Activity picked up a bit at the latest auctions after being on the quiet side the previous week.

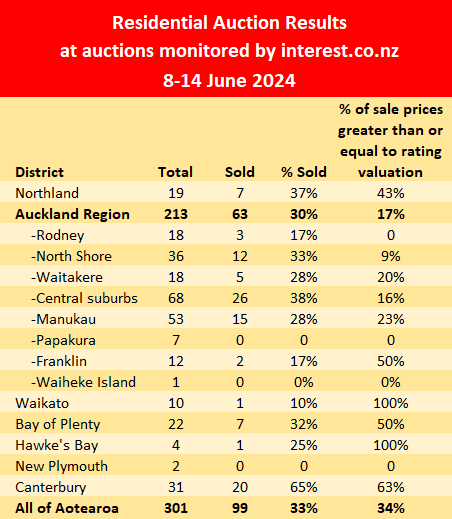

Interest.co.nz monitored the auctions of 301 residential properties over the week of 8-14 June, up from 255 the previous week.

However while more properties were on offer, the sales rate barely moved. With 99 of the auctioned properties selling under the hammer, that gives an overall sales rate of 34% for the week.

The sales rate has remained remarkably consistent at between 30% and 33% for the last seven weeks, suggesting the auction market has found its footing heading into winter.

However, there were signs of price weakness in the Auckland market where just 17% of the properties that sold achieved prices above or equal to their respective rating valuations.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

72 Comments

It is interesting to note that properties for sale have dropped about 10% in my district, quantity selling are increasing as per sold on homes in the district.

G'Day TTP

? Not sure of what you are referring to?

😆🤣

Your news doesn't match their narrative.

Your narrative?

Report the news as you see it. I've often been accused of being a spruiker for simply reporting back on what I have observed.

I answer this in reply to baptist

?

Have you got any BS to report on this weeks auctions, houses that passed in sold for x amount after passing in?

Market data. Whats the issue

Pukekohe and surrounding areas appear to have very poor results on auction day. Very often everything getting passed in with no bids.

My observation has been that houses that get bids mostly sell later by negotiation for more eventually. Not sure what to make of Pukekohe and surrounds as very few bids.

What's your district?

Northland (Whangarei)

Thanks. Only seven sold in northland so it is to be expected to have outlier with such a small sample size.

I have had an exact same mapped area for the last 3 years and it shows sold homes in the last year to date, got to nearly 1200 in peak (22), dropped to about 840 in the ebb about a year ago and now is up to 966. I believe this gives a pretty exact account of what is happening. Correct me if you think this is incorrect.

I see your point. I misunderstood and thought you were referring to the article data. Things are definitely not as bad as a lot of people make out.

Good Canterbury percentages are pulling up the numbers over-all

All the north islanders realizing the lifestyle that is on offer down here wether better value for a house and or not having to spend hours a day in traffic

Vendors getting very realistic.. 👏

How do you conclude that, since sales rates and % sold above CV have not changed for weeks ?

Apart from Canterbury what is the stats indicating? Maybe time to go to spec savers

Answer the question if you can:

How do you conclude that, since sales rates and % sold above CV have not changed for weeks ?

Read my previous response, you definitely need glasses

You didn't respond, you just asked another question, being "what do the stats say".

You did not respond because you can't, and you realise that no change in clearance rate and in % sold above CV, does NOT mean that vendors are becoming more realistic.

Stop your bullshit and read my response

My question is clear and simple, you just can't answer it, because your point is nonsensical. Nothing changing in the data for weeks, does not lead to your conclusion that "vendors are getting more realistic"

Where is the REINZ report?

"When it's this bad they just have to lie"......or delay, delay, delay.

Potential buyers should wait, build stroñg deposits at 6.3% in banks.

Much, much cheaper home prices in late 2024 and even cheaper prices into 2027.

The upcoming -15 to -30% drop, in the soon to arrive, councils new RVs, will really help crystallise the losses in forlorn vendors minds......

Then buyers can demand transactions at a discount to the new much lower CVs.

Good times.

Meanwhile paying upwards of $600per week in rent rather than a mortgage and being settled and secure in your OWN home?

Renting is JUST SOO CHEAP!

Compared to the $1250.00 per week mortgage and next 3 years of major capital losses in this Crashing housing market.

.....just wait for the REINZ report......I'm sure TTP/MyPTS, has had a glimpse, as proberty/legality was never his goodPointis.

If you are buying with a mortgage 2500 per fortnight then you are either not getting correct financial advice or you earn well. By my calculations, that would mean close to 1m borrowing. There are vastly cheaper options.

A 750k mortgage is more than 2500 per fortnight over 30 years

$2254 per fortnight w 2 year fixed rate

Plus rates

Plus insurance

Plus maintenance.

Equals twice the cost to own vs rent.

At the rate Auckland prices are dropping right now sitting and renting is saving you a whole lot of money.

$600 dollars per week is chips compared to the current price reductions in NZ housing. And interest is just paying rent to the Bank. Just face it.The young ones today are smarter than old boomers.

"Meanwhile paying upwards of $600per week in rent rather than a mortgage and being settled and secure in your OWN home?"

That is common and conventional thinking.

Let's quantify the cost of that short term peace of mind that the buyer experiences at the time of puchase.

Is that stability, a place to call their own, peace of mind, emotional need worth paying an extra $722,000?

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT")

The current median house price for Auckland is $995,000

For a buyer who waited, and used the same $260,000 equity used above, the mortgage at this price would be $735,000 (an LVR of 74%)

The Peaker has a mortgage which is higher by $305,000 (mortgage of $1,040,000 for Peaker vs $735,000 for BT)

As a result of that additional borrowing, at a 6.8% mortgage interest rates over 30 years, Peaker is paying $722,000 more over the 30 years than BT.

Assuming same incomes, and same living costs (food, travel, etc except mortgage), BT can save the $722,000 in payments that Peaker is paying.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

Short term emotional and physical needs of Peaker are met, with long term financial consequences that they may be unaware of.

With the recent rapid rise in mortgage interest rates, that owner occupier buyer in 2020 - 2021 may now be unable to meet higher mortgage payments and have to sell their property that is now in negative equity. That might mean that their entire life's savings (and Kiwisaver) might have all been lost, and they might still owe money to the bank. People who have fewer years in their working lives may be unable to ever financially recover, and some may need to apply for social housing.

Look at this person. At the time of purchase they will have been overjoyed at owning their own home, and the mental benefits of that.

Now look at that person after less than 3 years after their purchase. Potential cashflow stress (they don’thave much leftover income for discretionary spending), & mental stress, and the evaporation of this person's life's savings used as a deposit to purchase their home. Would they now have preferred to have rented and waited to buy at a lower price?

https://www.newshub.co.nz/home/money/2024/06/housing-market-drop-wipes-…

FYI, here are examples of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/2012/09/20/your-money/property/ove…

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

People are free to choose to ignore the lessons of history, however people are not free to choose the consequences of their choice.

Well outlined CN:)

You could teach our useless media a few tricks!

The CV doesn't determine the market price.

Agree currently. You need to take -30% off, the 2 and 3 year old RVs/CVs, then you have the likely market price.

The Ratable Value, is a desktop valuation accounting for the average, local area, sale price, at a set point in time.

"Where is the REINZ report?"

They're probably being delayed Gecko, because values CRASHED by 673% and there has not been a single sale

Are you ok?

Excellent Dr Yevil.

So you are furiously Doctoring the REINZ report? -So it's more acceptable and digestible to your REA and Spruiker masters?

Excellent to know, what going on behind the battered and beaten Iron Curtain, of the REINZ.

Please reserve your insightful comments to those that deserve a response, Yvil is definitely not in that category

So why do YOU reply to my comments in another thread above ? 😂

Now I'll be the first to criticise REINZ for putting some egregious positive spin on some shit figures time and time again...

But to be fair to them here - I did email a while back about the timing of releases, and they told me they usually aim to publish it around 10 / 11 working days into the month. Given this month started with King's Birthday Weekend, I've been expecting it on Monday / Tuesday.

Not seeing many if any outright bargains in the auctions. A few sad losses for mortgagee sales of houses that were bought only two or three years ago. Still hard to know if they are bargains. An old house on a cross-lease sold near me for a very good price in the week. Mind you a very good area of Central Auckland. Flawless presentation is key to getting a good price.

Brick & tile units are still good sellers. Nice single level, brick & tile houses with internal entry double garages seem to have no trouble selling.

I visited Hobsonville Point last weekend and was impressed with the developments there. Nice and tidy with autumn colours in the tree lined streets. The community out there are trying very hard to develop a good reputation and it looks like its working. Everyone pays a small sum yearly for public area upkeep. Green waste bags are dropped off regularly for everyone to use. Community groups go on litter patrol.

Nice updates. Whats your intel or simply intuition for market direction medium term. Are market participants waiting for lower OCR

We wont get out of the "doldrums" until interest rates go lower is my feeling.

CPI appears to be crashing, one problem is the pesky rates which shouldnt be counted anyway. Rates are taxes

I assume you have come from a crowded city to like hobby

The main drag did remind me of Coronation Street.

Parts of Hobsonville are going to look ghetto like it the years to come as properties age and aren't maintained...

Absolutely.. hence my remark to ZS... might end up looking like a slum..

"An old house on a cross-lease sold near me for a very good price in the week. Mind you a very good area of Central Auckland."

Find out if the buyer was on the same cross lease. If so, there's your reason for "a very good price".

I'm waiting for that 0% above CV week in Auckland.

Giving it 3 months.

Hmm could be within this winter

Won't happen. The CVs won't include a good quality reno.

FHB's with regrets are now sharing their financial nightmares. This is just the beginning. Many will be finding their own unique situations are too embarrassing to share...

https://www.stuff.co.nz/money/350310530/housing-market-drop-wipes-out-f…

Those who rejected the hype, will be buying in this deepening slump after building a decent interest earning, then interest saving deposit!

There never was any hurry.....

The embedded video with the QV employee in this article shows the positive spin downplaying the magnitude of the declines in house prices in NZ. Do they want to keep potential buyer's uninformed and maintain sufficient confidence to transact?

Most people watching that would continue to remain uninformed about the magnitude of losses in the largest asset class in NZ. Remember the asset class was valued at $1.76 TRILLION at the peak - a 15% fall is $264 billion - more than the entire market value of the stock market in NZ.

https://www.newshub.co.nz/home/money/2024/06/housing-market-drop-wipes-…

There’s still a huge amount of deluded wishful thinking out there

"There’s still a huge amount of deluded wishful thinking out there"

There are huge vested financial self interests at work.

Yes the dark energy, of the selfish vested interest REA crowd, are howling at the moon in pain, as they have lost a grip on the narrative and no longer able to hide the truth of this once in a lifetime, crashing market, that we just needed to have.

Wait till the low IQ media work out the REAL losses many are seeing on the properties and the REAL 30 to 40% losses sustained and actually report as such to the BBQ and water cooler crews......

Once we bottom out somewhere around 2027, NZers stupid habit, since the late 1980s/90s, of ploughing any spare cash into another rental needs a regulatory and financial holding uppercut. It is coming anyway, as insurance, maintenance and rates are rocketing and will soon be 10k + plus per year.

Then as we all know some LVT will be here within 5 years, I have great record on seeing tax changes a few years in advance, this one however is an easy call and a dead cert.

Those who rejected the hype, will be buying in this deepening slump after building a decent interest earning, then interest saving deposit!

This guy might not have realised it then, but being rejected from the bank was actually a blessing in disguise. Being rejected was better than getting approved to overpay for a house and potentially now be in negative equity with significantly higher mortgage payments

https://www.newshub.co.nz/home/money/2021/11/first-home-buyer-not-very-…

Here are some numbers to highlight the situation of the homebuyer in that story

1) At time of purchase Nov 2021:

Price paid: $743,000 (purchased at a 13.6% discount to valuation of $860,000)

20% deposit: $148,600

Mortgage: 80% LVR: $594,400

2) current situation:

Current market value: $560,000

Mortgage: $594,400 (assumed to be interest only for ease of comparison)

Equity value: NEGATIVE $34,400 (123% loss of equity deposit)

Equity deposit and potential life time savings evaporated in less than 3 years

Note that they borrowed from family for the initial deposit to purchase the property, and emptied their KiwiSaver accounts.

Oct 2023 valuations increased 21 percent over October 2020 values in Waikato. CN, this can't be true, is this a typo? I dont want to overpay based on vendors spruiking fake CVs if I buy a property in waikato district council area. Thank you

https://www.nzherald.co.nz/waikato-news/news/average-waikato-district-p…

"I dont want to overpay based on vendors spruiking fake CVs if I buy a property in waikato district council area. "

Do your own due diligence. Caveat emptor.

Might get a quick answer here. Why is TradeMe CV different from the homes.co.nz CV?

"Why is TradeMe CV different from the homes.co.nz CV? "

Interesting.

Don't know. Haven't compared CV between websites. It might be a data upload issue for the website.

Got an example?

Update: discovered the Thames District Council CV numbers are in fact very incorrect. The QV website, in some instances had also an incorrect amount listed. Not sure if this is localised or not.

Original post: TradeMe CV differs from Homes, OneWoof and Real Estate CVS.

https://www.trademe.co.nz/a/property/residential/sale/waikato/thames-co…

I think we're at -58.33332462381% from the 2021 peak. How easy people can manipulate things, in this case house prices. I suggest you all go talk to vendors of houses (not townhouse/apartment) in North Shore, Mission Bay, Queenstown.. and offer them a price after the reduction you've mentioned here and see what they will say. If you get a 5 percent reduction from 2021 peak, you're very lucky.

"I think we're at -58.33332462381% from the 2021 peak"

Is that a fictional number that you just made up and an attempt at sarcasm? Perhaps missing /sarc tag?

There are people have lost all their equity deposit and now in negative equity, and that would be over 100% loss of their equity, some may be forced to sell due to the rapid rise in mortgage interest rates. These people may be in cashflow stress and mental stress. House price bubbles impact real people and there are unintended socioeconomic and financial consequences on society.

In case you haven't connected the dots and how it could impact you or your family:

More social housing, more accommodation supplements, more people on social welfare -> less money for government to spend on health, education, police services, infrastructure, etc

Slower response time if you or your family are in need of police assistance, hospital assistance, fewer resources for public schools impact those families with young children, etc

Most people don't connect the dots and hence unable to see the potential unintended consequences on society and their own lives.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.