The number of new dwellings being completed in Auckland continues at a high level, although it probably peaked late last year.

Although there are still plenty of figures suggesting new dwelling completions in the Auckland region are running at a record high, the likelihood is numbers are already easing back from last year's peaks.

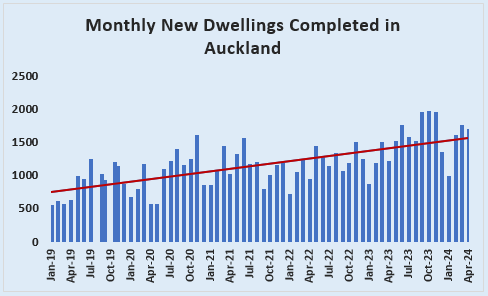

Auckland Council issued 1677 Code Compliance Certificates for new dwellings in April, which took the total issued for the 12 months to April to 19,376. That was the highest number of new dwellings consented in any 12 month period since Auckland Council began collating the figures in their current format in 2013.

The rolling monthly average, over 12 months, was also a record high of 1615 in April.

However, the simple fact is that more than 1900 new dwellings a month were completed in each of September, October and November last year and nothing since has come close to that, with 1583 completed in February this year, 1728 completed in March and 1677 in April. See the chart below for the longer term trend.

Code Compliance Certificates are issued when a building is completed and so are the best indicator of current new housing supply, while building consents are issued prior to building work commencing and so are an indicator of future supply.

While the latest figures suggest dwelling completions in Auckland have come off their peak, they are yet to sink to the lows of around 1200 to 1300 a month suggested by the latest building consent figures.

The current number of dwellings being completed suggests there is still a reasonably strong pipeline of residential construction work in Auckland, but the figures also suggest that it could start to decline quite significantly later this year as current projects are completed and fewer new projects get underway.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

38 Comments

Coinciding with the RBNZ finally realising they've over done it, yet again. Thus the seeds are sown for firm price increases from summer into 2025. 🥂🌴

Recessions bring consolidation and better utilisation of housing. There is likely to be a long lull before demand catches up to supply.

I think that will be regionally specific depending on underlying affordability. Westland and southland sure. I cannot see Auckland moving off its floor until mortgage rates start dropping. That could start in the summer but I wouldn't be surprised if there is little movement before the 25/26 summer.

Are you still predicting we are within 1-2% of this cycle bottom ? Just checking …..

Yes. My Jan 1 prediction was a flat YOY 2024. Currently we are up about 2.3% YOY on the REINZ HPI but I can see that being eroded by years end. Currently, the floor sits at August 2023 and I am less inclined to believe we will reach that (it will require a further 3.9% drop through spring). By summer the FED and OCR will have dropped, new build numbers down, and a number of other factors will solidify the floor.

My prediction is hardly in the realms of spruiker territory. Historical downturns in new zealand have been elongated floors with houses dropping in real value more so than nominal value. I do not see how this one will be different.

Respect others opinions though.

That's fair - I had a similar 1 Jan prediction, though I think it will be wrong.

The play I see is as follows:

Economy tanks, [time passes], GDP falls, [more time passes], CPI drops (supposedly related), [even more time passes], RBNZ starts cutting, [time passes], after several cuts and more time passing, a real floor is found.

What I'm seeing and hearing is that the economy is indeed tanking, and we're waiting for it to show up in the figures. This makes me think we're a long way away from a housing recovery.

Yes I thought + 2~3% this year. But could easily be a fall of at least 3-5%

I want to do a laugh emoji but unfortunately they are not supported here.

An update of NZ house price drops vs US during the GFC. Very similar trend - my personal view is that unless the RBNZ/government bailout the market in the coming near future, we have another round of drops coming over the next 12-24 months.

https://x.com/avidcommentator/status/1803239822208933893?s=46&t=MUwQeKa…

It appears to me that we’ve only now removed the covid froth, without reversing with the 2000 - 2020 market gains above real value (relative to fundamentals/incomes).

I think it is possible that we could see another 15-30% drop in house prices if this recession gets deeper with rising unemployment and contraction in spending/incomes etc. Not a forecast, just a possibility that people should consider if they are thinking about buying an investment property or first home right now - I’d personally wait 6 months and see how bad this recession gets.

A good and very well balanced comment IO.

Another 30% and mortgage rates at say 5.25% , interest deductable, and exceptional sites start to make some sense from a future development perspective.... plenty of crap that's still firmly in the bag holder mode though

Many who have owned rentals long term where shaking their heads in 2014/15

Yes the NZ "Wile E. Coyote" Housing market upto 2021, has well and truly speed far over the cliff, with no support apart from hard, sun baked rocks, 300 feet below.

The Wile E. Coyote feet are air running, fast as hell, and getting no traction.......and bad broken body losses below it, are a dead c.ert.

I see no hope of any positive upwards push upwards in NZ housing, unless the filthy lucre opiates, of below 4.5% mortgage rates, are re-pumped into the NZ housing market/ Debt junkies, collapsed veins.

The market 2021/22 Highs are not to be revisited for 10 years plus, maybe 20.

We will beat the nominal GFC losses of the USA easy. REAL loses will be the biggest NZ has ever seen in our history. The bubble is just so massive- the bust will be eyewatering. You debt Junkies have been warned!!

Keep us regularly updated on your fine chart IO:)

We may even see the catastrophic capital losses of the Japan style crash, that took 20 years+ to bottom.

The Coyote's feet may find dirt again in 2026/2028, but it will be needing to recover from badly compound broken legs first.........and a total; 180 degree sea change, in the unshakable NZ mindset of "You cannot lose on Propeeeerti"

The massive glut of unsold inventory, will be forced into liquidation, at lower and lower prices.

The Real Estate lobby is already screaming for the Government to remove the foreign buyers ban.

Not enough for them that even in a falling market they still make their vampire like commissions as people still buy and sell, they just do so for less, and less frequently.

Just have to look over to Australia to see what Chinese exodus money is doing over there.

Fortunately, it's unlikely even foreign buyers would want to buy in a falling market such as it is, but it would provide a higher price floor for those in the mid-high price brackets - which is where these calls are primarily coming from (and unfortunately are National's primary voter base).

Some of these more desirable properties already buck the trend - note OneRoof's constant cherry picking - "check out this property that sold for over the odds!"

It's only the intervention of NZ First that kept the ban in place it's bound to be renegotiated at some point - once the pain causes more people to feel it - National will bring it back to the table.

Small point but in the cartoons I saw when I was a kid it was Wile E Coyote who suffered all the pain - Roadrunner was fine. Maybe this suggests houses will be carry on unaffected, but those mindlessly chasing them are in for a world of hurt.

Roadrunner is always fine.... Beep beep

Wile E. Coyote (note the dot....) either goes over a cliff, or is blown up, or hit by a train, normally foiled by his own trap for the Road runner

In an effort to catch his prey, the hungry coyote employed such mail-order gadgets as Acme Anvils, Acme Dynamite, Acme Axle Grease, Acme Invisible Paint, Acme Giant Rubber Bands, Acme Rocket Powered Roller Skates, Acme Dehydrated Boulders and an Acme Jet-Propelled Pogo Stick.

The roller skates where cool.....

Right back on point, NZ Housing has now left the safety of the cliff, its pawing at the ground that's not beneath its feet.

No one has the ability to ... prop it up now as its just too big $$$ wise. It will fall as there are no new bag holders and people are nervous and either want or need to get out, yet few can afford property at 7$, 6% or even 5.25% mortgages... there are few buyers, those there are know they are in control.

as Bush said... This sucker is going down.

-10% Dec 23 to Dec 24 I am not going to say guaranteed as that was some one else's moniker, but .... we have 7 months of reports REINZ to get there and even the TAB would pay this one out at half time....

Thanks......hungry, dumb Coyote is back in his rightful place....

GDP up 0.2% as per rbnz prediction - breaking news.

There is a glut of terrible townhouses with no land that nobody wants to live in, let alone buy. Prices are too high. These will rot and people will lose money after being sold a dream that they can purchase a 900sqm section and load 8 homes on it and make a quick buck.

sorry folks, that dream is over

Yep still plenty of completions, which is great news for renters and rental inflation!

What the data doesn’t show is starts - which have fallen off a cliff.

A number of architectural practices , including some big ones, have gotten rid of their residential teams.

Maybe these articles should start with a little karakia for the fletchers head office 😎

great comment

So who can put together a graph showing the existing stock, rate of sale, and these new completed houses coming online.

A plus/negative available housing stock? A plus or minus supply?

Please.

It is interesting that CHRISTCHURCH has been classified as the happiest city in NZ, but then “The Man” has always said it was the best city in NZ to live.

It was ranked well ahead of Wellington and Auckland which we know are not great cities to live in for happiness and affordability.

There are already heaps of North Islanders heading south and this will increase.

Its the regrowth after the degrowth Man. Tell me, how happy was the GARDEN CITY for years and years after the quakes, was the relocated Ellerslie Flower Show happy.

Of course people werent that happy after the quakes for many years.

They still arent due to the mess that Labour made for 6 years.

But ChCh is the best City to live in NZ without doubt, it was before the quakes and is now .

People in ChCh have made a helluva lot of money due to the earthquakes and now have to ride out the current cost of living issues caused by mismanagement of NZ.

Yes I would love to live in a city where you are waiting for the next big one. Hence it’s forever low house prices.

I would suggest the better investment is in shares. You have many good companies paying 5-7 % (many tax free) In addition, the share market usually bottoms about 6 month before the end of a recession and the easing of interest rates.

The dividends may be 5 to 7% but would anyone be putting in hundreds of thousands into a company like they do with housing?

Yes the dividend will be better than the current rent yield on a property but it is also a lot riskier as the company can go belly up.

Good companies with good balance sheets, paying good dividends, don't go belly up. Housing is leveraged more with a mortgage so small % moves can wipe out equity pretty quickly.

better off putting into a mix of funds across a few good players, Milford, Fishers, Jarden etc

And you can also make very good money, buying well and improving and selling.

That is the way to do it now, as buying to rent out just dies not make sense at the moment.

Rents are going to continue to spike!

What you described is a TAXABLE activity, dont shortchange the revenue dept Man

Buying or building rentals without a mortgage works. Over the short term its lower yield than investing in public companies but you dont have the risks and volatility

Yes it is a taxable activity, but most things are and profits are good, if you know what you are doing.

No wouldnt be building anything to fent out whether with a mortgage or not.

That makes absolutely no sense at the current time!

You're saying you can make money house flipping in Chch at the moment for those who know what they are doing

Any examples please?

Yes, ChCh market has been the most stable market in NZ for years.

When they brought in the 10 year Bright Line, many investors changed their business plan.

There are plenty of New Zealanders who had modest incomes who had the nous and guts to put regular amounts into managed funds who are now retired and trying to spend their $5 to $10 m equity portfolios. They have diversified and interesting portfolios that produce huge annual incomes. It pays to be diversified.

Redundancies are about to kick off. Unemployment headed for 5%+.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.