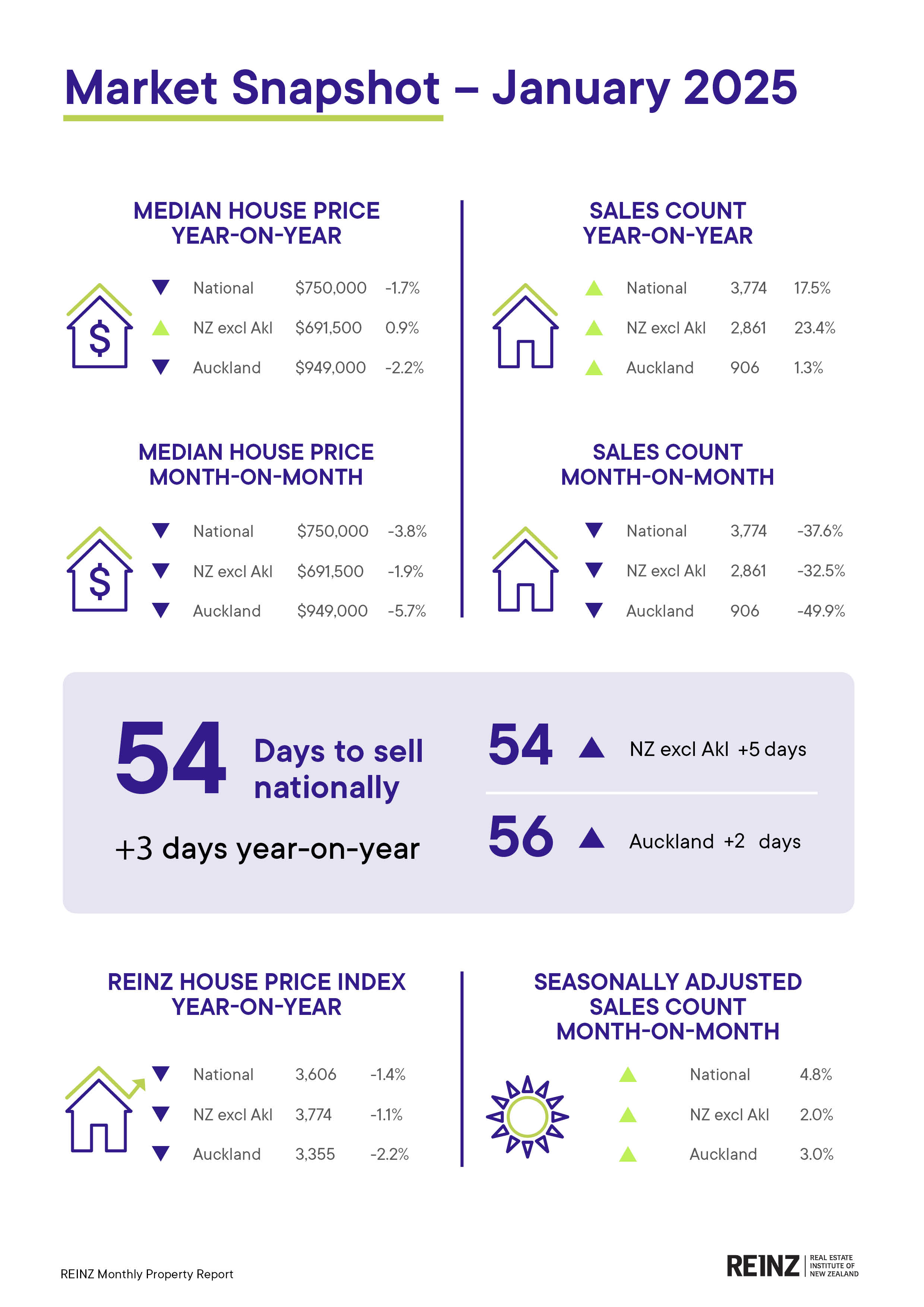

January brought mixed fortunes for the housing market with sales up strongly for the month but prices in decline.

According to the latest Real Estate Institute of New Zealand (REINZ) figures, 3774 residential properties were sold in January, up a solid 17.5% compared to January last year.

However, prices headed in the opposite direction with January's national median selling price coming in at $750,000. That was down $30,000 (-3.8%) compared to December last year, and -1.7% compared to January last year.

Auckland suffered a particularly savage fall in prices, with Auckland's January median of $949,000 declining by $51,000 compared to December (-5.7%) and -3,8% compared to January last year.

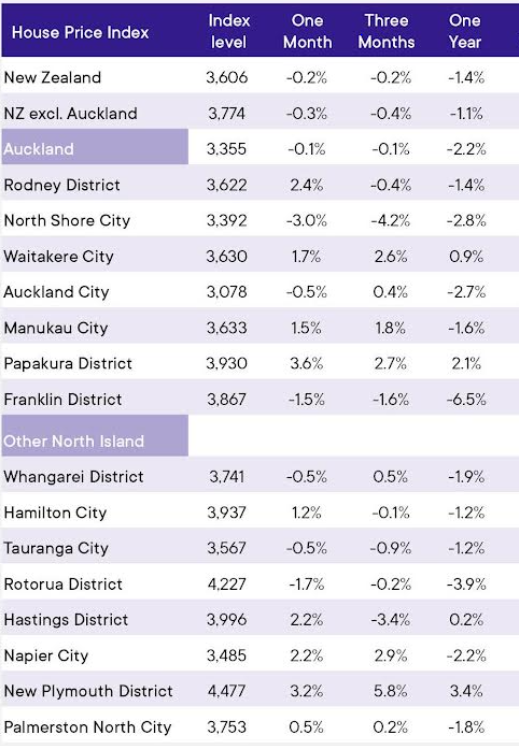

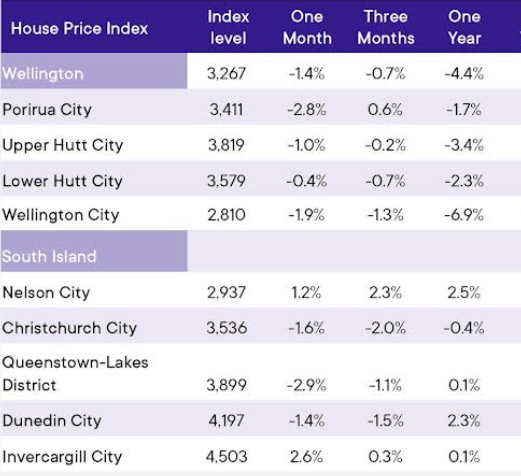

The REINZ's House Price Index was down -1.4% compared to January last year and -0.2% compared to December. See the table below for the regional figures.

The decline in prices was most likely helped by a strong increase in the number of properties for sale.

The REINZ recorded 8904 listings in January, which was a 10 year high for the month of January, and up 21.2% compared to January last year.

Properties were also taking longer to sell at an average of 54 days in January, compared to 51 days a year earlier.

"Buyers are still enjoying the choices on offer thanks to rising listing numbers and significant levels of property for sale," REINZ Chief Executive Jen Baird said.

"With vendors being realistic in their price expectations and meeting the market, there is a positive sentiment out there among agents," she said.

The comment stream on this story is now closed.

Median price - REINZ

Select chart tabs

Volumes sold - REINZ

Select chart tabs

REINZ House Price Index - January 2025

199 Comments

Fantastic news!

So Barfoot's was a lead indicator not an outlier.....

And drops in asking prices on Trademe were a leading indicator too...

Surging sales volumes when prices are relatively low suggests that the cycle trough is close - and that market stability/recovery is not so far away ….. 🍾 🥂

With abundant choice, relatively low prices and slashed mortgage interest rates, the upturn in buyer interest is hardly surprising.

Good to get in while the going’s good ….. 😁

TTP

I'll correct it for you;

In this strong Buyers Market, surging sales volumes when prices are still falling suggests the bottom is some ways off and by ratio, a growing number of sellers are chasing after increasingly discerning buyers....

Once again, you struggle to articulate the truth.

Properties were also taking longer to sell at an average of 54 days in January, compared to 51 days a year earlier.

Pity you can’t take advantage of the current market conditions, Retired-Poppy ……

But given the multitude of monikers/accounts that you use here, your membership subscriptions to the site must be costing you a fortune. 💵 Not much money left over for anything else. 😰

Finally, seasoned contributors here are well aware that, just as the Titanic had a problem with icebergs, 🧊 Retired-Poppy has a problem with forecasts. 🤯

TTP

Once again, you struggle to articulate the truth.

😂🤣

Let it go, Retired-Poppy. You don’t need to have the last word every time.

Quit your obsessing! 😵💫

TTP

Hey Tim The Price Fixer

Hows the fraud going?

https://comcom.govt.nz/news-and-media/media-releases/2017/property-brok…

Don’t be fooled by this clown, he couldn’t guide his way out of a paper bag let alone give an honest housing forecast.

Sincerely,

Interest Comment Section.

Oh dear ….. he just can’t let go. ”That’s All Folks” is Poppy’s latest moniker. 🙄

Sadly, Poppy's caught in the vice-like grip of compulsive obsession. 😬

TTP

Only a person with his head stuck up his own jacksy would attempt to explain away an army of critics as being just one person.

Good luck with that one 👍

Could you just come out and categorically deny that you are who people think you are?

As far as I'm aware you've never done that.

This whole back and forth is getting really tiresome.

TPP also created a business empire - starting from nothing, Thats some achievement. How many of us can say the same ?

If it was not TTP, it would've been somebody else. There are plenty of business empires in all sectors of the economy, that have been around for decades. Did they innovate? Or did they just by sheer timing happen to be the right company in the right point in time to capitalize on economic activity? And then grow under their own momentum?

Mainfreight is another example, they did very well but a lot of that came about from deregulation of road transport in 1983. If only I could get in my time machine, and go back to 3 years before I was born, and start a trucking company to compete.

Not knocking the highly successful, just putting into perspective that "yes well done pat on the back" and yes they worked very hard, but it wasn't their hard work alone that built that success.

Pop the bubble goes.

Looking at the Median Price graphs, they mostly look flat from Jan 2023 onwards. I am not sure where the "Pop!" is?

Sure the Covid madness has been wiped out, but they look pretty stable for the last two years unless I am missing something?

It was flat but I think we are making further headway down now.

January always comes up with lower median prices but this is the lowest median price since before the covid bubble.

New Auckland CVs and increased rates are about to come out and give a lot of people a rage induced headache.

Interesting times ahead.

I think you are seeing what you want to see

I think you are literally ignoring what you are seeing.

All I am saying is the data so far doesn't look like a "pop". Sure, it might keep dropping due to many reasons, but the last two years has looked remarkably stable

so we are 20% off peak and its stable? ROFL

I hope it does not become ... more stable for you.

Read my comment again and look at the graphs.

"Sure the Covid madness has been wiped out, but they look pretty stable for the last two years"

I do not trade off comments

I trade off data

20% off peak and its stable?

he said the last 2 years, there has been a 2% drop in the last 2 years?

But we agree it is still falling right?

Falling more slowly over the last 2 years but still falling.

No sign of the bottom that was apparently hit a year ago, and 6 months ago, and 3 month ago and 1 month ago ...

correct, prices are falling very slowly. most likely bouncing along the bottom.

😂🤣 - and the entertainment continues unabated.....

What's that saying? "what might appear as a small leak can sink a big ship"

Unfortunately many are heavily geared for uninterrupted capital gains.

haha ha

If you were my student, I'd have given you 10/10 for your optimism (and 2/10 for actually answering the exam question).

first term - tried hard

second term - still trying

third term - very trying

How exactly can it fall through the bottom?

Is the bottom also falling?

😂😂😂

The market has barely budged in the last two years, that sounds pretty stable to me. Probably about the longest 'flat' region in the whole timeline of the median price graph in the article (depending on how flat you think the post GFC market was

Agree although if we see another couple months of negative data and a new trend is forming, then from a technical analysis perspective (if you can apply this to a housing index!) I wouldn’t touch housing with a barge pole as the next floor could be a lot further down (thinking 2015 prices).

Id wait and watch for a few months if I were a FHB - there could be some good buying opportunities later this year if all the data keeps going in this direction (more stock and falling prices).

" from a technical analysis perspective (if you can apply this to a housing index!)"

Yup. TA works with houses - but the usual TA measures need some refinement. The trick is to match "like with like" rather than using broad measures. And everything takes a bit longer (black swans excepted).

Id wait and watch for a few months if I were a FHB - there could be some good buying opportunities later this year if all the data keeps going in this direction (more stock and falling prices).

For owner occupier buyers to be aware of:

Former prime minister Sir Bill English is optimistic that New Zealand’s house prices are going to trend downwards, in real terms at least.

“Our housing is too expensive,” English told delegates to the INFINZ (Institute of Finance Professionals New Zealand Inc) conference at Auckland’s Cordis Hotel on Monday.

“If we successfully deal with housing affordability, your house prices are not going to go up for the next 15 years, much.”

https://www.waikatotimes.co.nz/business/350451961/get-used-it-sir-bill-…

CAVEAT EMPTOR

Oh yeah, still looks like a terrible investment to me. If I were a FHB I'd consider buying if I had a decent deposit and some margin in my budget but I agree there's a reasonable chance that prices will fall or at least stay flat for a while yet.

Clearance looks like next summer 25/26 imho

by then interest rate outlook may be more certain,

People may have a better view of thier employment security

prices will have fallen enough to tempt FHBers maybe

I do not see a bounce in either the market or economy either

the low end of the market will be active, the mid and high will be very patchy as there

are a lot still expecting cv

TBH not deflating fast enough... really want it to crash like at least 50% from where it is today... just gotta wait for even bigger waves of productive people to leave the country... as National puts it "Everyone Must Go!" XD

...& the winner is...supply / demand

The winners are the young families who have a better chance of getting into a home.

Do they really though? People have completely oversimplified housing affordability as "the lower the prices the better". But if you achieve the low prices by doing the following:

1) Increasing interest rates

2) Requiring higher deposits (or you end up paying a higher interest rate)

3) LVRs

4) DTIs

5) CCCFA

then I would say its actually harder to buy now.

Imagine if food was too expensive and people were starving. So to get food prices down, the government said "only people earning over 100k are allowed to buy food". Food prices go down due to reduced demand, everyone pats themselves on the back, but actually more people are now starving.

No rush, FHBs. You’re not competing with investors, the math doesn’t work.

At these prices it does tbh. Seeing a lot of 6-7% gross yields popping up on Trademe. Even for standalone houses in 'transition' suburbs (not the poor areas, and not the middle areas, but the in between, which can come up nicely if it gets gentrified).

At a 6-7% yield with interest rates at 5%, 100% leveraged investment works.

AirBnB also works in select locations. Though check with your local council...

Good time to get in before prices adjust. The market takes a year or two to fully absorb interest rate movements, but with the mortgage book as short in maturity as it is (90% 1 year or less, with more than half 6 months or less) it should be quicker this time.

The low kiwi dollar is leading to record prices for our dairy farmers, so export led growth should flow through the economy.

There is a heck of a lot of stock on the market right now so I'd expect price rises to be muted this year, and perhaps pick up steam a bit next year, dependent on the degree of fast track consenting and speed of build in each local market.

5% interest costs, 0.5% on rates, 0.5% on insurance, 1% on maintenance. Getting pretty tight there, without accounting for gaps in rental and any management costs, let alone valuing your own time.

It could work out OK with those yields. If the value of the house keeps up with inflation (which is a reasonable assumption in the long term), then you make about 2% gain per year off the banks money.

Perhaps they'd do better in a managed fund, although that might be the next big crash.

100% leverage into an investment where you project 2% returns sounds like some kind of fever dream to me, but each to their own.

That's not the calculation. Suppose you find a house that you can rent for a 6% gross yield, your net yield (not including interest) is maybe 4%. You use equity in your own house such that you get a loan covering 100%.

If mortgage interest rates are 5% and you're on interest only you get a yield of -1% plus (or minus) any capital gains, your tax bill should be zero given you can deduct interest again, and you haven't invested any of your own money.

It's marginal and will quickly turn south if capital gains are negative, but I can see some investors getting back into the market, particularly if they expect rents to increase and interest rates to come down further, so the net yield could turn positive.

This is what some people were thinking in 2020 - 2021:

Suppose you find a house that you can rent for a 4% gross yield, your net yield (not including interest) is maybe 3%. You use equity in your own house such that you get a loan covering 100%.

If mortgage interest rates are 2.5% and you're on interest only, you get a yield of 0.5% plus (or minus) any capital gains, your tax bill should be zero given you can deduct interest again, and you haven't invested any of your own money.

Throughout history, there have been many financial fatalities of the carry trade. There will be more in the future.

6) Building smaller houses on smaller sections, so even if you get a house, it isn't like the one of your youth, with a backyard and climbing trees.

Unfortunately we have yet to appreciate the fact that a lot of new supply has created a price floor for anything arguably superior.

A five bedroom house on a 400sqm section of land is pushing $1.5m in far-flung suburbs. A four bedroom duplex will scone you for $1m.

It works if you have things like parks and playgrounds on your front doorstep like we do (planned developments do get some bits right), but for almost everyone else the houses are proving to have significantly less amenity considering that adding another bedroom seems to add $250K - $500K once you get past four double-bedrooms.

Yes very important point, the entry level shit boxes will never appreciate to allow you to move tot he next step of the ladder, No they will just keep building more of them, so you have no ability to move to the next ladder point, thus there are no buyers of that next layer up, ... and its turtles all the way up.

I suggest that over time perhaps the distance in legs of the ladder will close up somewhat as people can only achieve what a buyer can pay.

If I was a FHBer I would try to buy something that could be developed in time, ie land is bigger house is crap.

Right now developers are not really active so a good time, perhaps this is why regional nz is doing ok vs akl shitbox market

We have to recognise that younger generation don't have our preferences. In reality those small "shit boxes" are insulated, double glazed, electric sockets on every wall and room for a microwave, extractor fan in the bathroom. They are going to be less draughty in winter and easier to maintain

It's less things to worry about in the short term when you have a new family, but over time things like kids bikes and so on create a bit of a head-ache.

There's a difference between having 'space' on a floorplan and having 'usable space' (e.g. proper storage etc). It's a good stepping but the problem is that the price of anything over and above what I have now has accelerated into the sun.

So I would have to get a lot more usable space for the kind of money I'd have to front up to move to a different style of housing. It's like the housing ladder has the rungs spaced out about three times as far once you get to four bedroom/duplexes and the jump to anything better than that has been pushed up by the premium charged for newer but far smaller houses on tiny parcels of land.

I would prefer to pay an extra $300 in electricity over winter to have a full sized kitchen, a backyard, a garage, and storage space. And those shit boxes are hot boxes in summer, so any saving in heating costs is probably lost on paying for air conditioning all day and night over summer while those in older homes simply have to open a window or door for a breeze.

https://www.1news.co.nz/2024/12/15/a-sauna-without-the-fun-calls-grow-f…

And very very hot in summer; there was an article about it in the Herald a while back.

I can see that from the townhouses built across from us - tradies have told me they're horrible to work in as so ridiculously hot. No way I'd buy one.

As usual, Nelson seems to keep holding against all odds. Must be from those retiring as there isn't a great average wage here nor high jop opportunities either unless you work remotely.

There was an article in The AFR on that exact point today.

https://www.afr.com/wealth/personal-finance/major-parties-housing-polic…

"Major parties’ housing policies will trap young buyers in lemons

Through constrained supply, owners of these types of properties [single family homes] will therefore continue to see the desirability of their homes, and capital values increase, providing for strong equity creation and expanded property investment opportunities into the future.

For generations of Australians, a key motivation of home ownership was the expectation that, through the twin drivers of their own hard work paying off the mortgage along with some capital appreciation, subsequent steps up the property ladder would be achievable.

However, first home buyers today – encouraged into sectors of the market with a seemingly limitless supply of similar property [apartments] that can be released as prices strengthen – are now finding their move up the ladder suddenly becoming harder.

The fortunate few, often with parental assistance, are those who can afford to skip the lower rungs of the ladder. However, for the majority of first home buyers, it will become increasingly difficult to move into a more finite asset class that offers scarcity – a core driver of strong capital growth. What was once a reliable mechanism for financial mobility within society would be out of reach for many.

And therein lies the rub. Those who benefit most from lower prices on the way in – first home buyers, who have worked hard to save and buy – are those most reliant on the value of their homes rising to help build equity for their next move."

You could argue point 6 applies at any time for a growing city. 80 years ago my house in centralish Auckland was some kind of farm (and within walking distance of a tram into Auckland City).

Pretty grunty increase in demand…no concerns that it could be the market finding its trough if sellers are now accepting offers?

Equilibrium might be found later this year maybe 🤔

Season ‘25 & ‘26 of NZ Inc is going to be bloody good viewing regardless!

Down down in ponzi town. Cobid bubble was totally artificial. Throw in more normal interest rates, Govt restructuring and ongoing recession and there you have it.

Attention Vendors: your reality is served….cold. Take the money now before the value keeps tumbling.

"Vendors: your reality is served….cold. Take the money now before the value keeps tumbling."

The Block NZ producers paid $6.25m for the site in Browns Bay, which included removing the existing house and completing the four townhouses to shell stage

The four-bedroom homes on Beach Road, in Browns Bay, fetched a total of $5.88 million – well below the $6.25m the Block’s producers paid for the site in 2022.

That translates to an on-paper loss of $370,000 – and does not appear to include the cost of the build, the fit-out, and the marketing of the homes.

https://www.oneroof.co.nz/news/townhouses-from-cancelled-block-nz-sell-…

The origonal house was sold for $2.5million in 2022. The preparation of the land, and building the houses to shell stage, must have cost $3.75million, which seems an incredible amount.

If the producers did buy the site with houses to shell stage for $6.25million, then the vendor (probably a builder) would have been rubbing his hands with glee and pouring glass after glass of Moet for himself and his mates!

It wont be until the 2040's that all time high's are reached again.

Wow…huge statement…crystal ball is strong!

Japan historical property graph is exhibit A for what is unfolding

Yep, fair call…Ireland had a decent crash…maybe that could be an interesting comparison also?

They had a decent crash, their first year falls were 7% in Greater Ireland and 9% in Dublin. Their crash took 6 years to bottom out and were roughly 50% down

Ours peaked at $925k November 2021 and by the first year had fallen to $806k in November 2022. That's about 13%. We're about 3 years in and 19% down from peak value.

Every crash is different of course, not saying we'll end up with an Ireland style end result, it really depends on what happens with immigration I guess?

Its worth noting too that inflation in Ireland in 2009 was negative 4%, and then positive at ~1.8% for a few years.

As Granny Weatherwax pointed out, using tealeaves runs a much lower chance of getting shards of glass in your eye.

I prefer a yield based financial prediction.... the market will stop falling once there are more buyers then sellers, probably once investors return. Their return is ENTIRELY predictable based on "doing your numbers"

As TA Says investors are "Not active in the Market" and will not return until they investment property becomes less cashflow negative.

Its funny none of the Spruikers on this site want to propose that level as once they run the numbers they understand how far down it is...

I also think a lot of investors understand how seriously lost NAct are at the moment and how much of a real chance the left have of returning unless growth growth growth puts cash into peoples pockets. that means bright line capital gains tax and the dreaded reversal of interest deductability

...& likely a wealth tax to fund their ethnostate.

"Everyone Must Go" will be a popular meme if Labour/GreensTPM are returned next year. In the event of current close polls continuing I'd predict ongoing weak housing demand & no significant recovery through 2026

Thats exactly what I first thought when I heard the slogan LOL.

Hey, maybe Trump will offer New Zealanders refuge in America like the white South Africans? I've heard Florida is very nice.

Take your snorkel

WWH: Working in some Pratchett? - style points!

But Christchurch is doing WELL... nevermind.

I'm following the Chch market closely (wasting too much time on TradeMe, open homes etc) as we have a genuine need to upsize due to the unexpected, alarmingly imminent arrival of twins on top of an existing toddler.

There definitely seems to be a lot of stock sitting, or vendors "caving" and accepting some juicy price cuts in order to sell.

Speaking to an agent friend (who I genuinely do trust as I've known him for many years and he has nothing to sell me) he seems to think in particular it's your newer subdivision type areas where vendors have previously over-extended themselves to buy a "boujee" house and now factors such as higher rates (they purchased at lowest rates), job losses etc dictate sale and there are big discounts on offer.

Heck one agent I recently met at a viewing straight up said to me 'the vendor needs to massively adjust their expectations to sell this house'.

The new build townhouse market is on its arse as well, but that is a different category of property and I'm not following that much.

That being said, good family homes in the desirable school zones with a bit of land etc seem to be selling well enough.

If anybody has any good ideas for extending a 3 bedroom 1 living modern build house with only a small patio area and internal access garage to work with, then maybe you can save me the pain of house hunting for the expanding clan (it's already sad enough I might have to drive a minivan) and I'll just spend the cash to upgrade the current house.

Not sure about code acceptable solutions for building up on existing houses these days (eg wgtn requires an extra rebar in 2 storey foundations for new builds) however that used to work quite well in the distant past - assuming you're in an excellent area & want to stay there. I suspect that todays RCs, Engineering and code reqs make it untenable.

Converting an int access garage seems common esp in Auckland where a relative was looking for a house last year. Youd want enough space to add a standalone & probably require RC for plot ratio.

In the current economic environment reno build tender prices should be competitive

Thanks, helpful to know.

Our place is two storey already (only the garage is single level i.e. the upstairs isn't built over it).

We don't actually need the garage as we have excellent off and on street parking - as long as I sell my pride and joy which I'm going to have to anyway as I'll need some boring family wagon to cart the clan around in - so I have thought about the idea of converting it completely into a second living room (walling off the current laundry area) but I suspect the cost of doing so would probably result in us being a similar position if we just sold and bought a bigger house. It would also diminish value for a future buyer who wants a garage.

The other option could be some kind of very well-executed 'outdoor room' in the patio. In fact another property near us did this and we viewed it when it was for sale, and quite legitimately - as we viewed it - even when it was bucketing down with rain the outdoor room with lighting, heating, weatherproof louvres and blinds etc felt like a second living room.

Building an upper level extension over the garage might be doable at a reasonable cost. Minimum disruption, existing access & no change to plot ratio.

Easier to modify to satisfy engineering reqs, add beams etc

Hate to tell you this, but with three kids you are going to need a garage. Just wont be able to park a car in it.

My advice would be if you have very young kids, then you have time before needing a high school, so school zones are not that important yet. So look for a family home on the outskirts of the good school zones. Then you can upgrade again when the oldest starts high school without too much disruption. As an example - Mairehau is much cheaper than St Albans, Casebrook is cheaper than Bishopdale (which has shot up due to now being in the Burnside High catchment area), Spreydon is cheaper than Somerfield.

You are clearly up with the play.

Desirability of Christchurch is clear with 17 properties from 22 selling under-the hammer today.

Next all time high wont be reached until the 2040's.

Sales up, prices down…? Capitulation!

Sales up 17.5%

Stock levels up 21.2%

Yeah, so much for the increase in sales.

I'm sure Riverhead will be immune.

Rumour has it that the "River" will be replaced with "Richard" soon.

Savage, this is fantastic for those that were patient enough to wait.

Congratulations purchasers...

I feel the only area that is yet to turn is the Wanaka / Queenstown market. I can see there is a fair bit on the market but the prices are still way up there for a place with few jobs. Trying to live off retirement boomers is only a medium-term game.

QTown / Wanaka / Waiheke is unique, but not immune from price correction.

watch overseas events , if housing in USA rolls over so do the above

I think Airbnb income is helping prop them up too. You can pretty easily clear $60K a year on a modest three-bedroom, with the main limiting factor being the GST threshold and not wanting to go over it. Even more if you're willing to GST register.

I thought GST was on all airbnb now?

It's a bit of a mess. Under the new rules, platforms like Airbnb and Bookabach now charge GST, but short-term rental owners (operators) do not, unless they exceed the $60k annual income threshold. If an operator earns more than $60k, they are technically required to register for GST.

If your property is GST-registered and you later decide to sell it or convert it to a non-taxable use (e.g, a long-term rental or your own residence), you must pay GST on the sale price or market value. This means that if you rent out a $1 million property, surpass the $60k threshold, and later sell or move back in, you could face a pretty significant GST bill.

In practice, many people may be ignoring this requirement, but if you want to operate legally without having to register your property for GST and potentially face a massive GST bill, you need to ensure your short-term rental income stays under the $60k threshold.

Wanaka got down to 100 listings in August 2021. It's now 382.

Nothing you can live in under $1m

NZ HPI only down -0.2%, AKL -0.1%, hardly enough of a fall to justify the DGM glee in the comments... median sale prices are likely being skewed by all the townhouses developers are struggling to move (or in AKL at least)

If they are struggling to move the townhouses, how is it affecting the median sale price? Wouldn't the conclusion be the opposite?

Sorry I worded that badly, my guess would be developers are finally getting desperate enough that they're dropping townhouse asking prices enough to the point they're starting to sell, which is pulling the median sale price down. I wish REINZ would release sales stats based on property type, they obviously have the data internally.

NZ at -1.4% for the year is not really headline worthy. The market is starting to clear, prices are likely bottomng out. This year will be +/- 2% and then gradually moving higher again.

Sales up 17.5%

Stock levels up 21.2%

What is exactly starting to clear? The bank accounts of the overextended?

FYI - That table/image with the 1.4% is labelled as 2024.

Well spotted. Thanks.

Below that at the bottom it says 2025 REINZ national is -1.4%.

@Greg, you've got the January 2024 index not the January 2025 one up

Very mild declines, 1.4% over the year and 0.2% over the quarter (0.8% annualized).

Nothing to froth about.

clearly there's an increasing amount of people looking to take advantage of the discounted prices.

once unemployment peaks and people feel more secure....

That's the spirit! Have a great day.

Put in historical context, any declines in seasonally adjusted prices are significant, particularly in the context of wage inflation. Any increase in house prices that is lower than the rate of wage inflation is a real decline. According to Stats NZ, wages in the year to Dec 2024 were 4.3% higher than Dec 2023. So, a 5.1- 5.7% real drop in house prices last year.

I can see the sweat beads on your forehead and smell the rancid turd, that you are ever intent to polish the bejesus out of Rookster.

The market is halfway into a 6 to 7 year decline, the like of which PROPERTY CRASH, has never been witnessed in NZ before. Only the milder crash of the 1970's can partly compare.

With Inflation raging over 20% since 2020, the current property crash is, in REAL terms a -30% to near - 45% Crash NZ wide. IN USD much, much of a crash. We are still rolling crash crashdooms hill.....

This is where the Overleveraged property gamblers, lumping it all on the black get a mighty comeuppance.

The warnings have been made since 2021, and some are still to learn this gambling lesson.

The market is halfway into a 6 to 7 year decline

we are only 2 months in to the year with a 0.2% decline in the last quarter, let me know when we are at a 3.5% decline this year.

some areas showing a 50% increase in sales.

With Inflation raging over 20% since 2020, the current property crash is, in REAL terms a -35% to near -50% NZ wide.

Inflation is good for those with manageable debt. (don't get me wrong inflation is the devil otherwise).

The warnings have been made since 2021

and seen in 2022 with a 20-30% drop, flat since then with mild 1.4% drops.

Nearly 3,800 sales, nearly 9,000 listed in January. That's not good for your spin.

Did anyone else hear all of that angry yelling that was coming out of the One Roof offices today when this data was released?

Denial, anger... next is bargaining

Townhouses in Auckland, Christchurch and Wellington are extremely distressed. They will both skew data with number of sales and pull down averages

Standalone houses in traditional suburbs are in a very normal and stable market now

In reality and in real global terms ie USD. and adjusted for inflation, NZ house prices are more than 50% off their peak. They would have to double from today to hit that peak again

In reality and in real global terms ie USD. and adjusted for inflation, NZ house prices are more than 50% off their peak. They would have to double from today to hit that peak again

who sells a house to USD? clutching at straws here.

No one sells in USD. Its just a real world marker to qualify real value. Top line houses prices in NZD could triple but it wouldnt mean that much if the USD was at 0.25 and inflation was 20%.

I am also not sure what straws you think I am trying to grab on to? Strange thing to say.

NZ house prices are more than 50% off their peak.

When actually it is %18.9.

In USD terms and adjusted for inflation.

You don't buy or sell a house in USD so why compare it to that? everything in NZ compared to the USD has dropped 20% since the peak, all assets, all savings, everything.

Far from everything. This situation has increased the NZD value for milk powder for example. That ls why global everything is benched to USD. I’m not arguing a point, I was merely making one. Pointing out the stark reality of the decline

how about comparing house prices to a Big Mac?

I agree, but those adjustments should be used for all investments.

That’s the straw I think ole mate is referring too, it’s cynically bias when only used to highlight one asset class.

Not really, if you have a diversified investment portfolio its likely that 80% is offshore in USD...

True!

everything in NZ compared to the USD

80% of your portfolio is offshore…shit ITG, it ain’t the property ponzi that’s stealing all the money that could be getting pumped in “productive NZ businesses” then eh 😉

Valid point…but also ignoring the clear cynicism of the original commentator, no one on here talks about their TD return in inflation adjusted USD measures 🤣

it would make property look worse as us shares have increase as nzd has fallen

Yeah wow, the S&P 500 accumulation index in NZD is off the chart!!

I wonder how many people understand the concept of opportunity cost.....

you can't live in a S&P500.

"you can't live in a S&P500."

Perhaps you should calculate the opportunity cost from your purchase price and cashflows first. See how they compare.

You can't live in a house you can't afford

You can if you're renting it!

Standalone houses in traditional suburbs are in a very normal and stable market now

Can FHBers afford them here?

if not who are the buyers, downsizers? investors wanting to bowl and build more distressed townhouses, not trying to be a dick, just want to understand if a marginal old sellers going into a rest home sells, what do the buyer profiles look like?

These potentially are the best buys you could make in the next 2-3 years, crap old house, big land in a suburb that gets gentrified next cycle.

What suburbs do you consider or are you outside Auckland?

You probably need 600sq m 800 better, they will not be cheap, that shitty sierra one i linked at 1.65mil sale 2.4mil cv is a possible example. Glendowie is expensive but the land value has now fallen 50% in $$ terms already and that house is livable if you had to ...

now 2k a sq m ... at what price sq m price to you think investers or devoloers re enter?

I think Kenyon Clark and the Williams boys have brain washed everyone. The focus on land for townhouse development is crazy. You have to SELL the final product. Not just create it

A traditional buyer in these suburbs is probably a 55 year old couple, who want to move for work reasons, family reasons, school reasons and maybe they want more space. They are not investors or developers. They are however smart and see value

Conifer Grove fits this profile.

Although some of the houses need some fix up, have seen your exact buyer profile active there.

Its an OK Suburb, represents good value and I know a few people who live there and have a holiday home, rather then a flash home only in AKL. Most are cashed up, no mortgages. But not yet retired and salaries holding them in AKL, aged 55 up.

There is s major difference between Duval and Williams Corp, like chalk and cheese.

You can not compare the two, different business models.

The first was always going to fail, the second is run as a successful business and is very profitable

"There is s major difference between Duval and Williams Corp, like chalk and cheese.

You can not compare the two, different business models.

The first was always going to fail, the second is run as a successful business and is very profitable "

The question isn't about business models, the question is about credit worthiness. Profitability and cashflow are two entirely different issues. Can the business repay their debts as they become due? Such as to suppliers, employees, Inland Revenue Department and financiers?

Developers are giving non cash incentives to attract buyers. Lack of sales by developers means reduced revenues and reduced cashflow.

Is this how Wiilliams Corp is attempting to manage their cashflow situation? By delaying payments to their financiers?

https://www.nzherald.co.nz/business/companies/construction/williams-cor…

https://businessdesk.co.nz/article/finance/d-day-looms-for-williams-corp

"Fool me once, shame on you, fool me twice, shame on me."

Reality is that it just made total business sense to have a 12 month notice period, for planning purposes.

Labour made such a mess of the NZ economy so it was to stop a run on withdrawals if people needed money quick l.

Williams Corporation is a financially well managed and profitable business and there has never been any instances whatsoever of their accounts being not paid on time nor their shareholders not receiving their interest payments or withdrawals.

If you actually spent some time looking into the financials, the sales and the presales you would see that they will not havd any trouble paying their shareholders.

Tell us you have put money into investing with Williams Corp @ 10% returns without telling us :D

I think he's actually Matthew :-)

Reality is that it just made total business sense to have a 12 month notice period, for planning purposes.

"there has never been any instances whatsoever of their accounts being not paid on time"

This is not a 12 month notice period. That is an attempted deflection from the cashflow issue.

Payments to investors in the funds who had already requested a withdrawal were delayed.

Attempting to spin the above narrative as merely a notice period extension may cause people to raise questions of trustworthiness and transparency. Others can draw their own conclusions from the company's statement to the fund investors below.

“This letter is to inform you that we are extending the repayment date for any withdrawals/redemptions in respect of each of the above wholesale finance entities from six months to 12 months pursuant with the relevant investment documentation,” the letter said.

“These adverse market conditions are why we have decided to exercise the extensions clause related to redemptions/withdrawals. We understand that this may cause an inconvenience to investors, in particular those who have requested a withdrawal, however, this in the best interests of all investors"

CAVEAT EMPTOR.

CN, have you actually looked at the financials for Williams or Wolfbrook or are you just one of these Tall Poppy knockers?

I suggest you do some homework and then come back to us with your findings.

"CN, have you actually looked at the financials for Williams or Wolfbrook or are you just one of these Tall Poppy knockers?

I suggest you do some homework and then come back to us with your findings."

This comment is another attempted deflection from the core issue.

If people with undisclosed vested self interests, are going to make unsubstantiated assertions (especially in regards to large sums of money such as a sale of a product or service where the recipient receives over $1,000, providing credit, or providing financing), they should be prepared to have those assertions scrutinised.

There is s major difference between Duval and Williams Corp, like chalk and cheese

Spoken like a Williams employee

"Spoken like a Williams employee"

There is a potentially undisclosed conflict of interest, potential vested financial self interest.

Not an employee at all!

Educated on what is going on and just get annoyed with people making comments that are just plain ignorant.

If you have facts then quote them but if you do not, then do not!

Just teasing, that was some sale pitch for Williams which is unusual for a disinterested objective observer.

The ONLY difference between Duval and WC is one is run by an ex-bankrupt with no money and the other is run by a kid with a very rich father.

Wait

I thought "bank economists" 🤡 were forecasting 7% rises this year.

Privately the ones I drink with (self medicate with really) no....

But the releases from their departments at the bank yes....

do as i say not as i do

The "media" in New Zealand does seem to be an endless stream of propaganda and lies.

I would cross out in new zealand,

The "media" does seem to be an endless stream of propaganda and lies.

fixed it for you... I am not to sure I believe everything on X either.....

Agreed. What they say in private over a few medicinal ones is different to what gets published and/or cherry picked.

Exactly this - same with central bankers, what they think privately may differ substantially to what the say in public statements. You then realise that you are getting lied to in every which way by both state and corporate interests - the entities are telling what is best for their survival and not what the individuals working for those entities really think.

Let's not forget the fundamentals - the NZ housing market is one of the most overvalued markets in the world, for a housing stock of pathetic quality.

yeah its probably worth looking at the mean of the OECD and the mean of countries more like NZ, Ie aussie canada etc is and then working out how much NZ would have to fall to revert to said mean

there you go interest.co.nz an article that would get 200 comments at least

Not sure why you say the housing stock is pathetic quality ?

What is your evidence?

Thousands of earthquakes in ChCh and we didnt have a single property badly damaged at all!

luck? a mate got 2 written off in Sumner , full payout and THEN bought them back fixed and rented out 8)

had to sue in court though

No didnt have any near water and Sumner returns on rents just do not work and nothing really I have seen with upside over recent years.

Msny People have done really well financially since the quakes in ChCh.

Thousands of earthquakes in ChCh and we didnt have a single property badly damaged at all!

What sort of absolutely useless metric is that? The sort of metric this guy probably uses

https://www.reddit.com/r/BeAmazed/comments/igp70o/single_home_left_stan…

January is generally the low point for prices each year with a bounce back in Feb. Ergo, the falling price does not neccessarily indicate further falls are looming. Wait for Feb's stats to see. A 'lower high' in Feb would be telling ...

Anyway ... the flat-line is in tact. And from the recent bottoms, we can see a 'floor'. If that floor gets broken - run for the hills! (Probably won't though ... far too risky for the banks. They'll probably screw savers by reducing rates for deposits, while slicing a few points off shorter term mortgages to lure buyers back in, and plenty of - once again - short term 'sprecial offers' to drive the sales. Don't get sucked in - this flat-line will likely last for years so the bigger your deposit, the less interest you'll pay - unless our woefully bad RB drops the OCR way below neutral.)

the old bearish evening star pattern...

I prefer point and figure for property

bigger risk is that in this trade war china offers free on prem AI Models stopping the major US companies ability to monitise their ai offerings ie more deepseek etc if you can hurt the mag 7 you hurt USA, guns are out now, its economic warfare.

an equities correction would be very bad for NZD as we are a risk currency (lower = more imported inflation)

and it would also impact kiwisavers , do not discount its very very possible, on the plus side imagine if Xi dies of a stroke tomorrow, and the next guy was more of a moderate.... world suddenly pivots to lower cost model again, equities go higher still

its game on, as always hedge well

Looking at the B&T auctions today and it clear that the properties that fetch good prices, even in these troubled times, are single level brick and tile houses, preferably with internal access double garage. If you are looking to buy a house in Auckland these are the configurations to look for. With the plethora of blocks of townhouses sprouting up everywhere and many older wooden houses requiring maintenance these sorts of houses are where the comfortably off and actively retired, sensible people, will live. Perceived as sound.and easy to maintain and sell, they will always command a relatively premium price.

Many of the sales you refer to are in 'car-ville' locations. i.e. you need to get into a car for just about anything except to visit some small, sad local park. Check out where they are on decent maps. Schools? Car. Shops? Car. Entertainment? Car. Sport? Car! Nearest public transport stop? Long walk and infrequent service!

As Auckland becomes denser, people in car-ville locations will spend a heap of time in traffic. Sorry, the values of such places - even though holding their own at this time - won't appreciate anything like as fast as places in well connected locations. This happens in every big city as it grows. Auckland will be no different.

I don't think comfortably off and the actively retired, sensible people will be taking the bus anytime soon.

it took me 1hr 40min to get 40km on Monday left 7:20am dropped child at school and onwards to office got there at 9:00am

that was not a cross bridge, just Silverdale to Takapuna, a better trip then southern motorway...

It's not about taking the bus, it's about having things close enough that a car is not necessary.

This is where Wellington has it all over Auckland and Christchurch. I've lived in three different Wellington Suburbs in roughly the past ten years. Thorndon, Newtown, and Aro Valley. Every one of them had:

- Supermarket(s) within 10 minutes

- Large parks, hills, *and* bushwalks within 5 minutes (the greenbelt is such a great example of the kind of generous foresight planners had but now lack)

- Schools (primary and secondary, public and private) within 10 minutes

- Medical centres, dentists, pharmacies within 10 minutes

- Weekend farmers markets within 10 minutes

- Somewhere to swim within 10 minutes (beach or pool)

- Local pubs, restaurants, and cafes within 5 minutes

- A CBD within 10 minutes

- Community fairs and activities

- Sports facilities

- Etc...

The times above are walking - not driving, cycling, or public transit times. There are so many places in Wellington like this. Many with spectacular views and abundant native wildlife visiting your home.

All homes had sun and a backyard - I even kept chickens at one.

That weird guy with bad blonde hairdo is itching to press that "kaput" button for the world economy.. Expecting the bottom is a bit further to reach!

Greg the Grenadier, keep them coming.

I made around 50k today, guess that's how the investors do it, with those paper gains

*saved.

are you buying today? careful you might lose your savings.

30% down from here I could buy mortgage free, I'll wait. No rush.

There certainly isn’t. Property is pouring onto the market daily.What surprises me is the number of more expensive lifestyle and newish executive homes. Virtually none are selling. There are already heaps on the market. Death , divorce and debt are the usual drivers. Very interesting times.

Death , divorce and debt are the usual drivers.

There is another one operating under current conditions that most people may not see or recognise: selling by departees.

no hurry to buy when you rent these for such a great rate while prices are falling

He who hesitates is lost or, in your case, a terminal loser.

TTP

Getting more agitated TTP? Oh dear, don't do something silly like break the law in your anger...

you made way more because you have to repay 96k during the life of a 50k mortgage, ie you just got 50k cheaper house and the ability to have a cheap international holiday for the next 30 years!

50k loan 5% interest rate 30 year term = $268 a month or $3,216 pa payments

- Interest + fees paid: $46,480

- Principal repaid: $50,000

- Total amount paid: $96,480

if you get he house 100k cheaper its $537per month or $6,444 per year for 30 years (just wait and not only do houses get cheap but so does the quality of your international holiday each year)

- Interest + fees paid: $93,320

- Principal repaid: $100,000

- Total amount paid: $193,320

Not sure where these tumbling prices are in Christchurch?

Just watching auctions this morning and 13 out of the first 16 all sold,

The market is pretty warm in ChCh so nothing surer but prices will continue to rise after interest rate drop

The Man3, right again!

Property is so cheap in Christchurch because of its appeal or lack thereof and its low population numbers. Coming off such low prices if it is in fact happening is not hard. The Golden Triangle. That’s where the big boys invest and make serious dollars.

Property is so cheap in ChCh?

It is the most stable city market in NZ and is where you are able to make the serious money if you are prepared to work.

Those that put in the yards deserve every $ they make, ex agent!

Low population numbers? You havent got a clue, it is the second biggest population in NZ!

Property is so cheap in ChCh?

Low population numbers? it is the second biggest population in NZ!

Well it should be higher then shouldn’t it. But it isn’t because it’s Christchurch. Tauranga boxes above its weight. Because it’s warm and close to Auckland.

ChCh prices are value for money and gives more people the opportunity to own in the country’s happiest city.

If people are happy to live in the over populated Auckland then that is their choice, however we all know why it is over populated snd is very overrated.

Auckland weather is warmer and wetter and lifestyle not as good, with older colder homes.

Anyway no point discussing.

...so nothing surer but prices will continue to rise..

The data shows that they are falling though?

13 out of the first 16.

You do realise that agencies load properties that are more likely to sell at the start of the auction?

Working on the uninformed, clearly.

For all those still confused by RVs:

Economists explain Wellington’s 24% drop in home valuations

“If your property accounts for 1% of the overall property in the region, you pay 1% of council rates.”

Everyone on here understands how councils use CVs / RVs etc

The mystery is how Real Estate agents use them or chose not to use them....

in boom times they tell you property in this suburb is selling on average 12% above cv etc, One Roof does this all the time?

in bust its a big headline IGNORE CV...

you cannot run with the hares and hunt with the hounds without being called BS

and I am calling BS.

The man understands if you can buy at 50% of cv, you have a better chance of asking the bank to value it at full cv for future lending.

especially years later in a different part of the property cycle,

buying at low % of cv increases your ability to get credit later on

Everyone on here understands how councils use CVs / RVs etc

No they don't. I have to explain it again and again.

Need more negative news like this to support the coming interest rate cuts.

Keep them coming 👍

Negative? House prices falling is positive news 🥂

People calling the "bottom of the market" in February 2025 with unemployment on the rise and above 5%, skilled Kiwis leaving in droves, interest rates above 5%, average age at record highs, birthrates at their lowest since WW2.

These people claiming this is the bottom never correctly forecast the top. So how the hell they know this is the bottom is anyone’s guess. ITGuy appeared to be the most accurate at picking the top so I’d take his guess more than those who every couple of months claim this is the bottom.

I think he's right, bottom around 700-800K for Auckland median price. However, if inflation ticks up and we see rate hikes later in the year, I think it could go lower. We also will see unemployment this year move from 5.1% to around 5.5%, could be 6% by the end of the year.

House prices ‘tumbled’ in January? Not in terms of the HPI measure, the most credible measure. Down 0.2%…

Another disappointing clickbait heading from this website

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.