If you are a home loan borrower, here is a way to quantify the cost of taking a higher rate now in the hope of a lower one in the future. What does the rate have to fall to in the future to justify taking a higher rate now?

For example, if you choose a floating rate now, at say the 6.89% rate at ANZ (our largest mortgage lender), or ASB, or TSB, you are waiting for future rate cuts because this rate is much higher than some fixed rates.

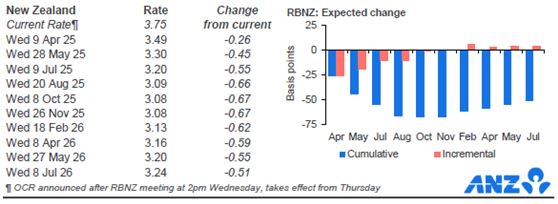

Financial markets seem certain there will be a -25 bps rate cut on April 9 at the next RBNZ OCR review, and another on May 28 at the following RBNZ review. And those expectations are unchanged even though Governor Orr has quit in the face of presumed pressure from a Government that needs lower rate for its "Going for Growth" strategies, and easier capital rules for banks so they can get more borrowers into debt. More debt is expected to generate more economic activity through "more investment" (including the unproductive housing investment).

These financial markets see little chance of the OCR falling any more than two -25 bps cuts, taking it to 3.25% for the rest of 2025 and all the way through half of 2026.

So we have the question. If that is the plannable future, where will the fixed rates need to fall to, to get you to shift and lock in a 'good rate'?

On the table now are carded offers of 4.99%. All the large Aussie banks and some challenger banks offer that for a fixed two year term/contract. That is about -190 bps lower than the floating rates from these same banks.

Borrowers have recently gone very short, indicating many borrowers are adopting this risk-taking, trying to game the interest rate options. Over the last three months of RBNZ data, more than a third of all new loans were taken out on floating rates, and another 28% were on six month fixed rates. That is more than 60% at very short terms, at high rates.

To test how this makes sense, we set up a standardised calculation model, one borrowing $450,000 over a 30 year term, presuming the borrower has a low LVR and good stable incomes that a bank finds attractive.

Here is the math. (It will work for any borrowed amount, and not just the $450,000 example wer have used.)

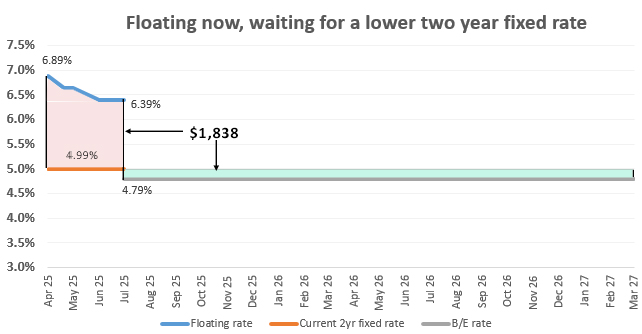

A floating rate of 6.89% now, falling to 6.64% on April 9, and to 6.39% on May 27 (and allowing a ten day 'notice period' before the rates become effective) ...

... for a $450,000 floating rate mortgage you will pay ...

$1613.96 in interest from April 1 to April 19,

$899.83 in interest from April 20 to April 30,

$2535.89 in interest from May 1 to May 31,

$572.08 in interest from June 1 to June 7, and

$1807.20 in interest from June 8 to June 30.

In total that is $7429.90 in interest payments. (We have ignored the principal paydown on payments you make.)

Over that same 91 days on a current 2 year fixed 4.99% rate you will pay $5591.55 in interest.

Over the 91 days at floating you will have paid $1838 more than being at a 4.99% 2 year rate.

So, you need the benefit for accepting that penalty to exceed $1838 ($7429.90 less $5591.55) for the risk of this pay-now-save-later strategy to work out. The gamble has to come off, or you are worse off.

The easiest way to make sense of the number salad is to see it in a chart.

Clearly, to take this risk, you will want the two year fixed rate you are waiting for to be less than 4.79%. How much less you need this to be to make the risk a worthwhile one to take is up to you.

This article just looks at one gaming option, float-now for a two year fixed option later. There are others. And we haven't considered the time value of money. If we did, the break-even target rate would be even lower.

11 Comments

Or wait till a couple of more drops then fix long. Insulate yourself from the economic effects of the Agent Orange rain.

This is where I'm at, a bit early to lock in for any longer than 1 year.

"Or wait till a couple of more drops then fix long"

Averageman, the probable OCR drops won't affect the long end of the mortgage terms. If your intention is to fix long, you may as well do it now and save money right away. It is very likely the longer term mortgages are near their bottom now. On the other hand, the shorter term mortgages will drop a bit more with the next expected OCR cuts, and provide more flexibility in the event of a black swan.

Thanks for a great article which goes to the core of Interest's values.

Hmmm due to come off fixed in a couple of months, might be good timing.

Slightly off topic but I don't know where else to ask. Last mortgage payment in April.

I've heard you need to hire a solicitor to get the bank's interest in the property taken off the title deed. Is that true?

Two optons: have your solicitor discharge the mtge from the title - minimal cost or leave mtge on the title to give flexibility should you wish to reborrow at a future date.

Thank you. So, a couple of hundred for the solicitor?

Thank you. Not much change from $600 then.

"Trying to game the mortgage rate" - as with any gambling, the house is always the winner.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.