This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

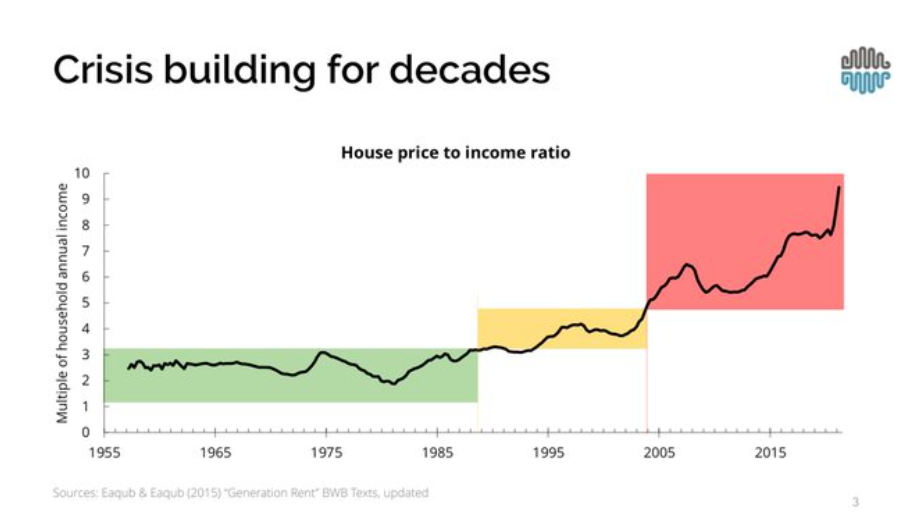

Chart: Shamubeel Eaqub, Sense Partners.

1) Open sourcing Covid-19 vaccine technology.

Writing for DCReport, Dean Baker argues more needs to be done to vaccinate people against Covid-19 in the developing world to help prevent more strains of the virus developing. Baker suggests open sourcing technology in order to boost vaccine production.

This would mean posting the details of the manufacturing process on the web, so that engineers all over the world could benefit from them. Ideally, the engineers from the pharmaceutical companies would also be available to do webinars and even in-person visits to factories around the world, with the goal of assisting them in getting their facilities up-to-speed as quickly as possible.

He goes on to look at whether governments can force companies to disclose information, and offers solutions to get around such issues.

As a legal matter, governments probably cannot force a company to disclose information that it chooses to keep secret. However, governments can offer to pay companies to share this information. This could mean, for example, that the U.S. government (or some set of rich country governments) offers Pfizer $1-$2 billion to fully open-source its manufacturing technology.

Suppose Pfizer and the other manufacturers refuse reasonable offers. There is another recourse. The governments can make their offers directly to the company’s engineers who have developed the technology. They can offer the engineers say $1-$2 million a month for making their knowledge available to the world.

This sharing would almost certainly violate the non-disclosure agreements these engineers have signed with their employers. The companies would almost certainly sue engineers for making public disclosures of protected information. Governments can offer to cover all legal expenses and any settlements or penalties that they faced as a result of the disclosure.

The key point is that we want the information available as soon as possible. We can worry about the proper level of compensation later. This again gets back to whether we see the pandemic as a real emergency.

Wonder when insurance companies start adding surcharges for people that choose not to be vaccinated (like they do for smokers).

— ian bremmer (@ianbremmer) July 28, 2021

In last week's Top 5 I included an update to the 1972 book Limits to Growth from KPMG director Gaya Herrington. In an interview with The Guardian Herrington talks about why she undertook the update.

“From a research perspective, I felt a data check of a decades-old model against empirical observations would be an interesting exercise,” said Herrington, a sustainability analyst at the accounting giant KPMG that recently described greenhouse gas emissions as a “shared, existential challenge.”

“The MIT scientists said we needed to act now to achieve a smooth transition and avoid costs,” Herrington told the Guardian this week. “That didn’t happen, so we’re seeing the impact of climate change.”

Since its publication, The Limits to Growth has sold upwards of 30m copies. It was published just four years after Paul Ehrlich’s Population Bomb that forewarned of an imminent population collapse. With MIT offering analysis and the other full of doom-laden predictions, both helped to fuel the era’s environmental movements, from Greenpeace to Earth First!.

Herrington, 39, says she undertook the update (available on the KPMG website and credited to its publisher, the Yale Journal of Industrial Ecology) independently “out of pure curiosity about data accuracy”. Her findings were bleak: current data aligns well with the 1970s analysis that showed economic growth could end at the end of the current decade and collapse come about 10 years later (in worst case scenarios).

The timing of Herrington’s paper, as world economies grapple with the impact of the pandemic, is highly prescient as governments largely look to return economies to business-as-usual growth, despite loud warnings that continuing economic growth is incompatible with sustainability.

Herrington says her key motivation is for the wellbeing of future generations. She wants the kids to be OK. And she expresses some optimism that they can be. If we act.

“The key finding of my study is that we still have a choice to align with a scenario that does not end in collapse. With innovation in business, along with new developments by governments and civil society, continuing to update the model provides another perspective on the challenges and opportunities we have to create a more sustainable world.”

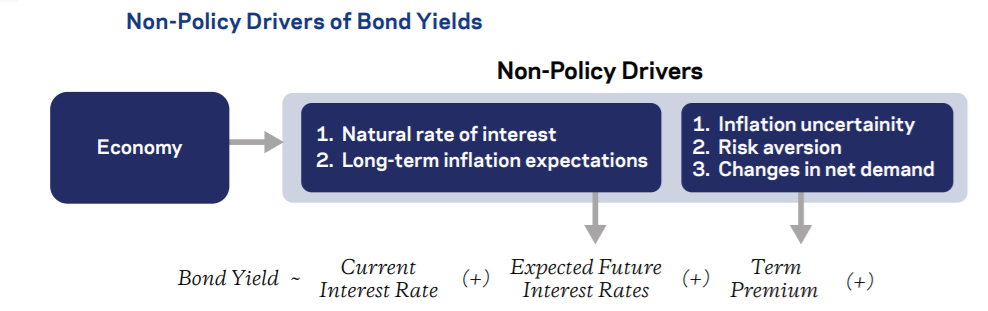

Jordan Brooks of global investment management firm AQR has published a detailed look at what determines the level of government bond yields and what drives their moves over time. It's a worthwhile read for those wanting to understand more about bonds.

My starting point is an identity: the yield on a bond is equal to the average expected interest rate over the life of the bond plus a term premium. (Throughout this paper I will use “yield” to mean the yield on a long-maturity bond – i.e., greater than three-month – and “interest rate” to mean the three-month T-bill rate.) Bond yields, therefore, depend on three factors: the current interest rate, expected future interest rates, and the term premium.

Bond yields and interest rates are familiar concepts, and “expected future interest rates” is intuitive to grasp. The “term premium,” however, may be less familiar. Definitionally, the term premium is the difference between the yield on a bond and the market’s expectation of future interest rates over the life of the bond. Hence, it embeds everything impacting the yield other than current and expected future interest rates. Another interpretation, however, is often more useful: the term premium measures the expected excess return investors require to hold to maturity a long-maturity bond versus rolling over a series of short-maturity bonds.

Cutting to the chase, here's Brooks' conclusion.

By decomposing longer-maturity bond yields into the current interest rate, expected future interest rates and term premia, and analyzing the drivers of each component, I’ve presented a framework for understanding the determinants of bond yields, and identified several of their fundamental drivers. Through the systematic response of monetary policy, the near-term outlook for economic activity and inflation influence bond yields. Unexpected monetary policy changes – to the current interest rate, the expected path of future interest rates (i.e., changes in forward guidance), and the size and complexion of the central bank’s balance sheet (i.e., change in QE policies) – influence yields as well. Non-monetary policy drivers are also critical, particularly at longer maturities. Indeed, declining estimates of the natural rate of interest, in part driven by a pessimistic outlook for trend growth, and falling long-term inflation expectations are important factors behind the secular decline in bond yields over the past few decades, and provide the backdrop for the extremely low yield levels we observe today.

Looking towards the future, investors would be prudent to conclude government bond risk remains two-sided even at low levels of bond yields, and a fundamentally driven approach to bond market investing remains viable.

4) US Department of Justice puts spotlight on Tether.

The US Justice Department is investigating whether executives behind the stablecoin Tether, which is widely used to trade Bitcoin, committed bank fraud, Bloomberg reports. The investigation is apparently probing back several years, and looking at whether Tether concealed from banks that transactions were linked to crypto.

Criminal charges would mark one of the most significant developments in the U.S. government’s crackdown on virtual currencies. That’s because Tether is by far the most popular stablecoin -- tokens designed to be immune to wild price swings, making them ideal for buying and selling more volatile coins. The token’s importance to the market is clear: Tethers in circulation are worth about $62 billion and they underpin more than half of all Bitcoin trades.

Bloomberg notes that Tether was first issued in 2014 as a solution to a problem plaguing the crypto market. That is banks didn’t want to open accounts for virtual-currency exchanges because they were worried about encountering funds tied to drug trafficking, cyberattacks and terrorism. But by accepting Tether, exchanges could give traders a way to park their balances without being exposed to Bitcoin’s price gyrations, Bloomberg says. Furthermore, funds could be transferred instantaneously from exchange to exchange.

A hallmark of Tether is that its creators have said each token is backed by one U.S. dollar, either through actual money or holdings that include commercial paper, corporate bonds and precious metals. That has triggered concerns that if lots of traders sold stable coins all at once, there could be a run on assets backstopping the tokens. Fitch Ratings has warned that such a scenario could destabilize short-term credit markets.

5) Diversifying the Dismal Science.

Writing for Project Syndicate, Northeastern University associate professor Alicia Sasser Modestino argues by discriminating against women and minority groups, the economics profession perpetuates a hidden bias in data collection and analysis featuring in important areas of policymaking. It should be clear by now, she says, that market forces alone won't solve the profession's diversity problem.

Why has the economics discipline failed to diversify its membership? The simple reason is that economists tend to rely on market forces to solve most problems – including discrimination. The late Nobel laureate economist Gary S. Becker’s model of discrimination asserts that employers who discriminate based on factors unrelated to productivity – such as gender or race – will incur monetary costs (by paying higher wages, for example). In a competitive labor market, non-discriminatory employers do not pay this cost and should therefore drive the discriminatory employers out of business.

This model makes many economists wary of analyses that ascribe wage differences across gender and racial groups to discrimination. Instead, they look to other possible causes, such as differences in educational attainment or occupational choice – often failing to recognize that these also might stem from discriminatory practices.

The emerging literature highlighting gender differences within economics is no exception. Earlier research showed that female economists are less likely to be promoted. But only with subsequent studies showing that women also receive less credit than their male co-authors, are more likely to have their work rejected by scholarly journals, and are systematically trivialized in online forums has the profession acknowledged its “gender problem.”

Cartoon: Matt Wuerker, Politico.

11 Comments

My issue with all of these economic and societal collapse predictions is that they've been forecast so frequently throughout history and not yet come to fruition. We seem magnetically drawn to forecasts of decline and end-times but historically these events are extremely rare. Even for those that do the process is rarely so rapid as to happen within one lifespan. We should view all of these predictions with due skepticism.

There is actually an excellent podcast series on several of the historic Civilisations that did "fall" available free here: https://youtu.be/glKe9njOB24

No Empire has survived, though the sites have sometimes been re-used when other energy/resource stocks have been found.

The problem now is the magnitude of the overshoot - both population and consumption (two sides of the one coin). What happens is that the resudual supporting energy/resources get swallowed up in a jiffy, Seneca applies, goodnight. We climbed higher and higher on the ladder, kicking out the rungs every time.

Writing for DCReport, Dean Baker argues more needs to be done to vaccinate people against Covid-19 in the developing world to help prevent more strains of the virus developing. Baker suggests open sourcing technology in order to boost vaccine production.

Well this is exactly what the makers of the Oxford vaccine, now called Astra Zeneca, were planning on doing.

Bill Gates got in contact with them and advised them what a terrible idea it was - basically vaccines for humans need to have strict quality controls, because if a bad batch of vaccines gets out it will destroy confidence in all vaccines, not just the one with the bad batch. So it wasn't feasible to simply open source the vaccine and let any bob, dick or harry produce a COVID vaccine and put it out into the wild.

Thus the Oxford researchers teamed up with Astra Zeneca. This is also how the conspiracy theory that Bill Gates wanted to plant microchips in everyone got started - why else would he have intervened to stop the oxford vaccine from being open-sourced, and instead pulled strings with his foundation to get big pharma involved in the production?

Great cartoon, pretty much puts into a picture what I said yesterday.

They should develop the vaccine in fine powder form, so people can be sprayed on and be done with. Quick immunity for the world.

Repeat ignore pls.

Repeat ignore pls

Tether is a fraud. They became a key provider of liquidity in the crypto world by guaranteeing they were backed 1-1 by $USD. It was always and remains a complete lie. This is not slander, it's something that has been proven in court. The undisputed facts of how they lied to investors and used a now-jailed money-laundering mob to do their banking are extraordinary. They invented huge amounts of Tether, exchanged it for Bitcoin, and thereby pushed the BTC price up beyond where it would have been driven by organic demand. The current spike in BTC is most likely the result of crypto holders fleeing Tether (and the Binance exchange, which also seems to be in regulatory trouble).

I think journalists do the public a disservice if they don't use strong and accurate language to describe ongoing and enormous frauds once they are proven to be fraudulent.

Backed 1:1 by the USD?

Pot meet kettle.

When was the last time the USD was 'backed'? Currently, they owe how much? Currently, it takes $3.50 US to 'generate' $1 of US GDP.

Good luck with that

Tether sure is dodgy.

They have updated their terms to say it is backed by "The breakdown states that the bulk of Tether’s reserves are in cash, equivalents or other short-term deposits, with the remainder in secured loans, corporate bonds and other investments. However, the first category is mostly made up of commercial paper, a form of corporate debt that can be easily converted to cash – or not, depending on the issuer and market conditions."

The problem is, with the supposed amount of commercial paper they hold/trade, they would be the largest player in the market, except no one has heard of them haha.

Tether does an amazing job for facilitating trades and allowing people to move into and out of crypto currencies to hedge volatility.

I think that it will eventually crash and burn, which will be like a MT Gox situation for the markets and may put it to sleep for a few years.

People will ditch their tether for other stable coins and Bitcoin, so price will go up a good bit, then dump.

It wont kill Bitcoin and will allow me to accumulate more at a cheaper price so bring it on.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.