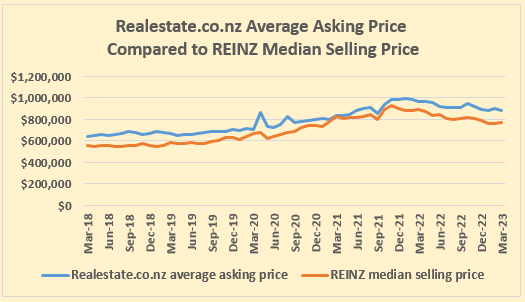

The latest data from the Real Estate Institute of NZ and its sister organisation Realestate.co.nz shows the average difference between asking prices and selling prices is more than $100,000.

In March this year the average asking price for residential properties throughout the country listed for sale on Realestate.co.nz was $883,823, while the REINZ's national median selling price in the same month was $775,000. That's a difference of $108,823 (12%).

Such differences are not unusual.

The difference between asking and selling prices has been above $100,000 in each of the first three months of this year. In percentage terms it has been in double digits since July last year.

According to Realestate.co.nz, the average difference between asking and selling prices has been 5.7% over the last 16 years. Hpwever, a closer look at the figures suggests the difference rises and falls along with market sentiment and there have been significant periods of time when the difference has been in double digits.

Based on the published data from both organisations, the percentage difference between asking and selling prices was continuously in double digits from January 2007 to November 2013, then again from April 2015 to October 2019, and again from July 2022 to March 2023.

The biggest difference between asking and selling prices was 22%, which occurred in January 2017 and then again in April 2020.

The low point was towards the end of the last property boom in March 2021 when the difference was a negligible 1%.

Since then the gap between the price vendors are hoping to receive and the price buyers are prepared to pay has opened up, and has been back in double digit percentages since July last year.

The graph below shows the national monthly trend since March 2018.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

57 Comments

100% success rate at B&T auctions in Auckland this morning.

Yeah, all three houses.

55 Kauri Road, Whenuapai - $1.2m, $215k below CV (15%)

54 Somerset Road, Mt Roskill - $915k, $160k below CV (15%)

2/16 Spargo Road, Massey - $724k, $46 below CV (6%)

Yesterday 1 out of 14 sold, but I guess that wasn't worth a mention.

CV is a crap barometer in both a rising and falling market

For sure I just ask the agent what S/He thinks its worth... they are normally pretty honest...

Alternately you can turn to the highly trusted valuations provided by OneRoof and Homes.

Agents will use the CV in their marketing when it benefits their narrative.

But how many times have I heard them say in the past 3 years that CV has no reflection on the value. Although the CV is supposed to be the market value of the property at the date it is carried out according to QV

100%. And like one roof etc they’ll all fit the narrative to suit. Knowing your target area is the only true way of recognising value in relation to your budget

The CV is what they are using now as a selling point now they they are so " covid*" high .

* - The covid hump/spike is not the result of covid but the Result of the Ardern governments poor economic managment of covid and the retutn of 200,000 " so called kiwis" who put the supply demand mode in an expensive ' up swing" !

Nonsense. Plenty of guys on the waterfront came in and none could afford a house.

It’s local boomers sorry mum and dad investors who gobbled it all up now sit like rats on their sinking ship, wondering why nobody is cashing them out at 2 years ago prices

Nice one Zach - lol!↘️

3 out of 4 at Bayleys auctions in the week. Green shoots!

$100k? It's only $39.5k according to Stuff.

https://www.stuff.co.nz/business/131813174/property-owners-selling-for-…

Ohhhhh. Their article title states "Property owners selling for $39.5k below asking price on average" but the article itself works on median price. Convenient.

The stuff article compares average asking price vs average selling price. Greg's article compares average asking price vs median selling price. Stuffs view might actually be the more realistic of the two.

Stats 101. Look at mean, median, sample size, and variance.

Before you do any of that, ask if the comparison makes sense. This one doesn't. If it was the initial asking price of the houses that sold it would be something useful, an indicator of how much vendors have been forced to lower expectations.

Why are we comparing mean to median? In a heavily skewed distribution (such as house prices) there's almost always going to be a gap.

I guess you could argue the increased gap shows the lower-quartile houses are accepting larger discounts, but this isn't really the appropriate way to present that information.

Picked this up as well. It is misleading.

Another which catches the unwary is the CPI. Do you use the arithmetic mean, logarithmic mean or geometric mean? They use the one which gives the best picture.

Hi Chaos, The reason we compare medians with averages is that Realestate.co.nz only reports average asking prices, not medians, while it's the opposite for REINZ, which only reports medians, not averages. It's not perfect, but it probably gives a reasonable idea of what's happening in the market and at the least will give an idea of the general trend. As for lower quartile prices, I suspect they have held up better than prices at the middle or top end of the market, although I haven't had a close look at this. Our next Home Loan Affordability Report may have some insights on what's happening at the bottom end.

Thanks Greg. Looking forward to it. (And I'll admit, I was so hung up on mean vs median I missed they were different entities ... :P ).

Guess they interchange them when it suits a particular narrative. Many NZers wouldn't know the difference between median and mean. But median for example can be very inaccurate when only a few houses sell. Likewise median can be very inaccurate if only high value houses are selling.

Given that price doubled from2018/17 value 100k drop seems very little.

Yeah but prices have stopped doubling. They haven't stopped falling.

Yip, then there is inflation. Even if prices don’t drop they become 6.9% cheaper annually at current rates.

Same as rents which have been under the rate of inflation for a while.

There is a large gap between

Wasting Everyones time level Asking prices and

Wasting Everyones time level Offers.

Politely the REINZ often refer to this as a difference in the perception of value between the parties.

You seem to be able to drive a bus through the gap at the moment

And driving that bus is about to get more expensive.

"Fuel tax subsidy won't be extended beyond June deadline"

Now. About that CPI figure yesterday and the future direction of mortgage rates....

Your bus has been cancelled due to lack of drivers.

Nothing a 35% rise in wages won't sort out.

"Fuel tax subsidy won't be extended beyond June deadline"

Also the election debates will be good natured and informative.

Sellers now starting to realise the grim reality of an incoming global depression and once in a lifetime asset deflation event.

Bet you’re the life of the party. 🎉🥳

I would rather be at a Party with The Black Swan than The Comb.

The comb would be fun at a party too.

No such thing as a half empty glass they are all 300% full.

Furthermore all beers should be purchased early as his survey says that the beer price doubles every 10 minutes (likely due to the possibly rapidly increasing number of rich and alchoholic new beer drinkers at the pub).

Especially important to note is that on the evenings every one is skint and losing their jobs and the price of hops and transport and wages is falling... is to drink faster and get beer in early because every day the market is going to change tommorow and there probably wont be enough beer to go round so the price will start to double even faster tomorow. be quic

So bring a big wallet (and expect a big hangover..)

I have been to a few events where Tony was the guest presenter, wheeled out to tell us property would only fall 5% from peak at most... blush blush..

Beer and wine are always flowing... and free for the guests.

I would rather party with Cam, he knows the true meaning of the least dirty shirt to goto work with the next day.... if indeed you get home from the Party at all...

It turns out that some Independant Economists are more Independant then others.

I would rather be at a Party with The Black Swan than The Comb.

Yes. BS would be more interesting than the smarmy schtik of TC.

Whenever there is a title with 'House' in it, you know people would come and bicker.

Which is how we'll know when the restructuring of our Property Sector is over. When no one wants to even read about it, and the mere thought of it send a cold shiver down the spine.

And for just one more opinion, from Ray Dalio this week:

- The financial system is close to needing "big restructuring."

- (He) cited higher debt burdens and rising interest rates.

- The economy is on the brink of a contraction that will make the next year or two difficult.

The Nz resi property market will continue with its boom and bust without any real changes- too many powerful vested interests with control of advertising spend in media (4 major brands), control from the top (the Nz initiative) and lack of knowledge or comparable advantages for other asset classes. More of the same to come.

Not connected but a good start would be bringing down the average comms for each property which is obscene compared to other countries

Entitlement mentality and moral corruption is the root of our housing crisis, so that'd need to change first.

This is the point where true smart money makes money... the profit is all in the buying well.

And you cannot beat rock bottom. The best deals here may be farm size blocks on the edge of town that you can run as a farm for tax purposes before the next big immigration boom....

Specarus is in freefall after the wax in his wings of debt have melted. Watch the usual suspects spin spin spin doctor this. Reality is the market is in a tail spin and the owners have passed out from holding their breath for to long.

Will they wake up before they hit the ground...?

That's the kind of comment that makes it hard to believe that you still own 4 properties.

Portfolio mananagement and asset allocation......

I have never seen an asset allocation be 100% cash, most asset allocations are written and targeted at an investor based both age risk profile and wealth.

You could have 100 houes and only have 10% of your total portfolio in property.

Maybe the Averageman is far from avergae, I rate his comments, I do not think this is his / her first rodeo.

Averageman: "the owners have passed out from holding their breath for too long." So you IT, believe this is a comment from a multi property owner? You're kidding yourself, something doesn't add up!

How about "the leveraged have passed out"..?

Belief and speech is free. Why do you keep deflecting the topic to me vs the reality that is obvious to all that can read. Stay on topic pls.

Freefall...

Of course most owners have above average houses, fortunately.

This made me chuckle

(Also as part of this phenomenon: every new build townhouse/apartment is 'Luxury' apparently.

The NZ property market, also known as the Big Rocket market is ready to launch once again. According to Elon Musk it has a 50% chance of making it to Orbit (either it will or it won't).

Unfortunately a valve between the bank and the punters is frozen almost closed, and the ground is coming up to meet us...

It’s always so gloom on here. What about an article on the cpi yesterday and the no doubt top of the interest rate cycle?

The trough is half full for this one

Hi Tony

Not so. Its so reality.

The leveraged are just upset that reality no longer fuels their position and trends towards significant downside. Leverage works in both directions. That it has enjoyed one way traffic for several decades does not mean it's guaranteed to always be so. I would suggest it means the chance of a significant correction is greater than it has ever been.

Leverage is a choice so hold em...or fold em. Before the Bank does.

I posted a couple of weeks ago. RE manager friend I caught up with, 1 - 1.5m ak range, offers coming in 20% under asking.

The end.

reaches higher to 2.5mil same same 20% under

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.