Auction activity continues to crawl along the bottom, with almost no difference in the levels of activity over the last two weeks.

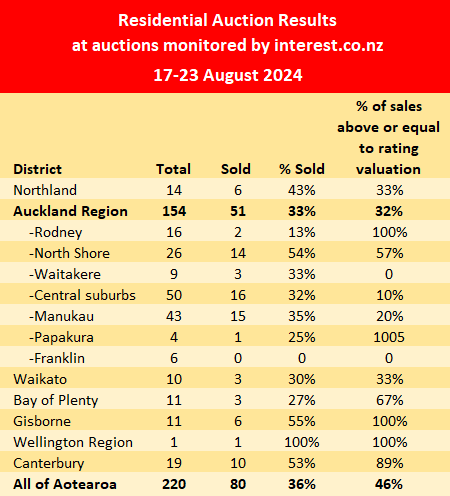

At the latest residential property auctions monitored by interest.co.nz (17-23 August), 220 residential properties went under the hammer, almost unchanged from 222 the previous week.

Of the 220 properties on offer, 80 sold under the hammer, also almost unchanged from the 81 that sold under the hammer the previous week.

That gave an overall sales result of 36%, which has been unchanged for the last three weeks.

The latest results suggest auction activity has found its winter floor and we should not expect activity to decline any further.

And now there are blossoms on the trees, the days are stretching out a bit and we are seeing more sunshine. That means activity should start to pick up a bit with the spring lift, although how big that lift will be this year is still too early to tell.

However, the next couple of weeks should give a reasonable idea of how this year's spring selling season is shaping up.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of the properties that sold, are available on our Residential Auction Results page.

- The comment stream on this article is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

110 Comments

It feels like over a year ago that I asked the following question: ‘Are there any reasons anyone can think of as to why property prices may shoot up again in the next few years?’

One of the few answers involved rising immigration rates to inflate demand.

Today it feels as though that last card has been played, given rising unemployment rates and less demand for cheap labour from struggling businesses.

So I ask the question again in the search for some objective answer;

Are there any reasons anyone can think of as to why property prices may shoot up again in the next few years?’

All views welcome, I’m not interested in shooting anyone down because of some spruiker vs dgm tribalism mentality thing.

House prices are unlikely to 'shoot up' off the back of lower mortgage rates alone, especially if potential buyers are uncertain about the economy and, more importantly, their ability to take on and service a massive mortgage for the next 2-3 decades.

My concern is that our economy has no legs to stand on. We've witnessed a huge outflow of skilled Kiwis, imported hundreds of thousands of low skilled workers and our infrastructure is as stretched for capacity as ever. I doubt milk and meat prices alone can pull the entire NZ economy back on its feet.

No they shoot horses not property

the pent up supply has to be purchased, instead it’s growing due to very low volumes of sales, summer will be telling

HPI for July showed house prices Shooting DOWN 7.8% in auckland MoM

HPI for July showed house prices Shooting DOWN 7.8% in auckland MoM

No, it did not,

Yes it did, are you saying interest.co.nz are liars?

House prices continued falling in July with the national median price declining 2.2% to $753,000 from $770,000 in June. It was also down by the same amount compared to July last year, according to the Real Estate Institute of New Zealand (REINZ).

However the fall in Auckland was much greater, with Auckland's median price declining $80,000, or 7.8%, to $950,000 in July from $1,030,000 in June.

The biggest monthly drop in Auckland was in its central suburbs, which includes suburbs such as Herne Bay, Ponsonby, Grey Lynn, the CBD, Parnell, St Heliers, Epsom, Remuera, Mt Eden and Mt Albert, where the median price declined by $182,000 between June and July, dropping from $1,250,000 in June to $1,068,000 in July (-14.6%).

That suggests the biggest falls in prices have been at the top end of the market.

Its like the difference between popcorn and corn, they aren't the same thing

Has the login "Flying high" just been disabled / deactivated?

interesting you cannot click through

So you are not able to differentiate between HPI and a raw unadjusted median price?

I like my data raw, so after they a d j u s t e d the data, how much did Auckland prices go up?

Just another empty can..

Your statement that HPI went down 7.8% in auckland in July is clearly incorrect. The median sale price did.

Do better.

HPI went down 1.6% in July over June in Auckland. (I just checked the data, page 8 on the REINZ report)

ITG "HPI for July showed house prices Shooting DOWN 7.8% in auckland MoM"

No it didn't, it went down 1.6%

Wait and see. While 2nd Hand house prices are sliding, are the Brand NEW prices also lower to stay... if and its a big IF the land component of a house and land package drops thats good

Agreed, I cannot see how it could be possible for prices to shoot off again (the next few years anyway.)

This housing bubble which has fuelled our economy for a long time is expected by many to have a ‘soft landing.’ Personally I think that’s wishful thinking. I think any correction will be ugly as sin, and play out over years, not months.

70% of bank lending …. Doesn’t leave much for productive businesses does it ?

for houses to shoot up Bank lending has to shoot up, I do not see that happening

I don't think prices will shoot off any time soon, but will likely to stabilize by February, and then flat for a couple of years. By around 2029, with increase in wages and probably lower interest rates, houses will seem to be more affordable, and prices could then take off again.

On the skilled kiwi outflow, I sometimes wonder how many of them obtained nz passports in the last 5-10 years. Is that sort of data available?

None of the young kiwis who left my company to emigrate to Europe, US and Canada were immigrants, they were all born here kiwis.

"None of the young kiwis who left my company to emigrate to Europe, US and Canada were immigrants, they were all born here kiwis. "

Are they off on their OE's?

A relative went on their OE to Canada. About to return to NZ.

Comes down to fundamentals, so NO, can't think of any..

What about emotion? Collectively we NZers are still stubbornly convinced that capital gains on the back of housing is the road to riches. This has to turn around for a real correction to occur… a sort of capitulation in the minds of the masses

When job security is weak, it trumps any other emotions..

When the word going around revolves around RISING unemployment, people are insecure

True that. It appears to be occurring now. Fear is in the air

When job security is weak, it trumps any other emotions

Agreed. Besides stating the obvious where easy cheap credit controlled the minds of the greedy, one only has to look at what happens to markets post FOMO fueled by the collective mentality that using as much credit as one can get ones hands to speculate will quickly reap wealth and respect. It deflates in all manner of ways, but it inevitably deflates and takes the precious equity speculators need for further purchases along with it. Look at what's happening in China. This RE market and it's paper rich participants once powered the world, now in reverse, we are only now starting to feel it's chill.

https://www.youtube.com/watch?v=jNRtOEujfQc

It is going to depend in the area of NZ.

Auckland will be flat for awhile as the returns and costs for investors just do not equate favourably.

This in turn will make a shortage of rental property.

There are other areas in NZ where prices will rise with the interest rate reductions and where people see value.

Latest data from reinz shows Auckland is dropping though, not flattening. If you believe it’ll flatten off due to interest rates, some may argue that they need to be much, much lower.

Yes, it’s been “flattening” for years now, and continues to “flatten”

Love the cute soft language, the big bad C word seems to be the equivalent of uttering Voldemort for some.

It's 100% crashing. I don't see how rents are going to go up when we have more housing coming online and less people coming into the country.

This in turn will make a shortage of rental property.

It's usually the opposite of this. Vendors, sometimes developers even, that are unable to sell for what they want often decide to rent out their houses while they wait for the 'market to turn'. This creates additional supply of rental houses.

Over the last 2 years there is a pool of people who have ben saving deposits in the anticipation of interest rates falling, now that has started, those people will make their moves. I think it's smart of them.

I have 2 colleagues doing exactly this.

Weather that will be enough to increase house prices, not much.

I think it will take time for an increase in buyers to erode the house stockpile before prices increase

Hopefully that brings construction back to life. I am starting to see several demolition jobs already occurring in my suburbs and the ones around it. Many of planned terraced apartments and townhouses have already been sold off the plan.

In the long run, house prices remaining flat or growing below CPI is the best general outcome

Good point, although hard to say if those deposit savers will outweigh the effect of other factors such as rising unemployment, economic issues and fear.

Also, many buyers will believe perhaps that with prices dropping, they’re better off waiting?

Hi Sam

so I will offer some views, which are clearly minority views around here. I have long been a housing DGM, but I would say at the more mild end of the ‘DGM spectrum’.

firstly, you always need to think of culture and mindset. We are overwhelmingly a culture obsessed with housing. That doesn’t go away overnight, despite a couple of years of a weak housing market. Despite the big falls of the past 2 years, I still hear a lot of denial and bravado about house prices.

secondly, there’s still plenty of money out there, even if a lot of it is tied up in housing equity. There’s still plenty of boomers with lots of equity who will be willing to help out their children. Also, despite what you hear about youth, many of their children (ages 25-40) are doing well, and accumulating plenty of money in their KiwiSaver accounts (which they will use as home deposits)

Interest rates are the major issue right now, but they will lower. Lower prices will eventually start stimulating buying too. Lower prices, the coming of spring, and the emerging view that interest rates will lower markedly in 2025, will - in my view - see the bottom of the market reached, at least in Auckland, by October. I think there could even be an ever so gentle increase in prices over this summer.

The economy is crap and unemployment is rising. Yet it needs to be kept in mind that even if 6% of the working age population are unemployed, 94% are still employed! I think there will be pockets of weakness though, where unemployment disproportionately affects the housing market ie. Wellington. I also think unemployment will disproportionately affect young people (18-25) still well away from house buying age. So not so much impact on the housing market.

I don’t think the market will shoot to the moon again, at least not in the next couple of years. But I think there’s a good chance prices will rise 5-7% between Spring ‘25 and autumn ‘26. From here to Spring ‘25, pretty flat, maybe small increases.

anyway those are just my views

I think you are reasonably on the money. Once the market has proven to be at the bottom, the fear of missing out will return, missing out on the lowest the prices will get, and with interest rates sure to decline rapidly, the ability for people to buy will increase. I have seen several properties sell recently and shortly after turn up on the rental market so investors must be starting to make an appearance as well.

The banks will start getting more desperate too. I was very surprised BNZ’s change in policy on low equity loans was not covered on this website:

https://blog.bnz.co.nz/2024/08/like-another-ocr-cut-or-better-bnz-simpl…

A disappointing move, it may spur some growth on their books, but directly increases their risk profile.

I'm surprised no bank has gone the other way, offering mortgages only to those with at least 40% equity, at slightly better rates, offset by savers getting slightly lower rates, on the basis of lower risk.

You're both overlooking the effects DTIs will have. LVRs used to be the only limit. Now with have both the DTI and LVRs limiting the amount a borrower can borrow. And let's not forget that our mercurial RB can adjust both at a whim (and they will).

Unless it’s 5 or less it’s unlikely to have much impact

An unemployment rate of 6% does not unfortunately equate to an employment rate of 94%. Unemployment is only calculated on those people who do not have work who are actively looking for work - it is not a measure of those not working. https://www.stats.govt.nz/indicators/unemployment-rate . The employment rate (June 2024 quarter) is 68.4%. The 68.4% does not count those who are underutilised (ie want more work). Under utilisation rate is 11.8%.

When the next phase of credit expansion occurs probably. You need people willing and able to take on debt, which is more difficult in a contraction/deleveraging phase of the cycle. Immigration is proving the share number of bodies currently is unable to do it based on all the per-capita data pointing south.

We might come out of this slide okay, or we could have another shock that makes it worse. It’s hard to know.

A couple of things to consider. Firstly we need to earn the interest and loan repayments in the real economy and that one is not on a solid footing right now. Latest prove of that are retail spending numbers and high energy prices, both for electricity and gas, have limited industrial activities. Also we need to consider that the next couple of years the 'boomer' generation will be looking at trading down and we might see a shift in the real estate market towards smaller units and more family housing for sale. The boomer generation might also be looking at spending more on overseas trips and therefore further impacting our already negative current account and leave less for New Zealand GDP grow.

Hi Sam, same answer as I've given many times before. I.e. Zoning for higher densities throughout NZ will facilitate much more overall supply - at many different price points - and with a much more dynamic response - ensuring dwelling prices remain flat in inflation adjusted terms for 20+ years.

(And put another way ... Those factoring the capital gains we've had in the past 20+ years are going to sadly mistaken when that doesn't happen. And put yet another way ... Any resurgence of FOMO will just see FOOP become a reality.)

Is there any way to correlate this data to buyer type? Are these new home buyers or existing home owners transitioning, or investors ?

Intuitively there should always be a base level of activity.

I was looking at barefoot results , lots of just under 1mil sales so cheaper quartile for Auckland is moving the rest not so much

Well having just gone uncon on one yesterday (and got 10k knocked off the signed amount) knowing that 5 other properties were all reliant on this one selling so they could all go uncon, none of them had gone to Auction. In this market I personally wouldn't sell a house by Auction and I would also advertise a price. So really I wouldn't base any facts on what has sold at Auction or not also knowing alot of property sells after the hammer has fallen.

That's what we use REINZ HPI for and it was the largest drop MoM in Auckland's data in REINZ History, no one hides from REINZ data

ITG, you don't seem to understand the difference between average prices, median prices and the HPI. The HPI went down 1.6% in July over June in Auckland. (I just checked the data, page 8 on the REINZ report).

Get your facts right.

Not so sure about that. In the past few weeks, we've still seen people at auctions lose their heads and emotion take over which has resulted in some extremely happy and stunned sellers. Not as many as in 2020/21 but still it happens.

More fool them. As I said I wouldn't go to auction obviously a few others believe that as well. Fine if you want to. But to state the market isn't moving or dead or flat just because one form of selling a house isn't working is not a smart or insightful way of making a judgment on the market. I would have thought that a most intelligent and non judgemental way would be to look at all sales and ways of selling in this market

There is (will be) a major conflict at play....the necessity to expand credit and the risk of doing so.

As noted the gov may (quietly) allow inward migration to continue at significant level but that will not make the banks any less wary nor is it likely to be at such a level as to outstrip supply in the short/medium term. Meanwhile life (and death) continue.

Looks like an 'L' for the foreseeable.

More an \ right now, its capitulation super slippery slide time

Yes it is looking like we have some more falling to do first....and the risks are to the downside, as they say.

But that is the conflict...should the downside continue it is likely they will not go quietly into that night.

Interesting to see the percentage selling above their valuation has increased. 46% of sales.

So (1) 54% have sold below RV, and (2) What does RV mean anyway, except the mathematical distribution of how much your semi-annual Council Rates bill is? (The RV could be $1,000,000 or $1 and the RV will still collect the same amount of rates from you. We could replace RV numbers with letters A, B,C etc, as they do in the UK, but that would take away the security of looking at "My RV" for solace)

I was pointing out that this statistic has been in the 20s and 30s for a while and suddenly, since interest rates have started falling it is in the 40s. Interesting to see what happens from here.

It will be meaningless as the council are about to issue lower CVs, at that point you would expect a higher number to sell above revised CV, its just moving the line.

I do not use it as a metric unless its at extreame levels, I like to use it historically, ie if I am looking at a property that last sold in 2015, I like to consider what the house sold for against its CV at the time and compare to simillar ie did the last buyer overpay or get a bargain, compared with what they want now.

There is a house along from me for sale 1H old villa relocated well done, its nice but most people who want to move to the country want a bit more then 1H and are also afraid of villa maintenance if older... they clearly overpaid relative to CV and are now asking way to much.. relative to current CV.

Its an indicator of worth especially if you subdivide, and then sell bare land, though bare land is reasonably easy to value.

Ignore that column in the table. The numbers are always nonsense.

Eg how do 10% of 16 houses sold sell above RV in Auckland central suburbs?

Interesting to see the percentage selling above their valuation has increased. 46% of sales.

Um, no - not exactly.. Being that the measurement is both above or equal, how many exactly could have sold equal to rating valuation? It could be 45%....

Anyway, these days the smaller pool of qualified buyers have the luxury of choice and those homes that tick the most boxes are more likely to sell and be represented here and therefore skew the mix in a low volume market. In frothy times, these homes would have sold 10, 20-30% above on FOMO alone.

Haven't CVs recently been set at a much lower level in some places?

Something like 16 properties in Auckland sold over CV.

No, the new CVs aren't out yet. They are still in Auckland all peak nonsense values.

Wellington in doldrums. National are going to top it, may as well move the Capital to palmy.

Looking at where our health system is tracking I suspect we have bigger problems starting to surface. Could be theres not even an ambulance to be found at the bottom of the cliff... (strike action)... plenty of deviation in the mix to hinder that positivity and confidence index....lol

https://www.rnz.co.nz/news/national/523686/what-s-gone-wrong-with-new-z….

https://www.rnz.co.nz/news/national/526038/disappointed-and-gutted-ambu…

Bingo!

We have a choice of what to do with all the New Debt that's going to be created to keep our leaky economic boat afloat. Do we plough it into resuscitating property speculation, or use it to fix the mess our neglected healthcare, education, infrastructure etc etc etc. is in.

It's not the Price of Debt that matters, but what we us it for.

I would do roads, bridges (Ashburton etc) ferries, new transport planes for Airforce, another Harbour crossing in AKL. and I would expect all these things to be tolled to return on investment, I would ring fence the lending in a Gov backed vehicle and run it like a PPP but without the partners money. ie an infrastructure fund for NZ - possibly with NZ Super involvement. The Airforce planes could be owned by the fund and leased to them.

Could add more generation into this mix (looks like easy money) perhaps a quick start LNG supplied station, feels profitable.

Aussie spends on infrastructure but its never free to use, tolls everywhere.

Will they do this, probably not they will hand big chunks to their corporate buddies, then go work on their boards once they leave politics...

You will not get this build it for NZ vision from this bunch, Muldoon had that vision as he was a man of the people, but lacked the financial governance required IMHO... after we went broke Labour had to sell stuff off and national continued.

National and ACTs game is to say gov should not be in business, but I disagree.... in a small country they should lead and make the profit of being first, biggest and able to carry risk, they should leverage that scale for the benefit of NZ. we could even build new hospitals that are EQ rated and lease back through this vehicle. I used to like Robert Jones in politics, I see no real vision anymore to do great things for NZ, its not hard we have the credit rating to do this now counter cycle

We 100% do not need more roads. We can't afford to maintain the ones we have.

If the 3rd Harbour crossing is a public transport and walking anc cycling one only then maybe.

Agree in the ferries but they need to be rail enabled.

You obviously haven't driven around SH1 bullie point around lake taupo. Last week drove back from taupo to arrowtown at bullie point was behind a linehauler who had to stop completely dead stop as two on coming line haulers were approaching bullie point as two trucks approaching each other is to dangerous. Now not just thinking of yourself and what you think is good for your little bit of NZ. Those trucks move basic goods around the whole country for the whole country, and when your supposedly SH1 is as bad as ours something needs to be done as no so called first world country has a main road system with 25k corners. You do realise SH1 still has one lane bridges in it.

Where are these pent up deposit savers who have watched prices almost double in a few years, gone without to hoard a few nuts and now salivating at the thought of ten percent discount at best? They should hold fire until 2019 prices and lower. The regions have barely moved so buying in any hurry seems desperate at this point. Everyone will do what their situation dictates so will be interesting to see what the peak selling season brings.

If you can pick up a Devonport Villa for 1.4 m, why would anyone in their right mind pay 1.2m for similar in one of Dunedin’s better suburbs. Would expect a ratio of at least 2 in favour of Devonport.

Agree...theres distortion everywhere and its even infected rents ...some values just dont stack up... FOMO residue everywhere... some folk are likely sitting on unrealistic values in some of the not so sought after NZ locales where employment prospects are low and the supply chain is more complex. Flogging off 'overcooked' wont be easy... Councils are not dragging the chain so much now as all the infrastructure crumbles around them.... costs are rising.... vanity projects are no solution.

That place was not a villa. Even the RE agent called it a cottage. Only your doom spruiker mate called it a villa.

Classic, it's a standalone villa on a 300m section in prime location. Even if you decide to create a new category of housing to try to cover the falls, those cottages were selling for $2.6M at the peak and the one that backs onto it sold several months ago for $1.9M.

Denial is strong.

I suggest you go read the ad, even the RE agent called it a cottage. Why would a RE agent call a villa a cottage? A genuine villa is way more desirable than a cottage. And yet the RE agent didn't call it a villa or a bungalow, but a cottage.. because it is, the aerial photo shows the roofline of a basic cottage with add-ons.

This 94m² home sits on a flat north facing 293m² site. It's a classic original cottage which could be transformed into a home with all the modern needs fulfilled and the exterior of a charming and character turn of the century Devonport home.

I've been in it, I live round the corner. There is nothing different from this villa to the other villas I've been in around Devonport.

I suspect the real estate agent is calling it a cottage because he's nervous, as you appear to be, that $1.3M for a villa in Devonport sets a new baseline, so he's calling it a cottage for copium.

what is the flow like to the back garden , looks horrible I may come to take a look

Dunedin has been distorted IMHO by the larger houses used as student accommodation, since students have been able to lend so many $$$ landlords have rorted them, back in my day we had limited funding so lived in the same hovels for peanuts

If you can pick up a Devonport Villa for 1.4 m

$1.3M

thats ask sale price may well be lower

The writing is on the wall, couldn't be clearer now is the time to buy property, you have until Christmas. Multiple rate cuts coming from September. The FED will start cutting, Orr will just follow as he must be pretty pleased with himself for jumping the gun on the FED.

No yesterday was the time to buy... Zwifter you win the prize for the Spruikiest Spruiker here.

You are wrong, but you will never stop spruiking and like a broken clock, somewhere along the 2026/27 bottom you will be right and at least you will be able to refer, going forward to that lucky seven hundred and thirty second spruiky post you made in July 27 that you called the bottom.

Even dissecting your comment - like if you don't buy by Xmas what happens, do you turn into a pumpkin?

I agree with this

Multiple rate cuts coming from September. The FED will start cutting, Orr will just follow as he must be pretty pleased with himself for jumping the gun on the FED.

but that does not mean that property suddenly becomes cash flow positive on the 1st January 2025, in fact at expected 6.25% 6 month fix at that point - I suggest property is still about 200bps of cuts away.

Zwifter, do you dream of COVID era froth returning? The following scaremongering comment of yours alludes that you do....

by Zwifter | 15th Aug 24, 9:40am

The WHO just upped it to maximum today, its now a global health emergency so I guess its getting serious. Potentially border closures are coming, you would have to think that halting all flights from Africa would be a starter but no doubt we will still f**k it all up again and leave it too late.

Mpox IS NOT the new COVID; https://www.rnz.co.nz/news/what-you-need-to-know/525913/mpox-isn-t-the-…

Its a crappy thing but not respiratory

No window for spec cap gains means you have to learn how to spell YIELD, with a side order of DTI. It's a long way back to were yield returns beats cash in the bank with no risk.

🍿

All the gain is in the land, younger people hate old cold houses now. National will open up land supply, the game has changed and gamed the slower players

Yield? Who cares about Yield! It's all about .... Leverage. Using Debt as THE tool to make yourself rich. Yield? That's for those not smart and brave enough to understand how the New Zealand property market has always worked, and always will. Use the Bank, and let The Tenant and the Taxman pay off your Debts for you. (just getting in ahead of the usual response!)

Err... ringfencing is still a thing, and DTI enforces a much larger deposit for the out of balance rent. Open banking when it arrives will allow the banks to see the specuvestor true debt load from the "spread the true risk" strategy.

So...what tax advantage?

Debt to income in a lot of cases allows investors and speculators to be able to borrow a lot more!

In our case several million so the DTI is going to affect the first home buyer and owner occupiers more.

I point out, that with prices where they are, it makes no logical sense to be buying to rent out, the better investors nowadays are buying and improving property.

Rents are going to be increasing in ChCh without doubt,

"Debt to income in a lot of cases allows investors and speculators to be able to borrow a lot more!

In our case several million so the DTI is going to affect the first home buyer and owner occupiers more.

I point out, that with prices where they are, it makes no logical sense to be buying to rent out, the better investors nowadays are buying and improving property"

Non owner occupier buyers continue to outbid owner occupier buyers in the existing dwelling market.

Policy makers can choose to prioritise owner occupier buyers over non owner occupier buyers in the existing dwelling market by bringing in Singapore's rates of Buyer's additional stamp duty.

Capital gains tax does not address this. Existing non owner occupiers will hold on - look at the impact of brightline test for non owner occupiers.

Home ownership rates in NZ are at multi-decade lows.

Policymakers should incentivise non owner occupier buyers to build new builds or buy new builds and add to existing dwelling supply in NZ. By re-introducing interest deductibility in the existing dwelling market, new builds are now less attractive, and more incentive by non owner occupiers to buy in the existing dwelling market over the new build market (and outbidding owner occupier buyers in the existing dwelling market)

wingman - West Auckland Pooperty

https://www.nzherald.co.nz/nz/sewage-trucked-away-from-hundreds-of-new-…

Miles away from Riverhead, I have my own bore and sewage system.

It's pretty manic out there, subdivision spreading along the Riverhead-Coatesville Highway.

I would go roof rain water not a bore. You cannot have a septic tank system and a bore, not a great idea. A large house has plenty of roof catchment, just put in 2 large tanks and you will never run out of water. Bore water probably good for watering the garden.

"You cannot have a septic tank system and a bore, not a great idea."

Hmmmm...you best contact the thousands then that have( and have safely had for decades) ....placement is the key.

I've had 2 houses previous with a bore and septic.

In all 3 cases, the water comes from 230m underground.

Bore water tastes like shit compared to rain water but that's just me. Most people probably cannot tell the difference. Spent a couple of decades total on rainwater, its about as good as it gets if you keep up the maintenance in the system.

Have to agree with you on this point I have 75k L in tanks I hate the taste of bore, I have spring feed dams, and use that for stock water and the vege garden.

See even across this huge divide we have something on common, soon you will be agreeing with me the bottom is not in yet.

You need to be a practical person living in the country to keep everything running. Good times we even finished building the house to save money when I was 17.

I've had 3 bores, and all have been tested by Analytica. They've all been passed as healthy and quite safe to drink.

The bore water we drink and use here tastes great. Rainwater... I had a place that relied on that. The underground tank leaked, and mud got in.

Birdshit, dead birds, lichen and possums on the roof. You drink it...not me.

If you find a dead possum in your tank its a sign you have pissed of your neighbour. Not interested in testing, I can taste the difference. Like I said its about maintenance, you need two tanks and a submersible pump so you can fully empty one into the other mid winter and clean it out every few years. Likewise the gutters, quite hard work and you don't want trees close to the house. All part of living in the country, enjoyed it no regrets.

Your chance to drive a hard bargain and score a great deal.

But 99% won't. They see doom, I see opportunity.

Still pulling the trigger too early now. The economy is in dire straits currently. So bad Orr had to make the move down otherwise it would need A&E. This is no quick fix. He went too high for too long.

Spring will be here shortly, you're going to see some action.

Walking around I ran into some developers and agents today planning an advertising campaign for a nearby subdivision. When it becomes obvious that the bloodbath is over, it'll be too late.

By the time you've homed in on your target and done your homework, you'll have missed the boat.

The action will be mortgagee auction action.... I can't miss the boat, I own it outright...

I have done Pacific loops in it, about to refit and do another, Wingnut I have been doing this for cycles... when things turned to shit in GFC I jumped on boat and went north, you cannot make money while everything arounds you collapses, but you can pick up the pieces one its safe to come out

I was planning to be heading north next July but got a job offer I could not turn down, still 2026 beckons

I was in an Auckland office building lobby last week waiting for a meeting

A couple of old mates ran into each other - one said "what are you up to these days?"

Other guys says "started an insolvency practice 12 months ago - has been mental ever since"

"I have a tonne of developers trying to liquidate everything they have... whatever they can sell"

"I've got land and rangers to sell if you are after one"

"Never seen it so bad in my 30 years... and there are no signs of it getting better"

So if anyone is after a Ranger they should pick up the phone to an insolvency practice for developers.

You know it's bad when even The Comb has turned into a DGM

Got to agree with you on that one mate, drive a hard bargain and buy before Christmas if you are currently in the housing market.

No change in auctions over 3 weeks and over 100 comments!

No change in the market either, it just keeps falling , did someone in the media say on average 8-9k a month all year?

Houses losing more then people make in a year?

Remember when houses used to increase in value by more then people made that year... tax free. nom nom nom

Auction sales rates always seem to be between about 25% and 35%, boom or bust.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.