The housing market appears likely to remain firmly in buyers' favour this winter, with more people wanting to sell properties than there are people who are willing and able to buy them.

The huge overhang of unsold properties on the market that has built up over the last nine months is at least as big an influence on the housing market at the moment as the prevailing high interest rates.

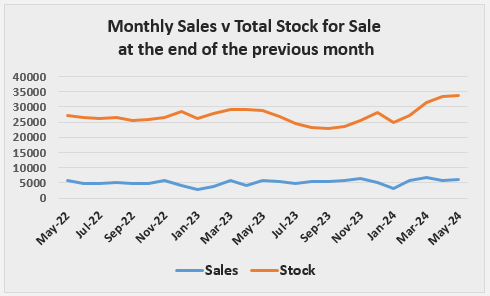

The total number of residential properties available for sale on property website Realestate.co.nz at the end of each month has grown steadily from 22,750 in August last year, to 33,815 in April this year.

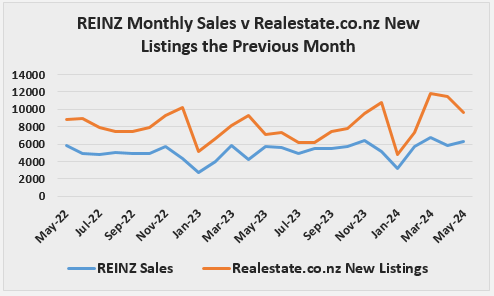

But from all of those properties that were for sale at the end of April, the Real Estate Institute of NZ recorded just 6203 sales in May.

That was one sale for every 5.5 properties on the market.

On top of that, another 9225 new residential listings were received by Realestate.co.nz in May, which meant sales were running at just two thirds of the rate at which properties were coming on to the market.

All of which points to a glut of properties for sale, which, if the normal rules of supply and demand apply, should see prices starting to fall, and the latest figures suggest that they are.

The REINZ's House Price Index, widely regarded as the best measure of residential price movements available, declined by 2.9% over the three months to May, with falls above 5% over the some period in some parts of the country.

This is good news for buyers and for first home buyers in particular, although the latest modest falls in prices are still miles away from restoring anything even vaguely resembling affordability for first home buyers on average incomes.

First home buyers will also likely be cheering recent comments by Housing Minister Chris Bishop, who said he regarded house prices as being too high.

That was an unusual, and perhaps brave, comment for a politician to make, and suggests at least there might not be any political pressure for moves that would prop up property prices in the near future at least.

This should leave market forces to do their thing.

And for the moment, those forces appear to be very much on the side of the buyers.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

119 Comments

It’s doomed

The news just keeps getting better..

Quick Adrian, cut in July, pretty please

I see you have reached the bargaining stage of grief. Next stop depression.

Today’s headline isn’t very original……. 🤷🏼♂️

TTP

Captain Mainwaring

Thought REINZ issued the numbers yesterday saying Auckland Central is +18% YoY ? No?

RNZ claiming prices rose 2.3% last month? Have I missed something?

https://www.rnz.co.nz/news/business/519742/property-market-number-of-ho…

Yes, prices rose 2.3% over the same month a year ago. But many novices are amazed that prices and sales decline, when moving from the peak autumn season towards winter...

The article states incorrectly:

The Real Estate Institute House Price Index for May indicates the value of the housing market rose 2.3 percent last month.

I just had another look at the REINZ property report for May 2024, here are the numbers for the HPI for NZ:

May HPI 3,595

Compared to previous month -1.0%

Last 3 months -2.9%

Compared to same month 1 year ago +2.3%

Last 5 years compound +5.5% pa

So yes, it seems RNZ are incorrect.

Ohhhh there is going to be some 'price discovery' happening over the next 6 months.

Just driving through some less desirable suburbs of the Hutt, you can easily notice scores of townhouses sitting empty with "for sale" signs up for months.

In fact, new housing projects are still breaking ground in leafier suburbs within the region. I counted at least 40 new medium-density houses a week ago being built within a 10-min walking radius of my house, most of which I understand are already pre-sold.

Those holding crappy stock in decent neighbourhoods or decent stock in crappy neighbourhoods should be worried.

The poor old property market can’t catch a break!

December 2019 Realestate.co.nz had around 18,000 listings and in December 2020 Realestate.co.nz had around 13,000 listings. Today it has almost 40,000 listings. You have to go back to December 2015 to get listings just over the 30k mark. Let that sink in for a minute. Data in link. https://www.interest.co.nz/property/108545/asking-prices-remain-buoyant-property-short-supply-across-country-reports?

What this suggests is well over 30k distressed or unavoidable sales. Moving for work, leaving the country, mortgage too expensive, divorce or, my favourite, speculators listing new builds at stupid high prices.

Will we hit 50k for sale when the bright line test changes? That could signal an Ireland style crash that could take 5 years to recover from.

With a bit of luck materials prices will start dropping as unsold products start building up.

its real easy to get timber, ply etc at the moment

Those who have become over-indebted may well need to sell-up on unfavourable terms……

But most house owners will ride out the downswing, awaiting more buoyant trading conditions.

As I always emphasise, the housing market is cyclical - though some here fail to grasp that.

TTP

I agree TTP, but the 5k houses that sell each month set the value for the 1mil odd houses not listed....

I don't have to remind an old Spruiker like you of that fact do I, we all know how valuations work.

We may never see 2.9% 5 year fix ever again, unless we have another pandemic.... that buoyancy is over.

I am still saying -10% Dec 23 to Dec 24, seems a lot more possible this week doesn't it....

"We may never see 2.9% 5 year fix ever again" - we may see it in a year or two once inflation is officially dead, unemployment is up, and the h̶o̶u̶s̶i̶n̶g̶ m̶a̶r̶k̶e̶t̶ economy is stuffed.

It's because the economy was the housing market. A giant ponzi scheme.

Now everyone has to actually work for a living again doing something that adds value. Til we get to that point everyone will be a bit broke

It will be like a dream..

New Zealand doesn’t have an economy it’s all based on how much your house is worth but it’s money tied up.

Been saying this for past dozen years. Finally saw the exact same wording used by one of the top economists/analysts 18 to 20 months ago.

Australians and Uk buy property to live in not necessarily to make a profit.

Once you had the LVR covered saw reports of ratios 9 up to 15 times your income to borrow.

But who do we have to blame for it?

Just out driving doing some errands and an ad on the radio comes on "Now is the time to sell your rental property. Take advantage of the Brightline changes and get your rental property on the market". From Bayleys Real Estate. It made me smile.

Why should someone sell their rental property? I thought the "grown ups" were back in power, everything is fine again?

Ohh of course, yield was never the intent it was always about capital gain. I wonder if intent comes into it. Could be fairly easy to prove intent if one sells immediately after the new brightline period.

https://www.ird.govt.nz/property/buying-and-selling/when-you-need-to-pa…

Selling residential property after the bright-line period ends

The bright-line property rule does not apply if you sell a property outside the applicable bright-line period. But other property sale rules will still apply when you:

- bought the property and you had an intention to sell it

Hi, I’m on the move and only have my iPad and can’t seem to access or download the latest REINZ housing report. Anyone know where I could access the full report. Thanks. I’m not a member of reinz etc. would that stop me from downloading?

Realterms: thank you

Try your local library or pub.

TTP

Get in quick and support my pyramid scheme - you can’t lose [NZ spuikers]

Definitely. Now is THE TIME to buy.

House prices always go up...every 10 years they double and all great stuff like that.

And you can buy loads of them and rent them to poor people coz there isn't enuf houses to house all the poor peeps we import.. it's great.

Disclaimer : except when there is a downturn and then house prices really really bomb and people who bought in the boom lose the shirt of there back.. and even the poor people want to leave.

Remember " You will own nothing and you will be happy" maybe the poor are happy. Without the assets and the associated debt that ties them to a place they are free to leave.

Leave a town, leave a city, leave a country.

TM figures still very elevated - plenty coming onto the market, plenty being withdrawn. There's a big overhang from Summer. A lot of listings were removed at the start of the month, but listing count remains fairly stagnant since then.

Bail out now! It's gunna be Harder for Longer baby 👶

I hope Adrian Orr and the reserve bank haven't been popping the little blue boomer pills. Or it could be "Harder for Long Time".

No happy ending?

He'll give us a stiff briefing at the next announcement

B. Hickey has long run the argument that NZ governments won’t/ don’t tolerate house price declines. I have pretty much been in agreement with this view.

Yet, there will be times when they can’t pull out a magic wand. This seems to be one of them.

Will be interesting to see whether they do try and introduce something to support the market. Yet I have no idea what that could be. Don’t think the country can afford FHB assistance on steroids? (For example)

If sentiment/market psychology turn deeply negative, there will be very little the government will be able to do to turn the market around the short term - just as we’ve had over a decade of governments promising to deliver housing affordability but have been completely unable to deliver on their promises.

Housing is too big and too leveraged to save a fall here, all NACT can do is try to form a plan to help form a base.

They no doubt, as per Chris Bishop, may even try to claim it as a win for affordability.

Its only a crisis for those losing equity not those gaining affordability.

Why should the government "turn it around"?

The explosion in house prices of recent years has been New Zealand's greatest social disaster.

Of course I didn’t say they should. But this seems to have been the approach for decades. Maybe now more people don’t and can’t own a house the political calculation is changing.

They shouldn't turn it around, but they are more worried about what will get them re-elected rather than what they should do.

I have a feeling the magic wand will be allowing overseas buyers back in

You can smell that pressure from here... I am not sure craft old Winnie is going to blink

there would need to be a floor price, was muted 2mil but I prefer 3 mil

I don't think there needs to be a fixed price restriction, but just allow temporary residents to buy a house. Those families coming in on work visas and international students would be able to buy homes. Then tax them like Australia does. Foreign buyers who are not temporarily resident should continue to be shut out.

Fine so long as they have to live in the house for a certain amount of time per year, there is a 100% capital gains tax when they sell and they have to sell once they leave the country.

Better to just add 15% stamp duty to every house sold for over $1.5m regardless of buyer. Gets around the foreign buyer, and because it would apply to kiwis, it doesn’t breach the tax agreements with either Singapore or Australia. The agreements with those countries require their home buyers to be treated the same as kiwis.

Tying the stamp duty to the sale price of $1.5m or more will soon see the dilapidated bits of wood and glass become $1.49m to avoid the stamp duty.

Queenstown would become the largest contributor to stamp duty in NZ. Think of how many cancer drugs or Air Farce Ones could be purchased with that extra revenue /sarc

Applying foreign buyer duty doesnt breach the Australian or Singaporean tax agreements. The Australian foreign buyer tax applies to Kiwis and Singaporeans. If they can do it to us, we can do it to them.

Australia and Singapore both had pre-existing duties in place prior to the tax agreements being signed.

NZ did not. Any new tax that applies exclusive of NZ buyers would breach the agreements.

Hence why the only way around it is to apply the duties to NZ buyers of property over $1.5m as well.

Are falling prices the reason the developers are bailing out?

In a word yes, but mainly because the cost of borrowing is 3 times higher than it was, so they can't afford the carrying costs and still make a profit.

Yes, but also potential buyers have increasingly dropped away over the past 12-18 months due to soaring interest rates.

It’s a double whammy for developers ie. the cost of finance is too high for them to finance their build, and also the cost of finance is too high for prospective buyers to buy.

Most developers need a high level of off the plan pre-sales to proceed.

And absolutely falling house prices massively compounds these things. The perfect storm.

This won’t start to resolve until the OCR is less than 4%.

I have a feeling the ocr isn't going below 4% for a long time. Before 2009 don't think it ever went below 5%

The 2009+ years were the outliers... one could argue they were a failed experiment and we ought to go back to a socially adhesive setting of 5%+ permanently. the economy will adjust in a good way.

Interestingly net migration only went nuts recently too. It used to be approx 30k per year.... and I think out natural increase is negative.

"The 2009+ years were the outliers."

Or were the indicative of the only future (though temporary) option in a world of declining growth?

@gregninness or anyone else - has anyone got a Realestate.co.nz or trademe.co.nz chart that shows total NZ listing levels going back to around 2008 - would be interesting to see how the latest number compares with any point since the GFC

I've got TM going back to 2017 for AKL. This year's peak of ~15,400 in April is about 1k more than the March 2019 prev high. But the noticeable thing is that in 2019, by mid-June it'd fallen to about 12k, whereas this year we're still sitting flatish at ~14800.

Mid-June 2021 (just before things went crazy), for comparison, was about 8k. Sept '21 low of about 6800.

I'd post you a graph if it were easy, but it's just too annoying.

I don't have data either, but noticing the same thing nationwide as commented above; the winter dropoff in listings doesn't seem to have kicked off yet. There seems to be a lot coming to market, as this article suggests. More listings than sales, yet the total listing count dipped slightly - suggests many are pulling out of the market and crossing their fingers for spring.

I track TM as well - although your 2019 figures I don't have. I saw the earlier 15,500 listings in Auckland as a new peak.

What hits me is the number of new builds listed - at 3,500 (up from around 3,000 earlier in the year). The issue with these is that a developer will list 1-2 townhouses when they have 10 to sell. So the 3,500 new builds is at least twice that number. I think around 3% of all Auckland properties are currently listed on trademe.

Fair point about new townhouse listings. Hard to control for though!

"has anyone got a Realestate.co.nz or trademe.co.nz chart that shows total NZ listing levels going back to around 2008 - would be interesting to see how the latest number compares with any point since the GFC"

FYI, current listings for sale are still below peak listings during GFC.

Lower interest rates are the reason we are in this mess

Yes, and a large dose of greed.

Agreed.

And not just low, or lower! The lowest ever in living memory!

Far too much of the green stuff being consumed amongst the members of the RBNZ's MPC during covid. (Come to think about - they need to start again now.)

Minsky Moment incoming

Yes, This is the week that the general market abandons all hope of a recovery from these price levels.

Lets see what happens over the summer ... it could be really brutal.

On a side note some of the building contractors / subbies etc on the North Shore are being stiffed by others who are just packing up and leaving for Aussies, debts remain unpaid and unrecoverable. You will see more and more abandoned sites.

Also the local metal recyclers have a good supply of scaffolding bits and pieces....

unless we see blood on the street, things will just get worse unfortunately.

Quite likely ... But some things to note for those bottom feeders amongst us:

1. The cost to build - like-for-like - sets a floor on how low the cost of a house goes

2. The cost of the land is not so restrained.

3. The cost of land - in desirable areas - seldom moves much.

4. The cost of land - in less desirable areas - can move a lot.

5. Current 'pricing' is set by a very small number of sales when the total stock is considered. (As J.C. says, at the periphery)

6. Like rents - buyers set prices by what they can afford to pay.

7. Buyers will pay more - for exactly the same item - when the cost of borrowing falls.

So - Who thinks the OCR will still be at 5.5% (retail mortgages at 7.0%) in two years?

For many of the reasons you've stated I am going to put my neck on the line and call the floor. For us to go below the HPI in August 2023 we will need to drop a further 2%. I just don't see enough momentum to get there this winter before the better weather and lowering the OCR turn the ship. I'm sure there are many on here who will be delighted to call me out if I'm wrong.

A recovering bottom feeder.

Don’t agree with that although I could see the *potential* for only a further 2-3% drop, then stabilisation - but only assuming the RBNZ surprises and cuts at least 75-100 BPs this year.

I want an ounce, can provide a medical prescription.....

Just had a quick keyword search in Trademe on Auckland properties alone:

"Overseas" 107 listings

"Leaving" 24 listings

"Australia" 5 listings

Quite a few using excess hopium and predicting interest rates falls will arrest the inevitable collapse in short order (like within six months). So some numbers ...

Assuming a borrower can service a mortgage repayment of $3,000 per month and a 25 year mortgage ...

i-rate / max borrowing

7.0% / $424k

6.5% / $444k

6.0% / $466k

5.5% / $488k (Housemouse's 1.5% fall)

5.0% / $513k

If the RBNZ cuts in 0.25% increments ... And banks pass on cuts 'promptly' (lol) ... How long before the slide stops?

Calculator here

Nice work.

And just to be clear - I said a MINIMUM of 1.5%, and even then it’s just some minor support for the market that might help stabilise prices and eventually see very minor increases in prices.

Not likely until mid 2025

The RBNZ's MPC says the 'neutral rate' for the OCR is around 2.75%

So even at 1.5% less i.e. an OCR at 4.0% - that's still restrictive, i.e. contractionary.

Given the economy is tanking at an OCR at 5.5% my guess is we'll see the OCR 1.5% less in short order.

That said ... The soulless, callous, heartless ghouls at the RBNZ likely have their own [insert any derogatory words you like] ideas about how to proceed.

The RBNZ's MPC says the 'neutral rate' for the OCR is around 2.75%

I cannot see their modeling, and even if I could I'm not sure I could understand the math behind it, except at a superficial level. What I do know is that central bankers tend to suppress the price of money. That is something that everyone needs to understand. Therefore, 2.75% is unlikely to 'neutral' in reality.

"What I do know is that central bankers tend to suppress the price of money."

An interesting view. Got any reference links to explain it in more detail? I'd be very interested in reading them.

My immediate counter view is that interest rates have been steadily falling for decades and that started way before central banks were given god-like control over the cost of money. I've put this down to a far better understanding of both risk and the likelihood of recovery.

An accurate view. And Alan Greenspan admits as such. There's a dearth of work on the topic. You can read The Price of Time: The Real Story of Interest by Edward Chancellor if you're interested. Chancellor identifies John Locke as “the first writer to consider at length the potential damage produced by taking interest rates below their natural level.”

as Fitch, SP downgrade us, our currency falls, and our cost of borrowing rises..... so RBNZ needs to cut more to pass on any benefit, and our currency drops further..... now normally this is in sync with other countries... if its not our currency will be hammered even more (but exporters will do OK)

If other countries are also in trouble, well then we are in really really big trouble.....

comment re above - The biggest thing that will stop house prices falling is when investors re enter the market, its time to re read the Robert Jones and Olly Newland books on positive cashflow properties.... When rent after actual outgoings covers the mortgage and there is a margin for risk, people like myself may re enter the market. I last saw these conditions in 2002, hint its a long long long way down to levels that investors will start, and who is not donkey deep already, they will have no equity to add.....

Demographics is important, you would not want to buy dying towns.....

99% of the population are / have been oblivious to this. It’s going to be a rude shock for most.

ITGUY: "as Fitch, SP downgrade us,..."

Your whole spiel relies on this occurring. Or put another way - the doom-loop is premised on fantastical thinking.

Care to explain why you think such a downgrade is likely when the rating agencies themselves are not indicating any such change?

ITGUY: "If other countries are also in trouble, well then we are in really really big trouble....."

Actually, no.

In that case we're all the same boat and no-one is in trouble.

Agreed, Its clear that a at best rapid retrenchment of rates, with DTi overlay, adds very little in the scheme of ponzi expectation.

Interesting case study here...

https://www.trademe.co.nz/a/property/residential/sale/wellington/lower-…

Homes.co valuation at $1.15m.

RV 1.2m

Bought in May 2019 for $928m

Listed at $760k, been on market for 2 months.

this is one where the agent normally says "ignore CV"?

or perhaps "Ignore all previous price indications, our vendor was dreamin!"

Even notwithstanding the price slump, that’s crazy. Eastbourne is lovely. Must be a leaker or on flood prone land?

Grew up in wellington. I'd hate to live in Eastbourne during the winter months or early spring stormy days..

Could be one with recently subdivided (so land now postage stamp) and CV hasn't been adjusted yet?

At risk from flooding or sea level rises?

Terrible shame for the vendors. Nice quiet spot for a WFH'er or retiree.

edit: TM ad says "Capital value (CV) $650,000"?

There are two of them for sale - Its possible that the properties used to be on one title (hence old sale price and $1M+ valuation), but have recently been split into two (with the new title having the $650k CV).

I think you're right.

edit: From the look of it - 39 has been split in two sections. Then two adjoined units, 39a and 39b, have been built on the split off bit. Further, the TM property records show a building consent for work that doesn't appear in the pictures, ergo, the property records probably relate to 39 rather then either 39a or 39b.

further edit: Yup. I found a past listing for 39. https://harcourts.net/nz/office/lower-hutt/listing/lh4483-39-pukatea-st… It shows work that could be part of the building consent. And the sale date records 22 may 2019 which is what the TM records shows for 39b. A total mess. I wonder who is responsible?

Further, further edit: On the plus side TM's page and Homes.co.nz provide a link to get to the property file, and from that I expect it'll all become clear what's going on.

And one last edit: It is indeed an interesting case study. If it's a single owner from when 39 was one large section then their development has probably made them quite a few bob and provided years of entertainment.

Looking at it I believe its linked to the property behind and not the correct one. If you look at 30A and B they have estimates of $760,000 and purchase way back in 2003. Agents not doing there job correct.

I think you're right.

2017 CV says 820,000. That what I'm seeing more and more asking prices in good locations for around 2017 CV. I posted two over the last couple of days in Devonport showing asking prices around 2017 CV. Homes still adding millions to the actual asking price.

AFR: A $10.7 billion windfall from soaring property taxes will pay for more public servants but won’t stop the NSW budget posting bigger-than-expected deficits for nine straight years.

Well, well, well. I had a quick look for how MSM dealt with the REINZ report. Guess what? Crickets!

Maybe I should go on with that expose on the MSM + property?

"I had a quick look for how MSM dealt with the REINZ report. Guess what? Crickets!"

Keep the general public uninformed so that uninforned buyers continue to transact. And avoid panic by the general public. (Note: time constrained buyers and sellers will continue to transact)

Similarly to avoid panics by the public when there is a depositor run on a bank, there is no reporting and only reported well after the fact. Look at how a news report sparked the bank depositor run on Northern Rock.

They have been totally corrupted by their reliance on RE advertising revenue

You can understand that now they are being dicked by google and facebook, they are captive to their provider......

To be fair, CN, journalists are bound in their reporting not to make a situation worse. While that might (would?) apply to bank runs, it escapes me why something as slow moving as houses would fall into this category ... Unless ... The banks would be at risk? I.e. if all mortgages have to be 'marked to market' then the sales at the periphery would drive down the total loan book and capital ratios may no longer be being complied with.

Scary thought, huh?

But don't worry. Our RBNZ says they've stress tested the big banks and they're all just hunky-dory.

edit:

But does the RBNZ have oversight of the secondary market? Sure, it's not that big. But big problems can start at the periphery, and snowball from the edges. Overseas, when the smaller guys fail, the big tuna rally around and either 'rescue' or devour the failee. And in such instances there tends to be a news blackout until a deal is done. In any event, the absence of any MSM reporting looks very odd indeed.

The banks have to report distressed loans in buckets ,like 1 to 90 days behind etc, as long as you keep up to date you are not a problem right......

Oh and they put aside provisions to use during defaults if they cannot clear the debt via sale of security

As at March 204 a near $500m increase in provisions for bad and doubtful debts to $640m.

They may well increase this a bit by the end of the year. Still peanuts to our 380 bil resi lending books...

so its all fine, no need for rate cuts as no one is really hurting.

"as long as you keep up to date you are not a problem right......"

Only part of the equation ...

"...they put aside provisions to use during defaults if they cannot clear the debt via sale of security."

Now you're heading in the right direction.

Think back to the bull-trap period when prices started rising. Remember many of the banks reduced provisions for bad and doubtful debts? Well - now they could be forced to not only reinstate them, but also to make them substantially larger.

Like I said, the absence of any MSM reporting of the REINZ results looks very odd indeed.

Someone on the PI facebook page was spitting tacks that the report had not made it to MSM headlines. RNZ falsley advertising that properties rose in May.

The Real Estate Institute House Price Index for May indicates the value of the housing market rose 2.3 percent last month.

This one made me laugh. You got your bloody interest deductibility back, now act like a "real business", shut up, and pay your creditors.

Is there any positive news for the Investors in New Zealand at all given the Interest rates are going to stay high for much longer. ?

We are are all hoping for the october announcement to be a bit investor friendly. At the moment it really hurts topping up and just feels way to anxious to be in this "investment" journey. Is investment all a bit of a farce in New Zealand ?

At the moment moving to Aus looks a bit of easy exit not that Aus is any better in inflation terms.

Reply: Yeah just borrow small I guess that way it won’t hurt too much. Let us know if your in Ak happy to help you with it

OP: well borrow small doesn’t go very far in a small market. Most people are just average Joe trying to get ahead.

worlds smallest violin

"Most people are just trying not to be the one left holding the bag"

Fixed that for them, as they stand holding the bag.

Would be more meaningful to get a longer time series for the charts and relative to population.

Gorgeous commentary on the Aussie Ponzi (here's the intro):

"Having a family is increasingly becoming a financial luxury for young Australians."

So this is it huh?

We've reached the stage of the Property Ponzi Scheme where the very purpose of life - to procreate - has become so difficult that it is now considered a 'luxury'.

Why is it a luxury?

Because an entire generation benefited from policies which serve only themselves, and are 1) too arrogant and stupid to admit it, and 2) too selfish to sacrifice anything for the future of this country.

Instead, they'd rather steal everything to enrich their own present. It's not an accident, it's all by design.

Central banks print money to prop up endless government expenditure - on consultants hired by governments that produce useless PowerPoint slides, political staffers that send fake emails all day, and fake government programs that are defacto 'jobs for the boys' schemes - they're all one and the same.

https://www.stuff.co.nz/money/350310530/housing-market-drop-wipes-out-f…

"They are among about 2000 first-home buyers whose equity has been erased by falling house prices."

It was valued at $860,000, but they paid $743,000 with a 20% deposit pulled from their savings, KiwiSaver accounts and borrowed from family.

"At the time people were buying similar houses in Lower Hutt for as much as $900,000 in places like Naenae and Taitā."

If instead they had pooled their money into rat poison from Nov 2021:

Lump sum: +14.30%.

Allocating monthly: +124.78%

JC its easy to trade the left hand side of the chart.....

I could find things that returned 1000%...

its the RHS that wants answers

Article by Susan Edmunds. She’s Stuff’s in-house spruiker. Shameless.

I wonder if Tony the comb is going to have more time for tramping and gold coast holidays in 3...2 ..1

Who on earth would pay nearly a million dollars in Naenae? You'll get your money back by the year 2100.

attended pooperty apprentice, or pooperty propellor, or tried to climb the ladder with Mr InTheDunny

who in their right mind would be advertising on the radio here, advising old NZers that the right thing to do to pay off their mortgage is to buy an investment pooperty here...

they will have to have an inhouse financial advisor and I suggest the regulator takes a very close look at that advice

Dude, you yourself made a fortune buying and selling property.

I can't help but feel sorry for the poor souls who bought this place in 2021:

https://www.realestate.co.nz/42578080/residential/sale/40-oxton-road-sa…

It's been on the market for quite some time. I wonder what the highest bid at auction was? Might be kicking themselves now...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.