At first glance the housing market appeared to have a reasonable spring in its step in October but a closer look suggests it may not be as strong as it looks.

The Real Estate Institute of NZ reported 6681 residential sales throughout the country in October, up 10% compared to September.

Additionally the REINZ's national median selling price increased to $795,000 in October, which was up 1.9% compared to September.

Both of those figures suggest the market had a reasonable spring tailwind as it gears up for the busy summer months.

However there were also numbers that suggested the market may not be as strong as it seems.

First, although the actual sales numbers were up on September, the seasonally adjusted sales figure was down 2.6% for the month.

One possible reason for that may have been that there were five Saturdays in October this year but only four in October last year, which could have affected sales patterns.

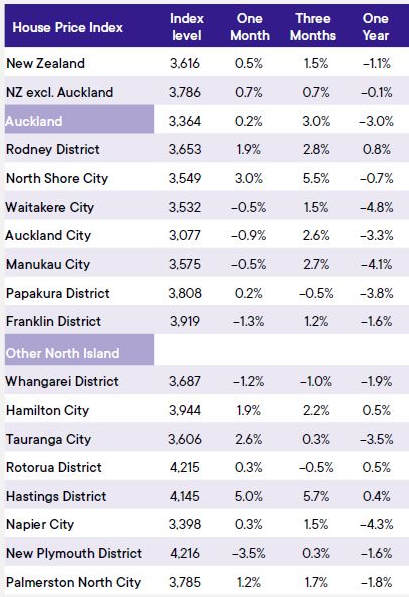

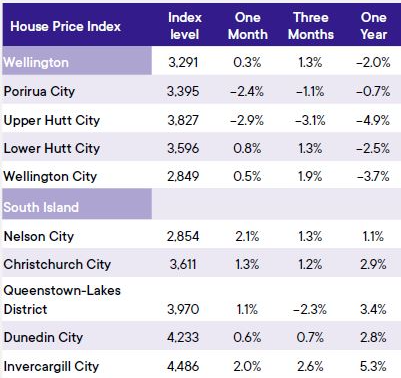

And although the median selling price increased by 1.9% in October, the REINZ's House Price Index, which adjusts for differences in the mix of properties sold each month and is considered the more reliable indicator of house price movements, increased by just 0.5% for the month suggesting price movements, while positive, remain fairly subdued.

What all that suggests is a market that's warming over spring, as it usually does, but is not running away in leaps and bunds.

Perhaps that's because the biggest changes to the market figures in October were for the number of new listings coming on to the market and its flow on effect on total stock levels, which were up 7.7% in October compared to September.

"Local salespeople note that some buyers remain cautious about overpaying for properties due to relatively high interest rates," REINZ Chief Executive Jen Baird said .

"This environment encourages buyers to be more strategic in their approach, making them feel confident in negotiating with vendors to reach an agreeable price.

The increase in available properties provides buyers with the opportunity to explore a diverse range of options that better align with their individual needs and preferences, allowing them to take their time shopping around," she said.

The comment stream on this article is now closed.

REINZ House Price Index - October 2024

Volumes sold - REINZ

Select chart tabs

You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

128 Comments

Pretty subdued especially in the big cities which lead. So much for FOMO driven by rates drops.

Also hello inflation my old friend. Don't expect too many more drops in the OCR if the FED is anything to go by. Swaps are on their way up.

NZ up 1.5% in the past 3 months, nothing to see here.

Spring has sprung.

It will be FONS soon with Mr Trumpy

FONS?

Fear of not selling

Good month for Hastings.

HPI increases 0.5 percent for October …….

TTP

The table in the article says 5.0% for Hastings in Oct. Is that a transcription error?

HPI up 0.5 percent nationally.

TTP

The NZ real estate market has failed to fire up after the most recent interest rate reductions.

Suspect it won’t kick off until we see a 12 month fixed rate of 4.5% and that could be a while off yet.

In Auckland it’s difficult to find a rental investment that stacks up and investors are holding back. First home buyers also seem to have gone off the boil.

Will be interesting to see how the summer selling market goes.

In Auckland it's difficult to rent out a property now period.

who would want to live in Auckland....

1/3 of New Zealands population...

By choice or by necessity though? It's nice to visit from time to time but if I stay too long I'm reminded of why I left - I'm in an industry that enabled me to take my income with me.

Necessity, that's where all the work is in certain industries, it was pretty much Auckland, Wellington or Christchurch for me .

Yes all people make decisions based on your personal preferences.

I know many people who would not live anywhere else in NZ even if you paid them double.

I'd take Christchurch out of those 3, there only 1 thing I don't like about Chch, earthquakes, I assume that's a reason for many.

Chch is looking like a nicely developed city atm.

Loved Christchurch pre quake.

You'd exclude Christchurch because of earthquake risk, but leave in Wellington? Interesting logic.

Especially when you consider all the unreinforced masonry in CHCH is long gone and replaced with current code buildings.

I would have thought that all NZ is at risk from quakes, all the time..

Not sure that's true - some places just have volcano and/or tsunami risks...

He's a rookie. Very opinionated but a rookie nonetheless.

Necessity or not, that doesn't matter, fact is 1/3 of NZ lives there and many new migrants mostly stay in Auckland when they arrive, for a while at least.

Besides, dare I say, Auckland is a pretty good city to live in. I lived there for over 20 years and enjoyed it. Mind you that was a few years back, before Covid.

Everyone off to the lucky country. 3 of my friends have left, were renting in Auckland.

As long as 2.5 x or 3 x as many homes are being listed compared with the number selling I suspect it will remain a buyers market

The shore out performing again...

Yep the Shore up 5.5% in 3 months. Property across the road from us sold pre-auction in less than 2 weeks anecdotal sure but with more rate cuts to come it looks solid.

Location location location

More about build quality these days if you know what you are looking at. The North Shore is difficult now its full of old houses and leakers, you need to move out a little to get a new build.

suggest it might be a good time to buy? or are knifes still falling?

perfect time

What have you bought?

when?

Now, the perfect time.

Yes i agree. now is the perfect time.

So what did you recently buy?

dinner, last night? probably the last thing i bought.

Oh, you were just spruiking. Maybe next time you could say:

"Hey I'm a spruiker spruiking, now is the perfect time for YOU to buy a house".

It must be hard keeping track of all your persona's TTP.

i bought in March - townhouse in Grey Lynn

Not sure about knives but auction hammers are falling...

By the wayside?

Try catching it and if we don't hear from you for a while, we'll have the answer

And although the median selling price increased by 1.9% in October, the REINZ's House Price Index, which adjusts for differences in the mix of properties sold each month and is considered the more reliable indicator of house price movements, increased by just 0.5% for the month suggesting price movements, while positive, remain fairly subdued.

The bottom has been reached, look out for summer and early 2025 where the progress will continue.

“The best lack all conviction, while the worst are full of passionate intensity”

The spring rush is flat, very flat under financial and economic reality.

It's performing a hell of alot better than what commentators here lead people to believe it would...

Auckland up 3% and NZ 1.5% in the past 3 months, Spring has sprung

Interesting that you wouldn't choose the 1 month figure or yearly figure 🤔

Is it a new trend, or just the usual seasonal bounce?

Place your bets now, and be sure to borrow most of the money to do so.

Rookie must have borrowed big to buy, it's the perfect time.

Agnostium makes big assumptions.

what do you consider borrowing big?

Oh, don't worry, I was just calling you out as talking shit. Telling other people now was the perfect time to buy but not putting your money where your mouth is. You can ignore me, it's for other people who come here. People calling gout spruikers helped me when I first joined the site.

Gout spruiking would be very niche…😂

Anyone with swollen toes now won't regret it in 10 years time. The best time to eat offal and drink red wine in excess was yesterday!

So who's the one talking shit if you not even wanting to have a conversation about it?

If 0.5% p.m. is flat my missus has DDs

This appears to be the best of it. Being a buyers market, there's certainly no need to panic. No need to rush out and buy before it's too late.

It's all very top heavy. I think it's reasonable that the still bloating inventory needs to be cleared first before a sustainable floor can be called.

, there's certainly no need to panic. No need to rush out and buy

Unless you're on the North Shore. Or Hastings. Or Queenstown. Or Southland...

Advice from the emotionally driven....

He's is basing that of recent statistics, seems like a logical way to make decisions.

"He's is basing that of recent statistics, seems like a logical way to make decisions."

There are many "statistics" used to make decisions. People can choose which have a higher relevance for their purposes. For many people in the property industry, the question might be which statistic or set of statistics has a higher probability on the future direction on future house prices? Some common statistics / data points that people have chosen to look at and prioritise over other statistics:

1) Historical house price change - 1 month, 3 month, 6 months, 10 year, 20 year, 50 year, etc

2) housing inventory

3) population changes - 1 month, 3 month, 6 months, etc

4) affordability

5) underlying housing shortage

6) construction costs

7) other

People are prioritising different "statistics" to arrive at their future house price growth expectations.

Some others may however have a unrecognised and undisclosed bias due to their situation, & select the statistic that supports their bias ("confirmation bias")

Some others may have an undisclosed financial vested self interest. CAVEAT EMPTOR.

The costs of property ownership are increasing before our very eyes. It's not just the cost of any Debt (which if anything has Bottomed, mortgage rates have?) and Council rates. eg: Last year, our Home & Contents insurance rose by 14.6%. Today's invoice for the coming year increases that by another 17.4%.

For every Buyer, there is a Seller. And no matter what the price of the transaction; be that willing participants or mortgagee sale, the price is Current Market Price. There is no 'lower than...." or higher than....." Market Price. Just Market Price. And only one Party will be 'right' in the light of future resale prices. But there is one big difference between the Buyer and the Seller of any deal - that being Future Risk. The Seller has been subject to Past Risk, now a known amount, and that ceased upon Sale. But Buyer is subject to Future Risk - an unknown amount.

And as one opinion suggests, that Risk has not been higher for generations:

"We're not going to be "saved" by interest rates going (lower): higher for longer is the future, as bond yield / interest rates cycles are multi-decade affairs. Zero interest rate policy (ZIRP) was delightful in the moment but the full consequences of that stupendous error have yet to play out."

https://www.oftwominds.com/blognov24/advice-for-leaders11-24.html

Just wait for more and more climate models to cause insurance rates to skyrocket further, thus nullifying any 'average' increase in certain areas. Who cares if the price across town is up if you have to pay 40% higher insurance costs over again in 4 years time? One would be asking for a significant discount on the sale price to counter this for it to be financially viable for many.

Quarterly figures now showing the true picture.

Auckland up 3%, annualized= 12%

On a fairly standard Akl portfolio value of say 5mill that is a wealth increase of 600k.

Rates and insurance pale in comparison.

Excellent news, almost had to fly economy a few times this year!

🥂

I recommend you diversify to other areas - Hastings' monthly is 60% annualised. Get in quick!

This post is brought to you by one of Yvil's sock puppets

I bought a new TV last month for $2.5k, so my annualised spend on TVs is $30k!

Yep! If you brought a TV every month.

You may have missed the sarcasm and facepalm in his post.

"This post is brought to you by one of Yvil's sock puppets"

How many other "sock puppets" do I have and who are they ? Are you one of them?

Oh dear, Yvils gone the way of Biden, he's forgotten where he put his socks. :)

Yves chooses deflection over denial. I wonder why...

True, I didn't say that Time Lord or Côte d'Azur weren't some of my many accounts. Which others, I forgot ?

Your Soundcloud account is the most entertaining

What's Soundcloud?

Edit: I've just Googled it, it's a music app. I use Spotify. BTW if you guys are bored figuring out how many accounts I have, I highly recommend the movie "The Playlist". It's a documentary of how Spotify became to be. It's on Netflix.

Your memory is fading a bit. Here it is Yves Soundcloud

Is that what you think Yvil would look like?

😂, hey, he's a good looking guy, 🤣. The tune is a bit crap though.

Can I put being an Yvil sock puppet under work experience in my CV?

A truly outstanding reference there !

Or you could annualise the monthly figure 2.4%. Or annualise the annual figure, -3%

to be more accurate its +2.4% over 3 months which is + 9.6%

or -10.8% for the next year if your chosen narrative is based on the monthly Auckland figure of -0.9% (in one of the peak selling times) and extrapolate that to -10.8% for the year. Certainly a disappointing result for Oct

Its a bbq story at best. That 600k is sitting in your wank account, you likely wank on about it at the BBQ.

Auckland up 3%, annualized= 12%

On a fairly standard Akl portfolio value of say 5mill that is a wealth increase of 600k.

Why waste your time in residential property?

A share price of a listed company was +92.75% in just one day. For an investment of only $1, this becomes $1 billion in 32 trading days (just in time for this New Years Eve). FYI, the annualized rate is a number that 10 to the power of 71.

'Auckland up 3%, annualized= 12%'

I think the table shows that Auckland is down 3% over the past year, not 12% up as you've presumed.

So on a fairly standard 5 mil portfolio that's a loss of $150,000. Not accounting for rental income.

Just for comparison, imagine if you had 5 mil sitting in something as simple as Term Deposits over the past year earning roughly 5% interest after tax (say, just over 6% pre-tax). That's a gain of about 250k after tax, so you'd be better off by 400k (not accounting for rental income received ) if that 5 mil was in various term deposits. Of course real estate in Auckland could go up from here and beat the TD in 2025 and beyond (especially considering the added rental income from Auckland RE investment).

I mean it really isn't that bad. Volumes around 2016/2017 levels. Trump trade will subdue things for a while and then we'll all get used to the idea.

Check how much stock was available on the market in 2016 and 17

2016, when there were half a million less people living in the country.

This morning, Commonwealth Bank (ASB) forecasted Trump's tariff plan would keep global inflation and interest rates high. It had already sent the sharemarket soaring and the bonds market falling.. So winter might have sprung back into action.

It will be "sell now" instead of "buy now", FONS..

"FONS"

What does that acronym / abbreviation that stand for?

http://m.acronymsandslang.com/FONS-meaning.html

Fear Of Not Selling

FORNS

FORNS?

Fear of really not selling?

Friend of Nigel Slattery

FORF

FORF?

Fear of ....?

Fear of renting forever.

The people are out looking at the Open Homes in Christchurch and homes are selling well.

I do believe that many are waiting for the next .5% drop in interest rates before they buy and there will be many doing this in ChCh.

Auckland market is going to be flat for quite awhile and only increased due to overseas immigration.

I do know that there are heaps of people who have lived in Auckland all their lives now coming down south and are telling us that Auckland has gone downhill and are pleased they have moved south for several reasons.

I might consider ChCh if there weren’t so many rednecks and narrow minded people

Rednecks? Too much sun in ChCh?

narrow minded, but better quality of life.

Defiantly a disproportionate number of nutters down there, its something about the hot Canterbury plains winds that feel like opening a blast furnace on a Mad Max set.

Too many people with shaved head and black jeans

If you are talking about Skinheads Chairman, then you obviously havent been to ChCh for a very long time?

There are far more problems in Auckland than ChCh, I havent seen any for a decade!

"Definitely" Zwifter, not "defiantly".

Well spell check cannot pick that one up. If you can work out wot its supposed to be its close enuf.

It's weird how some people regard personal decorum and public standards as "narrow minded."

I called this bottom a few months ago. It was rubbished by a few people.

I won’t claim it yet though. There’s a chance it’s another dead cat bounce.

Need to define a point at which the bottom is in can be confirmed. HPI up by 2% from the bottom, and sustain that for 3 months?

That seems fair

A few people ? LOL it got rubbished by the 20+ DGM's on this site. It would appear the bottom has already gone. The big unknown now is not interest rate drops in November but what Trump is going to try and pull out of the bag in January. Lets be real here, all the stars never align there is always some reason DGM's don't want to buy now.

IT Guy provided a brutal view on my call 😂

I'm pretty sure I recall IT Guy backing a -10% in house prices from Dec 2023 to Dec 2024.

I thought it was a far fetched call, seems the Rookie was right in that instance.

Probably not going to get my 3 to 4% gains either for Tauranga, will have to wait for reliable figures released in 2025. Could still be close enough not to worry about it, most people will settle for no losses in 2024. Big potential changes still on the horizon this month on the 27th.

IT Guy wrote it ( -10%) every day for over a month up until only a few weeks ago. It was getting kind of tedious.

Until he realized he was WAY off the mark.

I called Aug 2023 the bottom with a long flat there afterwards. Assuming aug 2024 was the bottom , i was off by 0.4%. RP and IT guy had a great laugh at my failure. I wish i was out by only 0.4% all the time. Id be a very rich man.

You did and you back up your opinions with reasons, appreciate your commentary.

The excitement a few have had with the narrative shift post Trumps W that his policies will keep rates high has been interesting…the very same commentators who all said bank economists had no bloody clue when the economist's were talking about slashing rates recently are now quoting these same bank economists if they are talking about rate increases…I love how they swing so fast when it starts to fit their preferred narrative 😂😂

It’s quite funny. Wait until the disappointment sets in when Trump’s Tarif policies doesn’t end up being as aggressive he makes it out to be, and the 10-year bond yield to start dipping again. People on here already calling this the bottom for interest rates, we’ll see about that.

yeah i went on record saying July was bottom. nothing has happened yet to prove me wrong.

My view: We're back to a 'normal' market.

i.e. No big gains over the next 10 years. But also no big losses over the next 10 years.

But let's be clear - that's from an owner occupier perspective !!!

From an yield investor's perspective? Still not great.

From an property developer investor's perspective? Still not great.

From an untaxed capital gains investor's perspective? Buy shares, keep the money in the bank, help out your kids, donate to charities. And no. I'm not joking.

What you've described is the most "boring" outcome and therefore the most likely to actually happen!

This is a key point. We argue all day and it totally depends on our own perspective. The REINZ report was actually kind of 'fair to middling' for a owner occupier looking to feel good about their house. Suggestive that the big falls are done. But if you are a buy to rent investor then yeah, pretty goddam rubbish to see all that stock coming on.

"From an yield investor's perspective? Still not great."

This property in the existing dwelling market was purchased in the last couple of weeks by a non owner occupier and listed for rent. A first home buyer on a single income was outbid by the non owner occupier buyer.

https://www.realestate.co.nz/property/21-dampier-avenue-awapuni-palmers…

21 Dampier Ave, Awapuni, Palmerston North. Listed for rent at a 6.7% gross rental yield.

https://www.trademe.co.nz/property/residential-property-to-rent/auction…

This is the potential unintended consequences of the reintroduction of interest deductibility. Would the non owner occupier buyer have bought if there was zero interest deductibility that would have been phased in under the previous policy?

Now for rent - with no improvements I could see - for $620/wk.

"Would the non owner occupier buyer have bought if there was zero interest deductibility that would have been phased in under the previous policy?"

I doubt it.

There was a-lot of first-home buyer foot traffic in New Plymouth over the weekend, notably in the rain! Agents reporting other ends of the market a lot softer.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.