Auction activity maintained a fairly steady pace over the week of 23-29 November, with only small changes in the results compared to the previous week.

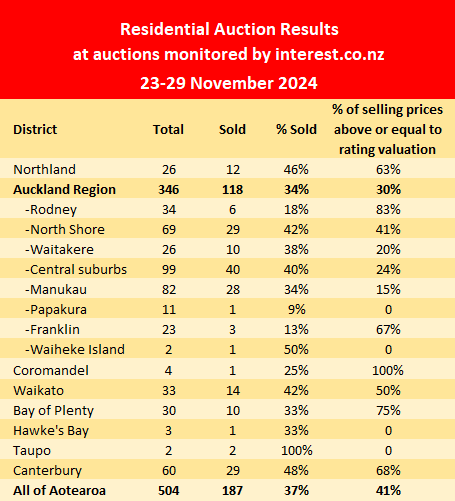

Interest.co.nz monitored the results of 504 residential properties from around the country offered up at the latest auctions, down slightly form 517 the previous week.

Of the 504 properties on offer, 187 were sold under the hammer, giving an overall sales rate of 37% at the latest auctions, up slightly from 35% the previous week.

These latest results suggest the market has found its level for the first part of summer, although with just three weeks to go until the Christmas/new year break, it's still possible there could be a last minute burst of activity in the next couple of weeks.

However, the latest results suggest it's steady as she goes as the market counts down to Christmas.

The table below gives the district-by-district results from the latest auctions monitored by interest.co.nz, while details of the individual properties offered, including the selling prices of those that sold, can be found on our Residential Auction Results page.

The comment stream on this article is now closed.

74 Comments

So this is peak boom......in the NZ property market.

Hell.......this bad.

If the hopelessly overleveraged, have not folded their wet, mildewed and blighted tent by now, they are done for, in 2025/2026.

With many industries slashing jobs and the ones that are still to cut, will be doing so right before Christmas ........ (the Grinch will be busy this Dec) or fold completely (holiday pay will cripple the already stench ridden, zombie businesses) as they cannot make payroĺ, debt and expense payments on the 20 to 40 % reduced incomes.

Santa's sac has been drained already in 2024.......and 2025 will be a year of harsh austerity.

No room for those singing the californiaponzi dreamin tune, to exploit NZ Inc- renters and would be FHBs,, in the NZ home/housing market.

The ponzi is like a dead snail, sizzling in its shell, on the sweating tarseal, in the summer sun.

Anyway and more positively, the sports look great, with Auckland FC just killing the opposition in the A-league and the NZ/Eng cricket matches looking like brilliant armwresting!!

Geckos are plucky forest creatures and truly glass half full types and always see opportunity and plenty of options to fill their bellies with flies and bugs........get out their NZ and diversify investments - your fly catching "means and ways" !

wait till 58 to afford a house, use ALL your Kiwisaver... and still have a mortgage

welcome to New Zealand, land of success....

https://www.oneroof.co.nz/news/couple-aged-58-empty-their-kiwisaver-to-…

Spruikers are allowed their own reality, but sooner or later the real REALITY will smack them in the face.

Where this age group is concerned, reverse mortgages are also a growing theme. This couple swapped rent for interest and to boot they got rates, insurance and maintenance costs thrown in. For some, moving next door to Zwifter just so they can hear "7% guaranteed increase next year" over and over, is the only way forward....

Always good to know that I'm renting some free space in your head RP, there is certainly plenty available.

🤣😂 Funny. You were the one that posted it less than a week ago. Obviously you're now regretting it.

Why would I be regretting it already ? we are not even in 2025 yet RP, check your calendar.

Now that you're owning it, that's a fair point. On the subject of calendars, will you be here posting beyond 01-March 25?

Probably not, don't people usually have to pay for good financial advice, not pay someone else to post it ? Perhaps interest.co.nz should pick the top 10 each year that had the best advice and give them a free 12 months subscription and a Gold tick next to their names. I might actually be worth staying on here.

Would there be an award for least accurate musings? They could be given a poopie emoji next to their name.

Perhaps interest.co.nz should pick the top 10 each year that had the best advice and give them a free 12 months subscription and a Gold tick next to their names.

Not a silly idea. Interest.co could also base this on 01-Jan predictions made for each coming year. Once upon a time, they used to re-post "comment of the day" too.

This aside, it need not be a competition and no matter what financial news is reported, either you want to financially support a good financial news platform or you don't.

Lots of negativity and catastrophising today - from an increasingly disgruntled DGM .......

There's no surer sign that the housing market is strengthening.

TTP

we will allow the DGM their own reality

(sarc re the bold letters)

@IT GUY - reality is certainly smaking me in the face - its tough - however i have learned from the last 4 years and wont find myself in this position again - the other realisty and this is true I made money the first 8 years I don't really want to say how much cause it is a distant memory and i am paying the price now (however i learned nothing it was to easy) to conclude its not easy making money on investment property now - there was a time i did make good money and was cash flow positive - lets see what the future hold

What bank lent them money? Looks like the CCCFA is doing exactly as I expected - stupid rules preventing young people getting into a house because they bought a coffee or something, while allowing this.

@jimbo - not lender as much as govt changing rules, central bank and high interest rates -

Except for using your Kiwisaver, I'd be advising middle-aged FHBs to do the same thing.

Don't buy now. Rent and save (and invest) like mad for the next 20 years. Enter the market at 60 with an 80% deposit, be mortgage free in 10 years and still have your nest egg for retirement.

Unless you believe we're going back to 3% mortgage rates and house prices doubling every 10 years, the calculation works out. It works out even better if you believe house prices will more or less stagnate in real terms over the same period, and interest rates will revert to historical norms. In this case the ladder only has one rung; you buy the house you intend to croak in.

I've done some numbers on renting vs buying in the past, if you started with a $150k deposit, invested the difference between owning and renting (about $2500 per month in my example), you could buy the house outright with some change to spare if house prices inflate by 5% p.a. and your investment returns 7% p.a. before tax.

Me personally, I'd rather guarantee my child the stability of having the same bedroom, backyard and school while growing up. Life's too short to only be enjoying the intrinsic values of home ownership from the age of 60, even if the numbers might not necessarily be the most favorable.

Me personally, I'd rather guarantee my child the stability of having the same bedroom, backyard and school while growing up

This is much less of an issue than people seem to think it is, especially in today's market. Landlords value high-quality tenants, and will pretty much fight each other for them. They're not kicking families out on a whim, or rushing to sell the place out from underneath them.

Worst case, your kid has to build a new treehouse. Seems like a pretty good worst case scenario to me.

Fair points. Admittedly I haven't had the best of experiences while renting so there's that. Where do these landlord fights take place?

Undisclosed location. Winner gets the young family, loser takes the 3 student flatmates.

Given how much hate landlords get, particularly from renters, I think this type of event could give UFC a run for its money.

We've moved a fair few times with our kids. Never bothered me as I moved a lot growing up (12 different schools!). Doesn't seem to have bothered my wife either, and she only moved once. Only time we had to move was landlord selling out to Kainga Ora. Every other move was to either a better or more suitable location.

But, when our [then] 5 year old asked why we moved so much, I took notice. It's also been very hard teaching the kids "our home is not our house" - especially when they also see the maintenance tasks that the landlord is neglecting to do.

Building a new tree house is not the worst case scenario for kids. It's being uprooted from their friends and arriving in a new environment where they have to make new friends all over again. It's going to someone's birthday party, or having them at yours, knowing that may well be a singular event that you may or may not reciprocate.

Kids are resilient, but they still notice.

I've done some numbers on renting vs buying in the past, if you started with a $150k deposit, invested the difference between owning and renting (about $2500 per month in my example), you could buy the house outright with some change to spare if house prices inflate by 5% p.a. and your investment returns 7% p.a. before tax.

Me personally, I'd rather guarantee my child the stability of having the same bedroom, backyard and school while growing up. Life's too short to only be enjoying the intrinsic values of home ownership from the age of 60, even if the numbers might not necessarily be the most favorable.

NZDan

Good for you.

That is a great example of a fully informed choice. Each person should do their own calculations based on their own situation to make a fully informed choice.

The purchase of a residential dwelling is likely to be the largest purchase by most households. The purchase price could be 500 - 1000% of the household's entire net worth.

How long did One Roof take to find that example? They're from South Africa and have been here 10 years so it's not typical. One thing with older buyers that's often left out is that many will get an inheritance/s in the not too distant future that could substantially pay down their mortgage.

With interest rates still being restrictive, the housing market is going to be subdued..

From the glory days of the favorite bbq topic being housing, it's now about how many roles are being cut within each one's companies... job insecurity is the number issue ATM

Interest rates may be restricted, but investors are happy to get a 5.5% mortgage and buy a rental with a 6% return.

"So this is peak boom"

Why is this the peak boom Gecko ?

Because it's spring and there are lots of juicy insects for lizards to eat.

Steady but low clearance rate whereas 63% of vendors left the room disappointed with the current market. It's not a stretch to expect exploding volumes and more like 63% clearance rates before a sustainable floor can be called. I feel with joblessness and liquidations still rising, a repeat of what happened earlier this year is likely. Come March 25, prices resume trending down. The benefits of lower interest rates will take some time - the lag effect. Local and Central Government are still cutting back and will be fiscally up against the wall for some time to come.

@gecko 😀you been working on that all week? Brilliant and some truths in there - rushed downstairs to grab my glasses to read it - thought the snails was escargot- but not today

He writes the same sh*t everyday... it must be depressing.

It's not all about your apparent state of mind. Others interpret Gecko's posts as hope and welcome entertainment :)

Some folks don't like the truth, so they lash out at others.. typical of the 2 above..

its more entertaining then you should have bought yesterday...

Well, you can't re-do yesterday.

But the sky might always fall tomorrow. Way more sexy.

@painter - hahaha great comment - had to read it a couple of times very funny - had a few beers last night so am a bit slow

Eh, you being slow ain't new... any other excuses?

@DGM no other excuses - at least the sun will shine for me again - if i may quote painter - way more sexiier thinking the sky is always falling - good day to you chicken little -

I love it that you roll with the punches

Probably the opposite, Friday nights must be giddy with the anticipation of unleashing some zingers in the morning.

Will I switch it up and not use caps this time, or double down and smash the caps lock key? So many choices.

Haha yeah true, clearly there's not alot going on for RP so this must be a highlight of their day.

Yep the Gecko scrolls, have been squeezed hard this morning, for uber relevant material !!

Them road roasting snails, are best left for the starving and low food option gulls to "chew and spew" on....

Anyway, glad your holding on, by the now near detaching fingertips and nails SAH - and giving the poor peasants a good, safe, dry house to live in. Sounds like your a good sort and not the nasty, garden variety, "cornered rat" landlord type..... that the above N1 seems to be, by his own accounts.

Great to see some rains today, greens up the veges and give them tasty flyies some moisturenessss.

Careful with your mention of the scrolls - it didn't end well for the last guy who talked about scrolls week in and week out! (Not a threat, just some friendly advice 😄)

found this one oneroof news - lots of green :)

https://www.oneroof.co.nz/news/new-zealand-house-prices-rise-0-7-as-int…

“brings the price tag of a typical New Zealand home up to $963,000.” - this is suspiciously higher than the REINZ median of $795,000.

Very suspicious. And no clear explanation as to how they came up with those figures (except to say it is the valuation that they are going by).

This, from the article: “The spike in the number of houses for sale on OneRoof over the same period points to renewed confidence among sellers,”

or it points to an oversupply of houses for sale that no one is buying because they are worried about their job or cannot afford the mortgage.

Haha what a ridiculous thing to say. Another layer of polish on the turd.

We can all see that the housing market is not in free fall as many here want to suggest.

Once again Canterbury is showing good sale numbers and Chch would probably be stronger.

Forget about commenting solely about the Auckland market as we all know it is only the way it is due to immigration and has made it a less desirable place to be living nowadays.

There are heaps of Auckland citizens that have headed south a d have told me that they shouldve done it years ago.

Some people went from ChCH to Auckland after the earthquake and love it. I think Yvil was one?

Auckland is a big place, there are really good parts to live in and some pretty awful parts, so yes some people will be pleased to leave. I was a bit jealous of the ChCh weather a couple of days ago when I turned the cricket on, but the day after when it was 13 degrees i changed my mind.

Yes there were so e that left for Auckland after the quakes and you can not blame them wanting to get out as it was horrific for most.

Personally decided to stay as I believed ChCh was going go recover snd wanted to be part of that, and no regrets staying.

There have been fortunes made by those that have put in the effort and despite what many here say about housing, there is still plenty of opportunity.

Moaning and groaning and continually saying that the market is going to drop is actually not helpful to yourself.

If you do not like the situation that you are in, change it by your own efforts.

That graph looks like a feline in rigor mortis trying to bounce…

@ Albert hahahah very good

Albert is hilarious- not

So many times we have heard it's a DCB from so many commenters. They can't think of anything else to say when property prices begin to rise.

Tron, many frustrated commentors seem unaware they can still enjoy living in their biggest asset even when it's falling in value.

Which ones on here are the frustrated commenters?

Like I said the other day, One Roof has my house price up and homes has it down so inevitably you cannot rely on the algorithms. If you watch what sells around you and you have a few smarts you can value your own place within $20K.

Oneroof is approximately 20% over real market price.

34% in Auckland after several meaty sets of interest drops.

"She dead mate."

Agree, while interest in housing is also dropping

Interest in people wanting to own their own home has not dropped!

Yes it is more difficult due to price rises but it is not going to get any cheaper where I reside, quite the opposite.

If you want to see expensive prices then Australia is the place to go.

$2million buys you an old fibrolite home in sydney if you are lucky unless you are a very long way out .

Yes there are some cheaper, but interesting to watch the Saturday auctions online from Sydney from Tom Panos, and you will quickly realise just how cheap we are compared to over there.

The housing market is still on life support.

As I have said many times, it won’t be properly resuscitated until 1/2 year retail interest rates are at 4.5-5%.

The housing market is just fine. It is the Ponzi aspect to it that is on life support.

2700 FHBs in October, and around the same number of investors, purchased houses.

November figures (out in about one weeks time) will be interesting.

North shore almost 50% above RV, considering all the townhouses, that's an outstanding result

1. This is the first time I've seen someone round 41% to 50%

2. North Shore doesn't have that many town houses compared to West and South Auckland.

3. What does 2. have with % sold above RV?

4. I am wasting my time replying to this

Spruikers gonna spruik.

It's actually 11 houses of 69 auctioned that achieved over RV.

Approx 16%.

Same as it's been for the last year or so. Nothing to see her.

Yep. On our street 2 houses gone within a couple weeks of listing. One was a pre auction sale. North Shore market is strong.

Or vendors are "motivated".

Plenty of SOLD stickers down here again even on places that have sat for months. The market is off and away again.

we will see HPI

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.