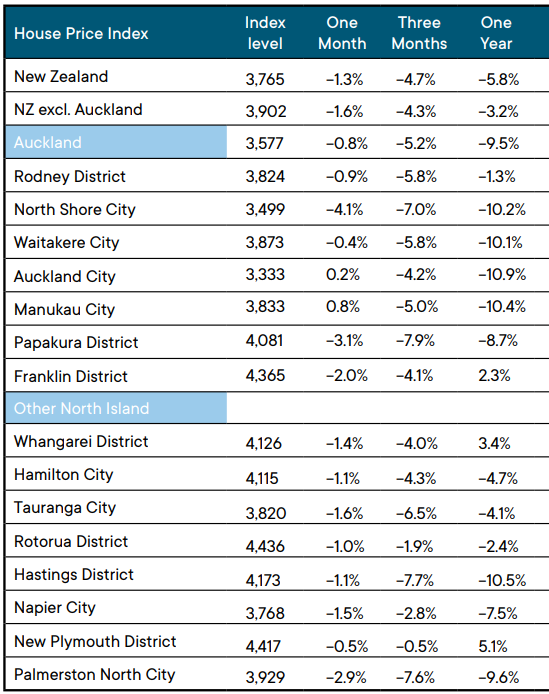

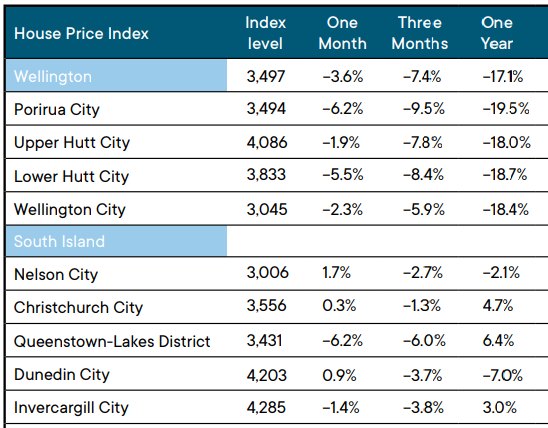

The rate at which house prices are declining slowed in Auckland in August but sped up in Wellington and several provincial centres, according to the Real Estate Institute of NZ's latest House Price Index (HPI) figures.

The HPI adjusts for differences in the mix of properties sold each month so is a more reliable indicator of overall price movements than either median or average prices.

In August the HPI for the whole of New Zealand declined by 1.3% compared to July, but that rate of decline was down slightly from 1.4% in July.

The slowing in the overall rate at which prices are falling was probably mainly driven by the Auckland region, where the HPI declined by 0.8% in August compared to a 2.6% decline in July.

Other main centres to show a similar trend were Christchurch, which recorded a 0.3% rise in the HPI in August following a 2.6% fall in July, and Dunedin where the HPI increased by 0.9% after remaining flat in July.

However in the Wellington region the HPI declined by 3.6% in August after posting a 0.1% rise in July.

Several provincial centres also posted bigger price falls in August than they did in July.

These included Palmerston North where the HPI declined by 2.9% in August compared to a 1.5% decline in July, Queenstown-Lakes where the HPI declined by 6.2% in August after a 1.8% gain in July.

Queenstown-Lakes and Porirua had the biggest price falls in the country in August, bringing a sharp end to the Queenstown district's recent golden run of buoyant prices (see the table below for the full regional figures).

Other centres where the rate at which prices are falling appears to be speeding up are Whangarei, Tauranga, Napier and Invercargill.

The overall movement in the HPI for all districts outside of Auckland was -1.6% in August, compared to -0.6% in July.

The comment stream on this article is now closed.

REINZ House Price Index - August 2022

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

85 Comments

I wouldn’t read too much into single month movements. Last month wellington prices didn’t change much, but Auckland’s did. individual monthly movements for regions can be noisy, but the trend is clearly down across the country.

*edit* here is a breakdown of falls from peak, and the annualised rate of the falls since peak. I think it gives a better picture of what is going on.

Nice work

I wouldn’t read too much into single month movements.

I'm not. I'm also not reading much into the Treasury's claims in Dec 2021 that house prices would rise 10%+ across the board in 2022.

https://www.newshub.co.nz/home/politics/2021/12/treasury-predicts-house…

I was specifically reacting to the opening of the article "The rate at which house prices are declining slowed in Auckland in August but sped up in Wellington and several provincial centres".

I think looking at a single monthly change, in isolation, doesn't provide much useful information. In context, both Auckland and Wellington have been trending down very quickly and its worth looking through the noise of month to month variation and look at the overall trend.

Sure. But I think anyone with a rudimentary grasp of data within a mkt context like NZ housing understands this.

So many who comment don’t unfortunately have that rudimentary grasp

The sharp people at the Treasury should have a good grasp of data. Not necessarily illustrated by their forecasting abilities as it relates to the housing bubble.

correct it's more about the trajectory post the inflection point - and it's pretty clearly pointing downwards (at pace)

"With investors and first-home buyers remaining cautious, now is a good time for house hunters to shop around for their dream home, Waikato real estate experts say."

It could actually be true or could just be biased talk. I wonder which one

Remember, folks, there's a real world of light and opportunity beyond this cyber-microcosm of doom and gloom. 😁

TTP

Anyone who jumps and skip’s into housing market now even with a big smile is going the be in negative equity this time next year, just facts much better to wait maybe end of 2023 the 20% deposit you have could turn into 50% deposit in 12 months now that’s something to smile about 😃

Tread cautiously...... Doom Goblins operating above and below. 🦹♂️

TTP

I can never understand why the majority of people are always doom and gloom.

Must be pretty depressing always hoping for the worst and wishing ill on others.

Strange comment. Owning investment property is sadly now a moral hazard that imparts ill on others.

Those hoping for a correction are hoping for a more fair and stable society.

I don't think that's a fair statement - There are a lot of other issues that have lead to this situation we are in. You can't just blame investors

I blame the cost of construction as a major impact on the cost of housing. The length of time to get resource consents through council and how reliant we have become on overseas materials.

Here's some data from RBNZ C31, 2014 to 2017. There were 2.5x more investors than FHB taking out mortgages over this period.

Total Lending per month

- FHB Average $656m

- Investor Average $1.6b

Total Number Borrowers per month

- FHB Average 1800

- Investor Average 4700

2017 to 2022. It's quite clear that investors have been crowding out FHB.

Total Lending per month

- FHB Average $1.05b

- Investor Average $1.24b

Total Number Borrowers per month

- FHB Average 2276

- Investor Average 3156

Gee you are misguided. You've made the assumption that investors and fhb are simply competing blocks. Yes that is partly true so you are partly right. But to what extent.... ?

Well we won't know the extent unless there's granular data publicly available. But according to RBNZ C31, the average mortgage size certainly since 2016 for Investors is always less than FHB (15 - 30%). Either because they're choosing to put in more of their own money, or....shock horror......LVR requirements.

Maybe you should not compare the two and imply that one groups buying activity affects the other.

Really this is just a symptom of a market that is not working. The housing market not functioning properly leads you to wrongly blame others for the entire failure.

Another reason you should mention for the lack of fhb buying from 2014 was the rbnz forcing them to have much larger cash deposits. That was a big policy change they were not ready for

As someone that was blown out of the water at auctions during 2019 -2020, I can confirm that the buying activities of investors were regularly affecting FHBs...

The price of things people need is decreasing.

Doom and Gloom! (Only from the perspective of the rent-seeking parasite or central banker)

And conversely "always hoping for the best" is a pretty poor investment strategy that is usually seen in gamblers.

Exactly why do people not want affordable housing, and to have most disposable income going towards mortgages. Better to spend money on productive parts of economy and help build businesses. Not sure why some want property prices to increase and the gloom of unaffordable houses. Happy times with house price decrease. Save me a load of money, more for my avocado on toast, maybe I can add some smoked salmon now as well.

You might be able to afford your own house TTP and no longer be a poor renter!

What a blessing for you.

But then again, affordable housing for poor renters like yourself is only something that doom goblins would ever talk about.

#mentalhealthproblems

Goodonya mate .....the world needs more people like you TTP ! Absolutely love your optimism :)

I am truly surprised a man of your standing, expertise and experience in this genre of real estate is renting ???

Is that really you Tim ?

Thanks, great info.

The price fall of nearly 10% in 3 months in Porirua is impressive (and others between 5-10% around the country).

Its a rate of fall that is exceptionally high - even in the context of other property bubbles that have burst around the world over the decades.

FHBs could find themselves in negative equity in the space of months, not years, with these rates of falls.

Be careful out there FHBs - opportunity awaits, but don't lose your fingers in the process.

Are you pinching yourself unable to believe it's actually happening and you are not dreaming haha

You're the one laughing.....not me. If this does come crashing down (to the extent to which it could) - I doubt you will be laughing.

Having lived through a property bubble before, I'm very aware of the financial and emotional distress that can/could follow so no I'm not pinching myself.

I knew people that found the aftermath of the GFC too much to handle (negative equity etc)...so I take no pleasure from what could be ahead of us.

Hence why it is better to avoid creating these circumstances, as opposed to trying to promote them for selfish personal financial gain (like many people on this forum).

.. it's a shame that it took decades for our politicians to wake up to the fact that there's a flip side to massive house price rises ... a huge social disconnect between the haves , and the have nots ...

Meebee we should rename the once beautiful Rotorua as " Have-not City " ...

I have told you before and maybe should repeat it that we are doing very nicely. Possibly lucky but just remember there are wheels within wheels. It is not all a homogenous (not sure if that is the correct term) effect across the board.

You answered my question to say that you were not pinching yourself and that is all you needed to say rathet than make it another righteous rant

Cheers

Sometimes you have to clearly articulate yourself. Laughing about what could be severe financial distress for individuals and the economy as a whole isn't that funny. And your post assuming that I might be taking pleasure in that happening is even worse.

If you find that to be righteous (not taking pleasure in the suffering of others) then so be it.

But glad to know that you're doing great as I'm sure everyone else is happy to hear also.

(Cheers...)

IO Weren't you not long ago saying the smart FHBs didn't buy over the last couple of years? The super intelligent FHBs stayed on the sidelines and now have plenty of buying opportunities.

On that note - Isn't it just dumb FHBs fault if they get in trouble? Same goes for anyone who bought?

Is the context of your argument that it is impossible to have compassion for people who may have made sub-optimal decisions?

Do I feel compassion for friends who got divorced because they married the wrong partner....absolutely.

Do I feel bad for relatives who have experienced business failure because they didn't manage the company well...for sure.

Will I have respect and concern for people who may now find themselves in negative equity and financial hardship because they may have purchased their home at the wrong time (from a purely financial perspective - with no consideration to any other factor to gave rise to that decision to buy a house)......of course I do and will.

So please don't try and twist the argument around from one that was purely financial (i.e. the best time to buy a house) to one where I think that 'people are dumb because they purchsed a house recently'.

Crispy Kawhai purchased recently I understand and yet is probably in the top 1% of earners and is therefore clearly very intelligent. If the house he/she purcahsed falls by 50% in the coming years and they experience severe negative equity, was that an intelligent financial decision? Probably not - but is he/she and intelligent person? Absolutely. And was it a rational decision because he/she wanted security to raise a family after years of waiting for affordable houses and because of his/her exceptionally high income can afford it no matter what happens? Again, absolutely.

So if you can't distinguish between these two different parts of a discussion or argument on this topic, then that is going to be your misunderstanding and not my moral flaw (which I guess is the intent if your post above - to highlight what you see as a moral flaw as opposed to a misunderstanding on your own behalf).

Mate you're the one that was summing up FHB's intelligence based on when they bought or didn't, perhaps you need to reasses how you describe people/groups...especially given how 'compassionate' you are.

Here's a question - have you ever read 'The Intelligent Investor' by Benjamin Graham?

Do you think Benjamin Graham offended everyone who purchased overpriced shares and lost money because they didn't follow his advice? (this appears to be the line of your argument).

He's such a nasty and bad person that Benjamin Graham - because he called his book the Intelligent Investor, he clearly thinks everyone who doesn't follow his investment advice is unintelligent! (yeah right!)

What a joke.

#gettingtrolled

I officially think the world has gone nuts when I read comments like this.

Pray for Crispy

Based upon your pay scale and job (and clearly intelligence) there Crispy I don't think you have any problems, nor do I think you are dumb (despite the line of argument above). People have reasons for buying property that extended beyond just the financial considerations.

But as I said at the time, if you were offended, it wasn't my intention (and I apologise...)

Lol what a kiss a**...

Did Benjamin Graham apologize to everyone who may have been offended by his book?

No apology necessary, thank you. Easily able to save >$100k/year while still making mortgage payments. We'll be fine.

As we burn the testament of the old Church, and turn to the prophecy of 2022, let us pray.

May the boards of your quarters weather any storm. Though prices they fall, may the instrinsic value hold true.

Prophet hear our prayer, though spruikers may spruik, a home is a home.

#pray4crispy

Blessed be thy home

FHB need to be patient. Even after prices eventually stop falling they will remain flat at the bottom for some time as lots of equity will have evaporated, debt and LVR levels will be high and banks will be gun-shy about lending. There won’t be a sudden bounce as many trying to talk the market up say.

Given the reaction in the States today after their CPI figures, can we expect the flow on effects to keep upward pressure on our mortgage rates here? It's looking likely.

Very much so.

Absolutely. It means Fed will raise further than expected yesterday, which means RBNZ will also have to raise further if they wish to protect the currency. Rates are likely to stay higher for longer, therefore more upward pressure on mortgages and further downward pressure on house prices

I'm looking forward to how the weekly RE "market report" emails are going to spin this.

They've already started.

https://www.oneroof.co.nz/news/tony-alexander-blink-and-you-miss-it-the…

Be quick! Don't miss this opportunity! There's plenty of room for upward valuation!

Say what you like about TA, he is an absolute master of spin.

It's what he gets paid to do...

I wonder if His Glibness TTP gets paid by big bro Guy Mordaunt to post his pollyanna propertyganda right here?!

Yes I find the situation really dodgy. There was a guy done for misleading and deceptive behaviour on an anonymous online forum (sharechat) a few years back. He was the CEO of a company and was talking up the company while selling shares. Think the FMA got him.

Here we have (probably Tim Morduant) the CEO of property brokers spruiking the property market on an anonymous forum, while pretending to be a 'poor renter' but then trying to convince everyone that affordable housing is only for doom gloom merchants.

If not misleading and deceptive behaviour that is illegal, its certainly highly unprofessional and unethical.

Crazy stuff.

its certainly highly unprofessional and unethical.

Consistent though, give him that.

I haven't been around long enough to know why everybody thinks TTP is Tim. What was the giveaway?

From memory TTP was using this username on another site which I think gingerninja (possibly?) found out to be Tim Morduant. He also signed off with Tim instead of TTP for quite a while on here.

If you do a quick google search of Tim Property Palmerston North, the first name to pop up is Tim Morduant, CEO Property Brokers.

It didn’t originate with me, let me find links. Hold on.

It didn’t originate with me but someone called “Sam Roma”. I’ve pasted his original comment below but if you click on the YouTube link from my comment back in 2020, there are 37 further comments about it. I genuinely have no clue if true though, only that when I teased TTP about it, he responded back and signed off as Tim (although that appears to have been deleted).

by gingerninja | 8th May 20, 4:35pm

He was outed on a DFA youtube vid in the comments. I don't know any more than that, but I did call TTP Tim the other day and then he replied and signed off as Tim, so he confirmed it surely? It actually makes sense, Tim Mordaunt is based on Palmy North and is heavily into RE.

I thought you may be interested to know that Tim Mordaunt who is the owner of the Property Brokers brand is also TothePoint or also known as TTP. TothePoint or TTP is a very active commentor in the comments section on a website by the name of interest.co.nz. Particularly on the property articles. I was given this information about 3 weeks ago, I then emailed Tim Mordaunt letting him know I had found out who he was. TTP ( Tim Mordaunt ) then immediately stopped all comments on interest.co.nz. 10 days later he tried to test the water by making a nice small comment in response to another person. I emailed Tim Mordaunt ( TTP ) again and asked him to stop or I would let others know who he was. He then immediately went very quiet again for 7 days. On Wednesday he decided to carry on with his comments. The reason this is a big deal is because Tim Mordaunt has Laws, codes of ethics and human decency to abide by. And TTP has broken all of those in numerous ways to sucker in new victims into the property market to keep the Property Ponzi alive. Other people on interest.co.nz do not know who TTP is, they do suspect he is most likely a Real Estate Agent. I wish I could let them know the truth ! Interest.co.nz have got over 3 years worth of comments from TothePoint (TTP) (Tim Mordaunt) on there search engine. Interest.co.nz has kicked off many users who ask fair questions such as " if you are an independent news source as you claim then why do you advertise for Real Estate Companies and Banks ? TTP seems to get very special favour from interest.co.nz and I would not be surprised if TTP ( Tim Mordaunt ) and interest.co.nz have been massaging some of the old comments in the archives . I guess a simple email to Tim Mordaunt asking him if he is TTP would be a good start. The lack of response may be your answer. If this is of interest to you and you do email Tim Mordaunt and he outright denies this then I would love to have this for the records I am keeping.”

I wouldn't even call him that. He's good at having those opinions he's paid to have, but he's not very good at convincing other people they should have them too. He's lost too much credibility.

Trouble is TTP has other account’s on here, sometimes his just talking to himself . You have to laugh at how desperate he is for people to believe him, very insecure person.

Yeah I always wondered who the other three instant likers were

He's a cockroach talking up his own undisclosed book.

He’s a spin master indeed, and a tricky one at that. He has all sorts of variations - the flipper, the top spinner, the googly, he even bowls left handed so throws in a chinaman for good measure.

I'm curious - a significant number of areas within the report use "rolling x months" for the calculated value.

If this is an average over a rolling window (due to low numbers of sales in these areas) - doesn't this mean there's still a significant lag in some of the calculated values?

Admittedly, if there are so few sales in these areas that they need windows as long as up-to 6 months, they probably have negligible bearing on the overall HPI.

Most of the fall happened in last three months as rate hikes set in surprise surprise. if the next nine months keep up this trend we will be well in to a crash, nothing is going to stop huge falls in housing price’s. If anyone is thinking of buying now it would be very prudent to wait as prices are dropping around 7000 a week in some places.

News about the second order derivative of house prices.

Only in New Zealand.

are we in the third derivative when we hear that the rate of increase in the rate of decline is decreasing?

Yes.

Last few month has been a major fall in Auckland and now will face some resistance as FHB still active before further fall.

Houses that will normally expect to sell last year between 1.3 Million to 1.5 Million are going between 1.1 Million to 1.2 Million and houses that were between 1.2 Million to 1.35Million are between million to 1.1 Million, one more wave of fall and will stabilize that is now that are selling between 1.1 million to 1.2 million (from 1.3 to 1.4 Million) should come in mid/high 900s or one million plus and this could be by December/January.

If it falls below that than NZ will replace Ireland in times to come

Given the most recent news overseas on the inflation front, and considering the actions that the Fed will be forced to take, I am now thinking that an OCR peak of 5% is a definite possibility, and the likelihood of a disordered correction to NZ house prices is increasing by the day. I would not be surprised to see a decrease by more than 30% in nominal terms, and well over 40% in real terms by end of next year.

100% fortunr.

NZD dipping below 60c more regularly and economic / employment data out of the US showing resilience - this is the worst news we could have expected. The NZ housing market is going have its pants pulled down to protect the NZD.

If the Fed says jump, the RBNZ are going to ask how high.

Exactly.

We will now see first hand how foolish it is for a tiny economy to play with excessive money printing and stupid low interest rates and thus create a huge asset bubble during the boom times.

Its why reserve banks are typically very boring and conservative and not foolhardy, experimental risk takers.

The all blacks may have lost to the Irish at Rugby, but at Housing market corrections we are really gonna show them up!

"Its why reserve banks are typically very boring and conservative and not foolhardy, experimental risk takers."

I don't believe they are conservative at all. Quite the opposite really.

True today - it wasnt true historically. Banks in general incl reserve banks used to be quite boring. Now they seem to want to create stuff to do to fill their time and experiment with concepts... play with max-employment, try out negative interest rates, etc. be better if they just stuck to the basics of getting OCR to a median of 4-5% and made slight adjustments when needed. IF they do need drastic action like in the pandemic they should bring the OCR back as soon as the economy allowed

The artificial sweeteners that was cheap covid debt, is now becoming poison. The revert to norm is underway, and increasingly being pushed from overseas with runaway global inflation. Those leveraged on anything can expect stress, a lot of stress.

Those leveraged up click here https://pepto-bismol.com/en-us

Yes. All the narratives being turned on their heads. Trump is an expert on being able to optimize the debt game to his own advantage. Bit different when average Joe tries to tap into similar dreams.

The OCR will have to go higher as employers are paying the wage increase above CPI.... need to cause a recession and the eventual hard landing destroys the demand....

Gotta love it. No sense of urgency to bump wages up when accommodation costs explode faster than wages rise, but as soon as they start to rise when it might not be convenient, we have to start strangling demand and putting people out of work.

So down 15% in real terms year on year, I'd say we might be about half way through the real decline. So maybe another 10% nominal drop plus 5% of inflation. That would rebalance the market nicely.

70% is more likely.

How Rotorua 23-year-old Raj Nakura bought his first home - without KiwiSaver

https://www.nzherald.co.nz/rotorua-daily-post/news/how-rotorua-23-year-…

Good on him

Why didn’t anyone explain to him price’s are falling and if he waits awhile the mortgage cost would be a lot less. Sounds like he worked very hard to get deposit if the house price’s drop another 10% over next 4 months (which they probably will) that deposit amount is gone and if price’s keep falling negative equity will be next stage.

It's one of those stories intended to shift blame onto lazy young people, or at least make them feel bad for not trying so hard. Like it's saying there's really nothing wrong with our housing market, or if there is it's not your concern, in the nicest way possible you just need to work a bit harder:)

Tons of them come out every year. March 2021 there was one about a woman who paid a million for her first home, everyone congratulating her but she 'felt sick'. Now she probably knows why.

Au contraire. You clearly missed this memo...

https://www.nzherald.co.nz/rotorua-daily-post/news/rotorua-bucks-house-…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.