Late last month, the Performance Improvement Review of Inland Revenue was released. This fascinating document concluded Inland Revenue (IR) was a “high performing organisation”.

The review had been carried out in mid to late 2023 on behalf of the Public Service Commission. This is part of the general Performance Improvement Review programme which is an initiative designed to lift agencies and system performances across the whole of public service. These reviews are intended to be forward-looking and identifying what's expected from the relevant agency or system over the next four to 10 years.

Now that all sounds pretty dry, but once you dive into the detail of the 60-odd page report it turns out to be extremely interesting. It gives us a clear sense of where IR is at right now, where it is expected to be and where it is expected to go over the next 10 years. It's actually one of the few occasions we get a review of IR by external reviewers. So, in that regard it's probably carries more weight than IR’s own annual report.

The review was led by the highly experienced Belinda Clark, QSO and David Smol, QSO, both former senior public servants. And it draws from publicly available IR documents plus a number of interviews, not only with IR staff, but across professional bodies such as the Chartered Accountants of Australia and New Zealand, the New Zealand Law Society, and the Accountants and Tax Agents Institute of New Zealand. Other bodies that it spoke to include the Citizens Advice Bureau, the four big accounting firms, software providers, trade unions and other government departments notably the Ministry of Social Development and Treasury.

“A solid foundation”

The new Commissioner of Inland Revenue, Peter Mersi, who took over in July 2023, welcomed the report, saying it had come at an opportune time following the completion of the Business Transformation Programme in mid-2022, which, in his words, “has created a solid foundation for us to build on as we look to the future.”

The impact of IR’s Business Transformation Programme is something of a recurring theme to the report, which highlights the benefits that have already been achieved so far, and what could be developed in the future.

The report breaks down into several parts. First of all is the context which sets out the scope of the review and IR’s mandate and functions. It's worth keeping in mind that not only is IR responsible for collecting 80% of all government revenue through the tax system, it also administers substantial social policies, such as Working for Families, the Student Loan Scheme and Child Support. It is an extremely wide range of responsibilities.

The report then moves on to the Future Excellence Horizon, looks at IR’s delivery and capability, and finally there are six appendices attached to the report. Appendix Three – Ratings overview and Appendix Four - List of future focus areas, are both well worth looking at.

“Delivering a world-leading tax system”

The Future Excellence Horizon section was developed by the reviewers in consultation with IR and the Public Service Commission. The purpose of that section is to answer the question

“What is the contribution New Zealanders need from the agency in the medium term?”

This section outlines the goal that IR is working towards. All ratings and discussions in the rest of the report are framed in reference to the contributions defined in this particular section. What outcomes are expected in the future, and what IR contributions are necessary to deliver these future outcomes? And the key outcomes are summarised as

“delivering a world leading tax system, remaining at the frontier for best practise for tax systems internationally, and for IR and the wider public service to leverage the capabilities delivered through Business Transformation to administer social programmes effectively and efficiently and deliver simpler and more integrated services at lower cost.”

What's notable here is IR is also tasked with making it easier for SMEs, micro businesses and the self-employed, to calculate tax due and move towards real time tax payments. There is to be targeted engagement with what are described as “less compliant sectors”, and sufficient enforcement action to retain public confidence in the system. This is a very important statutory role, under Section 6 of the Tax Administration Act, which makes it the duty of every official and minister involved in the administration of the various tax acts to maintain public perception of the integrity of the tax system.

Integrated public services

IR is also required to help delivery of simpler, more integrated public services at lower cost. The report notes that delivery of most public services is still optimised within, rather than across agencies. And that's something that we heard when I was on the Small Business Council. The issues around providing information to one government agency such as IR and then having to provide the same details again to another government agency. The general public tends to see the public service as a single body, rather than the collection of agencies it actually is. So here is something that all government agencies really need to work on to try and get away from their silo approach and make it easier for the public and businesses to interact across various agencies.

IR’s core functions and how it performed

Section Four then looks at how IR uses its capability to deliver key functions. The areas rated are:

- Responding to Government priorities and serving Ministers

- Stewardship

- Core Function One - administering the collection and assessment of tax revenue

- Core Function Two - administering social policy programmes

- Core Function Three - providing end to end tax policy advice

- Core Function Four - collaborating with other agencies to simplify and integrate government services.

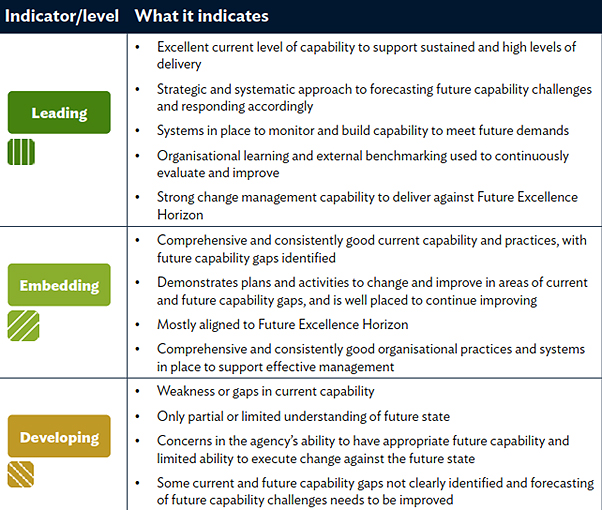

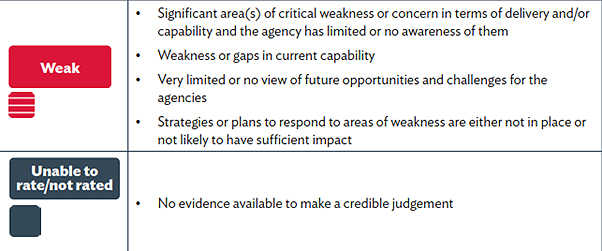

And each of those roles is assessed and rated on a five-point scale.

IR was rated as leading in 11 categories, embedding in a further 13 and developing in just three. So overall you can understand why it got the description of being a high performing organisation.

That's explained in a little bit more detail in the section discussing its delivery in, responding to Government priorities and serving Ministers. Page 25 of the report notes,

“there is widespread acknowledgment within the public service that they were the only agency that could have delivered these services in the required time frame (and this is in relation to the COVID-19 pandemic). Feedback from interviewees is that IR’s response was exceptional, with substantial contributions to several programmes, including the wage subsidy, small businesses loans and cost of living payments. Each of which leveraged capabilities created through Business Transformation. After the event reviews, such as the review by the Office of the Auditor General, supported this positive feedback”.

IR got a “leading” rating for how it responds to Government priorities and an “embedding” in how it provided advice and services to Ministers. An interesting comment here is that “Indirect feedback suggests that IR did a good job in developing an evidence base to enable ministers to consider potential wealth taxes.” (This was under the last Government).

Partner agencies, however, were more mixed in their feedback about IR’s responsiveness to priorities in social policy or related portfolios in the absence of COVID-19 pandemic like urgency.

It was rated as embedding in relation to the stewardship of the tax system. People were generally positive. This is where the support continues the Generic Tax Policy Process (GTPP), which underpins IR stewardship of matters. IR and interviewees see the GTPP as having provided fairly stable tax policy settings since the late 1980s, early 1990s. That's pretty true. Listeners will well know the GTPP is well regarded and seen as absolutely crucial by all tax advisors as integral to the running of our tax system.

On the core function one, administering the assessment and collection of tax revenue, IR got leading ratings in both sections here with high praise from interviewees.

“External interviewees spoke positively of IR’s capabilities and performance, and that included interviewees with experience working in multiple tax jurisdictions.”

I deal with several tax jurisdictions and yes, I would say, IR is actually extremely efficient. We probably don't acknowledge this enough.

An unusual situation?

There was a thought-provoking comment on something we probably don't appreciate is that New Zealand is quite unusual in having the tax policy function sitting inside IR, the tax administration agency. In most comparable jurisdictions, the Treasury leads tax policy. That's the case in Australia and in the UK. It's seen as an advantage for us to have the policy sitting inside administration, as that means the dual function can be used to improve policy and delivery. I’m not quite so sure about that point, but still, it is an interesting point of difference.

“A greater data and technology capability”

Coming back to the importance of Business Transformation (BT), the report notes:

“[It] has delivered IR a greater data and technology capability than most other agencies have. BT has also strengthened IR’s capability to deliver social policy programmes. However, and this creates a risk which IR is well aware of, is that the delivery of social policy programmes compromises the role of administration of the tax system.” External parties noted a big reduction in IRs ability to engage on tax issues when its focus was on delivering initiatives related to the COVID-19 pandemic”

During the pandemic this was something we definitely noticed as tax agents, and it's interesting to see this reflected in the report.

This speaks to something which the report fences around, which is does IR have enough resources to do what it is being asked to do? The report notes that about 1,000, roughly a quarter of IR staff, are responsible for administering the social policy programmes

The hibernating bear has woken up…

External IR interviewees stressed the importance of IR putting ‘boots on the ground’ and IR has responded to that by stepping up “the visibility of compliance and enforcement activity.” Hayden Wood of the GreenLine accounting and tax advisory firm, put it neatly on LinkedIn last week when he commented that IR having now got past all the work it had to do in relation to Business Transformation and the pandemic, was now returning to its core duties and is like a bear that has just woken up from a long hibernation and it's hungry.

We've seen that in recent weeks: firstly the media announcements they’re looking into smaller liquor outlets, then the discussion we had regarding what's happening in the cryptoasset space. This week there were a couple of media releases involving sentencing of people convicted of tax fraud and tax evasion.

Then on Friday IR released more details about what it's proposing with the extra $29 million a year it's receiving to improve tax compliance. $4 million dollars of that is going to go to student loan enforcement. In summary we're going to see much more activity from IR.

Measuring the tax gap

The section regarding IR’s provision of end-to-end tax policy advice which rated it “leading” did identify one weakness in the absence of the measurement of the tax gap - the difference in the amount between taxes legally owed and the tax collected. In response IR noted the technical challenges in estimating the size of the tax gap but acknowledged that it would be valuable to do so. That’s something HM Revenue & Customs in the UK has been reporting about and I think there’s similar commentary from the Australian Tax Office/Australian Treasury on this issue.

As the report notes tackling the tax gap has the potential to enhance trust and confidence in the system. This is very true. If people perceive that there is exploitation of the system, it's not being managed as it should be, then non-compliance will increase. So that's a pretty big issue that IR will need to manage.

Play nice with other agencies?

IR was rated as leading in Core function three - the administration of social policy programmes. Again, rated as leading. But there's some commentary about the difficulties of managing Working for Families payments and how recipients may find they've got a bill retrospectively. The review that 67% of those receiving Working For Families who received payments during the year were paid within 20% of what they're entitled to. This suggests maybe half may have been underpaid or overpaid during the year. But accurate real time payments are difficult at the present.

The review comments that IR is legitimately protective of its IT system and data sets in order that they ensure that they keep operating effectively and efficiently. IR is also very concerned, rightly so, about data leaks.

But as the review goes on,

“IR will nonetheless need to be open to making an increased contribution in the social policy area. Feedback from other agencies was that IR is not very flexible in assuming these further rules. While IR agrees to help from the perspective of the other agencies, the help is always on IR’s terms and not always what is required.”

In other words, remember to play nicely with the other agencies.

Collaborating with other agencies – room for improvement

Those comments from other agencies feeds into core function four – collaborating with other agencies to simplify and integrate government services. IR only gets a developing capability rating here. And clearly that ties into IR’s approach. According to the review interviewees from IRand other government agencies, “had diverse views on what future collaborations might look like.” Other agencies are clearly looking at IR’s great capabilities and wanting to make more use of them. In turn, IR are saying well, maybe, but you have to do it our way. Watch this space.

The rest of the report on IR’s capability looks at what's called a targeted consideration of each element of an agency; capability, such as leadership, culture and direction, collaboration and delivery and workforce. Generally, IR is rated as either “leading” or “embedding”, with the exception of workforce performance - what is the agency's capability to deliver, promote and develop a high performing workforce, where it is rated as “developing”.

There was commentary from IR staff that they felt parts of the Business Transformation Programme had not been well managed and there were some “residual feelings” about how certain episodes had happened.

It's noted by the way that the average tenure of IR staff following the completion of Business Transformation is still around 13 years, which apparently is high for the public service. And then there is a large number of staff apparently with 30 or more years of service probably including quite a few in the tax policy area.

Managing its money

In relation to public finance and resource management IR didn't get any leading ratings here, just all embedding. There was commentary that although IR’s baseline operating costs are some 15% lower than previously, for example in 2018 it cost $0.80 to collect every $100.00 of revenue, and in 2023 that had fallen to $0.43 – it apparently has had a practise or a habit of underspending its appropriation. And because that appropriation is so multi-category, it's then often able to take under spends in one category and allocate them to others. Basically, the reviewers are saying it can't do that in the future because the public service is expected to manage its finances better.

That's true, but as we noted earlier, there were some issues around IR not delivering as servicing certain areas, and there was also commentary that you can expect that is has to deliver more. So, I don't quite see how those two comments tie up.

Furthermore, and a point of concern for me, the review noted that IR’s START computer system seems to be not quite ready enough to deliver real time tax payments.

An underappreciated risk?

This led on to a very interesting discussion on page 49 of the review around IR’s current contract and relationship with FAST Enterprises, the company that built the current START platform. FAST was established in 1997 and I understand some ex-IR staff were involved in it. It currently has products operating in 95 different government agencies across the United States, Canada and several other jurisdictions such as Finland, Laos, Malaysia and Poland.

The review has the eye-opening comment that “IR is almost entirely reliant on FAST for the platform and software to run START.”

IR currently has an agreement with FAST for seven years, which expires in June 2029. According to the review IR currently has a “close partnership” with FAST and some FAST personnel are embedded within IR but START has been configured, but not customised to accommodate all the social programmes that IR delivers.

Backtracking a bit, in June 2014 there was a tax conference in Wellington about the future of tax administration and what would IR require?

It was fascinating at the time, but one of the most interesting parts for me was watching a very spicy exchange between New Zealand based technology and software companies and IR staff about the Business Transformation project which had just been announced. The New Zealand software companies all felt that they had been locked out of the process and were rightly aggrieved about it. The feeling was that they could have done the job for less than the $1.5 billion quoted and in faster time. One cited they'd managed to get the GST system for, I think it was Bermuda, up and running inside 18 months.

Those software companies will probably have a certain wry smile when they see these comments:

“We queried why such a critical dependency was not higher on IR’s risk radar. Expectations from IR and FAST are that the contract will roll over once the seven-year term ends. But this is not something that should be taken for granted.”

I would totally agree with that. I'd like to see this watched carefully in the future.

Overall, when you read this review, it has lots of interesting insights about IR. With its increased activities in the recent weeks, it's fair to describe it as a high performing agency.

And on that note, that's all for this week, I’m Terry Baucher and you can find this podcast on my website www.baucher.tax or wherever you get your podcasts. Thank you for listening and please send me your feedback and tell your friends and clients. Until next time, kia pai to rā. Have a great day.

4 Comments

Always an interesting read. Thanks Terry.

maintain public perception of the integrity of the tax system

Thank goodness it's only the 'public perception' they need to worry about!

Wrap that one in a KPI.

Reminds me of when I was gainfully employed...loads of buzzwords, and probably very little action.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.