President Trump was inaugurated for his second term last week, and he swiftly set about implementing his agenda. In his inauguration speech he remarked “America will no longer be beholden to foreign organisations for our national tax policy, which punishes American businesses.” This prompted me to ask on LinkedIn what the potential implications could be for the OECD Two Pillar agreement?

Repudiating the OECD Two-Pillar proposal

Well, President Trump didn't wait long to take further action. In fact, pretty much almost immediately he issued a Whitehouse Executive Order railing against the “Global Tax Deal” which “limits our Nation’s ability to enact tax policies that serve the interests of American businesses and workers.” Instead, the Executive Order “recaptures our Nation’s sovereignty and economic competitiveness by clarifying that the Global Tax Deal has no force or effect in the United States.”

The Executive Order goes on to direct the Secretary of the Treasury (the equivalent of our Finance Minister) and the Permanent Representative of the United States to the OECD) to

“…notify the OECD that any commitments made by the prior administration on behalf of the United States with respect to the Global Tax Deal have no force or effect within the United States absent an act by Congress adopting the relevant provisions of the Global Tax Deal.”

So “Shots fired” would be the quick response to that. But it's Section Two of the memorandum which caught my eye when I looked at it. The Order doesn’t have the technical and legal language you might expect, but it's written with very much the voice of Trump.

Getting your retaliation in first

Section Two of the Order discusses options for protection from discriminatory and extraterritorial tax measures. It directs the Secretary of Treasury in consultation with the United States Trade Representative, to

“…investigate whether any foreign countries are not in compliance with any tax treaty with the United States or have any tax rules in place, or are likely to put tax rules in place, that are extraterritorial or disproportionately affect American companies, and develop and present to the President, through the Assistant to the President for Economic Policy, a list of options for protective measures or other actions that the United States should adopt or take in response to such non-compliance or tax rules.”

Now that is something that I don't think many people have yet noted. Basically, it's a pre-emptive strike at other governments responding to a what appears like an almost certain collapse of the OECD’s Two Pillar solution by adopting digital services taxes (DSTs). We've introduced (but not yet enacted) that legislation. Several countries such as Canada and France do have DSTs in place as a backstop in case the OECD’s Two Pillar solution fell over.

So now we're in very interesting times. And the issue is that the large tech companies in particular are the target of the Two Pillar solution. Mark Zuckerberg, the head of Meta, together with the head of Google, as well as Elon Musk, owner of the site formerly known as Twitter, all had prime seats at President Trump's inauguration. Musk in addition, heavily financed President Trump's campaign. All now have the President's ear which will maybe enable retaliatory actions by the US against attempts by other governments to say, ‘Well, wait a minute, without the Two Pillar deal we're losing revenue ourselves here.’ The collapse of the Two Pillar solution could provoke the 2020’s tax equivalent of the notorious Smoot Hawley Tariff Act of 1930, which is often credited with triggering the Great Depression of the 1930s.

What could be the impact in New Zealand?

We are a small player, but from our perspective it's quite relevant how we tackle the taxation of the tech companies. According to Google and Facebook’s financial statements for the December 2023 year, the two companies probably captured about $1.1 billion in advertising all of which was sent offshore. However, the reported taxable income for those two companies for the 2023 year was just under $28 million before tax.

I'm bringing this up because this week NZME announced that it was cutting its newsroom staff by 40, and the financial woes of the media are well documented. Media is struggling as its advertising revenue has essentially collapsed because large chunks of it are now being paid offshore.

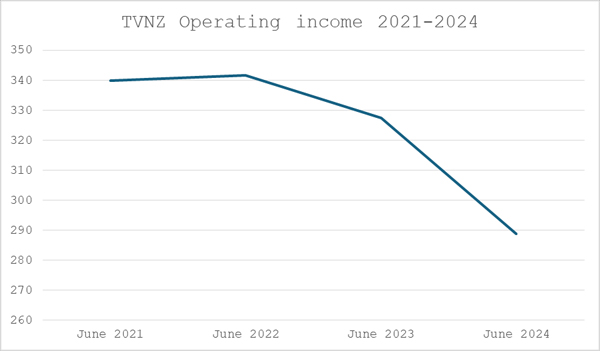

If you want to put it in some context of just how bad the problems are for our media, TVNZ’s pretax 10 years ago for the year to June 2015 was $333.9 million.

You'd expect with inflation those numbers would have risen. In fact, for the last three years, TVNZ’s revenue has plateaued at $339.9 million for 2021, $341.7 million for 2022 and $327.6 million for 2023 before falling by $39 million to just under $289 million for the year to June 2024.

The media is in desperate financial states and that has knock on effect for the Government, because sooner or later it will be called on for some sort of financial support. An option the Government might consider is whether a levy of some sort could be directed at advertising, which is paid offshore.

Sooner or later a New Zealand government will be put in the position where it may have to make an uncomfortable call. Meanwhile, we have the United States making it very clear that it is not going to accept the Two Pillar solution - and would take retaliatory action if it felt its companies’ business interests were threatened by a DST or other levy. It's not a great scenario and makes for a pretty rocky start to the year.

Raising taxes on the quiet?

Moving on, an interesting story came out over the holiday break in relation to the International Visitor Levy (IVL). Now this was quite controversially increased from $35 per head to $100 from 1st October last year. This move is expected to raise $149 million. The increase to $100 was way above what the tourism industry wanted or what ministry officials recommended. The IVL must be spent on tourism and conservation, essentially, it's what we term hypothecated – ring fenced for those particular areas.

It turns out that there's some digging been done by Derek Cheng at The New Zealand Herald, who found out under the Official Information Act that there was quite a bit of ministerial wrangling over how it might be possible to divert or repurpose the IVL income to improve the Government's overall finances.

Essentially, the dramatic increase in the IVL enabled central government funding which would have gone to the Department of Conservation to be frozen. According to the Herald report this move gave the Government approximately $307 million of ‘fiscal headroom’.

Now there's nothing wrong with this move although stakeholders in the sector are unhappy with the result. Apparently, the Minister of Finance Nicola Willis wanted to have the IVL funds become part of the Government’s Consolidated Fund where it could be spent as she directed. That was rejected as it would require a change of law.

I think this attempt indicates we're going to see more of this tactic from the Government. Nicola Willis made a passing comment at a briefing that she'd like to make more use of fees and levies to raise revenue. Looking ahead, the budget in May will give us a really good indicator of how increased fees and levies might be used to basically shore up the Government's books.

It’s a sleight of hand way of finding additional revenue without explicitly raising taxes directly. Fee increases such as those for the IVL means although the rates of personal income tax and GST remain the same, the Government is managing to extract additional revenue.

So, watch this space. Governments all around the world are trying to do this. In some cases, it's appropriate, it's a bit like user pays. But in other cases, you wonder if it's just a little bit too much financial wizardry for the sake of it.

Inland Revenue targeting collection of tax debt

Unsurprisingly Inland Revenue is continuing its actions we saw last year of increased activity in collecting debt. Stories have emerged since the start of this year relating to its pursuing families for overpaid Working for Families credits.

RNZ ran a story on 20th January about a parent who had incorrectly recorded her relationship status for Working for Families only for Inland Revenue to advise her she now owes $47,000. This was the third such report this year with the other two stories involving tax bills of $9,000 and $24,000 respectively. Inland Revenue’s response is that these are the rules, and it has to carry on and collect the overpaid credits. However, I am aware that there have been issues with parents registering new-born children through the Department of Internal Affairs website resulting in overpayments.

Don’t look at me, I’m only the Minister

When RNZ asked the Minister of Revenue Simon Watts for comment, he responded it was an operational matter for Inland Revenue.

“I'm advised that this issue affects a small number of taxpayers who have received an overpayment due to not providing IRD with the most recent information on their circumstances.”

To be fair to Inland Revenue, as Susan St John, an economist and Child Poverty Action Group member said, the problems were not with Inland Revenue's application of Working for Families, but with the system itself.

This touches on a point I've made repeatedly in the past. Working for Families tax credits begin to be clawed back (abated) where family income is at $42,700 per annum. Above that threshold, Working for Families is abated at a rate of 27 cents for every dollar earned above that threshold. Now that threshold has not been changed since June 2018, and I had a somewhat testy exchange with the Minister of Finance at the Budget Lockup in 2024 over the fact the threshold was left unchanged.

Who suffers the highest Effective Marginal Tax Rates? It’s not who you might think

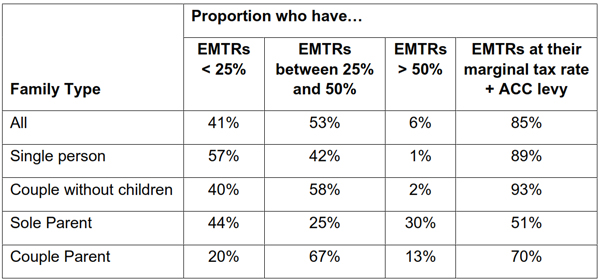

As a consequence, families on relatively low incomes face very high effective marginal tax rates. Coincidentally this week Treasury released a paper The Cost of Working More: Understanding Effective Marginal Tax Rates in New Zealand's Tax and Transfer Systems which analyses the impact of effective marginal tax rates on work incentives. The paper examines what happens to a person's effective marginal tax rate, when their income rises resulting in higher tax rates or the abatement of benefits such as Working for Families.

The paper notes that for most persons their effective marginal tax rate (EMTR) is equal to their top tax rate. For example, someone earning over $180,000, with no other benefits, their EMTR would be 39%. In other words, for every dollar they earn above that threshold it is taxed at 39%. Overall, most New Zealanders’ EMTRs are below 50%, with only 6% experiencing EMTRs of over 50%.

But the distribution of high EMTR varies significantly across different family types. Families without children generally experience low EMTRs.

Therefore, they have higher work incentives because they are less likely to be receiving government support payments that would be reduced by increases to income. Around 90% of such families have EMTRs equal to their marginal tax rate.

“The Iron Triangle”

The paper notes the issue of what it calls “the Iron Triangle”. This is the inherent trade-off between three competing objectives - providing adequate income support, maintaining reasonable government costs and preserving work incentives. Whatever you do, you're never going to hit the sweet spot on any of that. It’s therefore a question of continual adjustment.

The paper is very interesting as it breaks down the various family types, the composition of their income and the benefits they receive. People might be receiving Best Start, Working for Families, Accommodation Supplement, all of which are subject to some form of abatement and at differing rates. The paper then analyses what happens when people start earning additional income and the numbers are really quite astonishing. The paper concludes parents are the group that most likely face financial disincentives to work because of the impact of high effective marginal tax rates.

Where it gets really problematical as these abatements start kicking in is for families with children. 13% of couple parent families have EMTRs greater than 50%. 30% of all single parent families have effective marginal tax rates greater than 50%. And there are a number of families with children that have EMTRs higher than 100%. The stats don't reveal just how many people that might be affecting, but it's certainly 20,000 to 50,000 it would seem. Which is a substantial number of people.

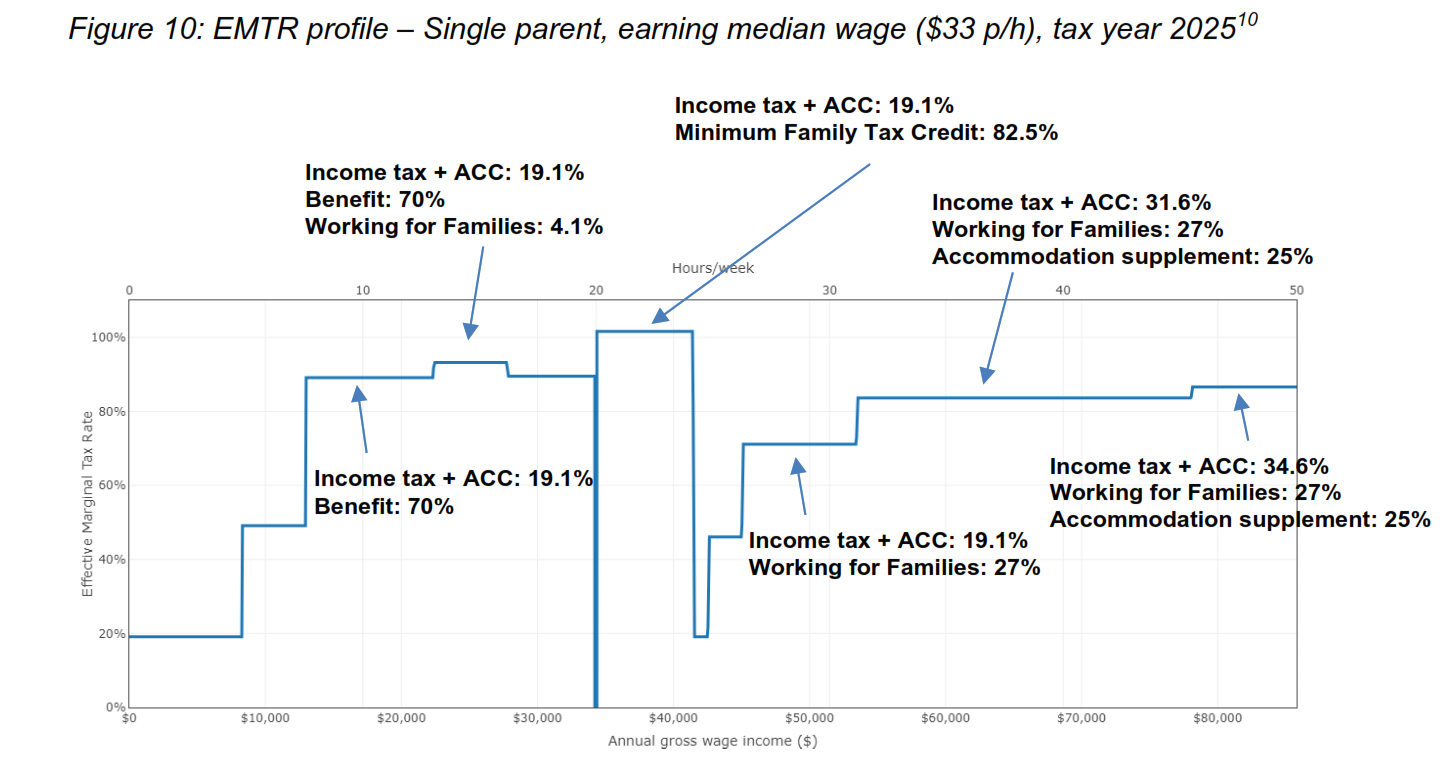

Figure 10 in the paper shows the EMTR profile for a sole parent family earning the media wage of $33 per hour. As the paper notes regardless of weekly working hours the parent faces high EMTRs almost consistently:

1. When working between 8 to 20 hours per week, they keep only around 10 cents of each additional dollar earned due to income tax and reductions in benefits and Working for Families tax credits.

2. When working between 20 to 24 hours, they keep none of the additional dollar earned due to reductions in the Minimum Family Tax Credit, income tax, and the ACC levy. In this case, they actually lose nearly 2 cents by earning an extra dollar.

3. When working between 26 to 31 hours, they keep slightly less than 30 cents of each additional dollar earned due to income tax and reductions in Working for Families tax credits and Accommodation Supplement.

4. When working between 31 hours and full-time11, they keep less than 20 cents of each additional dollar earned due to a higher income tax rate and reductions in Working for Families tax credits and Accommodation Supplement.

A long-standing issue no-one seems to want to fix

Compounding the matter, the paper notes that parents may be limited by childcare costs when choosing to increase their work, as there are fewer adults within the household supervising care for children. Overall it concludes:

“While the system generally preserves work incentives for most of the population, certain family types, particularly single parents, face significant financial disincentives to increasing work hours. This suggests that future policy development may need to focus on whether current abatement thresholds and rates are optimally placed.”

My response is that current abatement thresholds and rates are not “optimally placed”’ which was something the Welfare Expert Advisory Group was saying back in 2019. As I previously mentioned, the $42,700 abatement threshold for Working for Families (which is the limit of family income, not individual income) has not been increased since 2018, so there's a real issue here. The Minister of Finance, who is now the Minister for Economic Growth, is keen on getting people into productive work as part of that. But people are not going to take up additional work if they realise that between the abatements and the additional childcare costs they're going backwards.

It's a long running issue and it will be very interesting to see what response the government makes to that. As always, we'll bring you developments.

On that note, that's all for this week. I'm Terry Baucher, and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening. And please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

32 Comments

Grey nomad friend wondering why the unemployed couldn't just get organised and go fruit picking or something. Reminded him that when he does it on his motorhome trips he gets to keep it what he earns, less the paye. But for the UE it is a major pain in the a##. Can affect main benefits and supplementary and even social housing criteria.

Sooner we get UBI the sooner the mess explained in this article goes away - and msd shrinks by about 90%.

It's ok for super, should be ok for the rest of us. And would deal with the super 'for all' issue at same time.

I've been banging on about this for years. The system needs to change to incentivise work - I don't care what people say in regards to "work is good for you, be valued, make friendships etc" what actually matters most with kids is having enough income and if you disincentivise work you simply won't do it and it also encourages further kids in an entrenchment cycle.

Would be good for some general ideas - I thought about completely free daycare but then you'd have to massively scale that up over a number of years.

Any one in social services will give you examples of the crazy outcome from well intentioned policy. For example, having another feral when your last turns 14 so to avoid work testing is common. Or giving one up to a relative so they can avoid work testing.

NZ Welfare - how to encourage the least capable to breed. Policy makers and politicians are eyes wide shut on this.

Meanwhile middle class couples are having one or two because it is fiscally irresponsible to have more. In essence we over tax the responsible middle class to subsidise the irresponsible beneficiary class. Behind all the theatrics the only two groups in society Labour and National truly care about are beneficiary's and land owners.

So something that would be helpful would be to back off with the anecdotal stories of baby factories for benefits and such like which are such a tiny tiny minority and concentrate on those that the MTR is really effecting.

"The beneficiary class" is a pretty opaque description when you consider just how many "benefit" form government payments(almost 100% during covid).

It is the future social structure over the next decades that is the concern. Financial issues can be resolved over time if we have a hard working, educated and socially responsible citizen.

It will be very difficult to pull NZ out of a hole with the mass numbers of ferals that we are producing. They will be non productive and disruptive 50-70 years forward.

This is not a personal attack on individuals or their situation, but the reality of bad policy.

Could it be considered fiscally irresponsible to have not created enough future tax payers to cover your own universal super?

No, but it is an environmental necessity.

The best way forward to to broaden the way in which we collect taxes. Introduce a CGT or LVT we can use revenue from this to offer lower income taxes while still providing the same level of public service.

You don't consider parenting an important job which can set children up for a lifetime of success rather than children being effectively institutionalised? Have you seen how children behave who are fulltime in daycare? Have you not noticed a considerable reduction in the functioning of society since daycare became the norm? (No disrespect here to parents who feel they should or don't think they have a choice but to put their kids in daycare to earn / continue to develop their careers).

Every human in our society can agree that the current system of making the product of our labor the property of the government (income tax) has created an unfair and unjust society. It's in all our best interests to work together to figure out how we can fund the government without discouraging workers from earning an income.

In today’s modern age, where incomes are increasingly being earned in Bitcoin, the effects of income tax on New Zealand dollars deter people from purchasing NZD. Why buy NZD and pay a 30–40% surcharge (income tax) when you can simply spend Bitcoin directly? The income tax system also creates significant inequities, providing wealthy businesspeople and accountants who shield them from liability with unfair advantages. For example, business owners can expense cars, meals, and other costs, leaving the ordinary salary worker to bear the brunt of the tax burden.

If income tax were eliminated, the additional income in workers' pockets would still effectively be taxed at 15% through GST when spent, so it’s not accurate to call this a complete loss of revenue for the government. Furthermore, the best opportunity to raise tax revenue might lie in an electricity levy. A modest 2-cent/kWh levy would cost the average household only a few hundred dollars annually but could generate billions in revenue. Crucially, this burden would fall disproportionately on non-human entities like industrial and commercial users, rather than individuals.

This approach would also align the government with the private sector’s goals to significantly expand sustainable electricity generation in New Zealand, fostering growth and innovation while creating a fairer tax system for everyone.

Trouble is for some reason the general voter consensus is that the status-quo of income tax being better than any other form of tax is totally ingrained. There is so many other ways, Tobin tax, wealth, land tax. And so much to be gained by lowering rates by broadening the base. Voters HATE the idea.

Problem with that James is you'll be making a huge inflation problem from a cost perspective. What do you think will happen to construction prices if the big steel manufacturers get wacked with a 10%-15% increase in costs let alone all other big manufacturing items.

Inflation occurs due to currency debasement, such as when a government cannot attract foreign investors to lend it capital and instead relies on the central bank to print money out of thin air. This dilutes the value of everyone else's dollars, making each dollar worth slightly less.

For major industrial users of New Zealand's electricity—like Australia's Rio Tinto (13% of NZ's electricity), one of the world's most profitable companies—a 2-cent levy could represent a significant cost increase, potentially as much as 30%, given the dirt-cheap rates they currently enjoy. However, if they cannot afford to pay, there is a long line of zero-emission Bitcoin data centers eager to utilize the electricity.

It's worth noting that the current rates, about 5 cents NZD per kWh, were roughly equivalent to 5 cents USD a decade ago. Due to the devaluation of the Kiwi dollar, this is now closer to 2 cents USD per kWh. Even with a levy increasing it to 7 cents per kWh, New Zealand would still offer some of the world's cheapest electricity at only 3-4 cents USD per kWh.

"Inflation occurs due to currency debasement,"

Are you sure that is the only reason?

Improved Education and Contraception options for the Māori and PIs would be a good solution. It’s the poor young women having kids is the problem.

Not Pakeha Golfer...why's that? Oh that's right the Pakeha women are all rich and sorted?

I'm surprised interest allowed such blatantly racist comments.

Simplistic generalisation with little grounding

Wow, naive narrow minded racists still exist.

Interest, the thread was displaying the usual high level of community intellect with balanced, problem identification of cause & effect, plus creative solutions.....until the ignorant hit the keyboard

Golfer,

And might these 'improved contraception options' include forced sterilization of those deemed not to be responsible?

Perhaps you should stick to golf.

Amazing how triggered some become when statistically correct statements are made.

when we had our 2nd kid , with day care costs , we realised my wife was essentially working 40 hours a week for nothing. double whammy of increased daycare costs and wff gone. worst thing is , been self employed , you dont realise till the end of year accounts have been finalised.

We lost 13,000 of wff in (2018 from memory). Ran own company, wife was at home. Didn't find out till July the following year. Best part was, they'd determined we were ineligible for half the year, but took the full year away (not related to income level or kids, btw, we just ticked the 'wrong' box).

It was as much fun as when I was a student and my wife looking for work - but because she was under 25, she was meant to be part of my SA.. oh, but I was over 25, so she is ineligible and should get JS... we spent 6 weeks as a couple on a SINGLE person's AS till she found p/t work.

And while I'm ranting, I still hate that incomes are not assessed per household for tax purposes, but abatement rates are! Loved paying me that extra 10k tax per year.

I'm over 70 now. I remember loading a 20 foot shipping container as a temporary employee when I was on the DPB, a solo father with 2 boys at primary school, in my early 30s at the local milk factory by hand. More than 20 pallets loaded with 20Kg bags of milk powder to be carried by hand and stacked in the container from floor to roof starting at the back of the container. I did the first 3 hours on my own as no other staff were available. At $10 per hour I filled more than 2/3rds of the container on my own and for the 4th hour a team turned up to finish the job. I was taxed at 70%, so only effectively earned $3 per hour. I stopped work a few weeks later because when my additional income exceeded about $3000 p.a. and I then would have been taxed at 90%. The situation made me very angry at the time, but to work for $1 per hour was very offensive. What motivates the people who determine similar tax rules which clearly still continue to this day. Stupidity?, Malice?, Ignorance? I'd like to have the reasoning clearly written down, explained and justified by the persons who make and implement these distorting and punitive economic decisions.

How were you taxed at 70 or 90% I don’t understand

Did you read the article, EMTR.

benefit been reduced by almost as much as what he was earning. saw this happen in the 1990s with task force green workers. They at least helped them with transport to work, because if they paid for travel to get to work they were actually losing money working. Crazy.

So much structural inequity in NZ against low income parents, particularly solo parents.

Kee up the good work Terry. It seems entirely pointless to disincentivise parents to work or they are effectively penalised financially for doing so. We should be ensuring that nobody goes backwards from trying to progress their career, engage in work and succeed. Think of the compounding effect this would have on govt tax take, and ones lifetime earnings if they turn down a pay rise or don't seek a promotion as they end up with less money at the end of the week if they do. Despite the complexity of ACC levies, EFF and accomodation supplements among other benefits, we have the technology to solve this, we just need the political will.

Would like to know if child support is taxed as part of the single parent income? It is left out of this discussion both at the paying and the receiving end. For the payer it’s another often crippling tax and is disincentivising income for the payee.

Paying parents can end up with an only few cents in the dollar from a pay increase due to child support and inside this discussion there are a lot of them.

Stunning how few comments there are on Trump's billionaire mates sucking revenues out of NZ while paying next to zero tax on those revenues. And, I should add, leaving NZ businesses and workers to pay extra tax to make up for this.

Kiwis really aren't that bright. Or maybe looking over the fence and blaming their neighbors for everything has become so entrenched they can think of nothing else?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.