The Commerce Commission is likely to push surcharges "right down" but "not to zero" when it releases the draft decision from its consultation on the costs to businesses and consumers of card payments next week.

The consumer watchdog says the draft decision and a reasons paper will be released next Wednesday, December 18, proposing changes to the regulation of interchange fees on Mastercard and Visa card payments.

Commerce Commission Chairman John Small spoke about the issue in a Economic Development, Science and Innovation Select Committee hearing last week.

"So what we're doing in that space is basically pushing those interbank fees right down. The [Retail Payment System] Act when it first came in cut them a fair bit. We are currently consulting, we are about to go out with a draft decision."

"The proposal that we put out was to push those fees down a lot further and to include international cards in that. There are two purposes. One is to make the numbers smaller so that the merchant pays less and so surcharges are lower, and the other one is to simplify, take a lot of the complexity out of it, so that treating like [similar] cards alike so that it's easier for everyone to understand what the merchant's paying," Small said.

"That work is underway so I better not give you the spoiler. But I should say that the reason we're doing that is because then it's possible to push those surcharges right down, and that's what we'd like to do. Not to zero because there needs to be some money in it for innovators. Not to zero, but to something low. It's a balancing act."

Fintechs such as Dosh and Emerge advocate for interchange to remain in place as a source of revenue for their fledgling operations, offering competition to established banks. (See more on interchange below).

An issues paper the Commission released in July estimated merchant service fees amount to about $1 billion a year, with interchange fees comprising about $600 million, or 59%, of these fees paid for Mastercard and Visa card payments, mostly via banks.

Thus the Commission said further interchange fee regulation could reduce fees substantially. Assuming 90% of these savings were passed through to merchants, merchant service fees could fall by more than $250 million annually, it estimated. This estimate is based on 0.2% domestic and 1.15% international interchange fee rates, which are lower than current rates.

In its issues paper the Commission said the average surcharge imposed by merchants was about 2% but the average merchant service fee was about 1%.

"Whilst the cost for accepting contactless debit is lower (0.70% for those on unbundled pricing plans), merchants will have higher costs when their customers pay with a more costly payment method (upwards of 2% for international cards) so they may just pick the higher number," the Commission said in July. (See more detail here).

Quantitative evidence sought

The Commission says feedback on its issues paper, in general, wasn't well supported by quantitative evidence.

"This makes it challenging to weigh up the strength of different trade-offs when making decisions. We particularly welcome quantitative feedback in submissions on this draft decision."

Small told the Select Committee: "There's a payment that runs between two banks in that network, between your bank as a card holder and the merchant's bank. So the merchant's bank pays your bank a fee and it charges the merchant for that fee, and it could be 1% or 2% of the transaction value."

"The merchant has got to pay for that and so then the merchant's go 'well I need to get this back.' So they put a surcharge on. But often they don't really know how much that transaction is costing them and so sometimes they, whether it's lack of knowledge or they just want a bit of a profit margin, that is put on a surcharge."

"So that's the sort of thing that really annoys people. And you can see why. It also promotes that payment form over others...because some of that money comes back to the cardholder in the form of reward points," Small added.

The Commission says $95 billion of card payments in NZ are processed by Mastercard and Visa each year. Meanwhile, the revenue Visa and Mastercard generate in NZ is run through their Singapore operations where very low tax rates are paid on it.

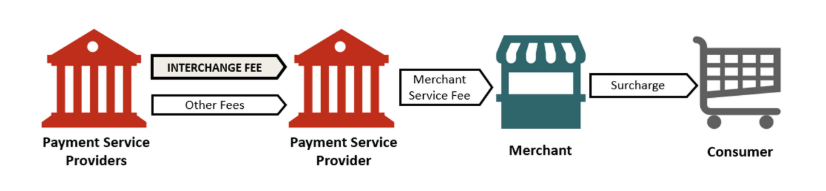

What are interchange fees?

Interchange fees are charged by the financial institution on one side of a payment transaction to the financial institution on the other side of the transaction. A typical card transaction involves four parties the cardholder, the cardholder's financial institution (the issuer), the merchant and the merchant's financial institution (the acquirer). For most card transactions, the interchange fee is paid by the acquirer to the issuer.

Visa and Mastercard point out interchange doesn't generate revenue for them. However it underpins and grows their networks and is the biggest component of merchant service fees paid by merchants to their banks. Interchange can thus drive up costs for merchants and ultimately consumers too, being reflected in retail prices and surcharges, with some also rebated to card holders as rewards.

They're also complicated. Visa and Mastercard have hundreds of interchange fee categories, impacting the cost and transparency of the merchant service fees paid, merchant service fee pricing and the accuracy of merchant surcharging.

Further regulation would mean a financial hit for bank card issuers for whom Visa and Mastercard relationships are lucrative.

*This article was first published in our email for paying subscribers first thing Wednesday morning. See here for more details and how to subscribe.

17 Comments

I guess the comcom was always destined to morph into a price control agency. Muldoonism never really died.

How dare they intervene against an international oligopoly (with huge barriers to entry and almost no competition) for the benefit of New Zealanders. What nanny state pricks. Don't they realise we want to be screwed by big corporations, making completely disproportionate and virtually untaxed profit?

interest.co.nz commentators really will find a way to complain about everything

Feel free to donate an extra 1% to 2% of your monthly spend to your bank if you really want.

A govt trying to stop the abuse of kiwis by the global banking system. Wow.

...But often they don't really know how much that transaction is costing them...

What rot Commissioner Small. You are assuming retailers don't understand their cost base?

Think again!

John Small was clearly referring to consumers, not retailers. Re-read the comment.

Small told the Select Committee: "There's a payment that runs between two banks in that network, between your bank as a card holder and the merchant's bank. So the merchant's bank pays your bank a fee and it charges the merchant for that fee, and it could be 1% or 2% of the transaction value."

"The merchant has got to pay for that and so then the merchant's go 'well I need to get this back.' So they put a surcharge on. But often they don't really know how much that transaction is costing them and so sometimes they, whether it's lack of knowledge or they just want a bit of a profit margin, that is put on a surcharge."

Looks like it's variable based on your bank and merchant bank? I suppose they could have a really long surcharge sticker, 1% BNZ, 2% Westpac, 1.3% ANZ etc...

An investigative journalist did their best to work out exactly where fees were being paid and to whom. It was a 3/4 part series in one of the major news sites. Stuff maybe? Anyways ...

He couldn't. It's a massive black box. And kept that way by overseas financial organisations sucking at the teats of all Kiwis.

If the RBNZ did introduce a digital currency ... We could perhaps bypass this morass of greed and save ourselves a friggin' fortune.

Open banking transactions facilitated phone to phone by QR codes would do the same thing. Without any opportunity for the government to make your access to digital currency conditional on whatever whims and fads they had on a given day.

Less fees sounds good to me. A friend had a debit card from Charles Schwab bank when travelling and the bank would reimburse all ATM fees worldwide making it far cheaper to travel. Would love to see this in NZ and lower fees all round.

I will enjoy my cashback card while it last, looks like their days are numbered

The 3%+ fee feels like the equivalent of increasing GST by the same amount, but with zero benefit to the country.

It's a straight impost to the economy and benefits only the finance industry. Rent seeking at its finest.

Fees any more than half a percent would be a massive failure of the ComCom. Let's get rid of the rewards and instead get banks to offer fair interest rates on transactional account balances.

Getting banks to give up profits? Good luck with that

The thing for me is I have started to be admittedly a little bit petty with these surcharges.

I have started to carry cash. If I see a surcharge over 1%, I pay in cash, because I understand the costs to them of cash transactions in terms of carry costs (incl. security etc..) are higher than the cost of the surcharge fee. So if I think they are taking the piss, I attempt to 'punish'. Hehe

Is it just me or is the ComCom finally starting to do its job?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.