the author of the forthcoming Accidental Conflict: America, China, and the Clash of False Narratives (Yale University Press, November 2022). Copyright: Project Syndicate, 2025, published here with permission.

14 Comments

Trump’s first presidency and immediate aftermath was distorted by the covid pandemic. Even so, Biden in succession did not implement outstandingly different measures, economically speaking at least.This time round Trump is acting both faster and more radically. While the majority of commentators speak ill of both ability and direction, it still remains to be seen if such dire predictions will materialise and if so, how long exactly that will take. American society though en masse, is not slow to apportion blame when their lot goes sour. Suggest that feature will likely soon be the barometer of Trump’s success or failure to MAGA.

Trump is a symptom, not a cause (the writer doesn't seem to get that). And Trump cannot solve the problem, no more than Canute stalled the tide. And voters are obviously somewhat less than informed, less than thoughtful - so expect incumbents to be ejected with rapidity from here on.

But what get me, is when Trump mentions resources - rare earths from Ukraine, I seem to remember hearing - no scribe stands back and asks the logical question(s).

Firstly, if the US needs outside resources, well, perhaps that suggests there are physical limits. And that the 'richest' nation seems unable to conjure up physical resources using keystroke-issued proxy. Who would have guessed? And it the US needs outside resources, and is attempting GROWTH...

But instead, we get a raft of folk blaming Trump for everything, now and in the future. Sure, he's a psychopath (as are most who get to the top) and lacks empathy and intelligence, but half of the US put him there. WHY? is the question.

I've put the Limits to Growth to Roach; "I do not agree with you" was the reply. No reasoning, no engagement.

Suggest the answer unfortunately to that logical question is little more than that those that are to be involved in said extraction of said rare minerals have no more thought than self enrichment. Call me cynical, call me correctly.

The US has significant REE deposits of its own. Maybe even has the largest deposits in the world. I suggest it is a simple as Trump asking advisors what resources Ukraine have that could be used to offset the costs of supporting their war and the answer was rare earth elements. Trump is a practical man.

Care to supply data?

https://worldpopulationreview.com/country-rankings/rare-earth-reserves-…

'The United States also has approximately 1.5 metric tons of rare earth metals.'

Your links have nothing to do with REE deposits?

Readers should note that rare earth elements are not particularly rare.

Cowboy State Daily: Rare Earths Discovery Near Wheatland So Big It Could Be World Leader

That kind of boosting used to happen on the Otago goldfields.

Wyoming has been known about for years, and my comment stands:

https://pubs.usgs.gov/sir/2010/5220/pdf/SIR2010-5220.pdf#page=22

Reminds me of palladium, and kiwifruit, and asparagus, and tulips...

Ain’t it true. Courtesy Andy Williams. The sun, there every day of waking for our less than pin pricks on fly spots of lives will one day, after billions of them, die. Does any one suggest when so with any accuracy. So given that eventual finiteness, is it not that the human race is making hay while the sun shines?

Nearly all our present problems are caused by abundance not scarcity.

Bollocks.

Abundance of what?

Land for housing? Biodiversity? High-quality energy stocks? High-quality resource stocks? Forest stocks? Topsoil? Aquifer replenishment?

The only abundance I see, is of faith-based optimism.

PDK you fell into that trap properly didn't you? Slow down and think before you bite. Try people for a start. It's fairly obvious there are too many. But Zac is right Too much oil, too much steel, too much concrete. The list goes on. It has all led to the population on the planet flourishing until it threatens the planet.

Yes, that was the first thing I looked up. But what I can't figure is why they would think the American public is so stupid. Surely heaps of Americans looked that up too - but we've watched lots of news and podcast out of the US - and to date no one has brought up that question. All seems very odd.

REE are everywhere. In the future it will be supplied at a faction of the cost it is now.

Bollocks, and you have no excuse for still peddling this.

I have often pointed out - using copper as a resource example - that the energy required to mine resources increases over time, because we mine the best, first. Thus copper has gone from requiring 10 tons of 'overburden' removed per ton of ore gotten, to 400 tons. That requires aa lot more energy.

And energy underwrites money - no energy = no work done.

So no, extraction will never be 'cheaper'; even now 'cheaper' just reflects the increasing unrepayableness of debt.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.