Last episode we discussed the International Visitor Levy and the Government’s thinking behind the attempted repurposing of the increase in that levy from $35 to $100. The increased levy could apply to potentially as many as 2,000,000 visitors to New Zealand.

Last week, with immediate effect, the Government announced changes in visa conditions, which will allow visitors to work remotely for an overseas employer client during a visit to New Zealand. This change will affect all applications received from 27th January. It includes tourists, people visiting families together with partners and guardians on longer term visitor visas.

A faster growth track

Basically, the changes are designed to encourage digital nomads to come here and enable them to carry on working for their overseas without breaching their visa conditions. As Nicola Willis in her role as Minister for Economic Growth explained in the accompanying press release “The change is part of the Government’s plan to unlock New Zealand’s potential by shifting the country onto a faster growth track.”

These new visitor visas are subject to the following conditions: the visa holder cannot work for a New Zealand employer, nor can they provide goods or services to people or businesses in New Zealand, nor can they do work that requires them to be physically present at a workplace in New Zealand.

What about income tax?

What difference, though, does the new visa make from a New Zealand income tax perspective? The short answer is ‘not an awful lot.’ Much of this possible digital nomad activity is already within section CW19 of the Income Tax Act 2007.

Under that provision the income that a non-resident person derives from performing personal or professional services in New Zealand is exempt if the if the visit is for 92 or fewer days, the services are performed for a person who's not resident in New Zealand and that income is taxable in the jurisdiction in which the person is resident. This would typically capture most of activity of a digital nomad.

Section CW 19 is a long standing provision and, as the New Zealand Immigration announcement noted, the 92 day exempt period can be increased to 183 days if the visitor is tax resident in a tax country with which we have a double tax agreement.

As the Immigration Minister Erica Stanford noted updating these visitor visas reflects the realities of current, current modern flexible working environment. It’s probably a good move to bring the visas up to date and make clear that it's generally not a major issue if you are working remotely when visiting and are not in breach of any tax obligations.

Keep in mind the 92-day exemption in section CW 19 is for employees only, it does not apply to any self-employed person who might provide goods or services to people or businesses in New Zealand.

Yes, but what about Taylor Swift?

The other group of people who aren't covered by the section CW 19 exemption are ‘public entertainers.’ Which means that if we ever did manage to get Taylor Swift here, theoretically the earnings that she made from any concert would be taxable in New Zealand. As an aside there are all sorts of very interesting and complex tax rules around entertainers.

Overall, it’s an interesting move which seems to now bring our visa practices in line with what's happening globally. It reflects that, because of the greater interconnectivity available now people have quietly been working remotely, effectively acting as digital nomads without actually realising that they may have been in breach of their visa conditions.

In any case, if the person has been here for under 92 days, then generally speaking, they shouldn’t be in breach of any of their tax obligations. As I said an interesting move and no harm clarifying the visa situation. What the economic impact will be, who knows.

An end to citizenship based taxation for US citizens?

In our last podcast of 2024, we discussed Inland Revenue’s paper on changing the Foreign Investment Fund (FIF) regime to make it more attractive for migrants. One of the issues the paper discussed was how the FIF regime created headaches for American citizens and Green Card holders tax resident in New Zealand but who still have to file U.S. Federal tax returns. The paper was proposing changes that might help deal with the essential double taxation issue for these taxpayers.

It so happens an Illinois Republican Congressman, Darren LaHood, has introduced the Residence-Based Taxation for Americans Abroad Act, which would implement a residence based taxation system for U.S. citizens currently living overseas.

LaHood’s press release doesn't mention it, but I'd be very curious to know exactly how much tax these expat American citizens pay in the US.

The preamble in the press release notes that the United States is the only major country that uses citizenship based taxation. According to recent estimates, there are about 5 million U.S. citizens currently living aboard. Based on the last census there are over 30,000 US born persons here in New Zealand.

LaHood is also a member of the highly influential House Committee on Ways and Means, (their equivalent of the Finance and Expenditure Select Committee) so perhaps this is a serious move. This bill could also gain from the general tax cutting mood of the new Trump administration. We'll be interested to see how much further this goes.

In the meantime we’ll also be watching for progress on Inland Revenue’s proposals to try and deal with the anomalies the FIF regime creates for U.S. citizens resident here.

New Inland Revenue guidance on depreciation

Finally, Inland Revenue as always has been busy pushing out guidance and draft consultations on issues. One which caught my eye and will be worth perhaps thinking further about is Interpretation Statement IS25/03 Income tax. Identifying the relevant item of property for depreciation purposes. There’s also an accompanying fact sheet which is always very helpful.

Our very detailed tax depreciation rules system rules have numerous depreciation rates available so it's often a worthwhile exercise identifying what assets are involved and maximising the available depreciation.

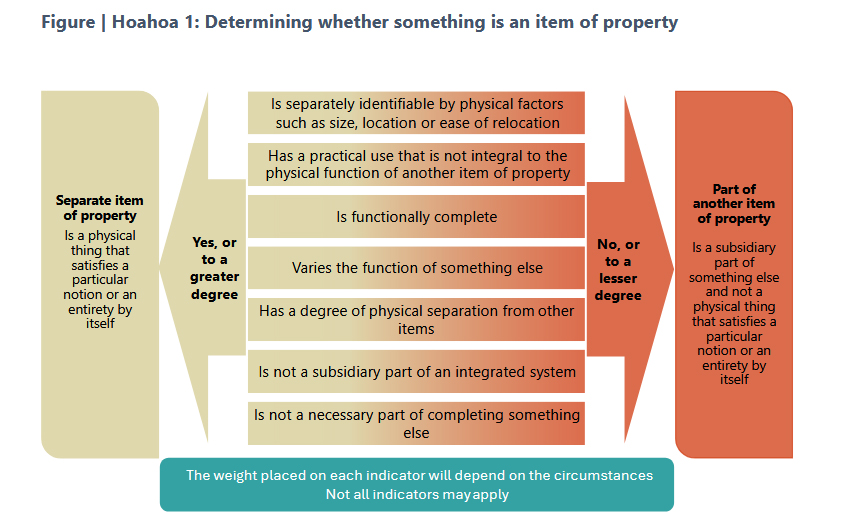

The Interpretation Statement therefore provides general guidance on how to identify the relevant item of property when applying the depreciation rules. The key issue is determining whether the item is physically distinct from a wider asset of which it might from a part.

In determining this you would first consider its location or size, whether it's integral to the physical functioning of a wider asset and the degree of physical attachment to other related assets.

Secondly, is the item largely functionally complete, in other words, can it function on its own? That doesn't necessarily mean that it has to be self-contained or used separately, but could it function on its own??

Thirdly, does the item vary the function of another item? What this means is two items will remain separate items where one varies the function of another item, enabling it to perform more specialised function.

The Interpretation Statement provides a few examples together with a useful flow chart.

A key part of the analysis is it always comes down to a question of fact and that means that there will be different outcomes for apparently similar situations.

The Interpretation Statement contains links to other Inland Revenue guidance on depreciation related issues. All this is very useful because in the run up to the end of the tax year on 31st March, we often have situations where clients are looking at investments and wanting to maximise depreciation.

And on that note, that’s all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.