There was a sharp increase in the number of homes listed for sale in September, adding to signs that the market could be reasonably buoyant over spring and summer.

Property website Realestate.co.nz received 10,372 new listings last month, up 11.7% compared to September last year.

The increase in listings was led by Auckland where listings were up a massive 31.9% compared to a year earlier, followed by Southland +21.2%, Northland +13.7, Wellington +13.5%, Waikato +8.4%, and Central Otago Lakes +5.8% (see the chart below for new listings in all regions).

The jump in new listings also helped to push up the total number of homes that were available for sale on the website, which increased to 22,847 at the end of September, up 5.2% compared to the same time last year.

The increase in the total number of homes for sale was also led by Auckland, where stock levels were up 17.7% compared to a year ago, followed by Nelson Bays +16.1%, Waikato +11.3% and Canterbury +8.2%.

The number of people viewing properties on the Realestate.co.nz website was also up, 838,706 people looking at listings on te site in September, a level which is usually only seen in the peak summer months.

Realestatate.co.nz spokesperson Vanessa Taylor said the increase in listings would benefit sellers as well as buyers.

"In this market it's less daunting to think about selling your home because there are more replacement choices," she said.

Asking prices are also holding up, with September's average asking price up 5.3% compared to August and up 11.1% compared to September last year.

Housing inventory

Select chart tabs

164 Comments

A song for the housing market.

https://www.youtube.com/watch?v=1XmwiwQjU8E

Foreign buyers, 'Since you ain't around my whole world's upside down'

And for those that like data to go with their music. (re-post from Friday)

Since Trademe broke at 32,000 listings the other day, as recommended by a fellow commentator we will switch to the realestate.co.nz site for future updates on the burgeoning supply of unsold properties around the Country.

Total NZ has risen from 33,448 (realestate.co.nz figures) on Wednesday to 33,728 this evening (A rise of 0.83% in 2 days). Before Trade broke, there had already been a 5.2% increase in the overhang of stock since 21st August.

Auckland has also seen a rise and now stands at 12,681 unsold homes (There were 2860 sales in August REINZ figures apparently with an average selling time of 42 days - see below) However by my calculations there is already stock in the market for 4.43 months of sales supply (132 days supply ) which would leave me to question the accuracy of the days to sell stats, which won't be near 132 but are likely to be a lot longer than 42.

https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2018/Residen...

(Bizarrely, there are quite a number of New Listings with Auctions scheduled for the 17th, 18th, 19th of October)

The spring rise in listings this year is definitely earlier and/or sharper than last year. Unclear though how much of that is down to the election last year, and a possible rush to beat the ban this year.

The days to sell stats are rubbish. I am starting to see more and more properties being relisted that failed to sell a few months ago.

Yup, everyone is rushing to auction before the 22nd of October (FBB). Not subtle at all.

I've seen a little mini rush of Chinese people visiting the property next to us which otherwise has had very little interest last 6 months. Interestingly a couple of very young couples. Looking to buy for ma and pa before 22 October? Bout time this nonsense ceased.

Be interesting more stock to choose from if prices will drop further around the main areas as sellers have to adjust their expectations. Banks lowering mortgage rates.

100% success rate at The Block auctions. No better scientific indication that things are looking good for the housing market.

You'd hope so. They had a 2 month TV marketing campaign. Plus low reserves to avoid last years debacle. So teams actually left with something.

Yes. If it wasn't obvious, I was joking - I don't actually think this is a scientific gauge of the housing market.

Very insightful. Thanks for such sound analysis of the market.

Yes because of the high profile the Property Industry have a financial interest in the success of the event. There's no way they would have let those crappy terraced boxes go unsold, gotta keep the game going, the figures rigged :) There realistically worth around $600-$700K to a working Kiwi.

The reserves were set well under the median price for a 3 bedroom house in that area, despite them being in the best part of the area, and coming fully furnished.

Plenty of supply in Auckland, the question is will there be demand from potential buyers...

Im guessing the answer will be no, we will see inventory rise and sales number stay really low.

there will be 14000+ for sale on realestate.co.nz in Auckland by the end of summer currently at 12695.

I'll wager over 14,000 Auckland listing before the middle of November and over 15,000 by Christmas. The level of growth in stock and lack of sales will escalate this rapidly. Plus if asking prices have gone up, vendors are still in dreamworld so sales for September and October are likely to be very sticky.

Stock breeds stock, for a few years now the market has been starved but, as buyers see things not selling and opportunity to trade up for a decreased differential the number of 'would be' traders will continue to climb. Will the first time buyers be able to prop it all up though? Remember if those that are not in the market choose not buy then values for everyone else and perceptions of equity are meaningless - Just ask the Aussies!

As far as Auckland and Wellington are concerned, listings might well increase in the further out, less sought-after localities - especially for run-down dwellings.

But listings for good properties (especially houses) in the central suburbs remain scarce - and are destined to stay that way.

TTP

You could be right about those central suburbs.

Residents are likely to 'get trapped' by a fall in equity and are not able to leave, even if they wish, as the lenders will have the final say over what price they can escape at. Not all will want to leave, of course, but markets never stand still, no matter what they are, and at some stage, sales will happen, and that will either allow others to move alongside them or further entrench their capture.

Hi bw,

Property in the central suburbs (Wellington & Auckland) is tightly held. People don't give up their trophies easily.

You should also note that a big chunk of these properties are unencumbered - no mortgage on them.

TTP

Ah. Trophy Properties! That's different to Central Suburbs in my book. But....

I know people with trophy properties, and from past experience, they are pledged, one way or another, to other financing arrangements. Why would you let the finance power available in a property to sit idle? Even if it's just a Negative Pledge.

And if push-comes-to-shove elsewhere in the Empire, property sales are forced! But, we shall see....

Data source for this sweeping statement please...

bw not everyone is in the position that perhaps you're in, there are plenty of people with capital and plenty of people with great cash flows who will buy and sell to meet their life needs and value their homes in well established suburbs close to the city in short we are not all peasants !

And my apologies if you think my post is suggesting such.

I have nothing but full support for those who "value their homes ". That's how it should be. Where I have an issue is the general mania that has developed over the last 3 odd decades of 'let's get rich by speculation in those homes!". It devalues life for all of us if we did but realises it.

As you'll read below, our son has bought his second home - the only one he owns - and he has done so, so that he and his partner can start a family with the sense of security that owning a home gives. It's not home ownership that is the problem - it's speculation by those who really can't afford to lose.... Speculate all you like if you can afford a negative outcome; that's how markets work. But just as surely as they do, markets fall as well as rise.

Is more than 100 listings in Remuera a reflection of scarcity? I had a look at the number of dwellings on the stats site and it indicated;

There are 1,308 occupied dwellings and 87 unoccupied dwellings in Remuera South.

No idea whether stats 'Remuera South' area aligns to Remuera (as per TradeMe geographic area for the suburb) or not.

But if we consider Wellington Central or Khandallah in comparison both have only 30-odd listings each.

That's well over 2 months worth of inventory for Remuera, then.

Generally they are averaging around 45 sales per month for the 3rd quarter, over the past 6 years.

Where did you get those Stats from?

I have followed Remuera listings on Trade Me for a while. Typically at the quietest time of year listings drop to around 80 (sometimes a little lower) and at the busiest listings are in the 140's. Geographically Remuera is a really big suburb - also anyone in a surrounding suburb Meadowbank/St Johns etc tends to list under Remuera.

But there is no doubt the quality of property available is getting better - two years ago rubbish properties were snapped up. Today there are nice homes not selling at auction, sitting for a while and then being taken off and put back on months later.

"But listings for good properties (especially houses) in the central suburbs remain scarce - and are destined to stay that way"

Can I borrow your crystal ball ? Mines broken obviously.

People who own or can afford to own in those central suburbs make up a small proportion of the population. They are like an island and are relatively meaningless for the overall market.

The market has a long way South to go before it could be regarded as fair value or even "affordable"

Auckland listings up 31.9% - far outstripping everywhere else in the nation - that's got to be good news.

That seems a significantly sized movement indeed.

I’d focus on inventory - up 17.7% but still it’s a big increase considering there was a lot on the market last year. I imagine the comparisons to 2015 and 2016 would show higher growth again. The trend is still emerging but if this trend continues the market is going to get very soft. The current prices were built on FOMO, certainly no reason for FOMO now.

The inventory chart at the bottom of the piece is also really interesting. Both Auckland and Canterbury have much higher levels of inventory in their regions than the national average - whereas Wellington has below the national average. Perhaps however it has always been that way?

Wellington is pretty tight at the best of times. The geography isn’t as conducive to increasing supply. And it’s already done a lot of intensification. Plus, remember that although prices have risen in Wellington they are still far cheaper relative to incomes than Auckland.

Add, a lower percentage of incomes are susceptible to changes in the real economy. Shall we call it a government backed guarantee?

I’m watching the news and realestate.co.nz are spinning this as ‘confidence’. Yeah Right.

Their logic is awesome. Basically NZers list their houses when they think they can sell them for a good price, therefore, any time there are lots of houses on the market it must be a sign of confidence. You can’t make this stuff up. Later she did admit it is a buyers market and sellers have to be realistic.

Yeah... saw that interview. Classic.

Lot's of listings means prices will go up, she said. Hmm. Also, because average asking price was higher. Hmmm, higher asking prices on a rising inventory....

Don't forget Wellington has had a couple of significant property mini-slumps in the last 20 years

The reported increase in page viewings is more than likely a story of elevated anxiety. Many a speculator will be concerned about their own fate at this high altitude.

Its all the upcoming sellers trying to get a handle on what they should ask for their property when they list it next month.

Didn’t see ‘The Block” auction as overseas.

However I think the prices received were really good considering what was being offered.

4 attached box’s, painted by amateurs and situated miles from Auckland in a pretty average location of Hobsonville!

Reserves were lower because the cost of the property to originally buy being attached units in a poorer location always meant lower reserves I would’ve thought!,

The participants didn’t seem to do a helluva lot of work this series compared to previous series.

Good luck to the buyers as I think they may need it!

Fully furnished too yes?

...the very best appliances was reported as another drawcard!

I agree the prices were good considering what was being offered. People forget that we are talking about prices in the order of $1M for terraced 3 bedroom units in West Auckland (albeit new and fully furnished to a very high standard).

Before the block came around, Jalcon were advertising the houses as 1.1 / 1.2 millionish.

To see them go for 200k under that mark, while being fully furnished was quite telling.

I've got the screenshots, but don't think I can attach them at all.

average profit $42K

The word 'profit' in the block scenario is fiction. There may well be zero profit.

The selling price was the only point of interest, but after the biggest real estate marketing campaign of the year, that too is distorted.

In the case of 'the block' profit from the auction is whatever you want it to be.

Hi Munter,

1.1M/1.2M is way above the area's median, and is high even factoring in the fact that the units are furnished. That was never going to happen. The median price for 3-bedroom homes for the 3 months ending August 2018 was $968,888. A developer/builder talking up prices shouldn't come as a surprise, and advertised prices often don't reflect the market or actual value.

Most people would agree that in a flat market, +- $1M for a 3 bedroom terraced unit in what is essentially west Auckland is a high.

The winning property sold for 4.2% above the Hobsonville Point median price for a 3 bedroom home despite being fully furnished, and two sold for well below the median price.

Being a CHCH rental tycoon Man where did you travel, NY, London, Paris...let me guess Brisbane!

Frazz, no not Oz this time.

Went to Vegas, now thru the Canadian Rockies and next a week in New York!

Why do you ask, did you want to carry the suitcases?

Presumably, if you're away for 21 days you've appointed an agent for your serfs, I mean tenants

https://www.tenancy.govt.nz/ending-a-tenancy/change-of-landlord-or-tena…

dp

Small anecdote from Christchurch. Sold in-law's home (front, sunny unit of a two-sausage string): 10% above a 2017 RV, 14 days on market with a deadline sale, two offers, higher accepted, settled last Friday. No fuss no muss. Buyer had been searching for this type of accommodation for 18 months. Enough Anecdotes, and ya has Data. Or if in China, "data".

...and another, from ChCh; this Saturday.

Son; keen on a particular property - his second step on the proverbial ladder, asking $660k. I suggested offer at $540K, but he was too embarrassed! But I relented and he bid $580k. Counter $639k. Son came back at $600k. Countered at $629k. I asked him to withdraw his offer ( being a financial crutch and all!). "Done @ 600k!" Settles in 4 weeks.

Any idea what the previous owner paid for it?

New build. Only 3 years old, and this is the first transfer. Nice. Hebel on an acre on the outskirts. Oh, and current owner is....a real estate agent! Now if she is calling it quits! ( although to be fair, she has a 'subject to sale of' on her next house)

And a third, despite an auction that garnered no bids, and little interest throughout the open homes, a post auction offer for a 3 year old 3 bedroom home was rejected, and it was put on the market for $100k more. Despite the fact that a brand new 4 bedroom home could be built down the road for $15k more than the offer price. The property has subsequently been withdrawn from the market.

Am I missing something here? A big jump in sales would indicate a buoyant market. A big jump in listings to me indicates people heading for the exits.

Indeed. Perhaps the dismal Block auction was the RE equivalent of yelling 'Fire' in a crowded theatre. In short, FONGO......

My sentiments exactly.

Good point Doris

Yep. Edge of precipice stuff. Auckland prices will be down 5-10% this time next year

Economy is slowing down. Look around - look how new car sales are looking? There is a lot of good deals around (cars, sports gear, clothing etc. not mentioning 'interest rate specials!). Manufacturing is slow, trade related to manufacturing is slow. Construction projects are still pulling but in general i see the clouds gathering.

Housing will be no different - in 3-6 months time there will be a different story in terms of mortgage approval.

Interesting summer in front of us...

Indeed, its a nice time to be on the sideline

Surely this massive increase in listings points to the beginning of a potential panic, as opposed to a buoyant market.

I have to say I have serious doubts. When people are buying investment properties in places like Levin and Dargaville, surely that means the property market is completely out of whack with reality.

Of course, there'd have to be a correction of around 50% for Wellington or Auckland to be worth it to me. And if that happened I'd likely be out of a job anyway!

I think you'd only start to see noteworthy downward pressure on prices if there was a sharp increase in interest rates, an external shock affecting key trading partners, and/or a significant rise in NZ employment. Elevated inventory will have some downward pressure, but unless there is a market change that affects home owners'/investors' ability to pay their mortgages, I think things are going to stay flat.

You're still thinking about cost of credit and neglecting availability of credit BLSH. which is being rationed by around 20% to new borrowers.

Further to that, just a 1 point rise in rates is for many a 20%-25% increase in cost of debt servicing... and inflation is starting to play its card as the dollar weakens and global oil prices go up and no amount of watching TV programs hosted by Mark Richardson is going to spare those that are over-leveraged.

Nic, do you ever take a moment to think that you might be wrong? You always post with such certainty.

I genuinely hope you have a backup plan if the market doesn't go the way you think (hope?) it will.

Hi saving4.

Answer to first question - No.

Have you ever had a sense of deja-vu? When you've seen things happen before and it all seems very familiar. When the banks have been lending like Northern Rock to people who just wanted to buy that house but didn't have the brains to work out what they were signing up for and then it all got a bit silly.

I've not been wrong on anything yet, time will tell and all I'm doing is offering a few warnings to those that haven't seen this before and are therefore at greatest risk of permanently damaging their future.. I'm in the fortunate position of not needing a 'back up' plan, so it actually doesn't matter to me either way. These stock level rises are phenomenal and that doesn't even take into account the volume of properties that have already been withdrawn this year after failed attempts. We're in the 'denail' phase at the start of a bear market in property

http://www.comstockfunds.com/default.aspx?act=Newsletter.aspx&category=…

It makes it very hard to take you seriously if you don't appreciate the potential for you to be wrong. Although I may have opinions, in reality I don't know where house prices will be even in one year let alone further out. Neither does anyone else - there are too many variables, too many moving parts.

When I make investing decisions, it's based on the hope that probabilities are in my favour, not the certainty that what I think will happen will indeed happen.

mfd.

There is nothing out there suggesting any form of strength in the market. All indicators are negative towards NZ housing. The moment I see something to the contrary I'll be happy to recognise it. I don't know where exactly house prices will be in 12 months time, only that they will be a lot lower and that that won't be the end of it. Unlike many others I have provided lots of information over the last few months to qualify my reasoning. In the case of the NZ property market, gravity is going to leave a nasty bruise and even the spruikers on TV, in the papers and even today's cheery headline from Greg are not a true reflection of how weak this market is getting in a hurry.

Nic

The only bit of data that hasn't lined up just yet is actual prices. In the country as a whole, prices are still rising a little, in the most expensive areas they're essentially flat, down a little in real terms. No real knock-out data showing that house prices are actually falling significantly just yet, although that may come soon. All part of the array of probabilities spread out ahead of us.

Negative interest rates and some more QE are a possibility. Universal income and huge wage inflation are also a possibility.

Hi Nimbo

RBNZ and NZ economy doesn't have enough influence for NZ QE or lower rates to do anything other than collapse the NZ dollar and cause a massive rise in the 20% of funding that our banks get off-shore. We're not the Fed, BofE, ECB, BofJ. We are a little economy, slightly smaller than the value of Apple, with quite a lot of household debt and an economy reliant on a lot of Tourism and a few primary industries (several which are also heavily indebted - Fonterra). Everything we import (because we produce naff all really) gets incredibly expensive if the NZ dollar collapses. It's just not a policy option and people are dreaming if they think it is. The rhetoric from the Reserve bank is just that, rhetoric to steady the ship.

Lots of people think that inflation will get them out of it but inflation in a global economy works differently to the 1970's as there are now 2.5 billion Indians and Chinese who will hammer the chance of wage rises in NZ to keep up with inflation. Businesses will just ship costs abroad, so unfortunately that old 'get out of debt' card is is not one we have in the deck this time.

You do realise just how powerful the RBNZ can be if the situation arises, right? Seems to me you like you’re just another guy with a poorly thought out view on literally everything.

I get scatter brain reading your comments.

Hey Nic, I have been following your replies on here for a while now and share similar thoughts and sentiment on things. I am an Auckland investor and was extremely bullish on the market until mid 2016 when I saw what was happening in NZ and globally with everything. We are in for a rocky ride ahead and from what I have researched (extensively) I believe we are in for another global downturn. Hopefully I'm wrong. Regardless, keep up the good posts. Those in denial will get a wake up call soon enough.

Hi Adam.

Thanks for your support it's appreciated.

Saving 4

A bit more from a post from earlier....relating to impact of Fed tightening and Oil price rises. This is very relevant, but you'll never see it in the herald which is paid for by the spruikers and purveyors of debt (banks) this will impact our rates sooner rather than later if it continues much longer.

'There are a few similarities to the 2006/2007 period. Fed tightening (see below chart for rate increases June 2004-Nov 2006. (FED rates started rising June 2016 this time around so we're 16 months in now, ie October 2005 equivalent, more to follow over the next 18 months.

Oil price has also doubled since January 2016, (last time around it peaked in June 2008). it's on the way up again.

NB the previous spike 2010-2014 was a liquidity spike from excess QE. It's now rising in an environment where interest rates are going up as well.

https://www.macrotrends.net/2015/fed-funds-rate-historical-chart

https://www.macrotrends.net/1369/crude-oil-price-history-chart

Nic,

Inflation is starting to play its card? No it isn't. Why do you think RBNZ indicating the OCR will remain lower for longer?

Inflation is low currently (1.5% July 2018) and almost all credible economists predicting it to remain at or below 2% for years.

People don't sell their property for cheap unless they are forced to.

'Bank' economists! If you are paid to offer an opinion your paymaster will always have an influence over what gets said.

Literally every economist/agency I’ve found is forecasting low inflation (at or less than 2.1%) for the next few years. What credible source have you found that is predicting high inflation soon? (I’m not saying it doesn’t exist, but I’d be interested to see it).

How do you figure 2.1% is low? Granted it’s not high but it’s high enough to justify taking the foot off the monetary gas.

The inflation forecasts are low enough that RBNZ has said it is expecting to keep the OCR where it is until 2020, with no indication if the next move will be up or down. 2.1% isn’t very low (unless you compare it to the 70s and 80s), but we still have a couple years of lower inflation until we get there - we are only at 1.5% now. At 2.1% RBNZ will start to think about raising rates, but nothing near high enough to cause the property market to crash as Nic Johnson has predicted. He predicted 2.5% OCR by Q4 2020 and 3.5% OCR in 2021 - keeping in mind we are only at 1.75% OCR now. That’s something like 7 rate hikes by 2021. And above Nic is saying that inflation is already (as in today) starting to “play it’s card”.

There's always going to be a percentage of people who *need* to sell. Enough of them - in raw numbers - will lower the asking prices for everyone. "Mum & Dad" landlords are beginning to trickle out of the rental property market as well, looks like a lot of them don't even have the 10k in liquid cash needed to get their rentals up to code!

I actually hope the property spruikers are half right, I have to stay in the country another 2 years. Here's hoping the economy holds steady.

There's always going to be a percentage of people who *need* to sell. Enough of them - in raw numbers - will lower the asking prices for everyone.

I agree with this. However, the number of people being forced to sell is currently quite low. This isn't surprising as interest rates are low, the economy is stable and employment rates remain healthy. I think you have to ask yourself - what are the chances of this picture changing and why?

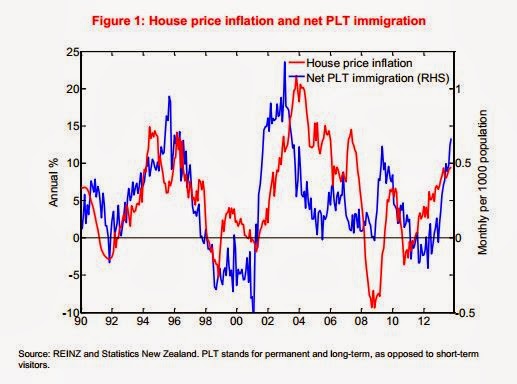

One factor you missed out is immigration. It's already on the decline - the universities and polytechs are feeling it first (Auckland uni crashing down the rankings and Massey University in a fair amount of trouble).

As for unemployment - the worlds two largest economies are on the brink of a trade war. The whole world has no real idea how healthy chinas economy is since none their statistics are reliable. They could be in serious trouble and we don't know it. If they sneeze we will catch a hell of a cold.

I feel like a stiff breeze could knock it over at this point. I don't think it's controversial to point out how over-valued houses are. The higher it gets the more nervous I become.

Yes. I did think about including immigration. I also didn't mention housing supply, or credit availability factors such as LVR restrictions.

There definitely is a close correlation (not necessarily causation) between immigration and house prices. http://3.bp.blogspot.com/-cWO6cw8gchg/UrNpMCkjXII/AAAAAAAAAYw/1wMIIejJW…

{kind=link}

Net migration gain is slowing, but still through the roof.

As for the trade war - there are always external risks, but I think the likelihood of this having a big enough impact to seriously dent NZ exports is low.

I basically don't think people will sell for cheap unless they are forced to, so I think the likelihood of a house price crash without something happening that forces people to sell is low.

Immigration numbers are now irrelevant - from the 22nd of Oct the vast majority of immigrants can not buy houses even if they came here with suitcases of cash. They will however, exacerbate the rental shortage beyond anything seen before.

Many immigrants get permanent residency and would qualify to buy houses though.

How many people are there in the market that don't own a home already. That either have or can access by other means the funds required for a deposit and can also meet the now far more stringent income and expenses criteria of the banks to service a mortgage. These people also have to want to buy (and right now why would they). If there is not enough of these people then there is no liquidity

I fit that criteria perfectly and yes, I’m sitting on my hands regarding buying unless what I deem an amazing opportunity pops up.

Head and heart are very different as I really want to own a home again but head says no so I can understand people still buying but I think the scales might be tipped towards waiting.

In the same boat. Guess I'll sit on my hands and keep renting for now

For all potential FHB, and owner occupiers (especially those who will use a high LVR mortgage to finance such a purchase), an essential read, so that you make a fully informed decision on the largest asset that you will likely purchase. Remember each geographical market is unique.

https://www.globalpropertyguide.com/real-estate-school/How-to-avoid-buy…

Some useful reference links

https://www.interest.co.nz/saving/rental-yield-indicator

https://www.qv.co.nz/property-trends/rental-analysis

https://www.qv.co.nz/property-trends/residential-sales-prices

https://www.interest.co.nz/Charts/Real%20estate/House-price-to-income

Me too. Looking to upgrade, but in no hurry. I can afford to at least wait 6 months post foreign buyer ban to see what effect its having on the high end of the market. I do see listings in the premium suburbs starting to pile up.

Is that spike in Listing the last minute attempts by boomers to get out of Auckland/ Sell their house before it loose 20%-30% ?

Who wouldn't want to get out at a peak though?

Most have well and truly missed that window I'm afraid, apart from those in the know, like Uncle John and his mate Mike.

for Auckland that peak was 18 months ago, but the press have been very good and keeping a lid on reality of rising stock levels, decreasing sales rates and price falls in many suburbs. I wouldn't be surprised if the narrative carries on throughout the crash, being there are so many vested interests who influence the media.

The media will have to start to reveal the truth at some point, (as they are starting to do in Australia) because so far there has been a massive deception of the youth who are still loading up with debt to the tune of nearly $1,000,000,000 a month and the foolish, for whom I have less sympathy.

It's like no one in property understands how a market works.

The message here is that there's a lot more supply coming online so that's going to make the market more 'buoyant', giving the impression prices could hold up or even go up?

In my world supply increasing means downward pressure on prices. But then I just work in markets for a living.

It seems many in the property market have resorted to the belief that if you say something enough it may come true.

Successful Economic model: "Make more things, at a cheaper price with a better quality level"

Failed model: "Make fewer things, at a higher price with a lower quality level"

Which model have we chosen for our residential property market?

Foreign buyers can still build, so not totally out of the market. And consents up recently. Mmmm.

Mr Xi has the printing presses running day & night & the Yuan needs to fall by plenty. So lots to consider.

As for the Block(?) well it certainly was. Reality rules. A lot of hard work for your return. The way it should be.

Asking prices have hit record highs. Not sure what all you doom and gloom merchants are on about....

https://www.stuff.co.nz/business/money/107489929/house-sellers-confiden…

That article has 'Alasdair Campbell' levels of spin attached. Its a thing of beauty (though not grounded in any sense of reality).

"House sellers have reached all-time levels of optimism over the prices they can sell their properties" - all time levels of optimism!! Hahahaha, I love it!!

I wonder if Rob Stock actually wrote it or he was just told to put his name on it so Stuff could publish with a veneer of legitimacy.

Reminds me of this one:

"The number of properties sold in November across New Zealand increased 17.8 per cent from the previous month – the largest October to November increase seen in six years," REINZ has just announced this morning.

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

classic! a bit of premature champagne popping wasnt it!

Brilliant.

I love Anne's 'this is big.....". Said with emphasis and effect!! No wonder she has risen to the lofty heights of Property Editor for a major trade journal, sorry, national news organisation.

Asking prices are not the same as selling prices. Asking prices are the thing that stands in the way of a sale, and results in properties being withdrawn from the market while the vendor tries to find a new real estate agent who will tell them more lies, or a tenant.

Stock levels up 17.7% but asking prices up 11.1% (both on Sept 2017). Somebody is not going together what they want...

I am intrigued by the reference to "asking prices holding up" and the year on year comparison.

Does anyone know where this number comes from and how it is collated.

Surely a year ago the number of houses marketed with a price were far fewer than by auction or by negotiation so doesn't more property with an "asking price" indicate market stress.

If this is a statistic based on a shift in marketing modus then the "holding up" and month on month and year on year comparisons are meaningless.

Finally "asking price" seems an odd statistic to bull given the Auckland market is flat at best or falling..

In a booming market, buyers pay over asking in order to secure the property and agents underquote to attract buyers. In a falling market, vendors accept a discount on asking prices. So asking prices are pretty meaningless in the end. Although in overseas jurisdictions, the discount on asking is a tracked statistic - something someone might want to keep an eye on here.

An unknown statistic with regards to your "vendor discount" is whether a property (or properties) has sold for less than what it could have fetched 12 - 18 months ago. Not all houses on the market have recent sales data to compare to.

While the average sell price remains stable in Auckland, are people getting a better property for the average price than they were 2 years ago i.e. an increase in purchasing power?

My question relates to how the averages and m on m and y on y comparisons are sourced and collated.

Is it based on properties marketed with an asking price on an area by area basis or on REA anecdote?.

As it is being used to "puff" this piece I wondered as to its bona fides.

When you list for sale by auction on Trademe you need to put an actual expected price, This is the stat they use.

Bw, on the outskirts of Christchurch?

Where on the outskirts was this acre with a 3year old home for 600k?

How big was it as well?

Appreciate your answer!!!!!

You'd be lucky to get a quarter acre with a house on it for that in Pegasus, and that's beyond what i'd consider the outskirts of Christchurch.

People are paying well over half a million for houses 25km from christchurch?!?

I don't know whether to laugh or cry. That's both terrifying and hilarious.

You can pay close to a million for the flasher houses in Pegasus and yet Pegasus is a long way out and not that popular

Are you genuinely not concerned by this?

Very average houses 25km out from a very average town cost 10x a decent working class salary?

Do you think this is the sign of a normal and healthy market?

To be fair, we're talking about an above average new house with significant land, and Chch is the 3rd largest city in the country (and the largest on the island).

It's quite possible to find houses in the city in the 300ks if you don't want a lifestyle block.

yeah but dude it's christchurch. The largest town in the south island sure. But that's still the largest town on the least populated island of a kind of obscure country. Do property people have no sense of global perspecitve? I mean look it's nice here. But it's not $600,000 for 25km away from a provincial town of 380,000 nice.

Remember we're probably talking about quite a nice lifestyle block here, not the kind of property most people are looking at. A normal house actually in the city (say, within 15 minutes bike of the city centre) can be had very comfortably for 400k.

Quarter of an acre is not a lifestyle block. It's a big yard.

Ah, we may be talking at cross purposes. I was still referring to bw's example of a 600k 1 acre property on the outskirts of Chch.

A well renovated, older 3 bedroom house on a 1500 sq m section in an upmarket part of the north west of Chch can be bought for under $600k. Or you could get a 4 bedroom on a 2300 sq m section for $700k.

A lot of people live in the south island and fly out of Queenstown or Christchurch internationally on a regular basis for work and entertainment. Time to get out of your bubble. My office is in LA and I live 30 mins from Christchurch in a cheapest property in our area around 1.5 million valuation...most are 3-4 million dollar properties around us.

Of course I am not concerned.

Section price plus build cost of approx 2500 per square metre on the low side plus finishing is replacement cost.

Yes build costs have escalated but you can still buy a liveable unit or home for under $300k in Chch if you want to.

Yes if you want better then work your way up to it like my generation did.

If you are prepared to get off your butt and not exoect everything to come to you then you can do well.

Wow those values in Christchurch are lower than I expected them to be. Reflects the fact that it is not a place to move to. Expect them to continue to drop.

The (comparatively) low house prices are one of the reasons I like it. It's an attraction, not a turn off. Here I can buy a house, save a bunch of money, and afford some toys and a good life.

What values Gordon?

You can get a 2bedroom small unit for $260k in less desireable areas.

You can buy a 3 bedroom smaller home in the cheaper areas for over $300k

You can buy a reasonable house in a average area for $450k

New houses anything over $500k.

We have bought far better than this though Gordon, which I know will totally annoy you!!

Even though you say you buy well The Boy all you are doing is delaying the deepening of the hole as those values creep down in Christchurch. They don’t even beat inflation. You should put what little money you have in the bank as it would serve you better there. I can see why you are a RE agent. You could not do anything else.

Even though you say you buy well The Boy all you are doing is delaying the deepening of the hole as those values creep down in Christchurch. They don’t even beat inflation. You should put what little money you have in the bank as it would serve you better there. I can see why you are a RE agent. You could not do anything else.

Whatever you say Gordon, you are such an expert on property investment I accept that!

Values in Christchurch are not dropping at all, but yes there are still,some very good buys before the market in chCh takes off again.

Anyway, in our hotel in Banff, (The Rockies) and it is snowing quite heavily expecting about a foot before we leave for New York tomorrow!

Hope you are well Gordon, love your banter

TM 2. You may have done well in proprty. What puzzles me is that you appear blind to the ppty carnage that is about to implode upon us.

I'd suggest that if you are as astute as you maintain, you would not be displaying the blindness to maintaining your views/position with such vigor.

The ppty market in both Aus and NZ is on the brink of a major correction. ChCh will not escape it.

Christchurch only has so far to drop. Already number 17 in values New Zealand wise which is pathetic considering it is the largest town in the South Island. One rental in Auckland equals several in Christchurch. That is why he is the Boy. One day he might be able to afford a European holiday in the sun.

The reason our housing is affordable is we have a functioning housing market. We have supply which actually meets demand. This is in stark contrast to other cities where houses are not affordable, and I know where I would prefer to live.

A lot of New Zealanders disagree with you mfd. They choose to live in warmer areas of New Zealand where there are more job and business opportunities and of course superior water recreation facilities.. And they are prepared to have larger rents and loans to service as they realise you only live once so you might as well live where you have the best standard of living overall. Hence the huge disparity between Auckland’s and Christchurch’s population. It will never change.

Each to their own, of course. I've been quite happy going against the crowd, if others want to add several years to their working life to live somewhere warmer but rainier I won't stop them. My hobbies of tramping, skiing, mountain biking and trail running are very well served by Chch's dry climate and nearby mountain range.

Exceeds demand.

Gordon, you say one rental in Auckland equals several in Christchurch.

3 Rentals in Christchurch would return us approx $1300 per week, would one in Auckland return that???

Our portfolio could drop by 50% and we would still be ok as we would still haveequity and the returns would still average approx 9 to 10%!

Doesn’t matter what you ever say Gordon, property has and always will provide us with a substantial rental income and huge capital gain should,we ever decide to sell!!!

The Boy you have cost your family a fortune. Imagine if you had the guts and money to buy property in the Lakes or Auckland. We all know you love capital gain. It must give you nightmares thinking about what you missed out on in hitting the wrong market.

The Boy you have cost your family a fortune. Imagine if you had the guts and money to buy property in the Lakes or Auckland. We all know you love capital gain. It must give you nightmares thinking about what you missed out on in hitting the wrong market.

I tend not to agree with TM2 on most things but your attacks on him are just silly. Particularly centering it around Christchurch constantly. Lots of people prefer the superior access to skiing/hiking/climbing, much less rain, longer summer nights, less muggy, house prices that are actually reasonable for many people, a rugby team that doesn't suck, less traffic etc. Other people prefer the busyness, job opportunities and beaches of Auckland to each their own really. Your feud has descended into childish bitterness.

Your generation didn't work harder than any others. You benefited from a post war boom then made the next generations pay for your retirement and property maintenance.

Yes its frightening. Went through Matamata on the weekend.lovely town , looking very prosperous, little change from 600k for a decent family home. Can hardly expect rural town wages for young couples stretch to that. How is it in anyway affordable? Ten years ago an elderly friend retired( downtraded) there and bought a solid respectable home under 150k. How is 350% price increase justified on rural town wages?

Panic stations.

Nzdan, yes I am waiting for an answer from Bw

It is going to be very interesting to see if we get an answer as I think Bw is making up porkies!!

There are a few on here that live in dreamland and for some reason come up with these wee

Stories that are not true

BIG Jump in listing....Defenitely as any vendor who want to sell will and should try to sell before the foreign buyer ban is in place.

So who and why be surprised with the jump.

Wait and Watch.

They’re living in a dream land if they think they can market, sell, and settle in three weeks though.

Number of days taken to sell is pure bunkum.Properties get flipped between different agents, withdrawn & re-listed etc. Its the number of days it was held by the last listing agent who sold ( or w.e.f commencement of most recent relisting till date it was sold) that is captured in the data.Another BS happily twisted by real estate industry

dp

More listing Should be supported by more sold signs or..........

Next few months will decide the direction the housing market takes.

All I know is when shitboxes are selling for 900k in the crappier parts of Pakuranga something is seriously out of whack

Why are all the posts now dominated by some arrogant guy called Nic who is never wrong? I get sick of his constant jaw boning. NZ has a population smaller then most world cities, we can't build houses quick enough to keep up with current demand, and more and more people will come here, the government can't restrict immigration (as we have just witnessed, this govt was appointed on that basis and nothing much has changed) and as a result the North Shore of Auckland looks like a suburb of China with complete blocks of shops with no English on them at all. While it would be nice to stop the population displacement I think the reality is the government has realised that it can't, so the population has only upside. Housing as a long term investment seems pretty sound based on this but no one really knows, not even Nic Johnson despite what he tells you.

We need Nic to counter the ppty spruikers - who are already supported full time by msm.

Heavily into property perhaps?

Housing is only a good long term investment ... if people have jobs.

Which is where its about to break down.

Some good points. I recall Bernard Hickey making predictions of 25% drops on this website 10 years ago and boy was he wrong ( and I gave his opinion too much respect and suffered accordingly). Even though it's seemingly irrational, property prices seem to continuously surprise on the up side. Having said that I pick some mild-moderate declines.

Rubbish, housing is a great investment from the first day you buy it!

Especially if you have bought it under “true”market value and it has upside.

Forget about talking about the housing market as being solely Auckland, as Auckland is only a small proportion of the total no. of houses in NZ!

If you don’t like the Auckland market then buy elsewhere!

TM2

Your comment clearly shows you are a savvy, skilled and experienced property investor and in the minority of participants in the property market. You may even be a property market professional.

Most other property market participants are non professionals in the property market (i.e they do not make the bulk of their income from this). Most owner-occupiers and first home buyers and most novice / part time property investors are price takers and buy at market price - they have had very few historical property transactions. These are people who may not have studied the property market with the level of intensity that you have. These people know very little (if at all) about buying below "true market value". Most of the comments above are being directed at this audience in Auckland rather than savvy property investors like you.

Bw, we are still waiting for you to tell us where on the outskirts of Christchurch this 3 year old home on one acre was purchased for $600k????

I am calling you out on this BW, because I know that you are telling porkies aren’t you??

Wish some people on interest.co would stop telling lies as it is not a fair go for anyone!!!!

Want to see what NZ's over priced property markets will look like soon? Here's a preview - 20-25% offers below asking. https://www.cnbc.com/2018/09/30/nyc-real-estate-becomes-a-buyers-market…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.