Here is a thought experiment for those contemplating what to do when their fixed-rate home loan comes up for renewal.

The issue is this: The highest rates currently are for one year fixed, the lowest for three years (and longer).

Do you buy the idea that because rates will be coming down 'soon', it is better to go short now, so you can catch the even-lower rates coming when the Reserve Bank cuts the Official Cash Rate (OCR)?

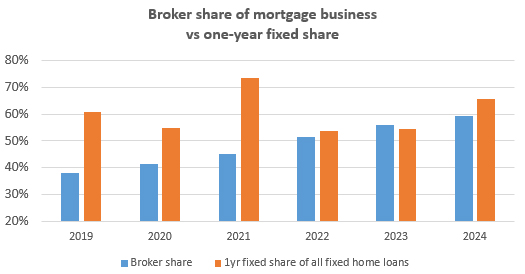

That seems to be what an increasing number of borrowers are doing. The one-year fixed term is now the most popular. Curiously, that has moved shorter as the proportion of deals done through mortgage brokers has risen.

But there are two issues here.

First, taking a 7.14% one year rate now, the lowest from a main bank, and forsaking a 6.35% three-year fixed rate, the lowest rate from any bank for any term at Heartland Bank, mean in a year rates will have to drop by 120 basis points just for the borrower to be even, and stay down. Even if they do, the uncertainty risk hardly seems worth it.

The numbers for a $500,000, 30 year mortgage are:

| Repayment | 1yr Fixed |

3 yrs Fixed |

||

| Year 1 | 7.14% | $40,861 | 6.35% | $37,695 |

| Year 2 needs to be | 5.95% | $36,112 | 6.35% | $37,695 |

| Year 3 needs to be | 5.95% | $36,112 | 6.35% | $37,695 |

| ---------- | ----------- | |||

| Total payments | $113,085 | $113,085 | ||

Possible, but risky. You are betting that the Reserve Bank has won its inflation battle in a year and has then cut the OCR by 25 basis points nearly five times.

And you are counting on the international influences on our interest rates not upsetting that expectation. Otherwise you would go for the lower and certain current three year fixed offer on the table now.

Secondly, there is the issue of the historical track record. And we can test that, and by bank.

If you have a $500,000 home loan due to roll over on July 1 this year, and you had chosen the lowest rate for any fixed term in the prior five years, this is what would have happened to your payments:

| Lowest rate available ... | |||||

| 1 yr | 2 yrs | 3 yrs | 4 yrs | 5 yrs | |

| 01-Jul-14 | 5.98% | 6.24% | 6.44% | 6.90% | 7.13% |

| 01-Jul-15 | 4.89% | 4.99% | 5.29% | 5.65% | 5.60% |

| 01-Jul-16 | 4.19% | 4.19% | 4.49% | 4.90% | 4.89% |

| 01-Jul-17 | 4.45% | 4.74% | 5.09% | 5.49% | 5.59% |

| 01-Jul-18 | 4.19% | 4.39% | 4.79% | 5.19% | 5.39% |

| 01-Jul-19 | 3.85% | 3.85% | 4.05% | 4.29% | 4.39% |

| 01-Jul-20 | 2.65% | 2.69% | 2.79% | 2.99% | 2.99% |

| 01-Jul-21 | 1.85% | 2.35% | 2.45% | 3.39% | 3.69% |

| 01-Jul-22 | 4.90% | 5.29% | 5.59% | 6.05% | 6.19% |

| 01-Jul-23 | 6.40% | 6.20% | 5.95% | 6.15% | 5.99% |

| from these banks ... | |||||

| 01-Jul-14 | multiple | multiple | multiple | multiple | multiple |

| 01-Jul-15 | ASB | multiple | BNZ | BNZ | Kiwibank |

| 01-Jul-16 | Kiwibank | BNZ | multiple | Kiwibank | Westpac |

| 01-Jul-17 | ASB | multiple | multiple | ASB | Westpac |

| 01-Jul-18 | Kiwibank | Kiwibank | ASB | Kiwibank | Kiwibank |

| 01-Jul-19 | multiple | multiple | multiple | Kiwibank | Kiwibank |

| 01-Jul-20 | multiple | multiple | Westpac | BNZ | multiple |

| 01-Jul-21 | Heartland | Heartland | Heartland | Kiwibank | Kiwibank |

| 01-Jul-22 | Heartland | Heartland | Heartland | Kiwibank | BNZ |

| 01-Jul-23 | Heartland | Heartland | Heartland | Kiwibank | Kiwibank |

| so the annual repayment cost was ... | |||||

| 01-Jul-14 | 36,262 | 37,247 | 35,358 | 36,714 | 40,807 |

| 01-Jul-15 | 32,119 | 37,247 | 33,609 | 36,714 | 40,807 |

| 01-Jul-16 | 29,586 | 29,586 | 33,609 | 32,156 | 40,807 |

| 01-Jul-17 | 30,515 | 29,586 | 33,609 | 32,156 | 40,807 |

| 01-Jul-18 | 29,586 | 30,300 | 31,751 | 32,156 | 40,807 |

| 01-Jul-19 | 28,391 | 30,300 | 31,751 | 32,156 | 30,300 |

| 01-Jul-20 | 24,369 | 24,498 | 31,751 | 25,477 | 30,300 |

| 01-Jul-21 | 21,867 | 24,498 | 23,730 | 25,477 | 30,300 |

| 01-Jul-22 | 32,156 | 33,609 | 23,730 | 25,477 | 30,300 |

| 01-Jul-23 | 37,893 | 33,609 | 23,730 | 25,477 | 30,300 |

| over ... | |||||

| five years | $144,676 | $146,513 | $134,692 | $134,063 | $151,499 |

| ten years | $302,743 | $310,479 | $302,628 | $303,958 | $355,534 |

| so the penalty over the lowest cost choice is ... | |||||

| five years | $10,613 | $12,451 | $630 | ... | $17,436 |

| ten years | $115 | $ 7,851 | ... | $1,330 | $52,906 |

The above table shows the costs per year in mortgage repayments by sticking to the same term and rolling over at that term.

But you can change when your fixed rate contract ends. The savings grow if you then choose the lowest rate available for any fixed term

For the past five years, you would have been better off choosing the BNZ four year 2.99% fixed rate than any other term from any other bank. The year before making that decision you would have been better off on the one year rate of 3.85% from one of ANZ, BNZ, or Kiwibank. Over the full five years you would have made payments of $130,299 using this "lowest current rate" strategy. That is a $14,377 saving over always going for the lowest one year fixed rate, and a $16,214 saving for always going for the lowest two year fixed rate.

If you extend the analysis to 10 years, a combination of one, two and three lowest rates worked best. It was the BNZ two year rate in 2016, followed by Kiwibank and others for one year options from July 2018 to July 2020, then Heartland Bank's three year rate from July 2021 onward. That combination of always choosing the lowest rate on offer for any term at the time you needed to make a decision would have cost $281,088 over these 10 years, far less than just sticking to the one year minimum rate, and you would have saved $21,655.

Of course, history is no guarantee that the future will repeat. But at least you should be aware of how this strategy played out over the recent past.

The shift in the market to one year fixed rates wasn't a smart choice, this hindsight analysis shows.* It is curious it came as the mortgage broking industry became dominant.

The other point to make is that mortgage brokers get their commissions from most banks, but not all. The best of the scenarios includes Heartland Bank over the last three years of the review. It is doubtful a mortgage broker would have recommended choosing a Heartland Bank mortgage, or even offering it as an option, because they don't pay brokerage. But from an individual homeowner's point of view, you clearly should include them in your assessment if you want to pay off your mortgage at the least cost.

Financial advice can be very useful when dealing with home loans. But that is undermined by the clear conflict of interest brokers have when they are being paid by banks - and they won't even offer options they don't earn brokerage on. Regulator-required "disclosures" are a pointless salve. What is really needed is a mandatory end to the financial conflict of interest.

You can find all current home loan interest rates here. And a full-function mortgage calculator here.

* This analysis compares rate options at the carded levels. Obviously those with good financials should be able to win a discount from carded rates. But be aware that Heartland Bank rates are unlikely to be discounted. Also, the availability of non-rate cash incentives will affect your final assessment as well. These come and go. You can find the current ones listed here. If you use all that cashback money to pay down your mortgage, that will affect your assessment too. Again, Heartland Bank has rarely offered cashbacks, if ever.

50 Comments

ANZ App Today

1yr = 6.85%

18mth = 6.69%

2yr = 6.75%

3yr = 6.65%

They’re offering better rates offline, like $6.39 for 3 years,

ASB (although it probably depends how much debt you have):

6mth = 6.89%

1yr = 6.85%

18mth = 6.62%

2yr = 6.59%

3/4/5yr = 6.39%

why not fix 6 months here.....

ASB on app

6 months 6.89%

12 - 6.85%

18 - 6.62%

24 - 6.59%

36+ - 6.39%

Oh that is identical to my offer (above).

I am finding it hard to choose between 6mth or 18mth. I'd probably have to fix at ~6.5% for a year after the 6 months to end up better than the 18 months. That is probably 2 OCR cuts worth. But there is more chance of deep regret with the 18mth IMO, if rates do come down quickly due to terrible recession. Maybe I should choose one then do the opposite as I always seem to get it wrong...

I think I will go 6 months as its only a portion of mine thats come up.

I am overpaying it and the 6 months gives me some flexibility as I am hoping for a work bonus to materialise in the coming months.

The other amounts have 2 and 3 years to run before coming up. But those rates are in the 5's, so I am not too concerned. The reason I fixed longer on those was I wanted some certainty and rates were on the rise at the time. So far its been ok as rates have been higher ever since. Whether that stays the same over the next few years....who knows?? ...if I did know I would be a billionaire trader haha.

Yes maybe I need to split mine into chunks again (we used to have that bit ended up paying off the smaller chunk very quickly). The other advantage of splitting with ASB is you can increase each of them by $500 a fortnight if your circumstances change.

Yeah thats what my thoughts are after we pay off this shorter term chunk....just switch the payments to the next one.....and keep on grinding!

Just advised my partner to go 6 months so she just locked it in for August. Unfortunately se didn't take my advice to go 5 years and went 3 years so now its costing an extra $60 a week. Still expecting a rate cut in August or November latest, either way rates should have dipped come Feb 2025.

Always worth frequently checking what the break fees are too. I’ve done this many times and mostly it’s $0 or something close to that.

Ive always threated to walk if the bank fee isn't waved. As of yet I have never paid a fee.

Please don't take this as a brag. Im just a beggar telling others where I have found bread.

Year 2 needs to be 5.95%

actually year two needs to be 5.85% to break even. as in scenario when you take 7.14% on year one, the year two starting principal will no longer be 500k (if it's not interest only).

the principal paid on year one needs to be taken into consideration. this is compounding interests working against mortgage holders....

Shots fired at mortgage brokers...

That's a relevant & timely article as I have a relative who had a house offer accepted on Sunday with a week to confirm finance (has preapproval but still needs to reconfirm on specific property). I was considering recommending not more than 1yr fixed & will now reconsider (mge loan is ANZ).

Why bother trying to guess what rates might do?

For a long term mortgage like 30 years, and probably 20 or even lower, the floating rate is the most efficient. Very few people would beat the market for the term of their mortgage.

However, for some reason in NZ, the banks add a huge premium on the floating rate. So the default is to spread the loan over every fixed term available and just keep rolling it over.

Most corporates run their term debt terms in a similar way.

If David had a good broker, he would know that no clients are being offered 7.14% fixed for 12 months currently. We are getting 6.85%, so when comparing that to the best 3 year rate in market of 6.35% then second two years would have to average out at 6.1% to break even which is realistic.

Would love to know why David has an axe to grind with Mortgage brokers. Every chance he gets he takes a shot, even when as in this case the stats he provides do not back up his points... "It is curious it came as the mortgage broking industry became dominant." 2021 Mortgage broker share 45%, 1 year fixed share 73%, 2024 Mortgage broker share 59%, 1 year fixed share 65%.

I am sure the FMA would say that Mortgage brokers who are not affiliated with Heartland Bank should not be providing any advice about their products or services. Would you do a home loan directly with the bank and expect them to provide you advice and suggest you go to another bank to get a better offer? I guess everyone working at the banks have a clear conflict of interest....

I guess everyone working at the banks have a clear conflict of interest....

Yes they do have an incredibly transparent conflict of interest..

As do advisers, we have to declare exactly how much we are paid by the banks... do car salespeople, your doctor, the bank staff... or yourself have to disclose what you earn to your clients?

Didn't say otherwise. You acknowledge the conflict of interest.. the other chap is denying it.

Where is the denial? Although in saying that, while we declare our commission structure and our conflicts of interest to clients. Bank commission is not classed as a conflict of interest according to our disclosures (dont shoot the messenger I didnt create the disclosure).

How much you make in commission is just one thing to declare. The really really interesting thing is how much it changes your advice.

DC, I'm not sure why you use 7.14% for the 1 year term, any bank will offer 6.85% right away. This changes your comparison significantly, when you conclude that the longer cheaper term saves the most money.

Presumably the advertised rate for the 3 year fix can also be negotiated down though..?

"Presumably" ? It would be nice if you could reply with an equally precise reply and give us an exact lower 3 year term to the one DC, mentions. I can't see one, but I'm happy for you to prove me wrong.

DC is using the published rates. Pretty logical.

It stands to reason that if you can negotiate one of these rates down, then you can negotiate any of them down.

Maybe that's not in fact true. I'm not claiming to know. If you say that its possible to get lower than the 1 year carded rate but impossible over any of the other terms, I'll accept that.

Stands to reason however not the case currently. While banks discounting their advertised short term rates they are not discounting the longer rates below the advertised 6.39 that westpac is advertising.

Really great analysis.

Just got 1% as wanted an extra heatpump and double glazing. Used the money to pay for these to pay off the mortgage and got a 1% mortgage top up to pay for the work.

Why is everybody thinking that lowering the OCR would mean lower interest rates? See what happened with the 3 M/6 M German Bund after the ECB lowered their rates last week. Barely any downside movement!

See: https://tradingeconomics.com/germany/3-month-bill-yield

and: https://tradingeconomics.com/germany/6-month-bill-yield

The bond markets are in charge; Not the central bankers.

When RBNZ eventually realises that it has overcooked the OCR, interest rates will be coming down by much more and much quicker than people are currently expecting. Adrian Orr massively over-corrected during Covid, so it shouldn’t surprise anyone that he is over-correcting again now.

Poor old David letting his personal hatred of advisers get in the way of a semi-decent story.... it's not just about the interest rate David, if you consider yourself such an expert on the topic that you feel the need to write articles then you should know that. As an aside, every client that I have had that went to Heartland Bank came back to me as they either didn't get any response from them or were declined with no explanation as to why

Bit harsh on DC. This is good info.

Whenever there is a potential commission involved some of those who will receive it are going to compromise themselves. Especially if there is a third party offering a larger commission to an advisor. That certainly happened during the Finance Companies debacle. Taking advisors up to Auckland, wining and dining them and offering a bigger commission than the other companies was too much temptation for some advisors. All undisclosed to trusting clients of course. Insurance is rife with brokers getting into bed with certain companies who have offered brokers better commissions.

Lawyers too

Yes I completely agree, the incentivising to advisers was wrong and has now stopped (as far as I can see anyway), if a bank hosts an update session for advisers these days there normally isn't even coffee offered lol

Far from "hating advisers", my view is the opposite. Good professional independent financial advice is crucial for a properly functioning financial system. Many users of that system are ill-prepared to deal with the professional banks and other institutions. It is crucial that independent and professional financial advice is available to them.

What I do find unacceptable is that the current setup has these 'advisers' working for the banks because they are paid by the banks. I know, the FMA has all these rules on disclosure and fiduciary responsibility to the 'client'. But when the banks are the ones paying the advisers, I think it will be forever compromised by the obvious conflict of interest. As I have pointed out before, other countries have outlawed the conflict. And any independent investigation done locally has recommended that the same restrictions should be applied here. The fact that no politician has taken up those recommendations just goes to the heart of the matter - money talks.

I say good professional independent financial advice is crucial. But it will only meet that test when the money-flows for that advice are from client-to-adviser. (I do understand why mortgage brokers resist, and vehemently. But that does not make it right.)

And for the record, the issue is not just related to mortgage brokers. The insurance 'advice' sector is conflicted in a far deeper way.

No one person or firm in the industry can change the current 'model' on their own. It must be a change driven by the regulator(s), the same standard for all.

Is it legal in NZ for brokers to offer financial advice outside of the mortgage itself?

I regularly see brokers online trying to pursuade people into making purchases using outdated truisms and platitudes.

Of course when someones livelihood depends on a person borrowing, there advice will always be to borrow. There is an obvious distinction between advice on the how of borrowing vs advice on the decision to borrow in the first instance, influencing a person to take on mountains of debt with one-sided advice for personal financial gain is hugely immoral in my opinion.

I am not implying that all brokers do this.

It depends on what the adviser is accredited to give advice on, it's not uncommon for an adviser to be accredited to give advice on all strands of advice (mortgages, investments, risk insurance and general insurance). But yes I agree there are a lot of snake oil salespeople out there now and some of their advertising is very borderline

Using the word “hate” was a tad extreme. David is just stating the obvious. People tend to be loyal to those who pay them. It’s human nature. If people wanting finance want a totally independent broker they should pay the broker a fee from the cash contribution the bank gives them. Of course we won’t. It’s free if the bank pays.

David has shown in previous articles that he has a strong dislike of advisers (he can't even bring himself to use the term adviser). I think what people don't understand is that in our community there are tens of thousands of people that have no idea how to 1. get in the position to buy a home 2. Get approved to buy and 3. How to manage that new loan. I spend 90% of my time educating people about all of those aspects and a lot of those people don't even become clients (not initially anyway). In reality, the actual loan approval process is generally very straightforward, it's educating about the buying process and managing the loan afterwards that are the key issues for most home buyers, most people are too busy dealing with life to spend too much time thinking about their mortgage. If the banks are willing to contract out that service to advisers so that the clients don't have to pay for that additional service then that is a win-win for everyone involved

In the mortgage advice world, the conflict of interest is very minimal as the banks all basically pay the same once you break it all down so it really comes down to what is right for the client. In saying that yes there are dogs in our industry (just like every other industry) that are in it for themselves but I would argue that the vast majority of advisers are in the game for the right reasons and that is to get the best outcome for people looking to borrow funds from huge banks that only have one group of people to look after... and that ain't the clients

I just consulted this article and comments as I was waiting to speak to ANZ for refixing mortgage. I asked what ANZ could offer for 1 year and we have just refixed at 6.85% for 1 year and decreased the term of our loan by another 2 years. We are attacking the mortgage but also want to have a little bit of a life, as I have had cancer. I would never have asked what they will offer before and would have fixed at 7.14% as per their website.

Thanks Team.

Good for you Gracey. It's always worth haggling.

It's a legitimate strategy, however it's still guesswork. It's been interesting when the SBS 5.99% 3YR special came out as many advisers jumped on that to offer that to clients. Since then SBS has closed up that offer having it open for a very short time. What that did though was bring others such as Westpac and BNZ down to 6.39%. Using that same contrast strategy, there has been some more adoption of that 3YR rate, albeit not entirely.

It's the same rationale why the 2.99% for 5YR wasn't an obvious choice at the time as all the official guidance from RBNZ, Economists as well as Interest.co.nz analysis showed interest rates weren't likely to triple.

To eliminate guesswork, a more effective strategy is a split rate one - the contrast strategy can be helpful to put more or less weighting to any given rate though.

Some issues with the analysis was you were going of advertised interest rates not the actual ones. Advertised interest rates sometimes reflect reality, but usually they don't. As others have pointed out, the market is comfortably sitting at 6.85% for 1YR while the advertised rate is north of 7% for most banks. It's been like that almost all year!

Another factor missing was cashback offers and product range. Heartland competes on rate, but when looking at the full picture they are remarkably similar to the competition. As a result they've had a cautious approach to entering into the adviser market as the likes of SBS,TSB,KB have had capacity issues dealing with adviser business. Love them or hate them, but the big banks have a bit more resources and systems behind them to capture that demand. Also need to take into account lending policy, and overall offering. It's not as black and white as you see it David.

I think this is now the 3rd article in a row you've been making the assertion that MA's are incentivised by commission alone? It's already been well evidenced that's not the case yet you're still pushing for that to somehow be true? Would be a good idea to go and interview several high profile MA's and see how they run their businesses, and how they select a lender. You may be pleasantly surprised that the split of business is actually very broad!

Let's throw some numbers out, and back them up with other numbers. It's all a guessing game. Eventually the guess will be right, but at what cost?

Just as 3 years ago when everyone was saying interest rates would go negative, which was why BNZ were willing to offer 2.99%. They didn't though, did they?

Of course, everyone that took that rate has been killing it. And would be doing even better if they kept their repayments at the level required for current floating rates. That is, repay as if you were on 8.69%, then when that fixed rate expires and you have to refix at 5.5% ~ 6.5%, at least you would have paid down a greater portion of the debt, so the interest shock won't be so bad.

At the end of the day, you got to do what you can afford, but perhaps spread your risk? Take 50% at 1 year fixed and 50% at 3 year fixed.

I've recently been made redundant due to corporate cost cutting, but because I was paying more per month for my home loans, I am able to reduce those back to minimum, plus cut out my luxury spending, so that my savings will last a few more months longer, giving me a bit more time to secure new employment.

How do you repay as if at 8.69 without hitting early repayment penalties

"For the past five years, you would have been better off choosing the BNZ four year 2.99% fixed rate than any other term from any other bank."

Wouldn't it have been been even better to have chosen the Westpac(and others) five year 2.99 fixed rate rate? Surely five years beats four years in the current environment.

Have my loan split into 5 lots, 20% comes out every 12 months. Average rate is 4.05 % Just took 5 years at 6.39% for 20%

Congratulations to David Chaston.

So good to see such an analysis. You know it's money and about the numbers. Yet so often we don't see the simple math.

As for the offended advisors. This is actually the advice you should be offering. Maybe print Davids article and hang in on the wall. 2400x1200 would be a good size.

And get a rate quote from all the banks - all - and present all to your client.

1 year rates, if it is still the same as when I was in banking, have a lower margin on top of the underlying swap rate. In short, as long as the market prices correctly then the 1 year rate will on average be cheaper.

I can't be bothered doing the calcs but from this recent article it still looks to hold true: (margins higher for longer tenors.) https://www.interest.co.nz/banking/125282/looking-wholesale-interest-rates-there-are-signs-we-may-be-peak-rate-about-now

This article really misses the point and is misleading. His table is only from 2014 and clearly shows the 1 year rate being lower right up until 2021-2022. Guess what happened then? Huge increase in OCR that was NOT priced into the 3 year rate he lock in July 2021... https://www.interest.co.nz/charts/interest-rates/ocr

The only reasons to lock in over or under the 1yr are:

-

possibility of early repayment

-

interest rate certainty is more valuable to you than paying a lower average rate

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.