The slump in Auckland house sales that's occurred over the last couple of years has affected all classes of property buyers, according to a mortgage lending report by property analytics company Valocity.

The report analyses the number of mortgages taken out in the 12 month periods to the end of March from 2014 to March 2018, and breaks them into borrower types - first home buyers, investors, people moving house, those staying put but refinancing and those buying a second home.

As well as analysing those trends on a national basis, it gives the number of borrowers in each category taking out mortgages in Auckland, Hamilton, Tauranga, Wellington, Canterbury and Dunedin.

It shows that although there's been a decline in the number of mortgages being taken out in all areas, the biggest decline by far has occurred in Auckland.

According to Real Estate Institute of New Zealand figures, Auckland property sales peaked in their current cycle in the 12 months to March 2016, when 30,631 homes were sold.

That number has steadily declined and in the 12 months to March this year had slumped to 21,628, a decline of 29.4%.

However in the rest of the country excluding Auckland, the number of homes sold declined by just 12.7% over the same period.

So the slump in sales is mainly an Auckland problem.

The Valocity report shows that the resulting drop in the number of new mortgages being being taken out in Auckland affected all types of buyers, led by investors (-43%), followed by people buying a second home -39%, people moving house -35%, refinancing an existing property -33% and first home buyers -30%.

The figures also show that while mortgages being taken out by investors peaked (in the current cycle) in the 12 months to March 2016 and then started to decline, mortgage lending to first home buyers and existing home owners moving to another home had been in steady decline since 2014.

That suggests affordability issues in Auckland have probably been weighing on the minds of first home buyers and people considering moving up the property ladder for some time, while investors may have been a bit more gung ho on price, at least up until late 2016.

Although the Valocity report does not provide data on the amount of money being borrowed, when its mortgage numbers are married up with Reserve Bank figures showing the amount of mortgage money being loaned to different classes of borrowers, that suggests that the average amount borrowed by first home buyers (throughout the country) increased from $190,100 in the 12 months to March 2016 to $273,687 in the 12 months to March 2018, while the amount being borrowed by investors headed in the opposite direction, declining from $1,122,550 to $712,315 over the same period.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

179 Comments

.

An explanation of banking that I hope you all enjoy. This little clip is now 7 years old. The debt issue was already a problem back then but, low interest rates, specu-debtors, massive DTI ratios and interest only borrowing, not forgetting, turn a blind eye regulators and governments, have allowed it to continue to proportions that rival Northern Rock in 2007. 8 times interest only mortgage anyone?

I saw a mortgage broker the other day and he suggested I go interest only to leverage up that extra bit. I fear a lot of FHB's took this option and will be paying a heavy price with the incoming price drop due to sales slump.

What does it matter for the owner-occupier home owner? It's not like if they made a decision to not buy and their rents would have gone lower, infact the contrary. They have the security of owning their own home and their repayments is not relevant to house price movements. If they can't afford to meet repayments and have to top up loans regularly, then they should have never been given a loan in the first place.

It's called duration risk. If said FHB got an interest only loan for 1 -2 years, then you have to renegotiate with bank for new loan at the end of period. If prices drop then you have to stump up the difference to keep the LVR ratio or sell at a loss.

There is no reason for the genuine FHB who is buying own home to have interest only loan. Paying down principal steadily and quicker if can always made sense and still does.

Totally agree, unless its at 10x you income and you simply cannot do so. Oh yeah... that's the close to the average...

The idea was sold to me as a way to buy the house that i really wanted.

https://www.rbnz.govt.nz/statistics/c32

looks like the figure for April 2018 is

Total new debt = 5,375 (million)

new lending interest only inc FHB = 1,050

So a billion in interest only loans about to go negative and thats just from April....

Why did you see a mortgage broker Moneyphobe?

I would like to own my own home one day and needed to get info on the current lending environment.

Moneyphobe, the major concern for FHB with interest loans only is not the drop in house values as principal plus interest repayments in the first years of the loan will not significantly reduce the loan value. As long as they remain in the property market (e.g. there is a marriage split and the need to split and sell without re-buying) they should be able to weather the storm even if there is a slight drop in values.

The biggest risk for interest only highly leveraged loans is if either interest rates increase or the bank requires repayment of principal as well as interest. The likelihood of BOTH of these happening in the near future is very high.

In such a situation a FHB highly leveraged on interest only loans would be facing a double whammy increased cost and are therefore highly vulnerable in being unable to service the loan.

Agree with Pragmatist.

This story is now history - rather than news. We've all noted the decline in house sales volumes - but with little impact on (Auckland) house prices.

Now is a period of consolidation - which will likely continue for the foreseeable future.

TTP

Forgetting the leafy suburbs – I would anticipate a gentle softening in prices.

Various key drivers of price appreciation over the last few years have softened – not disappeared, but I would suggest have at least been tempered.

Prices are at somewhat lofty levels – perhaps more so at the lower end and those more basic apartments.

Again, I don’t think a gentle softening in prices would be out of the question.

I agree. The central leafy surburbs (grammar zone) are not going down and I find still appreciating. It's frustrating as I have been missing out on a number of properties. If I take capital gains out of the equation, then I will need to go away from central and base investments on yields. There is no shortage of tenants but with the prices even with 10-20% declines don't work for yields in those surburbs.

So many people here continually bag property investments. Fellas, where else would you invest?? Don't tell me bullshit share market and commodities, very high risk. In times of uncertainty, brick and mortar still work, interest rates not going anywhere but most likely down.

Chessmaster, now that we're entering a period of low returns, its seems gut wrenching for some! Only the one trick ponies still bang on about property as the be all and end all. There really is investment life outside property in a low inflation environment. Property has had a good run and is now in for a (long term) period of disappointment. If (longer term) term deposits of 4.20% are currently not your thing, then maybe it's a lust for high digit yields that blinds you to ongoing opportunities.

It's interesting how many claim to be sitting on much equity on investment houses yet, successfully realizing this unbanked equity is very much at the discretion of the markets and lastly the IRD - right? Now that speculators have had a good go, property for investment purposes is no longer a fail safe formula for win-win!

There is a killing to be made in US treasury bonds, go get em

Houseworks, such a forecast deserves at least one baseless fact. Quick, make something up. You're good at it!

US treasury bonds may be the next thing. They rise in value when interest rates go up, so you can earn capital gain and interest income at the same time truly

No, bonds decrease in value when interest rates rise. Your existing bonds become less attractive as comparable new bonds are issued with higher interest rates. If you have a fund or portfolio of bonds, this is counteracted to some extent by your average interest raising slowly as you renew your expiring bonds. Conversely, if interest rates fall, your existing bonds rise in value.

I assumed Houseworks was being sarcastic....hard to tell.

You could be right, there's enough economic misunderstandings on this thread that I'm on edge.

Yes you're right mfd there is misunderstandings and I would add mis-truths put about esp about property from the anti-property brigade. Nzers love property and also love to hate property and for that reason it is the most talked about topic here on interest.co.nz. The funny thing is that some of the best property buys can be done when property is not the darling flavour of the month, just saying

Whose offering 4.2% mate? Is it a finance company? Can't believe any banks are doing that as my recent mortgage rates offered been lower than that.

Chessmaster, https://www.rabodirect.co.nz/ All bank rates are published on this website under the saving button near the top. I currently am six months into a five year TD @ 4.27% paid monthly. It's a good place to be.

Chessmaster would you really be happy with 4.2% minus tax = 2.9%? Sounds absolutely miserable to me

Yvil, rest assured, being that it's my primary income not all of it is taxed at 33%! Most of the interest is reinvested. Right now, it's a good place to be!

While minimising your tax liability and still expecting to draw super and cost tax payers in health services is personally smart, we as a country need to send you a signal and introduce land tax. It's evidently the only way to make sure you pay your fair share for the next 35 years.

Ex Expat, I think you need to get a life and cast your jealousy aside. Other people besides you have also done well by hard work/saving. Enjoy your lot and be grateful ;-)

"Right now, it's a good place to be!" R-P

It's your Happy Place that you have been wallowing in since around 2012 earning 3.5 percent a year :-o You have something in common with a nz company that did use "happy place" in its advertising and that company's prospects also aren't looking anywhere near as bright as they were six years ago.

Hmm, sounds greedy to me.

Locked away for 5 years. Haha that's ridiculous low return for that length of time.

Chessmaster, your worthless opinion is noted however, I call it an insightful strategy in a world filled with elevated valuations and greedy expectations. I can see this world of greed turning to fear very quickly.

Greed and fear are not dissimilar states of mind.

I don’t get your comment “If I take capital gains out of the equation, then I will need to go away from central and base investments on yields. There is no shortage of tenants but with the prices even with 10-20% declines don't work for yields in those suburbs”. I agree, but those stupid low yields would indicate to me the central city areas are the most overvalued and the most at risk, not the least.

And no, no one is just bagging property investment full stop. But right now, for the foreseeable future, it’s a dog. We are right at the apex of the biggest credit and real estate bubble in our history and the signs aren’t looking that great. Prices will fall. The yields are terrible.

"those stupid low yields would indicate to me the central city areas are the most overvalued and the most at risk"

Bobster, the lower the yield the more sought after the property, not the other way around. (the opposite is true too)

The amenity value of the property is evidenced by its rental. A renter pays only for the benefit confered by occupation, not ownership. Rent reflects what someone is prepared to pay for the benefit of occupation of a property. The higher price of central Auckland property is well in excess of what could be explained by reference to its amenity value (ie the yield is far lower than elsewhere) and that excess of price represents the investment value placed on the property. So the speculative bubble present in Auckland property is just as present in the central suburbs as the outer ones.

Diversification is the best way to even out your returns, potentially increase returns if you re-balance appropriately, and reduce your chance of being wiped out. Depending on your age, plans etc, high risk isn't necessarily a bad thing. You're being extremely short-sighted to assume that shares are risky and property is not, especially if you are using leverage in your property portfolio.

Personally, I have roughly equal investments in property and shares, and a smaller position in cash & term deposits, and even smaller positions in peer to peer lending and crowdfunded equity type investments. Most people in NZ are already way overweight in property purely from their main home.

..nothing wrong with the sharemarket. Try exiting (or entering) property in 5 minutes from the office pc. No real estate agents, no open homes, no marketing fee...simple and quick.

Would love to hear your comment on share market investment after you make your first million in it. Buy lotto every week as well. Better chances

Hmmmmm Hopefully your Chess play is more strategic than you investment strategy

You say ."interest rates not going anywhere but most likely down."

This is a big assumption to make and assumes the the RBNZ actually has control of interest rates in NZ.

I would be looking overseas as a better indicator for the future of interest rates here as that is where our credit is sourced. I believe the risk is ever increasing for interest rate rises sooner and higher than you might expect.

I would be feeling uneasy about the recent statements made by the head of the reserve bank it feels as if he is posturing so he can stand back later and say i warned you.

Not to mention it looks as if the Legendary NZ housing bubble has started to deflate. That in itself would be ringing massive church sized alarm bells for me. To big to fall comes to mind.

Turning to TTP or Zac for investment advice seems crazy to me at this point!!

TTP

Please make sure that you put your own oxygen mask on before attending to the panic of others in the 8% that are sharing the 40% of the $250,000,000,000 mortgage debt. We are now entering a period of rapid decline in altitude.

Best Nic

.

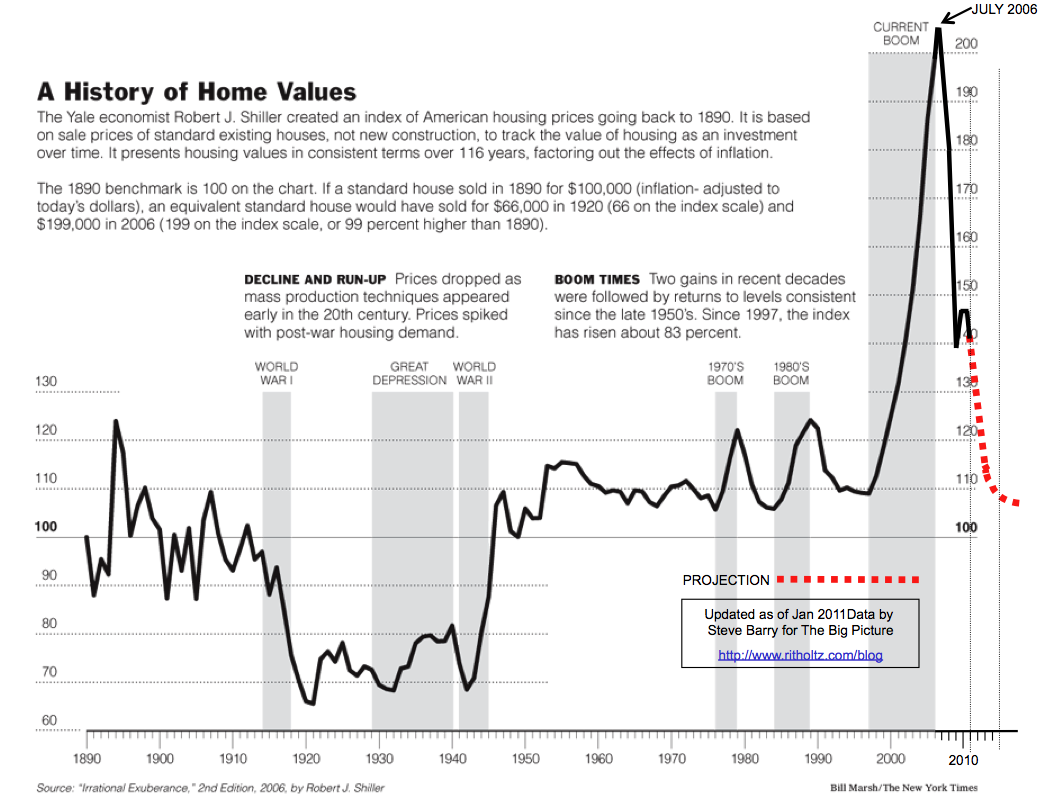

Or here's the analysis of real returns in the US:

http://ritholtz.com/wp-content/uploads/2011/04/2011-Case-SHiller-update…

{kind=link}

I like that chart... make me feel good about going from owner to renter in the US August of 2006...

My personal perspective is that his chart is likely using a lagging indicator, as my data suggests that the highest values were achieved in early 2006. If I had top ticked the frothy peak of the bubble in early 2006, I could have gotten 5-10% higher sale price than what I ended up selling for. I felt very lucky at the time to get the robust price that I got when I sold, and I was so very thankful that we had several offers to choose from at the time.

Yenkiwi.. 'make me feel good?' We've had this discussion before I think? US market or somewhere else?

TTP

" ....We've all noted the decline in house sales volumes - but with little impact on (Auckland) house prices."

Think economics 101 supply and demand; it will be after a sustained fall in volumes that prices will fall.

If we have noted the fall in house sales volumes (that is true), then my money would be on downward pressure on prices, and sustained price levels would be at best hopeful thinking.

Hi Printer8

I've been around a good while........

Long enough to know that textbook economics often doesn't explain real world markets.

TTP

Seems to explain it in every other country and industry, just not NZ housing market, how strange.

Less sales and no impact on Prices interesting, strange phenomenon., normally when sales decline then prices drop to meet market

So what happens to the house sales not sold due to unrealistic prices. These numbers don't get counted and are conveniently swept under the carpet. Sooner or later someone's going to budge and the house of cards may tumble. What will cause this, increase in interest rates, even tighter lending, no foreign buyers, less immigration, no ring fencing losses, GFC....................

Hi Greg,

You write: "The slump in Auckland house sales that's occurred over the last couple of years has affected all classes of property buyers.."

I think you will find that you have offended Mr tothepoint with the word "slump".

Better words to use are "negative growth" or "delayed uplift" among others.

RM

I think “downward oscillation” is the phrase you are looking for

How about negative acceleration?

Nicely put

The term used on another blog is "negative sideways movement" LOL

.

Hi RichMuhlach et al,

I'm not offended by Greg's choice of words/expressions at all - and never have been.

Greg is a capable journalist/wordsmith and perfectly entitled to make his own choices.

Afterall, freedom of the press is an important tenet of democracy.

TTP

As I have always said ToThePoint has always been POINTLESS

Auckland rental listings up 30 percent on Trade me,compared to 1 year ago. Any correlation with falling sales.

The clear and present danger of the reluctant landlord…..??

Overgeared top end houses are now the biggest issue ahead and where the greatest level of financial stress will occur. A top down correction is inevitable as is being witnessed in Sydney already. It was all a confidence trick you see, once the banks had run out of first time buyers, they had to con people who had already had paid off their mortgages once into taking on a new even bigger loan to keep the Ponzi going. A million dollar mortgage in your late 50's when you started in the 1970's with a $15,000 loan and had it licked once. Ooops.. And now they all want to get the cash back, but they can't sell the family home, because they've priced everyone else out of the market. Now that we have run out of specu-debtors to buy each others houses from one another the whole system collapses, unless of course Andrew King and Tony Alexander can magically create some more fools. My guess is that John Key (ANZ being the main sponsor of the NZPIF) had a fair idea that we were running out of fools in 2016. So jacked the PM job in and sold his house.. those that ride the waves in the sunshine (then go off for a beer) tend not to drown like those that stay out surfing in the storm...

Good luck everyone.

To under estimate a top economist that's been around for decades with a remarkable track record as Tony Alexander has is very foolish. Tony has the best understanding of modern economy's in the business. He calls it as it really is whether it's good or bad news. I have and will continue to value his opinion not agreeing with him does not make him wrong, time will always be the truth. Smart people would do way better listening and understanding what he has to say rather than the angry rant above.

Tony Alexander. Lets look at the details shall we...

An economist, yes, who works for one of the major lenders responsible for this mess, yes, who also has his own rental portfolio, yes, speaks at NZPIF seminars on a regular basis, yes and regularly has a feature in the property press, yes. Could possibly have a vested interest in the Ponzi scheme? There are two answers to this question.. Yes or no. You obviously have a view but would you say his economic opinion could be at all biased in any particular direction given what we know about his background?

I'm sorry but TA's only role in the professional economist circle is to make everyone else look good. Something he takes very seriously and is naturally predisposed to doing, I must add.

The guy is about as lowly regarded among his peers as is almost humanly possible.

Shoreman - have you heard of or follow the views of Robert Shiller? (he's a reasonably decent economist and doesn't work for a bank....).

When people talk about politicians and vested interests in Property, I can't help but point out John Key.

Campaigns on tackling the housing affordability issue back in 2007. Spends 9 years doing nothing about it. Then becomes Chairman of the ANZ who I'd imagine are profiting quite handsomely from house price inflation.

He's set himself up quite nicely.

After selling his house to a foreign buyer..

Actions always speak louder than words. When John Key sold a large proportion of his Parnell home and land in September 2017 (and kept only 650 sq m of land to build a home), that told me a lot about his thinking about Auckland property prices. Remember he has his background in FX trading, so once a trader, always a trader ...

Correct me if I'm wrong, didn't John Key oversee the mortgage derivatives for Merrill Lynch? Hopefully he can package up ANZ's bad debt and leave someone else holding that bag.

We havent run out of fools yet. Why do you think Labour has refused to implement the foreign buyers ban or restricted immigration visas? Plenty of them left, you can wave to them as they get off the planes at the airport. Apparently April was a record month for new arrivals.

.

Can't sell because there's too much debt, can't rent because there is too much debt and tenant wages can't afford to pay the interest. There will be a slow realisation that a reduction in price is the only option, but the thing to remember here is that a lot of these people are inherently stupid (that's how they got sucked into buying investments with negative yields in the first place), so the penny is likely to take a little while to drop. Sheep are not the brightest animal.

So, what housing shortage?

As I have said before, the shortage is exaggerated. Much of Auckland's population growth in students/low wage workers are slumming it in apartments and homestays

In housing market - flattening of the market is the first step and will follow by drop.

How much will it dropped or how sharp the drop will be, can be debated but one thing is for sure that from here on market will not go upward for few years so people in property market for fast money will be out, as it is now, anyone who has bought in last 2 or 3 years and want to sell are struggling and many are ready to take a hit depending upon their capacity (If theyhave been buying and selling since last 5 years and number of times than it does not matter as have made money few times and even if they lose now still in profit)

FHB should buy for long term but not in a hurry as the situation has changed and it is not that they will miss the bus now for they have already missed the bus and have to wait for the market to settlel before entering now.

Never a right time to buy in falling market (Even if it does not fall is not going up soon so why rush).

Media and so called experts will come up with theory - One day boom another day slump so not to be influnced by it and to use your own judgement - Buy only when you feel that you are getting a good deal as have seen property going as low as 50% less RV though the norm now is 15% to 30% (Though RV is not the correct indicator and has been raised for rates - Mayor had promised not to increase the rate so how does one increase thge revenue - raise the RV)

50% below, may be the house had some problem that you must have seen or a plaster house but yes many houses are going 10% to 20% below RV (most) at the moment and if it is a do up may be 30% and few are still selling near around RV but as you yourself have said that RV is not a true indication of the value.

.

Thanks for pointing that out, so much ignorance about how rates are set.

Hi Taimaiakka0

You write: "......property going as low as 50% less RV though the norm now is 15% to 30%"

That's absolute rubbish. Complete balderdash.

TTP

50% less than CV? LOL!!

So many properties are going below RV and many are between 15% to 30% (That 50% which I had seen must have been sold so not able to send you the link) but another property in Pakuranga heights 4 Riverhill Avenue had a asking of 869000 or 879000 and RV of 1050000. Do not know at what price it was sold but you can find out the price that was sold, if interested or may be not sold. Even if it went at the asking price is more than 15%.

Another stand alone property in Hutchinson road with land area of more than 800mts went for early to mid 800s and RV was mid to to high 900s.

So the story continues..........

Hi taimaiakka0,

Selecting a handful of extreme examples to try to argue your point is disingenuous - to say the least.

You ought to know better.

TTP

If one really sits down to find can easily find much more.

Like it or not it is the norm. Most property are selling much below RV but yes some preiumum properties are selling near around RV and if this is plateuing of the market, what will hppen when it really falls.

Hi taimaiakka0,

It is NOT the norm at all.

The statistics from QV, REINZ show nothing of the sort - as you well know.

Also, see Nzdan's analysis below.

Taimaiakka0 - you are NOT reputable.

TTP

I too have seen few houses for my friend and houses are going 10% to 20% below RV in Auckland but yes 50% is for effect like National 11 billion hole in last election :)

I also have observed that houses bought in 2015 or afterwards if want to sell now are not able to sell without a loss with some exception who may be are able to breakeven.

Saw Nazdan's comment below and is correct that now the trend has changed and as per his comment property are selling uptill 37% below RV and this is just the start.

When value was going up it was with just one house in a sreet going much above RV and that was used as a bachmark for that area by real estate agent and speculators. Similarly now it is other way round lol.

Hi taimaiakk0,

Nzdan's analysis (below) shows that, in fact, only 6 out of 45 properties sold for more than 10% under CV.

The majority of them sold ABOVE their CV.

Thus, your comments have been highly MISLEADING and DECEPTIVE.

TTP

.

TTP, don't waste your time (and your sanity)

Yvil , I thought you were smarter than that, you've lost all credibility

The 1 that sold at 37% below RV had the RV increased from $1.3 mill to $2.25 mill. It sold above the 2014 RV of $1.3 Mill.

Looks like the 2017 RV includes both 49 and 49A as Rastus mentioned.

.

This is a classic example of the ZS theory of "what is my house worth right now?" which is the price you paid plus whatever percentage the value of houses has gone up since you bought it (+/-5%)

Something seems wrong with the RV. The mirror image of 49 Tawera is 51 Tawera. It actually has considerably more land at 1639 compared to 1282 yet its land value is 1550k per crosslease section compared to 1975k.

The real indicator of what is happening here is the sales history of 49A Tawera. In 2007 it sold for 720K so 1400k is a 94% increase in value which is slightly more than the average for Auckland during that time period.

Compare 2/10 Empire Road, similar value crosslease in DGZ with RV of 1800k, sold the same week for 1650k yet sold in 2007 for 839k which is an increase of 96%.

Oh so similar appreciation!

What looks like a perfect example of a crashing market at 37% below RV turns out to be a ringing endorsement of the ZS Rule of Auckland house price current value. Nice when that happens..

You're better off talking about the 91 properties that didn't sell. 29 of these properties were bought by the vendor within the last 4 years, the properties are now back on the market again and failed to sell. I wonder what their reasons for selling are?

60a Centorian Drive speaks to your narrative taimaiakka0.

CV $1,075,000. Paid $995,000 in September 2016. Listed for $898,000 on Barfoot Website. Failed to sell at Auction the week just been.

60a Centorian Drive speaks to your narrative taimaiakka0.

CV $1,075,000. Paid $995,000 in September 2016. Listed for $898,000 on Barfoot Website. Failed to sell at Auction the week just been.

Phew. That's quite the bath taken if they end up selling below the asking price!

Not if you are laundering illicit funds. Thats quite a small loss.

Yeah

I understand falling market will disapoint many and will be hard to digest that the party is over as a result the reactions. Though people buying for long term normally do not go wrong in property but Yes short time speculators and fast money is gone for some time to come.

Zach was having the week off so i ran some numbers on the Auction Sales Results for Auckland.

45 Sold, i had difficulty finding QV information on 4 of them so working on the 41 remaining properties:

19 were sold under CV, of these:

- 13 were 1 - 9% under CV

- 5 were 10% - 20% under CV,

- 1 was 37% under CV

22 were over CV ranging from 3% over to 28% over.

2 sold at exactly CV.

The property at 37% under CV was:

49A Tawera Road, Greenlane.

2017 CV $2,225,000,

Sell Price $1,400,000.

2014 CV $1,310,000.

Have we passed the tipping point?

Immigrants are leaving because they don't like the new Government. Aucklanders leaving town for other regions because they cant afford to live on 100k income. People sharing houses in greater density than before. Fletcher's loosing a lot of $, smaller building companies struggling and some going to the wall - see Tauranga. Borrowing tightening up, a bank dashboard now available so you can see how leveraged the home for your deposits is, big gap between sellers and buyers with near record low sales volume. Aussies banks review exposing very poor lending, and looking to spread to NZ. Aussie banks have pulled interest only - will that happen here as well. Reporting of Chinese walking on apartment deposits because they cant settle. Loss ring ring fencing coming, brightline extension in place, overseas ban in progress, Italy looking like it might beat the UK out of the EU by being ejected which would expose and potentially start a the unraveling on the debt pyramid that is the EU. QE printing presses having a well earned break. Share PE ratios simply in la la land.

All in all amazed that RE in NZ continues to hold up as well as it does. Once the ban is in and is being enforced I think we will see just how naked the emperor is, especially in the $3m plus range (range that most kiwis can only dream).

Note that the number of immigrants has decreased from record highs, but the number of immigrants still remains at astronomically high levels compared to the historical situation.

The current high levels of immigrants - along with historically low interest rates - are still are a driving force in the property market especially Auckland. (Without the current levels of immigration - and low interest rates - we would certainly be seeing considerable price drops especially in Auckland)

Quality comments today. I agree with most!

Great article Greg.

Most pleasing aspect is that you have referred to both the number (not the value) of new mortgages and you have considered the different markets.

Previous articles on interest.co have referred to the national value of mortgages (from NZRB data) to suggest that FHB are the new force in the property market. The number of investors nationally taking new mortgages are certainly well down; over a 35% decline from 2016 on NZRB data. While the percentage value of mortgages nationally taken by FHB is up as reported by interest.co, the percentage increase of FHB is not as great due to house price inflation; and it is now good to learn - but not surprising - that in fact this is limited to those areas outside of Auckland.

So far its only a sales volume slump, wait for the price slump, its just around the corner!

That's a relevant point. Sales volume dropping off a cliff exacerbates the following:

-- The small army of people who rely on trading houses for a living

-- More importantly, the emotional well-being of the sheeple, which is crucial for consumer spending, which is ultimately more important that the price of houses. If the sheeple are spooked, they may hang off that trip to Fiji or the new car for a few months ("to see how things play out"). We know that without their own perceived self worth, their propensity to spend is hampered. For the 'avocado on toast' segment, they're irrelevant and best for them to continue as they have been doing.

Given that $6 in every $10 spent on groceries in 2017 were sold on promotions (effectively discounting), it would seen that something has to give in NZ. Manufacturers and retailers will be crimped massively. No other developed country can match that level of discounting. The questions is as to why. If Kiwis need to scrimp on food and other daily necessities, how can they splash millions on property? And what will they ultimately do for the FMCG economy that pays the wages of much of our society?

Not at all.

The whole idea of discounting is profit maximisation.

It tells a story, but not necessarily the one you think. It is not the story of consumers needing to purchase things on discount, just that demand reacts relatively elastically to price. A completely rational expectation.

The level of discounting is a reflection of the supernormal profits we allow in New Zealand due to our inherent belief that the way to get ahead is to sell things to each other at inflated prices.

It tells a story, but not necessarily the one you think. It is not the story of consumers needing to purchase things on discount, just that demand reacts relatively elastically to price. A completely rational expectation.

Right, but I think you're missing the point. If 60% of sales are on discounted products, that's a directional indicator that price is the key purchase variable across categories. Now given that NZ consumer and h'hold debt is off the richter, there is nothing wrong with forming a hypothesis that "NZers are focused on discounted FMCG products because of budget constraints."

The level of discounting is a reflection of the supernormal profits we allow in New Zealand due to our inherent belief that the way to get ahead is to sell things to each other at inflated prices.

Not sure I agree, I think that many manufacturers and producers have no choice. It's very difficult to sell on volume in many low purchase frequency categories.

that's a directional indicator that price is the key purchase variable across categories

As it is for anything.

The purchaser balances the price and utility bearing characteristics. It's not necessarily an indicator of anything based on that observational data only. The only thing it confirms is a rational response by consumers.

Correlation is not causation.

It's very difficult to sell on volume in many low purchase frequency categories.

Okay, that doesn't matter, though - You said $6 of every $10. That is on gross revenue, irrespective of product and volume.

The majority of the figure will be from FMCG discounting. That is a certainty.

OK. I'm not going to battle you. Given that comparative data for other developed countries shows price discounting for the same FMCG categories is closer to 20%, NZ is definitely unique.

Also, Katherine Rich mentioned to me that NZ FMCG manufacturers and producers are doing it tough. Your idea that they're sitting sweet doesn't gel with what I've been hearing. If they cannot drive incremental or even break even in their business units, discounting is necessary.

.

Agree.

I think Briscoes are moving to the Kathmandu retail model ie price it stupidly high and expect to sell little except to the needy and have few staff as no one will be shopping and then do a 60% sale to sell the volume. So example, until pretty recently (last year or 2) Briscoes "normal" price was always a bit less than Moore Wilsons and then in a sale an even better price. Now Briscoes normal price is substantially above Morre Wilsons with their discounted price only a few dollars less.

Example Sunbeam 2.4kw electric frying pan I just bought last month, $185 is Moore Wilsons, $249 In Briscoes reduced to $181 in the "sale" 2 or so years ago.

However Briscoes seems to be selling more and more cheaply made crap, ie I went through 3 toasters each lasting very little time (like 3 goes to 3 weeks before exploding) before getting a refund and going to kmart for a $26 dollar one, its still going 6+ months later and cost me 1/2 as much as the "sale" price.

Solid bedtime reading. I used it as an example to businesses in trouble to point out where they were off the mark. https://www.amazon.com/Rma-Annual-Statement-Studies-Benchmarks/dp/15707…

Don’t fall for the spin. Retailing is about revenue growth and margin control. Just because discounting is visible, it doesn’t mean the retailer is sacrificing margin e.g. Rebel Sport and Briscoes.

"Just because discounting is visible, it doesn’t mean the retailer is sacrificing margin"

Ahh, that's exactly what discounting means.

What you mean to say is that the retailer/supplier is seeking to maximise profit.

The proposition is that discounting is a sign of consumer weakness. My contention is that it’s (largely) a marketing ploy. Call it profit maximisation if you want, but unless we are in the strategy meetings with the supplier and retailer we’ll never truly know what’s going on. I’m willing to bet that the local supermarket has no need to discount that double pack of ginger nuts. It’s likely a strategy between the supplier and retailer but it doesn’t mean the retailer is having its lunch cut.

I suggest you read an elementary textbook on industrial organisation.

The motivation is purely profit maximisation.

You do not discount something if you believe that by doing so you will return overall less profit than by not doing it.

Stop arguing for the hell of it and see some common sense for once.

.

And we have a Fair Trading Act and a Commerce Commission to protect against that.

.

Easy, do what I do, dont switch the TV on any more....at least not for TV channels.

I haven't watched "TV" channels since 2010. I went to stay with a friend in Melbs recently and she *only* had TV channels (not even netflix) and the adverts drove me absolutely nuts!!!! I love my advert free life.

.

Do you reckon that chick who has fronted their ads for the last gazillion years has been handsomly rewarded by Briscoes or is a wage slave?

actually I tend to agree with expat and you. Recent article suggesting that discounting is a strategy to grow market % and if it doesnt grow your share its a bad idea. Personally I think there is more going on. Partially its discounting as stock isnt moving off shelves as much. Also I do suspect there is actually some nefarious action going on, ie a quiet attempt to recover profit margins by fooling the customer with "discounts" which are really not.

Pot, Kettle, Black on sale for a limited time, 30% off. Stock unlimited so you won't miss out.

What's interesting too in this equation is how much more information advantage buyers have than in the past. I.e. they know they can get the t-shirt from AS Colour and the patch from AliExpress for a whole lot less than $99, and they know they can get good quality and low-priced local items from the likes of Daiso, parallel-imported Ikea etc.

People are definitely going off being overcharged for rubbishy goods by local retailers.

If there is a crash and people seek to blame the new government, it will pay to remember that Bill English took credit for achieving a "flat to falling" housing market last year.

Pretty much sums up the self interest of the previous government. Hey its in our interest to try and resolve the housing issues. Oh hold on its in our interests to make the housing issue worse and see prices rise. Oh sentiment is shifting again, its now in our best interest to claim we now have a flat housing market.

@Averageman | Thu, 31/05/2018 - 10:10.

Never Fear! Replacing the buyers from the Mainland are those escaping DT in the land of Freedom !

Response to Averageman above, you said: All in all amazed that RE in NZ continues to hold up as well as it does.

Me too. And my relatives in the US are even more astounded!!!!!

Here's a great example/comparison:

Green Bay, WI - listed January 2017 (still unsold)

Price: USD 359,900 (NZD 515,173)

https://www.zillow.com/homedetails/2110-Sylvan-Ct-Green-Bay-WI-54313/88…

Palmerston North, NZ - listed January 2018 (sold Feb 2018)

Price: USD 393,311 (NZD 563,000)

https://homes.co.nz/app/address/palmerston-north/hokowhitu/487-college-…

Population Green Bay metro = 312,409

Population Palmy North metro = 85,300

Both homes built in the mid 1970s.

Green Bay property:

4 beds - 3 baths - 278m2 (house) - 31,160m2 (section)

Palmy North property:

3 beds - 3 baths - 163m2 (house) - 872m2 (section)

Okay, okay - so it snows a lot in Green Bay. But it's only a 3hr 14min drive to Chicago (if you want a dose of big city life) - whereas it takes twice that to get from Palmy to Auckland... and I can vouch for the fact that Chicago has a lot more quality entertainment on offer than Auckland.

Don't get me wrong, I'd likely never move back there, but things are indeed insane here in our little deep South Pacific island nation with respect to the RE market.

Columbus Ohio has a median price of USD236,000. The economic power base of Columbus would swamp the whole Manawatu.

Have a sister in Denver, CO. Now that's a lovely place to live.

She's 3 bed, 3.5 bath - detached house - 600m2 section - current Zillow estimate converts to NZD $491,395.

Any Aucklander that thinks prices there are good value needs their head read.

Have you been to Denver? I have. Close to the Rockies which is about the only thing going for it. NZ is paradise compared to Denver and San Fran and most of the US. In 20 years, as the over populated world continues to live over themselves, they’ll still be generating cash. China has so much cash they don’t know what to do with it. NZ will continue to be in hot demand.

Who wouldn’t want to live in a funky, green, liberal, friendly, open economy with beautiful surroundings. NZ property might take a small blip for a few years, but long term, is a sure bet. Literally everyone will want to live here in a few years.

I’m not sure that too many commenters on this site are funky, green, liberal or friendly. There is an amazing amount of negativity and Shadenfruede. It’s easier to be negative than try to better oneself and focus on monetising opportunities. There are a heap of opportunities on our doorstep.

Property Taxes about NZ$6000 a year. But yes a lot of house for the money. Also you could buy with 20% down and fixed rate mortgage for 30 years a 4.3%. Oh and the mortgage interest is tax deductible. WTF would Americans want to move to NZ. Even if they made Rosanne president.

Their property taxes there pay for schools and local law enforcement too, I think. And they're quite high in comparison to ours) everywhere.

Hi Kate,

Palmerston North is certainly an amazing place!

And the fact that NZ is small and far away from other countries is part and parcel of why it has become so sought-after, internationally, with commensurately high-priced real estate.

There are heaps of people abroad who would give an arm and a leg to live in NZ.

Am certainly glad I live in NZ. Wouldn't want to live in USA - or anywhere else.

TTP

.

Best laugh Ive had all day. Thanks

I agree, hilarious. Palmy is a shithole in the middle of nowhere in NZ's least inspiring region

Thought the same before we moved there, but really, really enjoyed our time in Palmy.

It's such an easy place to live - flat, wide roads - parking galore, never have to round the block to find a park. Might get stuck in line behind 8 cars maximum at a roundabout during the 10 minute duration peak time of day. Very few traffic lights and you can avoid most of them via an alternate route if you'd rather.

Live anywhere and nothing is much more than 10-15 minutes by car. All the major retailers are there, and good choice for specialty shops as well. Primary school kids can all walk (or bike) to school.

Some very pretty neighbourhoods with lots of deciduous canopy trees. All services are underground.

Hot summer days are lovely hot. Himatangi Beach is a 20 minute drive - huge expanse, very safe swimming, also has a surf club - cars can drive on it, you can take your six pack down there and dogs off lead are never frowned upon.

No seaviews but fantastic views over the river, city and plains with both Ruapehu and Taranaki as backdrops on many a morning if you're happy living on the hill.

Stress free.

https://www.stuff.co.nz/national/89850315/a-love-letter-to-palmerston-n…

Hi Kate,

Don't take any notice of the knockers here.......

By and large, they are just a bunch of jealous/envious losers - many of whom would love to have a home just like yours! (It wouldn't matter which city you mentioned, they'd knock it.)

As well, Palmy has a very good university (Massey) and other fine education facilities. Excellent health/hospital and sports/recreation facilities too. It is supported well by agriculture, the Ohakea Air Force base and Linton Army Camp.

Enjoy your life in Palmy!

TTP

I think Kate has moved to Wellington.

It might be pleasant enough but it's also really boring

The best kept secret about Palmerston North is the wind! Having lived there for two years (originally from Welly) I can vouch that PN weather is much crappier than Wellington. The only plus about PN is that you can drive from one end of the city to the other without having to change gear on manual car (Ferguson street)

The best kept secret in Palmerston North is how to get out.

For years the locals seem to have been trapping the degenerates of society by neglecting to tell them how to navigate out of the god forsaken place.

At least they get the village idiots to shift to Epsom.

TTP is the source of Palmerston North's wind. It blows hot and often brings with it the fragrance of "pies in the sky"

.

Just moved back to Welly - gotta disagree with you there. It's always 2degC colder here than Palmy. Not sure which is windier - we lived in a really sheltered part of Hokowhitu for a spell and on the hill below Te Rere Hau (two complete extremes).

Back on a Welly hillside now. Had the recent southerly cold snap (accompanied by very high/freezing humidity... hail storm included). And we're waiting for our first good Nor'westerly blow.

And before these, I came from Chicago. So I'm a bit wind hardened, I think.

Kate - NZ is a total rip off in most respects!

Ouch that is too depressing. Many friends back from the US and those who are looking at making NZ a more permanent home were discussing the prices. Mansion in the US vs hovel in NZ small town. By comparison we all know which one is better for health & quality of life. Trouble is though the incidence of guns in the country (whereas NZ is mostly sheep & respiratory diseases).

House sales in Japan are really odd. The buyers are almost all very young married couples, with a baby or a couple of toddlers in tow. No smug and arrogant silver-haired boomers strutting around with a grotesque sense of divine entitlement, snapping their fingers at the help and roaring on about the supposed worthlessness of Millennials. It was all so disconcerting. Young families buying homes for themselves -- What's wrong with these people?

OK, this is where you come in with the obligatory reply about how "Un Zul'n/Juppun us duff'runt un spusshull."

This is pretty hair-raising stuff - https://www.stuff.co.nz/business/104369683/commerce-commission-review-f…

"New Zealanders are being charged rates as high as 803 per cent a year to borrow money, the Commerce Commission has found."

"The Commerce Commission said they were in the niche mortgage market offering lending such as short-term backing for property investors and high-interest lending to people who were bankrupt."

Good Grief…..

This out of Australia:

"Another big player is predicting a tough time ahead for the Aussie real estate market.

It could be bad news for real estate investors if predictions from Westpac turn out to be true.

In a weekly update released by the bank earlier this week, some grim predictions were made about house prices over the next 24 months.

House prices, the update predicted, were expected to fall by as much as 10 per cent over the next two years “with weakness particularly centred on the Sydney and Melbourne markets”.

The update added that this predicted drop could also hit the broader economy.

“This will represent a considerable change in the “atmospherics” around housing wealth and may weigh further on prospects for consumer spending,” the statement read."

“As much as 10 per cent over 2 years”?! Thats peanuts, I really doubt they’ll get off that lightly.

Perhaps Westpac were deliberately treading lightly….for all the obvious reasons.

That's where I think Auckland will go too.

To be honest I’m quite surprised by this from Westpac – I actually think this is quite concerning.

For Sydney / Melbourne – read Auckland.

If this does indeed play out – it could get quite bumpy – and a little nasty.

Perhaps some of the reluctant landlords should indeed bite the bullet – take what profit is on the table and sell – there would appear to be some significant risk out there.

My God that sounds absolutely horrible thank God they have just had a 90% increase over the last 5 years LOL....

Meant nothing in the US crash....

.

Property is a bit of an odd thing – it can go up by 10-15% easily year after year with many smiles all round – but should it ultimately turn down 10-15% over a 1 or 2 year period – serious stuff.

Too many may have geared up towards the end – a 10-15% downturn sometimes becomes quite serious – and creates a self-fulfilling downward spiral.

As someone mentioned earlier – you can’t or don’t want to sell, but renting it out won’t cover outgoings – stuck, and now possibly just have to get rid of it to sleep at night.

Unfortunately, this may well be at the same time as quite a few others.

Oh dear!

Wow, so much talk, so many differing views, a lot of anger, not agreeing, arguing, scorn and laughing - hey, seen it all over many years, just a normal bridge from boom to bust, get over it, relax and enjoy the ride, opportunities arise...

Indeed – it can be an interesting and fun ride.

You just need to make sure you’re able to stay on board to enjoy it.

The market is evenly poised.

A significant economic event abroad will put our housing market into free-fall.

The news out of Australia is very concerning. Remember Australia got through the GFC largely intact, and this insulated NZ from the full impact of a global meltdown.

Ive said that a million times, but some think that NZ is insulted and isolated from the rest of the world

NZ so easily offended - by the insults!

Well put. Without a global / regional shock, nz property will probably dip a bit and stagnate next few years. With a shock it could readily enter into free fall.

NZ is totally at the mercy of global events. We partially rode out the GFC because of the Chinese's ravenous appetite for minerals in Aussie and milk from NZ. Look at the impact on Perth from that appetite waning.

What would an global event look like.Lets speculate things like... Brexit actually being complete, Euro collapsing under member issues (Italy), Deutsche Bank having a potential Lehman's like event, Country's abandoning the Petro dollar for other currency settlement, USA considering reducing combat power in Europe (how many bases are there again), USA actually being called on their debt problem (seen California lately), USA and China getting into a Trade/Cold war, China flexing its wallet and investing in military muscle, Russia flexing its military muscle.

All of this is speculation....right?

None of the scenarios you outline are any cause for alarm, and half of them are already happening.

NZ is paradise to most of the world. But what might harm NZ’s standing is insular, surly, negative people who would rather cut immigration than come up with a good plan to monetise the opportunities that we have in a sustainable and sensible way.

Having moved back for a while now after a fair amount of time offshore, it’s striking how negative and short sighted we are.

Rest assured the world is NOT going to end in 5 years time. In fact in 20 years, if we play our cards well, literally everyone will want to visit NZ, spend money, support our small businesses, and want to live here.

It’s good for everyone.

NZ is the size of the UK with the population of Birmingham.

The reason wages have stagnated and people are struggling is because we haven’t grown sustainably nor had a long term strategic plan. That’s not a political statement. It’s time to grow up.

Stat NZ is going to publish a better picture of overseas buyers of NZ property-

https://www.tvnz.co.nz/one-news/new-zealand/new-stats-give-fuller-pictu…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.